5 big analyst AI moves: Apple lifted to Buy, AI chip bets reassessed

Introduction & Market Context

Moody’s Corporation (NYSE:MCO) delivered record quarterly results in Q3 2025, according to its earnings presentation released on October 22, 2025. The company reported unprecedented quarterly revenue exceeding $2 billion for the first time, representing an 11% year-over-year increase. Despite these strong results, Moody’s stock declined 1.63% in pre-market trading to $477, suggesting investors may have already priced in the positive performance.

The company’s robust performance comes amid a favorable debt issuance environment, with refinancing needs continuing to grow and spreads remaining at historically low levels. Moody’s has capitalized on these conditions while expanding its analytics offerings and improving operational efficiency.

Quarterly Performance Highlights

Moody’s Q3 2025 results demonstrated strong growth across key metrics, with both its Moody’s Investors Service (MIS) and Moody’s Analytics (MA) segments contributing to the record performance.

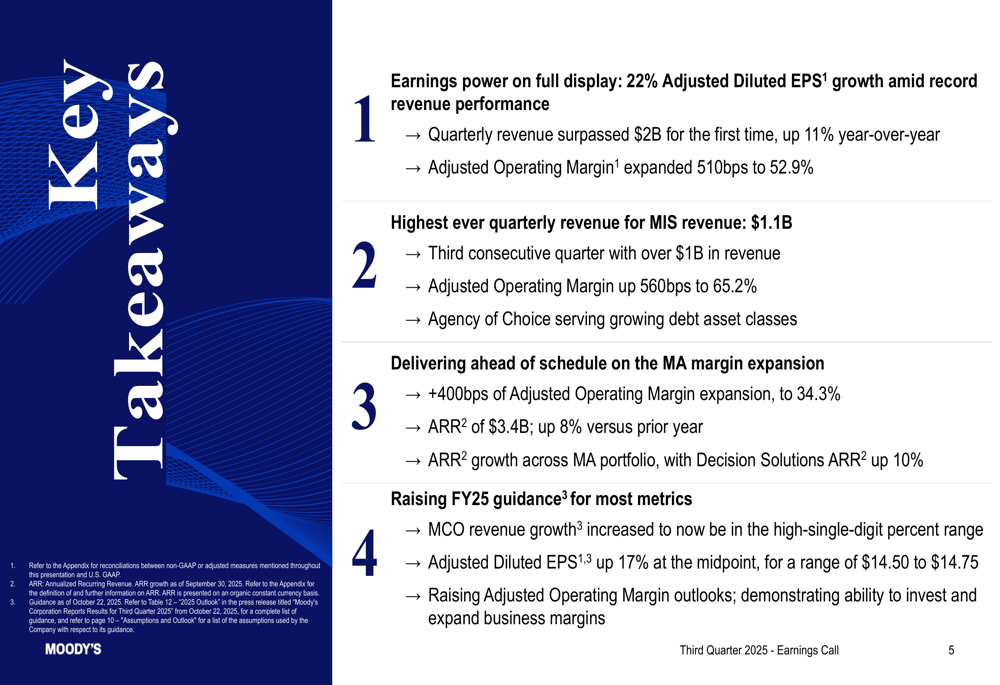

As shown in the following key takeaways slide, the company achieved 22% growth in Adjusted Diluted EPS while expanding its Adjusted Operating Margin by 510 basis points to 52.9%:

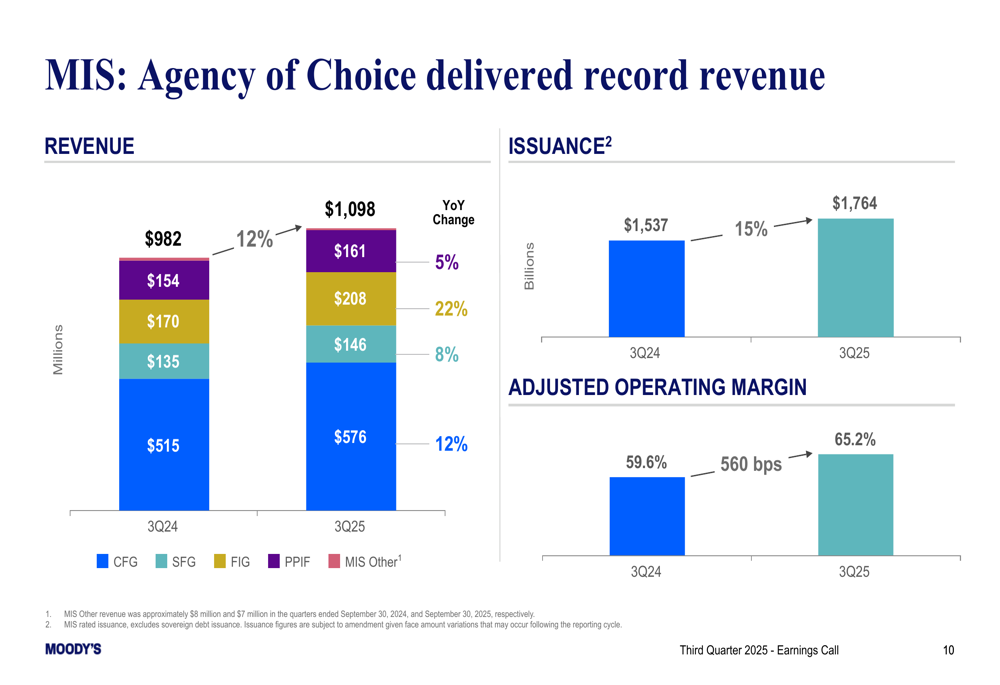

The ratings business (MIS) delivered particularly impressive results, with revenue reaching $1.1 billion, marking the third consecutive quarter exceeding $1 billion. MIS Adjusted Operating Margin expanded significantly by 560 basis points to 65.2%, reflecting the segment’s operating leverage and disciplined expense management.

The following slide details MIS’s record revenue performance across different segments, with Financial Institutions (FIG) showing the strongest year-over-year growth at 22%:

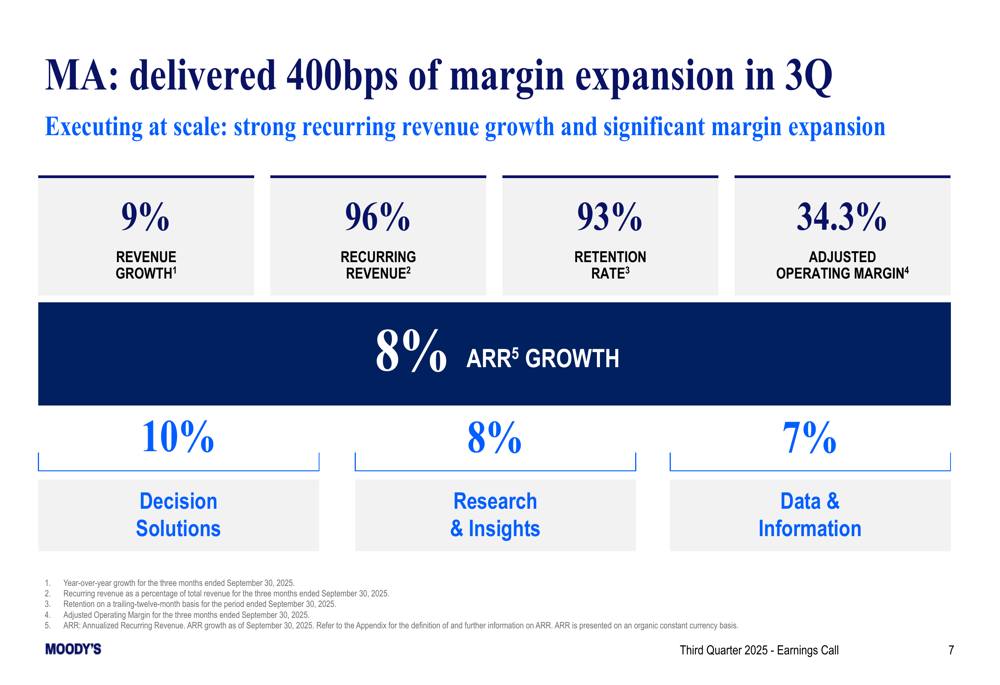

Meanwhile, Moody’s Analytics (MA) continued its steady growth trajectory with revenue increasing 9% and Annualized Recurring Revenue (ARR) growing 8% to $3.4 billion. The segment achieved substantial margin improvement, expanding its Adjusted Operating Margin by 400 basis points to 34.3%.

