US stock futures inch lower after Wall St marks fresh records on tech gains

Introduction & Market Context

Multiconsult AS (OB:MULTI) presented its second quarter and half-year 2025 results on August 19, 2025, revealing how calendar effects significantly impacted quarterly performance despite underlying organic growth. The engineering consultancy firm’s stock closed at NOK 204 on the presentation day, showing a 0.99% increase, reflecting investor confidence despite the mixed results.

The company operates in a market environment characterized by strong demand in energy and defense sectors, while housing and real estate continue to face challenges. CEO Grethe Bergly emphasized the company’s strategic positioning across diverse business segments as a key strength in navigating varying market conditions.

Quarterly Performance Highlights

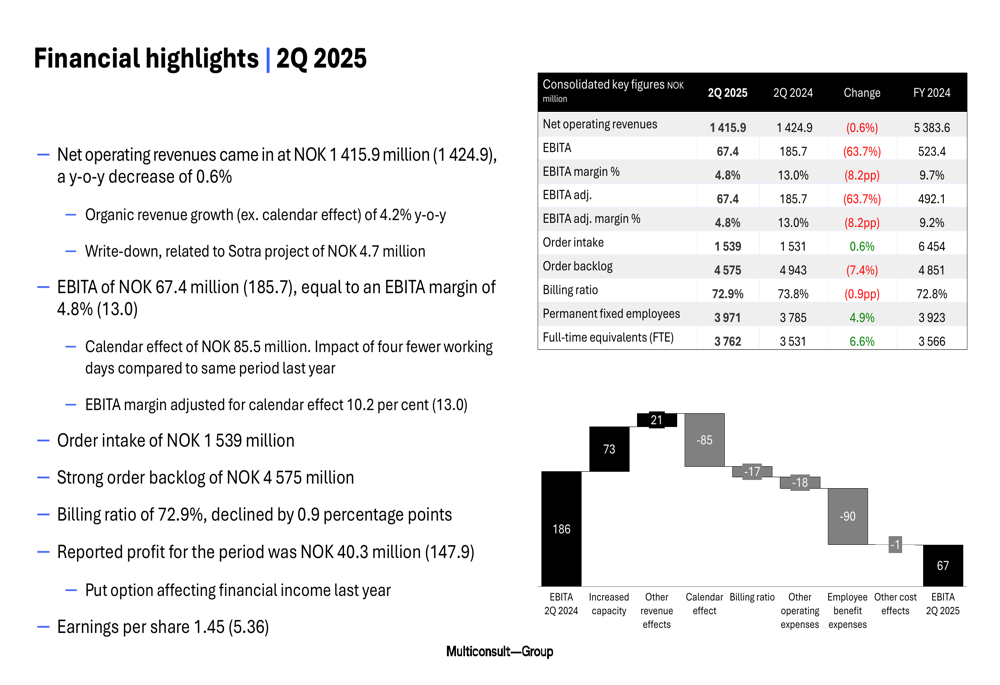

Multiconsult reported net operating revenues of NOK 1,416 million for Q2 2025, representing a slight year-over-year decrease of 0.6%. However, when adjusted for calendar effects (four fewer working days compared to the same period last year), organic revenue growth stood at a healthy 4.2%.

As shown in the following comprehensive financial overview:

EBITA came in at NOK 67.4 million, resulting in an EBITA margin of 4.8% – a significant drop from 13.0% in Q2 2024. This decline was primarily attributed to the calendar effect, which had an estimated impact of NOK 85.5 million. The company’s billing ratio decreased slightly to 72.9%, down 0.9 percentage points year-over-year.

Order intake remained stable at NOK 1,539 million, a marginal 0.6% increase from Q2 2024, while the order backlog stood at NOK 4,575 million, down from NOK 4,943 million a year earlier. Earnings per share declined to NOK 1.45 from NOK 5.36 in the comparable period.

