MicroVision MOVIA lidar gains support on NVIDIA DRIVE AGX platform

Introduction & Market Context

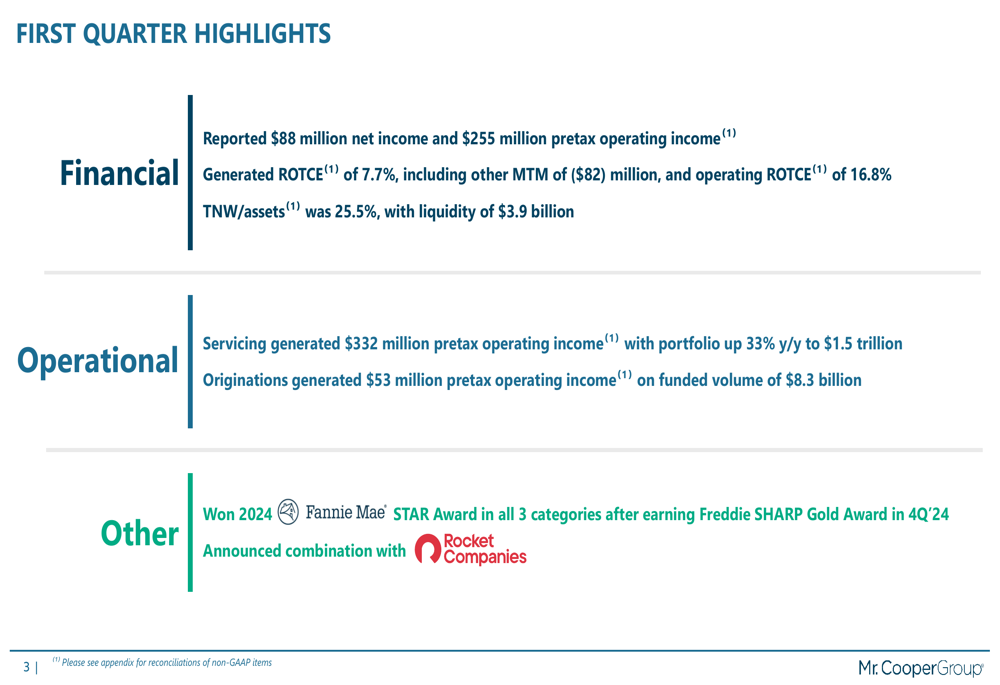

Mr. Cooper Group Inc (NASDAQ:COOP) released its first quarter 2025 earnings presentation on April 23, highlighting continued growth in its servicing business and announcing a significant combination with Rocket Companies. The mortgage servicer reported pretax operating income of $255 million, up from $235 million in the previous quarter and $199 million in the same quarter last year.

The company’s stock has been performing well, trading near $113.60 in premarket trading, up 1.37% following the earnings release. Over the past year, COOP has demonstrated strong momentum with shares trading well above their 52-week low of $76.85.

Quarterly Performance Highlights

Mr. Cooper reported net income of $88 million for Q1 2025, down from $204 million in Q4 2024 and $181 million in Q1 2024. The decrease was primarily due to a negative $82 million mark-to-market adjustment on mortgage servicing rights. However, the company’s operating performance remained strong, with pretax operating income reaching $255 million, up 8.5% quarter-over-quarter and 28% year-over-year.

Operating ROTCE (Return on Tangible Common Equity) improved to 16.8% in Q1 2025, compared to 15.8% in the previous quarter and 14.5% in the same quarter last year. Overall ROTCE was 7.7%, impacted by the MSR mark-to-market adjustments.

As shown in the following summary of first quarter highlights, the company achieved significant milestones in both financial and operational performance:

