Two National Guard members shot near White House

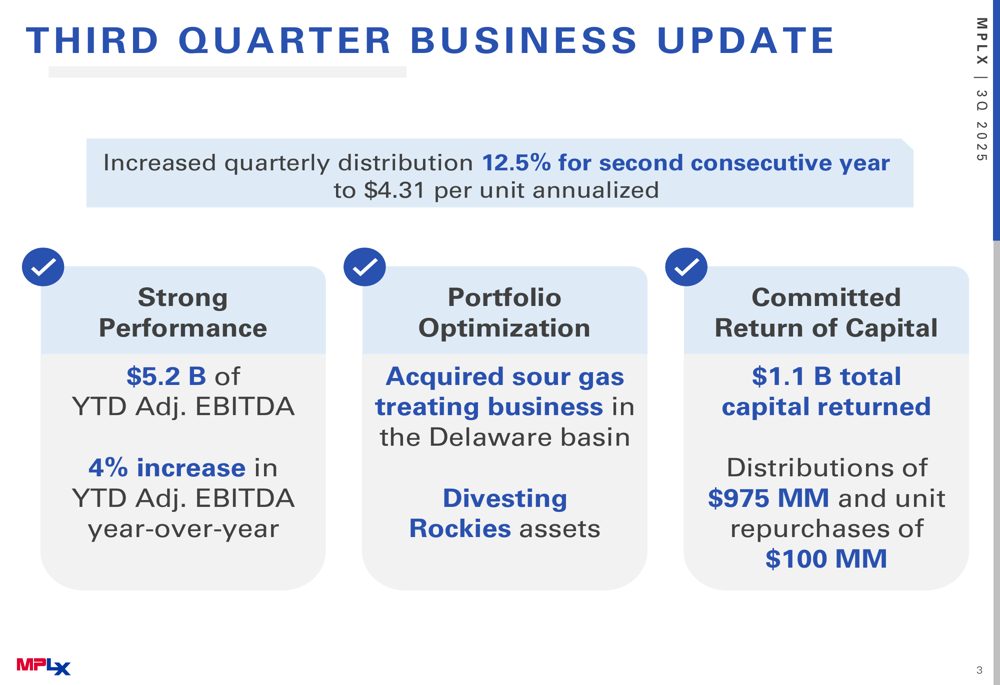

MPLX LP (NYSE:MPLX) presented its third-quarter 2025 results on November 4, highlighting strategic acquisitions in the Permian Basin and continued distribution growth despite increased leverage. The midstream operator reported year-to-date adjusted EBITDA of $5.2 billion, representing a 4% increase year-over-year, while announcing its second consecutive 12.5% distribution increase.