As illustrated in this slide, MA’s performance is built on a foundation of high recurring revenue (96%) and strong customer retention (93%):

Guidance Upgrades

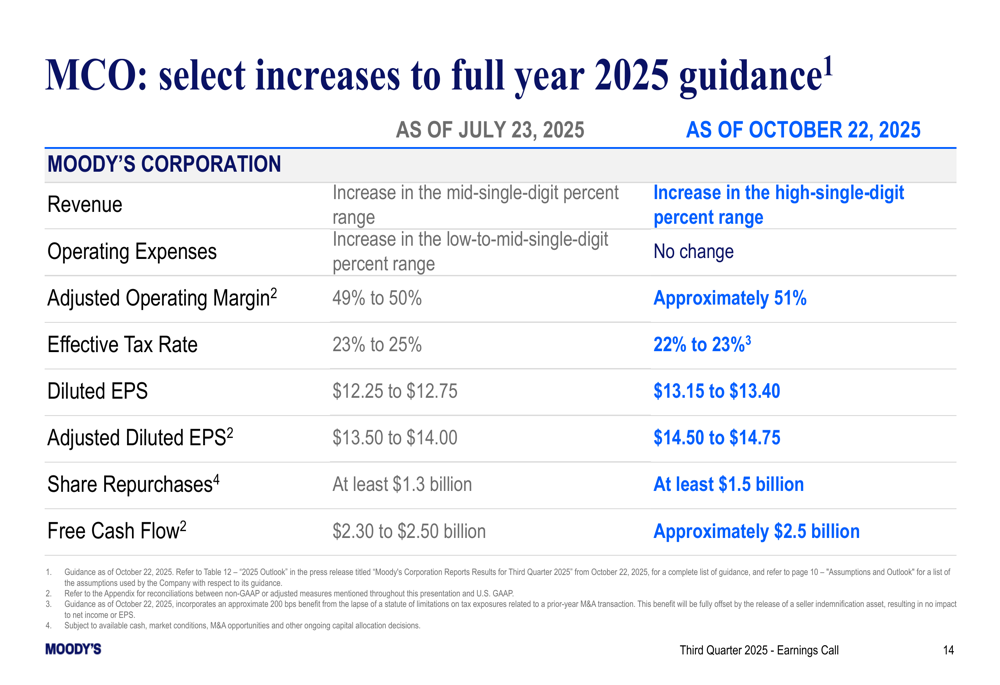

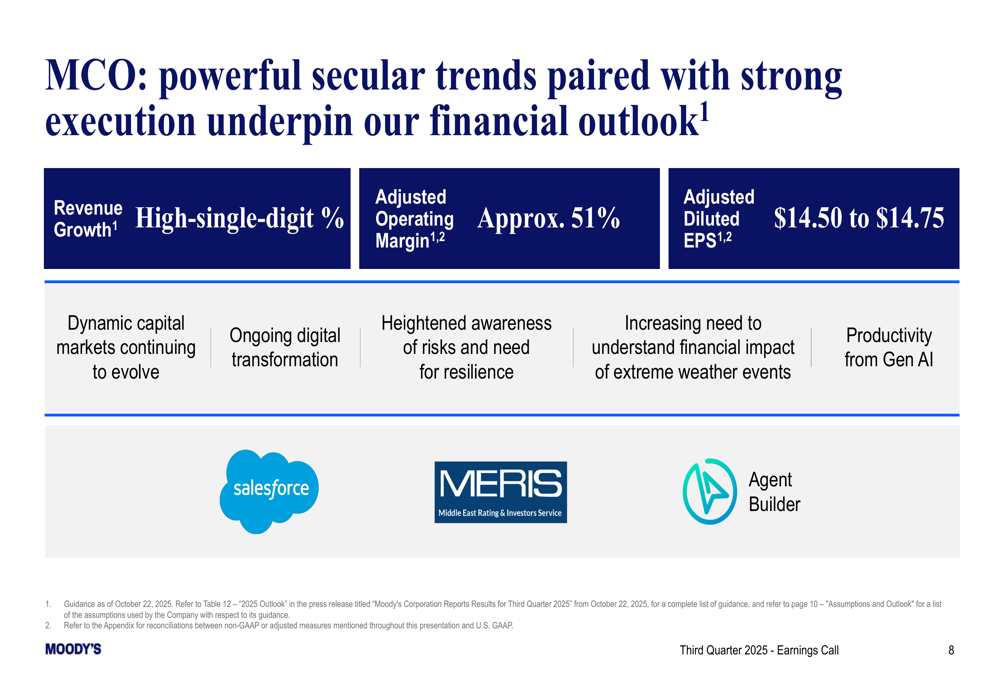

Based on the strong Q3 results and positive outlook, Moody’s has raised its full-year 2025 guidance across most metrics. The company now expects high-single-digit revenue growth for the full year, up from its previous mid-single-digit guidance.

The following slide details the specific increases to Moody’s full-year outlook:

Notably, Moody’s raised its Adjusted Diluted EPS guidance to $14.50-$14.75, representing 17% growth at the midpoint compared to the previous year. This exceeds the earlier guidance of $13.50-$14.00 provided in July. The company also increased its share repurchase target to at least $1.5 billion and raised its free cash flow guidance to approximately $2.5 billion.