Servicing Segment Performance

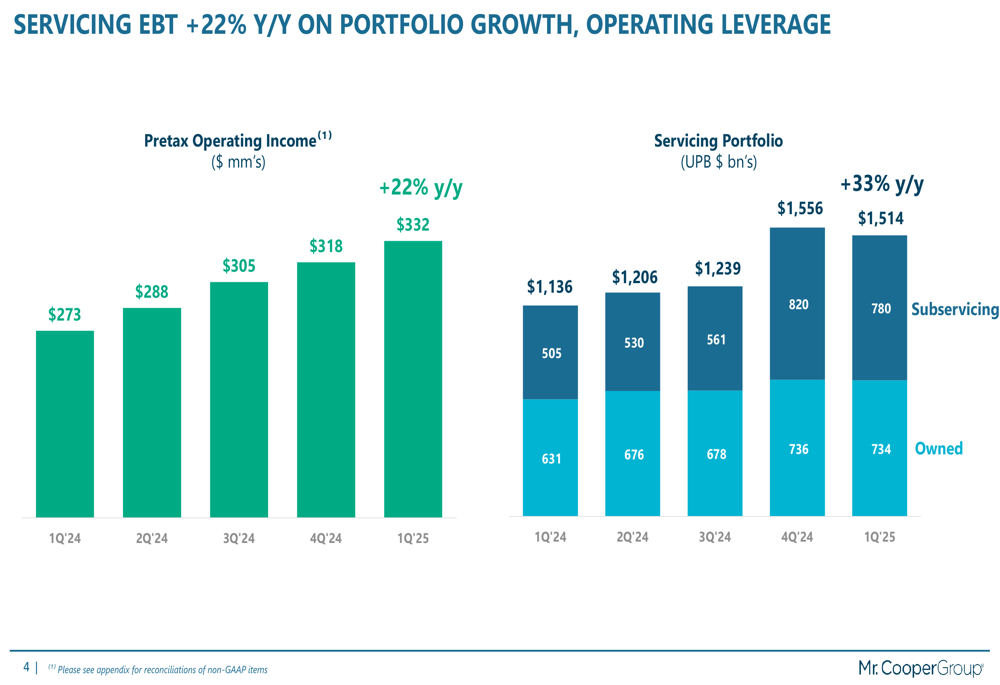

The servicing segment continues to be the primary driver of Mr. Cooper’s growth, generating $332 million in pretax operating income, up 22% year-over-year. This growth was fueled by a 33% increase in the servicing portfolio, which reached $1.514 trillion in unpaid principal balance (UPB).

The servicing portfolio is now evenly balanced between owned MSRs ($734 billion) and subservicing ($780 billion), with the latter becoming the majority of the portfolio for the first time. This shift toward subservicing, which requires less capital, has contributed to the company’s improved operating ROTCE.

The following chart illustrates the consistent growth in servicing pretax operating income over the past five quarters, alongside the expansion of the servicing portfolio:

Originations Segment Performance

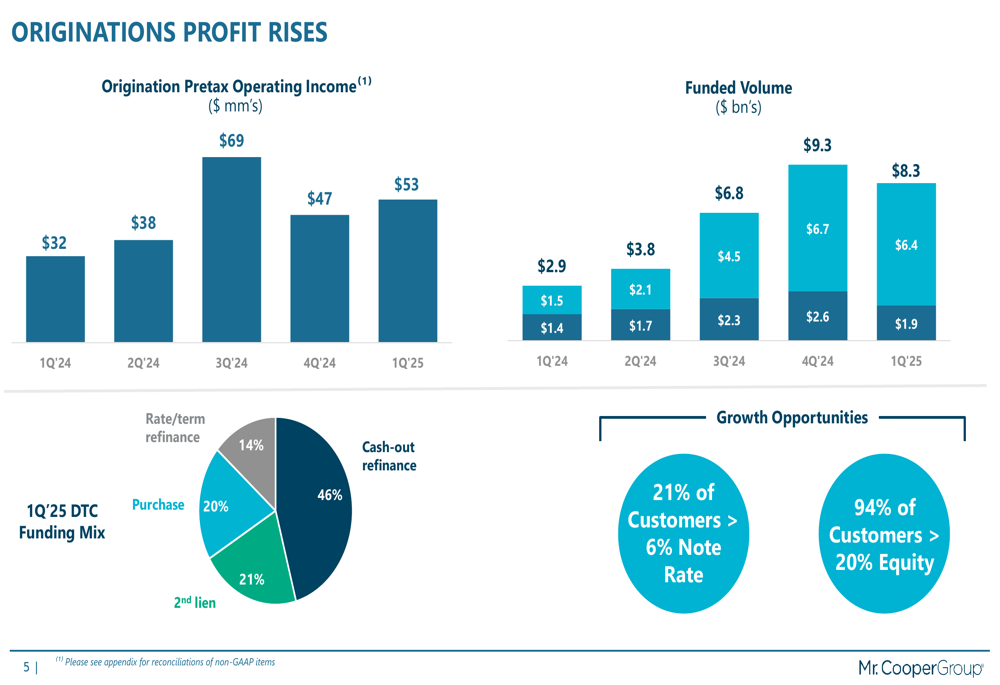

The originations segment also showed strong performance, with pretax operating income of $53 million, up from $47 million in Q4 2024 and $32 million in Q1 2024. This represents a 66% increase year-over-year, despite a slight decrease in funded volume from $9.3 billion in Q4 2024 to $8.3 billion in Q1 2025.

