German construction sector still in recession, civil engineering only bright spot

Introduction & Market Context

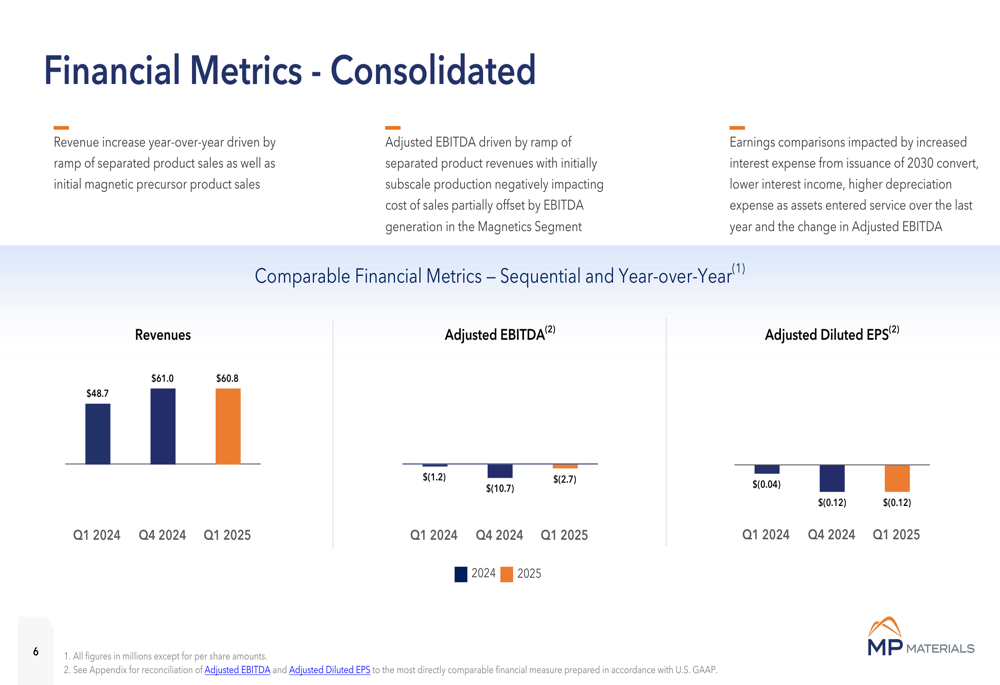

MP Materials Corp (NYSE:MP) presented its first quarter 2025 results on May 8, highlighting record production of NdPr oxide and the successful commercial launch of its new Magnetics segment. The rare earth materials producer reported revenue of $60.8 million, essentially flat compared to the $61.0 million in the previous quarter but up 24.8% year-over-year from $48.7 million.

The company’s stock closed at $23.62 on the day of the presentation, up 1.02% in regular trading, though it dipped slightly by 0.55% in after-hours trading. MP Materials has shown strong momentum in recent months, with its shares trading well above the 52-week low of $10.02, though still below the high of $29.72.