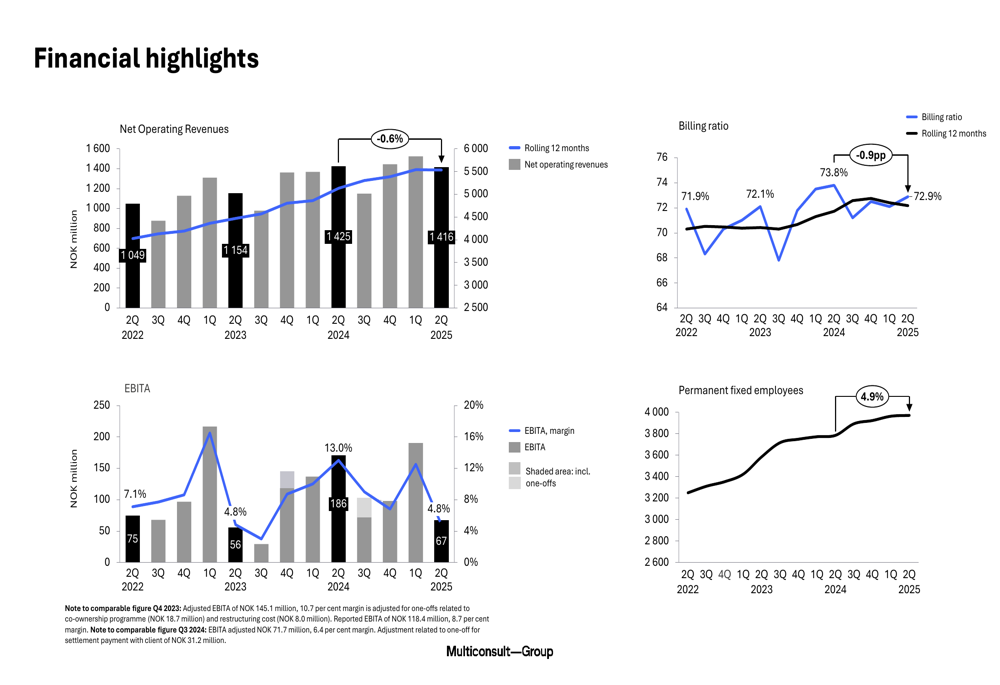

For the first half of 2025, Multiconsult delivered more robust results, with net operating revenues increasing by 5.3% to NOK 2,939.4 million and EBITA reaching NOK 257.8 million (margin of 8.8%).

The following chart illustrates key financial metrics over time:

Segment Performance

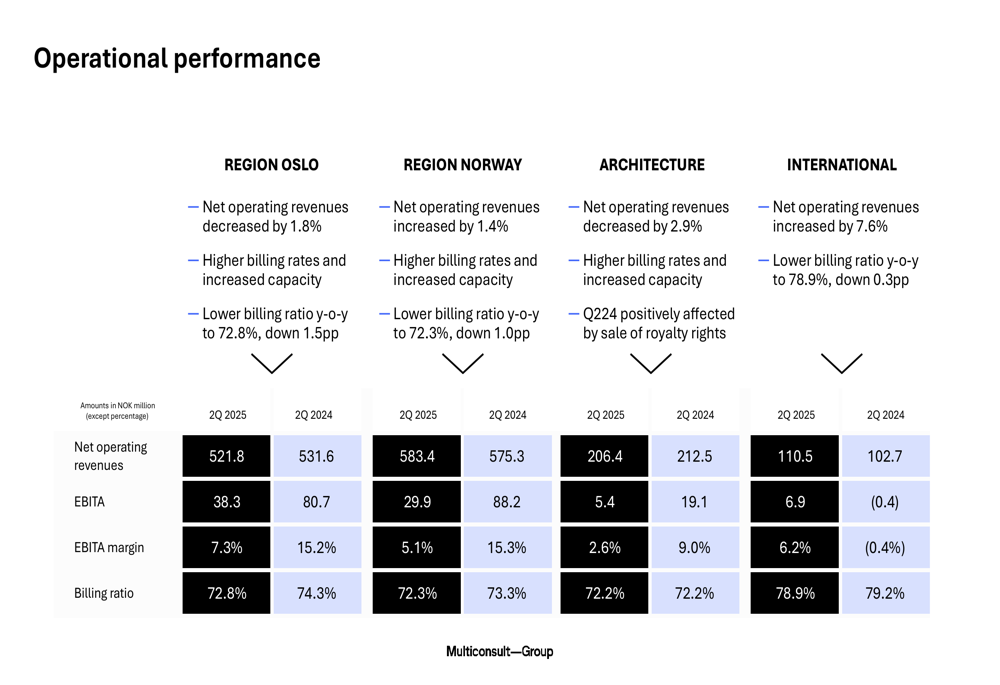

Multiconsult’s performance varied significantly across its business segments. Region Oslo, the company’s largest segment, saw net operating revenues decrease by 1.8% to NOK 521.8 million with an EBITA margin of 7.3%. Region Norway performed slightly better with a 1.4% revenue increase to NOK 583.4 million, though its EBITA margin was lower at 5.1%.

The Architecture segment faced challenges with a 2.9% revenue decline and a modest EBITA margin of 2.6%. In contrast, the International segment emerged as a bright spot, delivering 7.6% revenue growth and a solid EBITA margin of 6.2%.

The operational performance by region is detailed in the following breakdown:

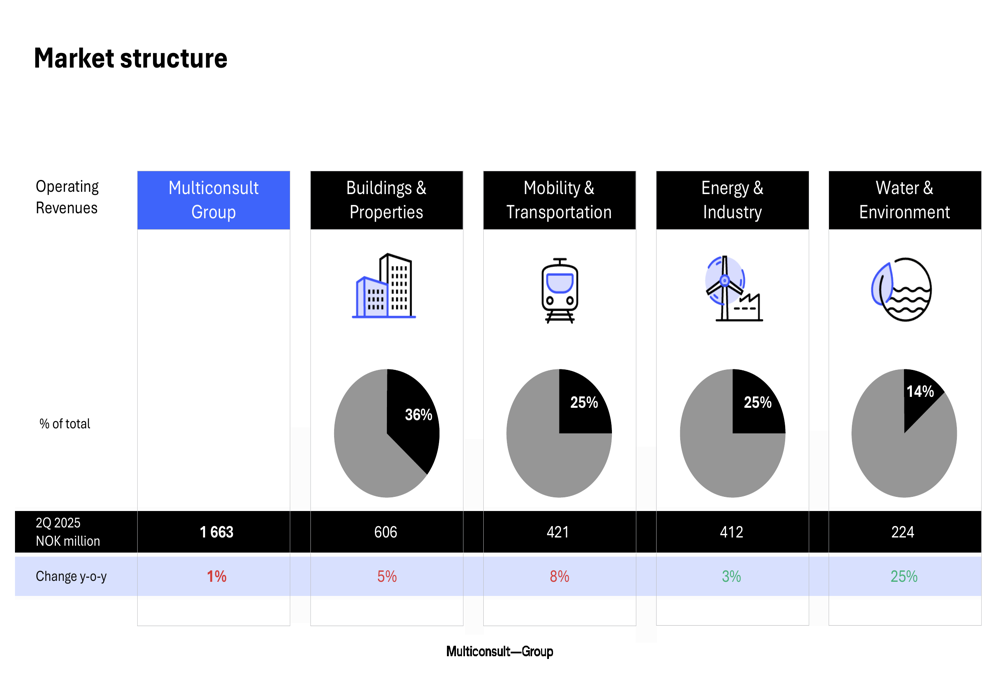

From a market perspective, Multiconsult maintained a balanced portfolio across sectors. Buildings & Properties remained the largest contributor at 36% of operating revenues, followed by Mobility & Transportation and Energy & Industry at 25% each, with Water & Environment accounting for 14%.

The Water & Environment segment showed the strongest growth at 25% year-over-year, while Mobility & Transportation grew by 8%, as illustrated in this market structure overview:

Strategic Initiatives

A centerpiece of Multiconsult’s strategic development is the announced acquisition of ViaNova, a Norwegian infrastructure consultancy founded in 1998. This acquisition aims to strengthen Multiconsult’s position in the transportation sector, creating what the company describes as "Norway’s strongest mobility and transportation team."

ViaNova brings expertise in transportation, urban environments, and smart mobility, with 129 employees across four entities. The company generated net operating revenues of NOK 227.5 million in FY 2024 with an EBIT of NOK 21.9 million. The transaction is expected to close in Q3 2025.

