S&P 500 struggles for direction as investor await inflation data

Introduction & Market Context

Motiva Infraestrutura de Mobilidade SA (B3:MOTV3) reported a substantial increase in profitability for the second quarter of 2025, with net profit soaring 235% year-over-year to R$897 million. Despite these impressive results, the company's stock closed at R$14.00, down 0.64% on the day, reflecting broader market concerns about future growth prospects.

The infrastructure mobility company, which operates across toll roads, railways, and airports in Brazil, has maintained its position in B3's Corporate Sustainability Index (ISE) for the 14th consecutive year, underscoring its commitment to sustainable business practices while delivering financial performance.

Quarterly Performance Highlights

Motiva's second quarter was characterized by significant margin expansion across all business platforms, driven by operational efficiency initiatives and strategic portfolio optimization.

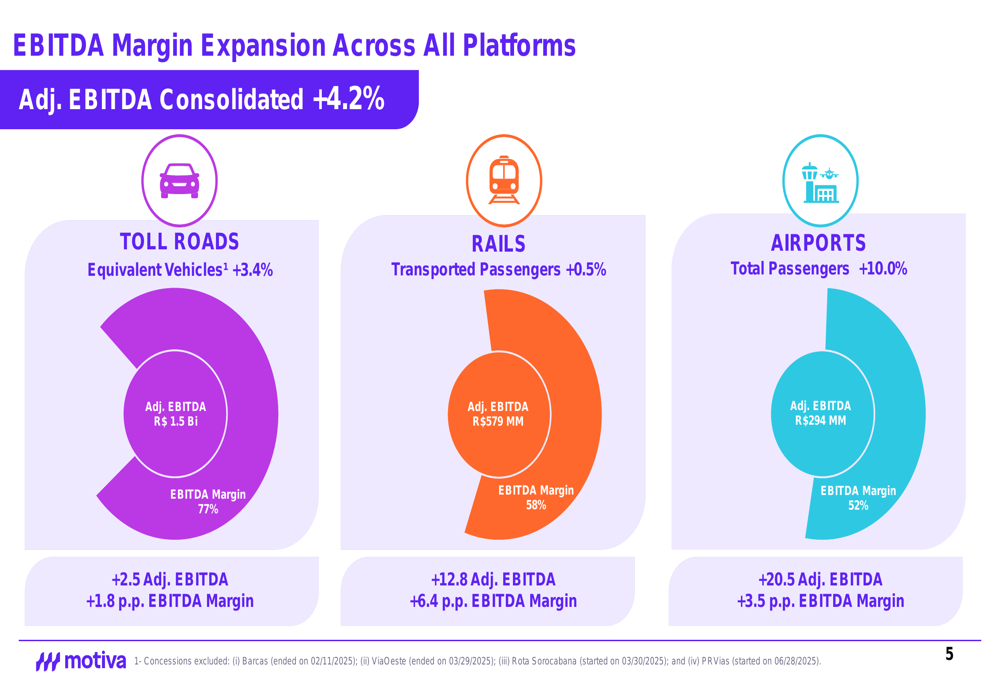

As shown in the following chart detailing EBITDA margin expansion across the company's business segments:

The company achieved a consolidated adjusted EBITDA increase of 4.2% compared to the same period last year. Most notably, the Rails segment demonstrated the strongest improvement with a 12.8% increase in adjusted EBITDA and a 6.4 percentage point expansion in EBITDA margin to 58%. The Airports segment also performed exceptionally well, with a 20.5% increase in adjusted EBITDA and a 3.5 percentage point improvement in EBITDA margin to 52%, supported by a 10% increase in total passengers.