Growth Drivers

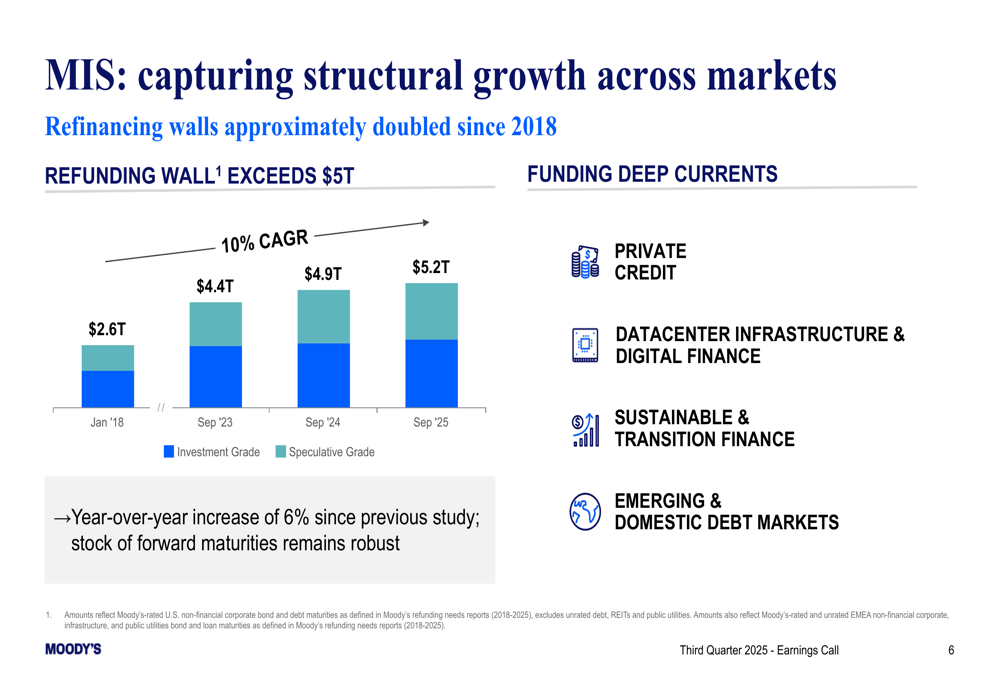

A key driver of Moody’s performance is the growing refinancing wall, which has approximately doubled since 2018 and now exceeds $5 trillion. This structural growth factor provides a solid foundation for future issuance activity.

As shown in the following slide, refinancing needs are expected to support robust issuance volumes in the coming years:

The company is also benefiting from several secular trends, including digital transformation, heightened risk awareness, and the increasing need to understand the financial impact of extreme weather events. Additionally, Moody’s is leveraging generative AI to enhance productivity and develop new solutions.

Strategic Positioning

Moody’s Analytics continues to build on its strong foundation of customer retention, with 93% of its base retained as of Q3 2025. The MA segment is seeing the strongest growth in its Decision Solutions business, where ARR increased 10% year-over-year.

The company’s strategic focus areas include expanding in private credit, datacenter infrastructure, digital finance, sustainable and transition finance, and emerging markets. These areas represent significant growth opportunities as global capital markets continue to evolve.

Moody’s long-term growth algorithm for MIS targets 6-9% revenue growth, driven by economic expansion (2-3%), value proposition (3-4%), and developing capital markets (1-2%). This balanced approach positions the company to deliver sustainable growth across different economic cycles.

Forward-Looking Statements

Looking ahead, Moody’s expects continued strong performance through the remainder of 2025, with several key macroeconomic assumptions underpinning its outlook. These include U.S. real GDP growth of 1.5-2.5%, two federal funds rate cuts in Q4, and a global high-yield default rate declining to around 3.7% by year-end.

As illustrated in this comprehensive outlook slide, Moody’s is positioning itself to capitalize on powerful secular trends while maintaining strong execution:

During the earnings call, CEO Rob Fauber highlighted the company’s record quarterly revenue and emphasized the transformative potential of AI, stating, "AI is really an unlock opportunity." The company’s focus on technological innovation, combined with its strong market position in both ratings and analytics, positions it well for continued growth.

While Moody’s presentation emphasizes the positive aspects of its performance and outlook, investors should also consider potential risks including macroeconomic pressures, market saturation in key segments, regulatory changes in emerging markets, foreign exchange fluctuations, and increasing competition in the analytics space.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.