CEO Grethe Bergly highlighted five strategic priorities that continue to guide the company’s development:

The company also emphasized growing opportunities in defense-related projects, securing framework agreements with the Norwegian Defence Estates Agency, and positioning itself to address Norway’s significant infrastructure maintenance backlog.

Financial Position & Outlook

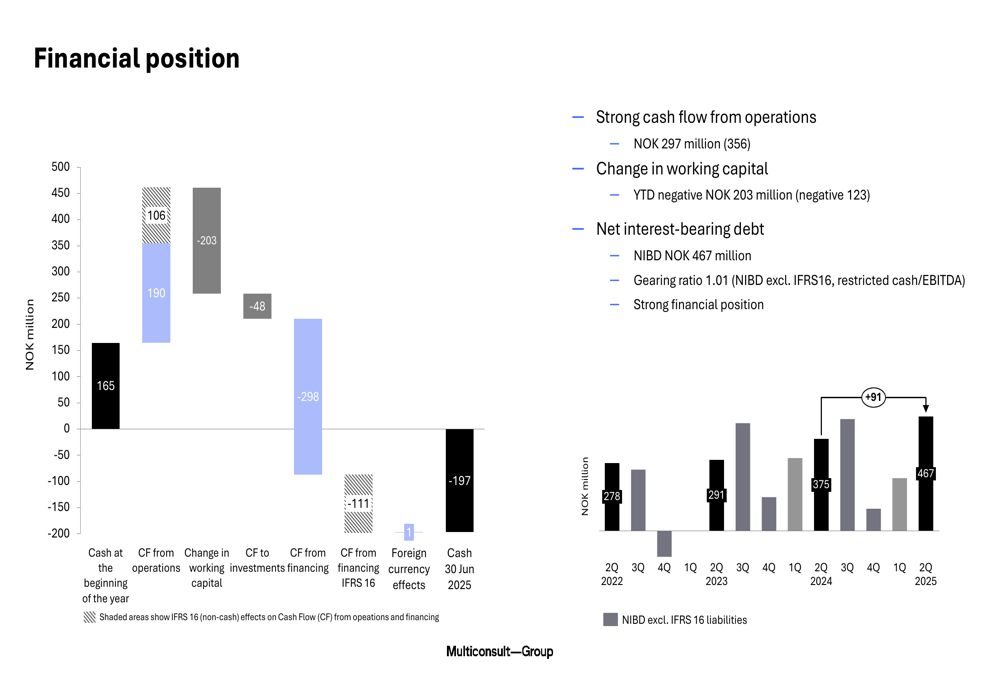

Multiconsult reported strong cash flow from operations of NOK 297 million, though working capital showed a negative change of NOK 203 million year-to-date. The company’s net interest-bearing debt increased to NOK 467 million, up from NOK 375 million at the end of 2024.

A significant financial development was the successful refinancing of credit facilities, expanding from NOK 1.12 billion to NOK 2.5 billion. The new facilities include a revolving credit facility of NOK 2.1 billion and an increased cash pool facility of NOK 400 million, with maturity set for June 30, 2028.

The following chart illustrates the company’s financial position:

Looking ahead, Multiconsult maintains a stable market outlook, with continued investment expected in key public sectors and a solid infrastructure market. The company noted that the housing and real estate market continues to face low investment levels, while pricing pressure remains a challenge across segments.

Forward-Looking Statements

Multiconsult’s management expressed confidence in the company’s diversified business model and strategic positioning. The acquisition of ViaNova represents a significant step in strengthening its capabilities in the transportation sector, while the refinanced credit facilities provide financial flexibility for future growth initiatives.

The company’s focus on defense-related opportunities and infrastructure maintenance projects is expected to offset challenges in the housing and real estate markets. With a strong order backlog of NOK 4,575 million and positive organic growth trends, Multiconsult appears well-positioned to navigate market uncertainties while pursuing its strategic priorities.

This measured optimism comes after a first quarter that saw stronger performance, with Q1 2025 having delivered 11.4% revenue growth and a 40% surge in EBITDA. The significant impact of the calendar effect on Q2 results suggests that underlying business fundamentals remain solid despite the quarterly fluctuation in reported figures.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.