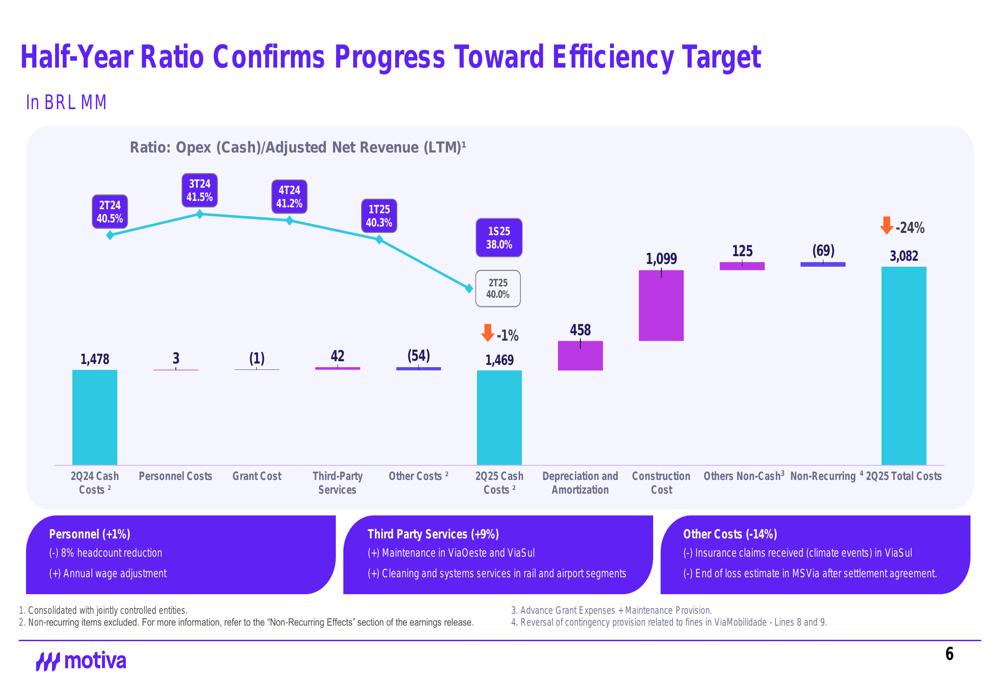

Motiva's aggressive cost-cutting measures have yielded significant results, as illustrated in this breakdown of cost reductions:

Total costs decreased by 24% year-over-year, with the company reducing its headcount by approximately 10% (around 1,700 positions) since December 2023. The Opex (Cash)/Adjusted Net Revenue ratio improved to 38% for the first half of 2025, demonstrating progress toward the company's efficiency targets.