Quarterly Performance Highlights

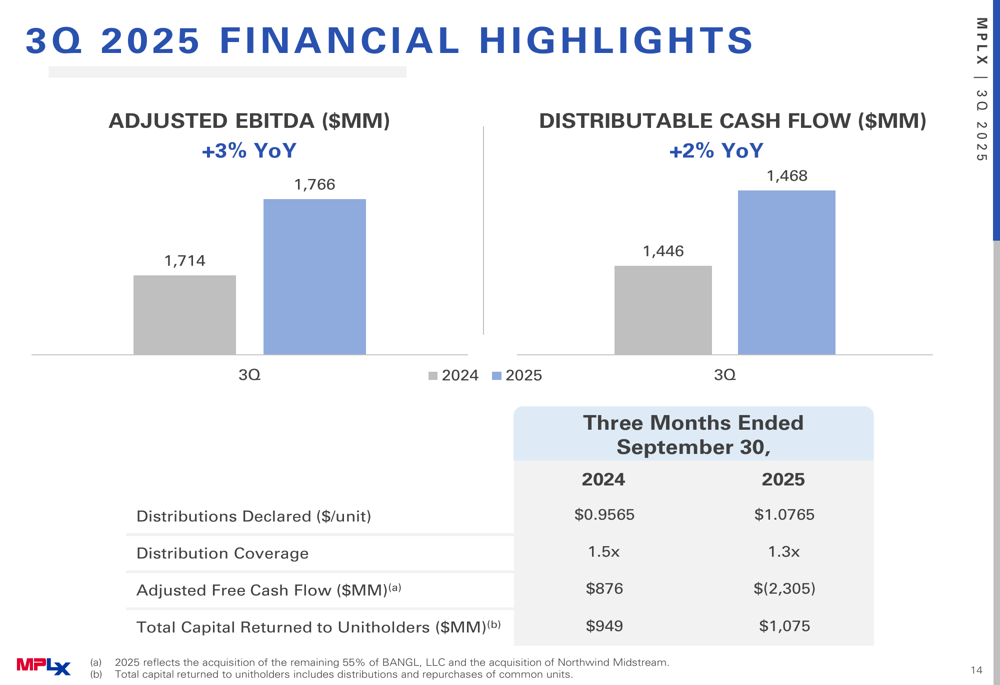

MPLX delivered solid financial results for Q3 2025, with adjusted EBITDA of $1.77 billion, up 3% compared to the same period last year. Distributable cash flow reached $1.47 billion, a 2% year-over-year increase. These results exceeded analyst expectations, with the company reporting an adjusted EPS of $1.52 versus the forecasted $1.08, representing a 40.74% surprise.

As shown in the following quarterly business update, MPLX increased its quarterly distribution to $4.31 per unit annualized and returned $1.1 billion to unitholders through distributions and unit repurchases:

The company's operational performance showed modest volume growth across key metrics. In the Natural Gas and NGL Services segment, gathering volumes increased 3% year-over-year to 6.9 Bcf/d, processing volumes rose 3% to 10.1 Bcf/d, and fractionation volumes grew 7% to 677 mbpd. This segment generated adjusted EBITDA of $629 million, up 1.5% from Q3 2024.

The Crude Oil and Products Logistics segment delivered stronger financial performance despite flat or slightly declining volumes. This segment's adjusted EBITDA reached $1.14 billion, a 3.9% increase year-over-year, driven primarily by higher rates that offset increased operating expenses.

Strategic Permian Basin Expansion

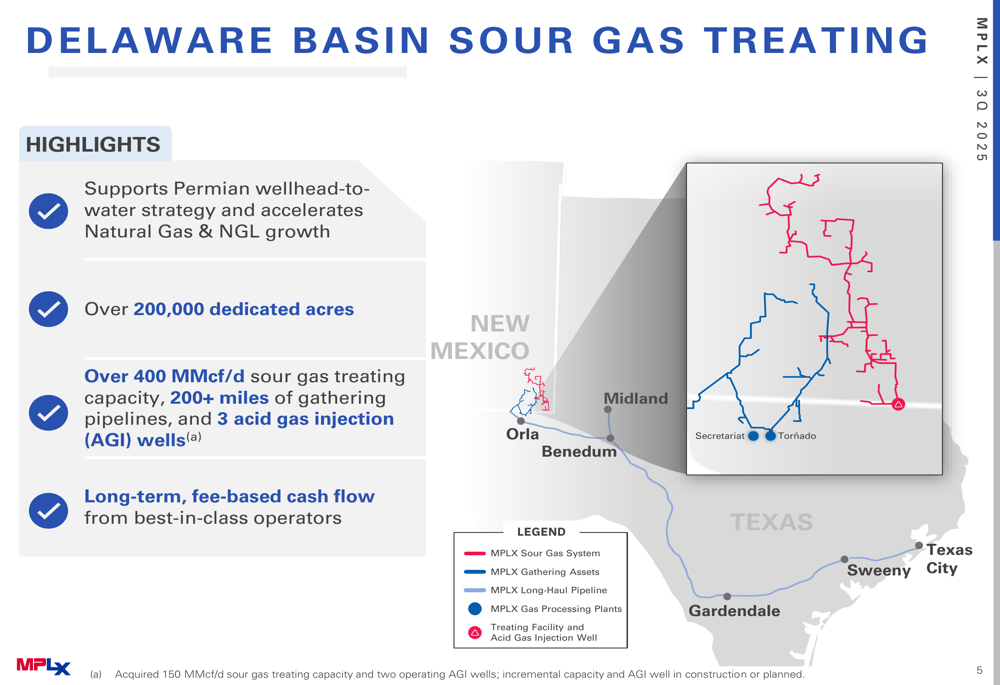

MPLX's most significant strategic move during the quarter was its continued expansion in the Permian Basin, particularly through the acquisition of a Delaware Basin sour gas treating business for approximately $2.4 billion, with plans for an additional $500 million investment. This acquisition aligns with the company's "wellhead-to-water" strategy in the Permian region.