Cash-out refinances dominated the direct-to-consumer funding mix at 46%, followed by second liens at 21%, purchase loans at 20%, and rate/term refinances at 14%. The company noted that 21% of its customers have mortgage rates above 6%, creating potential refinance opportunities, while 94% of customers have more than 20% equity in their homes, supporting continued demand for cash-out refinances and second liens.

The following chart shows the growth in originations pretax operating income and funded volume over the past five quarters:

Balance Sheet and Credit Quality

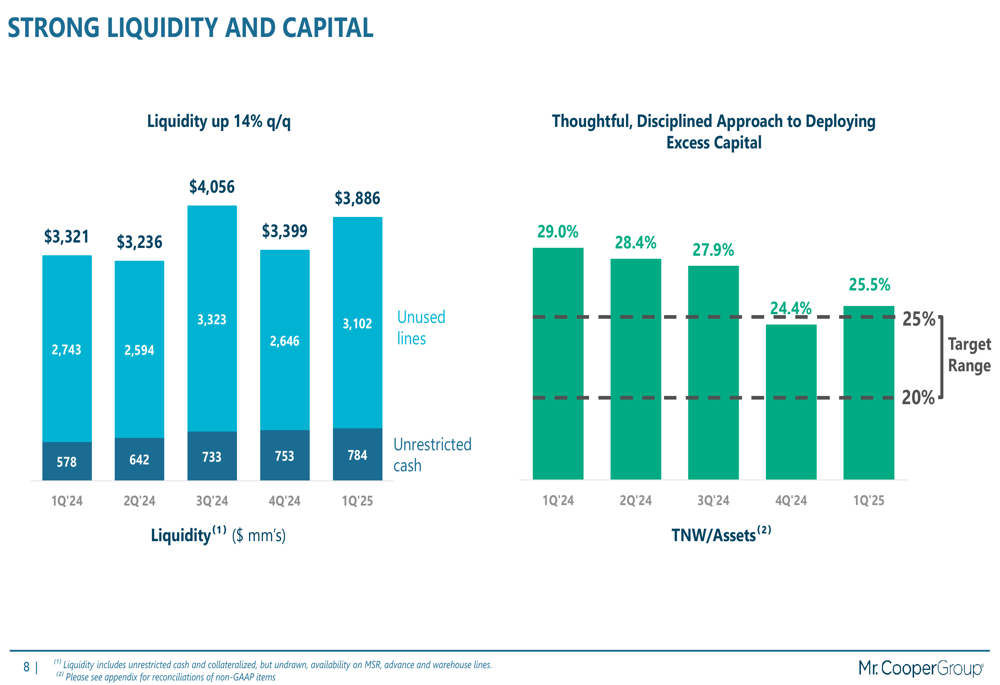

Mr. Cooper maintained a strong balance sheet with liquidity of $3.886 billion at the end of Q1 2025, up 14% quarter-over-quarter. The company’s tangible net worth to assets ratio stood at 25.5%, within its target range.