Detailed Financial Analysis

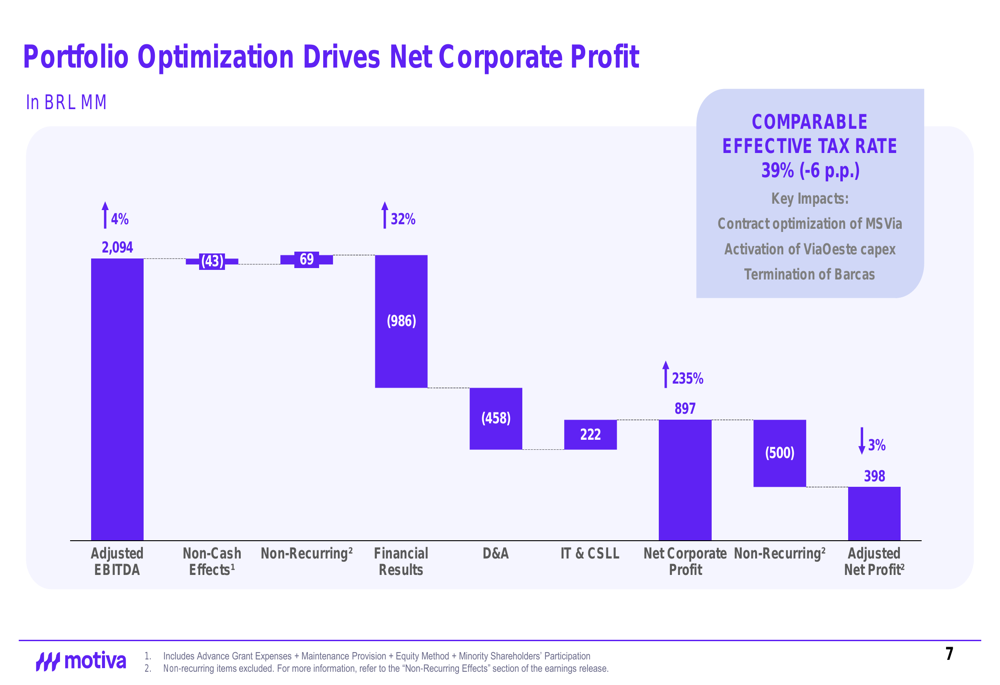

The dramatic improvement in Motiva's profitability can be attributed to several factors, as illustrated in this waterfall chart showing the progression from EBITDA to net profit:

Starting with an adjusted EBITDA of R$2,094 million (+4%), the company benefited from positive non-recurring effects of R$69 million and improved financial results (-32% in financial expenses). The effective tax rate decreased by 6 percentage points to 39%, primarily due to contract optimization at MSVia, activation of ViaOeste capex, and the termination of Barcas operations.

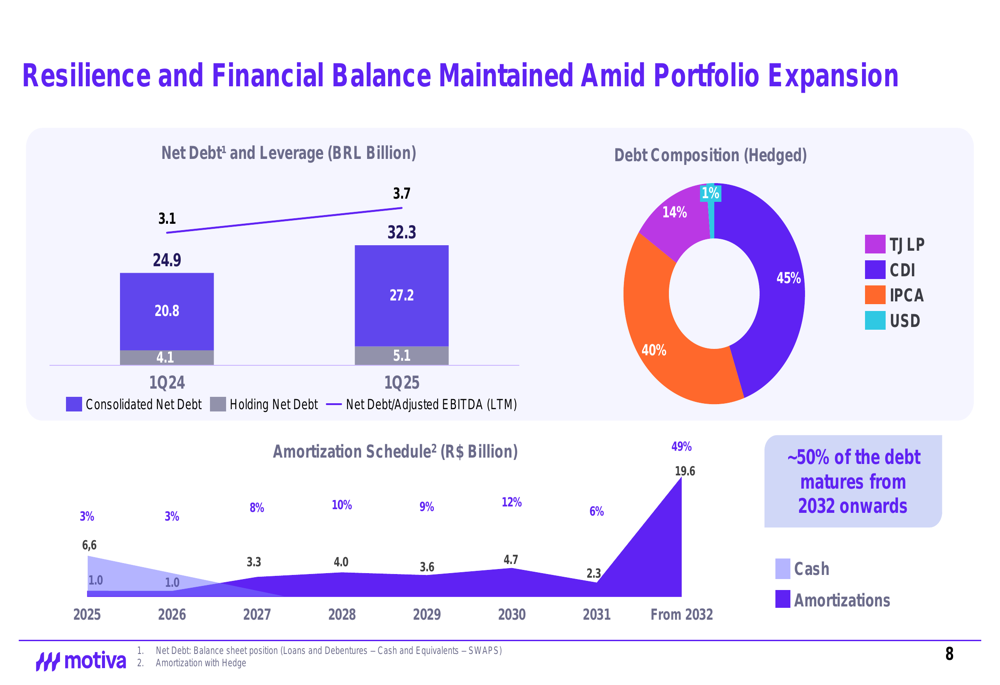

While maintaining its focus on profitability, Motiva has also managed its debt profile prudently:

The company's net debt increased to R$27.2 billion in Q1 2025 from R$20.8 billion in Q1 2024, with the leverage ratio (Net Debt/Adjusted EBITDA) rising to 3.7x from 3.1x. However, Motiva has structured its debt with a favorable maturity profile, with approximately 50% maturing from 2032 onwards, providing long-term financial stability. The debt composition is well-diversified, with 45% in USD, 40% in IPCA (inflation-indexed), 14% in CDI, and 1% in TJLP.