The following map illustrates the strategic footprint of MPLX's Delaware Basin sour gas treating acquisition:

The acquisition includes over 200,000 dedicated acres, more than 400 MMcf/d of sour gas treating capacity, 200+ miles of gathering pipelines, and three acid gas injection wells. This infrastructure supports MPLX's integrated value chain in the Permian Basin, where natural gas production is expected to grow approximately 40% through 2030.

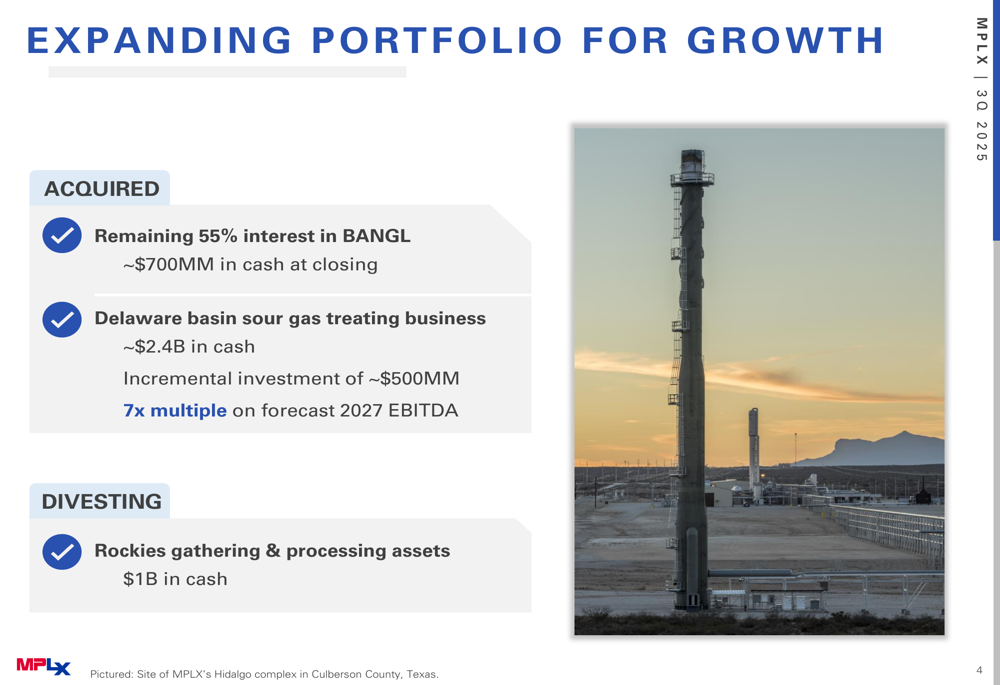

In addition to the sour gas treating business, MPLX acquired the remaining 55% interest in BANGL (Belinda, Alma, Napoleonville, Geismar, and Louisiana) for approximately $700 million. These acquisitions were partially offset by the divestiture of Rockies gathering and processing assets for $1 billion.

As shown in the following slide detailing the company's portfolio expansion:

Growth Platform and Financial Strategy

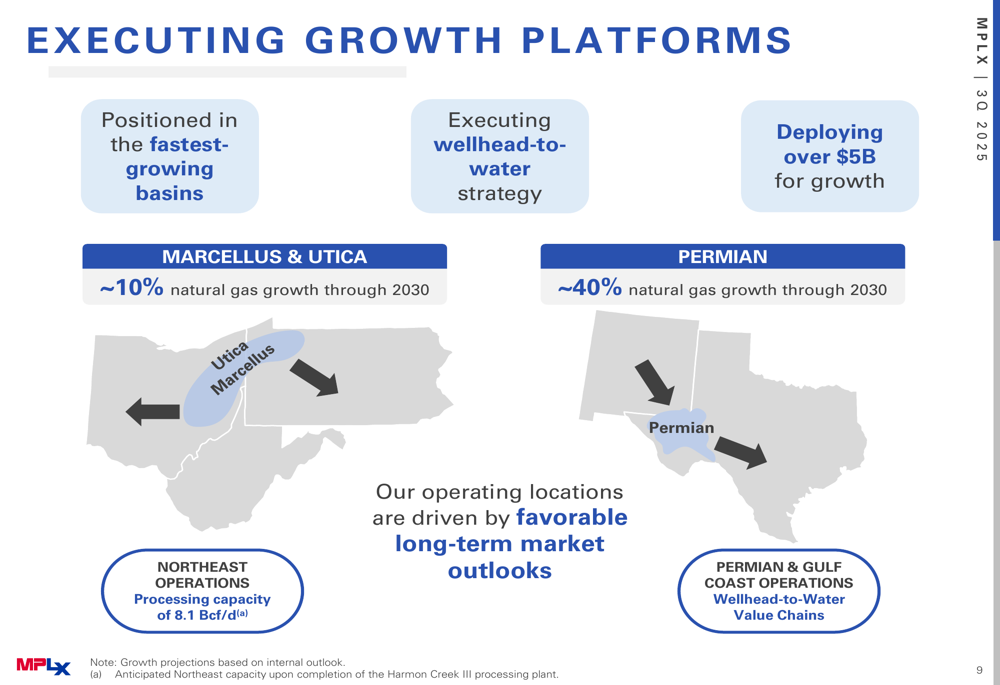

MPLX has positioned itself in what it considers the fastest-growing basins in the United States, with significant operations in the Marcellus, Utica, and Permian regions. The company's strategy focuses on executing integrated value chains from wellhead to export terminals.

The following slide illustrates MPLX's growth platforms and basin positioning:

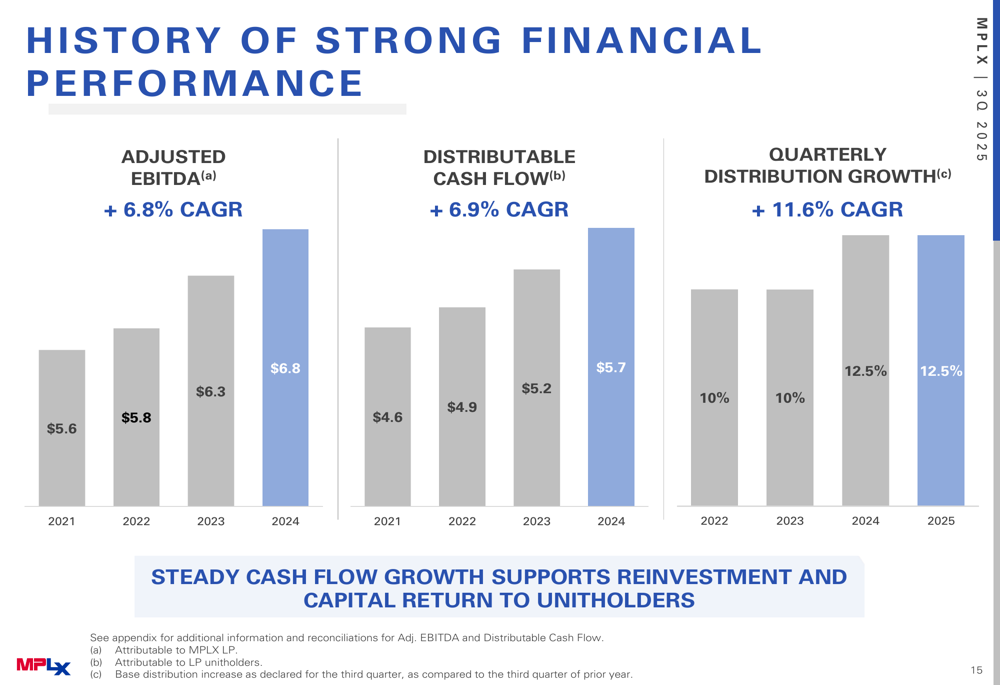

From a financial perspective, MPLX has demonstrated consistent growth over multiple years. The company's adjusted EBITDA has grown at a 6.8% CAGR from 2021 to 2024, while distributable cash flow has increased at a 6.9% CAGR during the same period. Quarterly distributions have grown at an impressive 11.6% CAGR from 2022 to 2025.