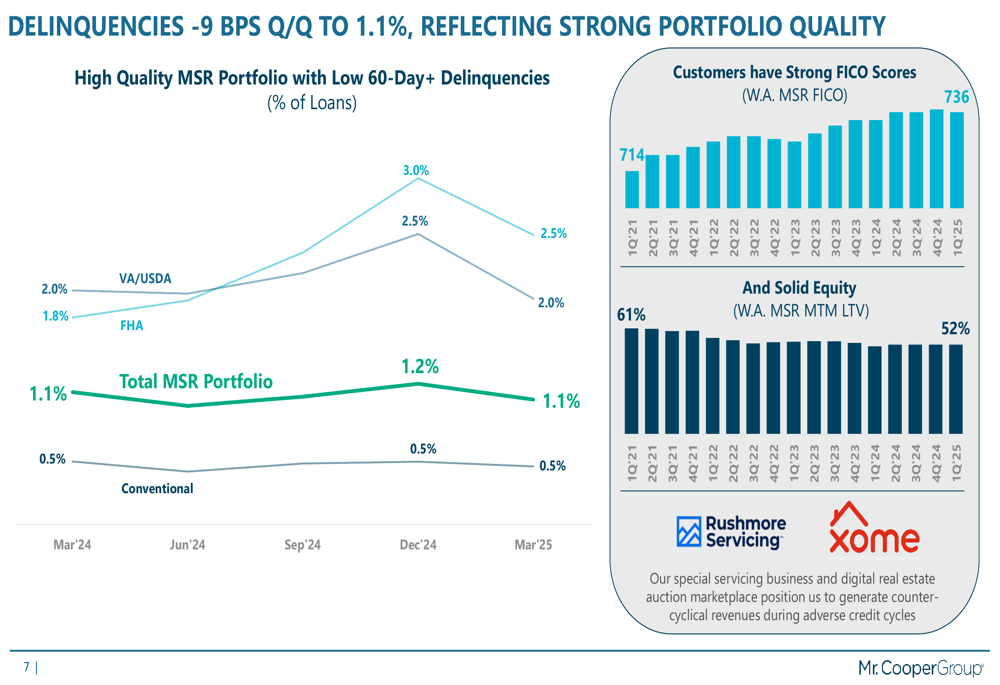

Credit quality continues to improve, with delinquencies decreasing by 9 basis points quarter-over-quarter to 1.1%. This reflects the strong quality of the company’s mortgage portfolio, supported by improving customer FICO scores (which increased from 714 in Q1 2021 to 736 in Q1 2025) and decreasing loan-to-value ratios (which fell from 61% in Q1 2021 to 52% in Q1 2025).

The following charts illustrate the improvement in delinquency rates and customer credit metrics:

The company’s liquidity and capital position also remain strong, as shown in the following chart:

Strategic Initiatives

A major highlight of the presentation was the announcement of Mr. Cooper’s combination with Rocket Companies, which will create a significant player in the mortgage industry. While details of the transaction were not elaborated on in the presentation, this strategic move is expected to enhance the company’s market position and create synergies across both platforms.

Mr. Cooper also highlighted its recognition in the industry, having won the 2024 Fannie Mae (OTC:FNMA) STAR Award in all three categories after earning the Freddie SHARP Gold Award in Q4 2024. These awards reflect the company’s commitment to quality, risk management, and performance in mortgage servicing.