Quarterly Performance Highlights

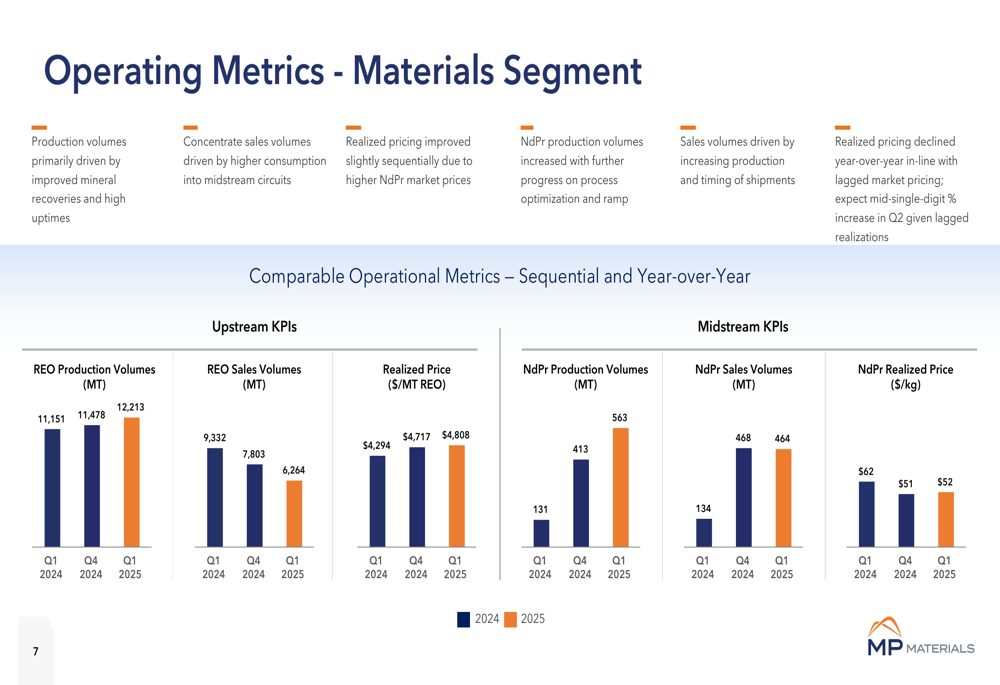

MP Materials achieved several operational milestones in Q1 2025, most notably a record NdPr oxide production of 563 metric tons, representing a substantial 36% sequential increase from Q4 2024 and more than quadruple the production level from the same period last year.

As shown in the following chart of key highlights from the quarter, the company also commenced commercial metal deliveries, generated its first meaningful revenue from the Magnetics segment, and initiated the General Motors (NYSE:GM) magnet validation process:

The company’s Adjusted EBITDA loss narrowed to $1.2 million, a significant improvement from the $10.7 million loss in Q1 2024 and better than the $2.7 million loss in Q4 2024. However, Adjusted Diluted EPS remained unchanged year-over-year at $(0.12), representing a decline from $(0.04) in the previous quarter.

The following chart illustrates the company’s consolidated financial performance trends:

Segment Analysis

Materials Segment

The Materials segment, which encompasses mining and processing operations, demonstrated strong operational execution with REO production reaching 12,213 metric tons in Q1 2025, up from 11,478 metric tons in Q4 2024 and 11,151 metric tons in Q1 2024. The company attributed this increase to improved mineral recoveries and high uptimes.

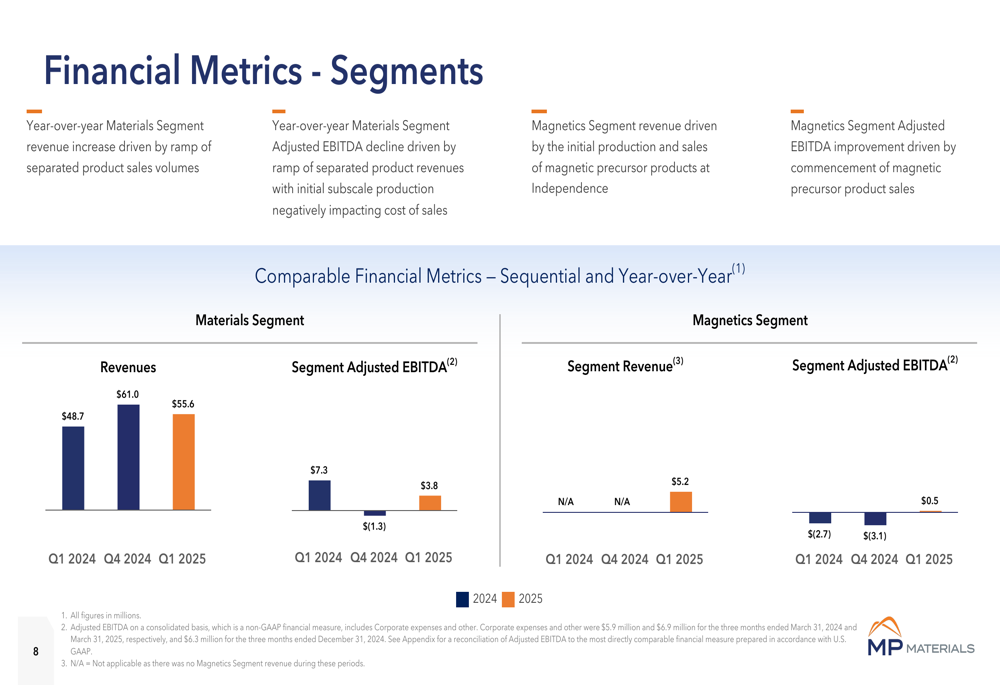

The segment generated $55.6 million in revenue, down slightly from $61.0 million in Q4 2024 but up from $48.7 million in Q1 2024. Segment Adjusted EBITDA improved to $3.8 million, compared to a loss of $1.3 million in the previous quarter.

The following chart details the operating metrics for the Materials segment:

A notable strategic shift was the company’s decision to cease sales of concentrate to China, focusing instead on higher-value separated products. This transition is part of MP Materials’ broader strategy to develop a fully integrated rare earth supply chain in the United States.