As shown in this multi-year performance chart:

Balance Sheet and Capital Allocation

MPLX's significant acquisition activity in 2025 has impacted its balance sheet metrics. The company's consolidated total debt to LTM adjusted EBITDA ratio increased to 3.7x in Q3 2025, up from 3.1x at year-end 2024. To fund its acquisitions, MPLX issued $4.5 billion in unsecured senior notes on August 11, 2025.

The company's adjusted free cash flow turned negative in Q3 2025 at -$2.31 billion, compared to positive $876 million in Q3 2024, reflecting the substantial capital deployed for acquisitions. Despite this, MPLX maintained a distribution coverage ratio of 1.3x, though this was down from 1.5x in the prior year period.

The following financial highlights slide summarizes these metrics:

Forward-Looking Statements

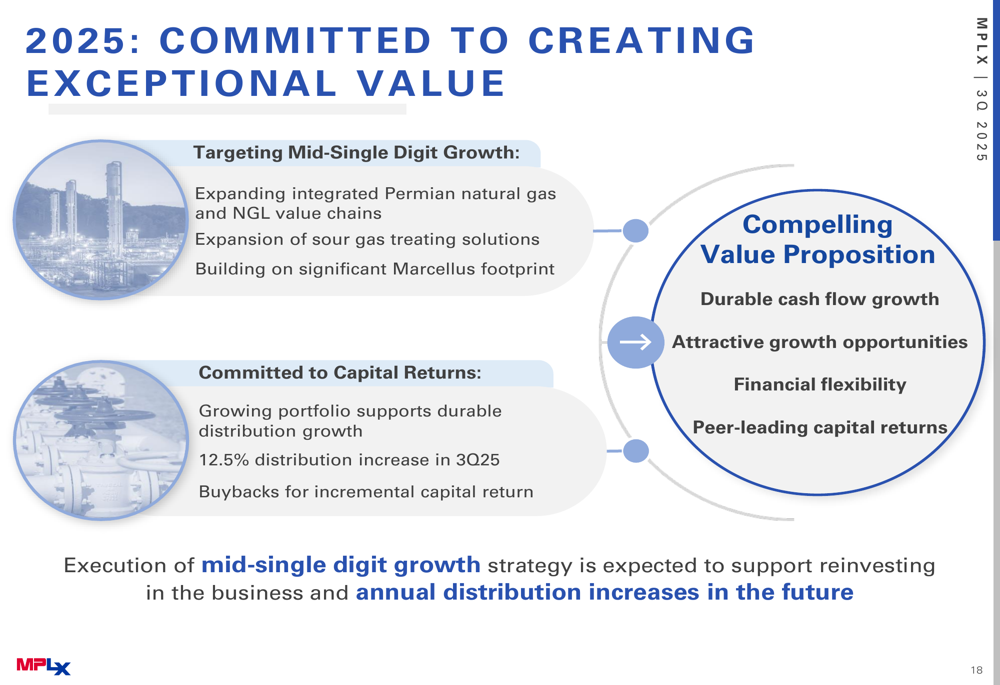

MPLX is targeting mid-single-digit growth going forward, with a focus on expanding its integrated Permian natural gas and NGL value chains, expanding sour gas treating solutions, and building on its significant Marcellus footprint. The company has committed to capital returns through distribution growth and unit repurchases.

As illustrated in this forward-looking summary slide:

Management expects the execution of its mid-single-digit growth strategy to support both reinvestment in the business and annual distribution increases. The company's CEO emphasized MPLX's positioning for long-term natural gas volume growth during the earnings call, stating, "We are positioned for long-term natural gas volume growth."

MPLX stock responded positively to the earnings release, with shares rising 1.12% in pre-market trading to $51.42. The stock remains near its 52-week high of $54.87, reflecting investor confidence in the company's growth strategy despite the increased leverage resulting from its acquisition spree.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.