Growth Opportunities

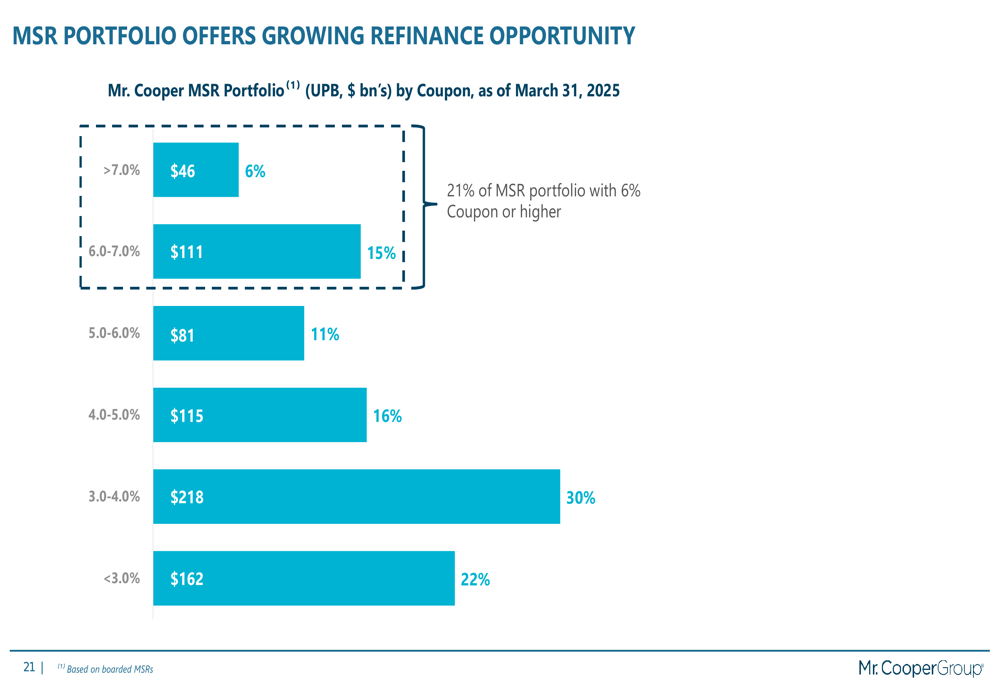

Mr. Cooper identified several growth opportunities in its presentation. The company’s MSR portfolio offers increasing refinance potential, with 21% of the portfolio having coupon rates of 6% or higher. This positions the company well for future refinancing opportunities if interest rates decline.

The distribution of Mr. Cooper’s MSR portfolio by coupon rate as of March 31, 2025, is illustrated in the following chart:

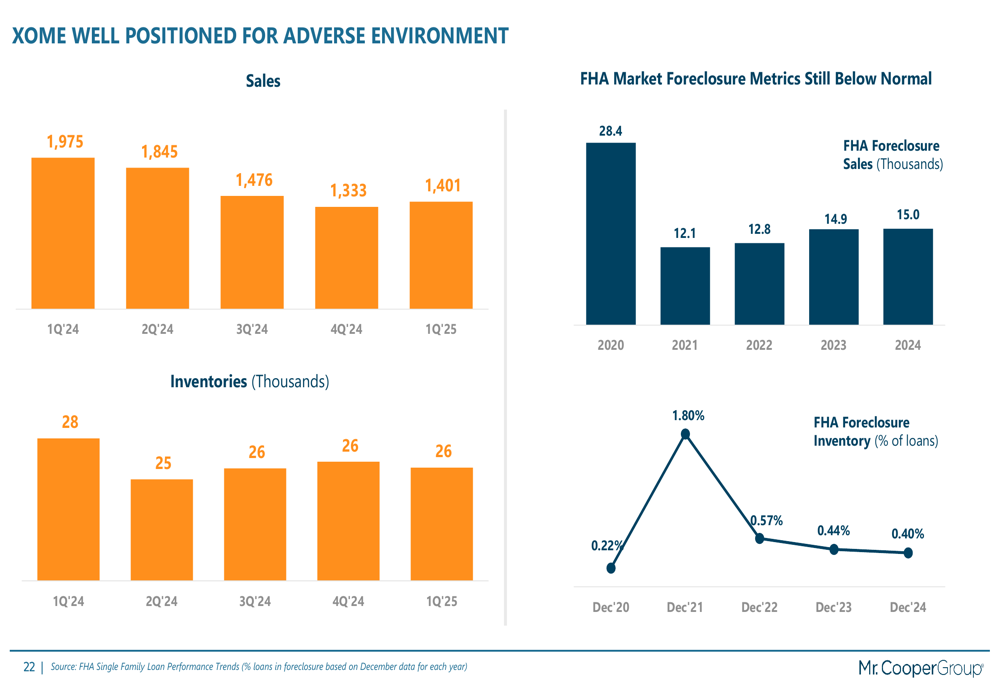

Additionally, the company’s XOME business, a real estate auction marketplace, is well-positioned for adverse market conditions. While sales have declined from 1,975 in Q1 2024 to 1,401 in Q1 2025, inventories have remained stable at around 26,000 properties, providing a potential countercyclical revenue stream if foreclosure activity increases.

The following chart shows XOME sales and inventories over the past five quarters:

Forward-Looking Statements

Looking ahead, Mr. Cooper appears well-positioned for continued growth in its servicing business, with opportunities to capitalize on potential refinancing activity if interest rates decline. The company’s strong liquidity and capital position provide flexibility for future acquisitions and investments in technology and customer experience.

The combination with Rocket Companies represents a significant strategic move that could reshape the competitive landscape in the mortgage industry. Investors will be watching closely for more details on this transaction and its potential impact on Mr. Cooper’s future growth and profitability.

With delinquencies at low levels and strong customer credit metrics, the company is also well-prepared to navigate any potential deterioration in economic conditions, making it a resilient player in the mortgage servicing industry.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.