Magnetics Segment

The Magnetics segment marked a significant milestone by generating its first meaningful revenue of $5.2 million in Q1 2025 and achieving positive Adjusted EBITDA of $0.5 million. This represents a substantial improvement from the $3.1 million EBITDA loss in Q4 2024.

The following chart breaks down the financial performance by segment:

The company also received its third $50 million customer prepayment on April 1st, underscoring the commercial traction of its magnetics business. Commercial magnet production remains on track for year-end, with the GM magnet validation process now underway.

Strategic Initiatives and Outlook

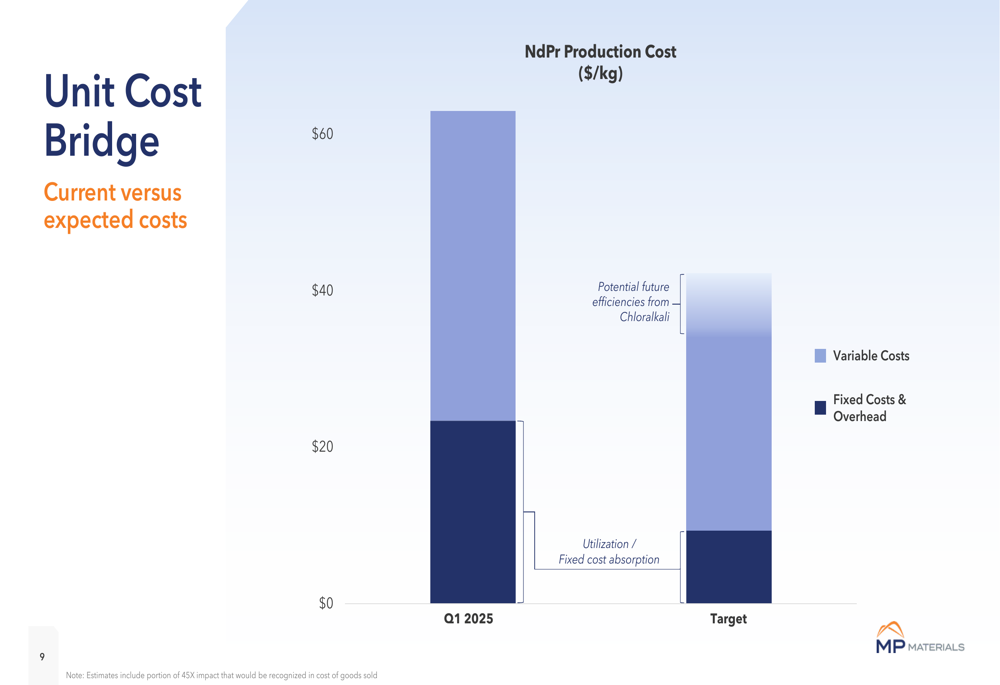

MP Materials continues to focus on optimizing its production costs for NdPr oxide. The company presented a unit cost bridge that illustrates the components of current production costs and the potential for future efficiencies:

The company’s strategic pivot from selling concentrate to producing higher-value separated products and magnetic materials represents a fundamental shift in its business model. This vertical integration strategy aims to capture more value from the rare earth supply chain and reduce dependence on Chinese processing.

Management highlighted "intensifying engagement from industry and government," suggesting growing recognition of the strategic importance of domestic rare earth production and processing capabilities.

Financial Analysis

MP Materials’ consolidated P&L shows a net loss of $22.6 million for Q1 2025, compared to a net income of $16.5 million in Q1 2024. This decline in profitability was primarily due to increased interest expense from the issuance of 2030 convertible notes, lower interest income, and higher depreciation expense as assets entered service over the last year.

Despite the net loss, the company’s improving Adjusted EBITDA trajectory suggests progress toward profitability as production scales and efficiencies are realized. The positive EBITDA contribution from the new Magnetics segment is particularly encouraging, as it validates the company’s vertical integration strategy.

The company’s focus on scaling magnet production and targeting gross margin profitability in NDPR production aligns with its long-term strategic objectives. With continued execution on its production ramp and cost optimization initiatives, MP Materials appears positioned to capitalize on growing demand for rare earth materials in critical applications such as electric vehicles, robotics, defense, and physical AI markets.

However, challenges remain, including fluctuating NDPR prices, potential inventory write-downs, and the uncertain impact of global trade policies and tariffs. The company’s success will depend on its ability to navigate these challenges while continuing to scale production and improve operational efficiency.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.