Strategic Initiatives

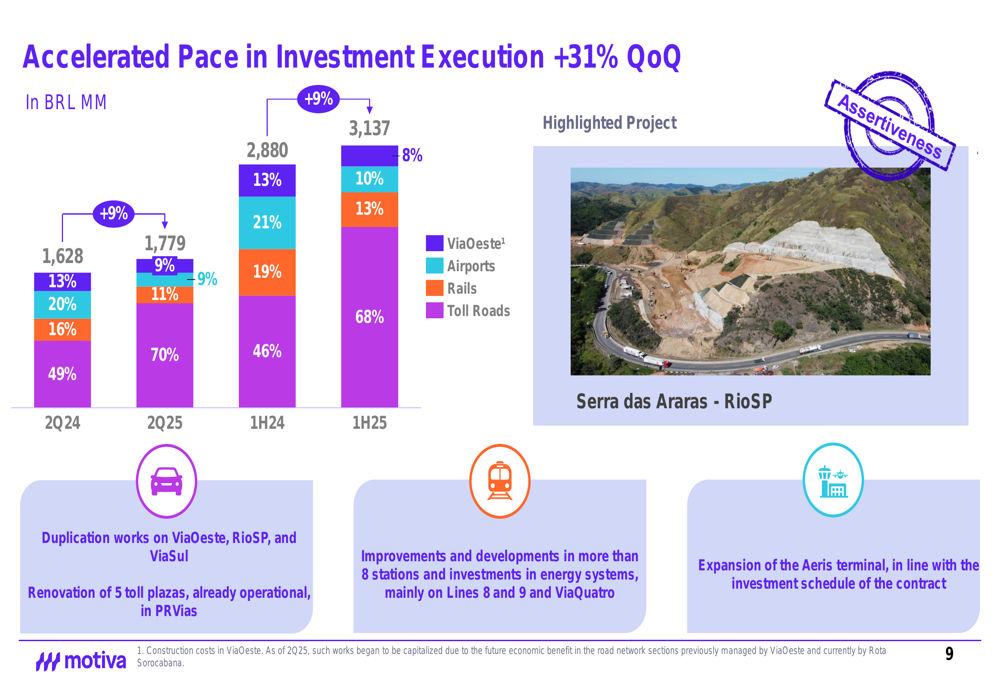

Motiva has accelerated its capital investment program, with quarterly capex increasing by 31% compared to the previous quarter:

The company invested R$1,779 million in Q2 2025, bringing the first-half total to R$3,137 million. These investments are strategically allocated across all business segments, including duplication works on ViaOeste, RioSP, and ViaSul, renovation of toll plazas in PRVias, improvements to railway stations, and terminal expansion at Aeris.

The company has also made significant progress on several strategic fronts, as highlighted in its quarterly summary:

Key achievements include the conclusion of the MSVia contract optimization, the start of new concessions (Sorocabana and PRVias), and the signing of an amendment for ETCS implementation on Lines 8 and 9. Additionally, Motiva executed a successful liability management operation that resulted in a gain of approximately R$320 million.

Forward-Looking Statements

Looking ahead, Motiva's management, led by CEO Miguel Setas, remains focused on operational efficiency and strategic portfolio optimization. The company's presentation emphasized continued progress toward its efficiency targets, with the Opex/Revenue ratio trending downward.

The accelerated pace of capital investments suggests confidence in future growth opportunities, particularly in the toll road and airport segments where traffic volumes have shown positive momentum (+3.4% in equivalent vehicles for toll roads and +10.0% in total passengers for airports).

While the increased leverage ratio bears monitoring, Motiva's well-structured debt profile with extended maturities provides financial flexibility. The company's consistent inclusion in B3's Corporate Sustainability Index also positions it favorably with ESG-focused investors.

As Motiva continues to optimize its portfolio and improve operational efficiency, investors will be watching closely to see if the remarkable profit growth can be sustained in coming quarters, particularly given the challenging macroeconomic environment in Brazil and the company's increasing debt levels.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.