German construction sector still in recession, civil engineering only bright spot

Introduction & Market Context

Mycronic publ AB (STO:MYCR) presented its second quarter 2025 results on July 11, revealing substantial growth in sales and profitability despite a significant decline in order intake. The Swedish technology company, which specializes in production equipment for the electronics industry, saw its stock rise 3.45% to close at SEK 209.8 following the presentation.

The results come amid a broader electronics industry recovery, with the global electronics market projected to grow 7.4% in 2025 after 5.0% growth in 2024. The semiconductor industry, a key driver for Mycronic’s business, grew 19.2% in 2024 and is forecast to expand by 11.8% in 2025, providing a favorable backdrop for the company’s operations.

Quarterly Performance Highlights

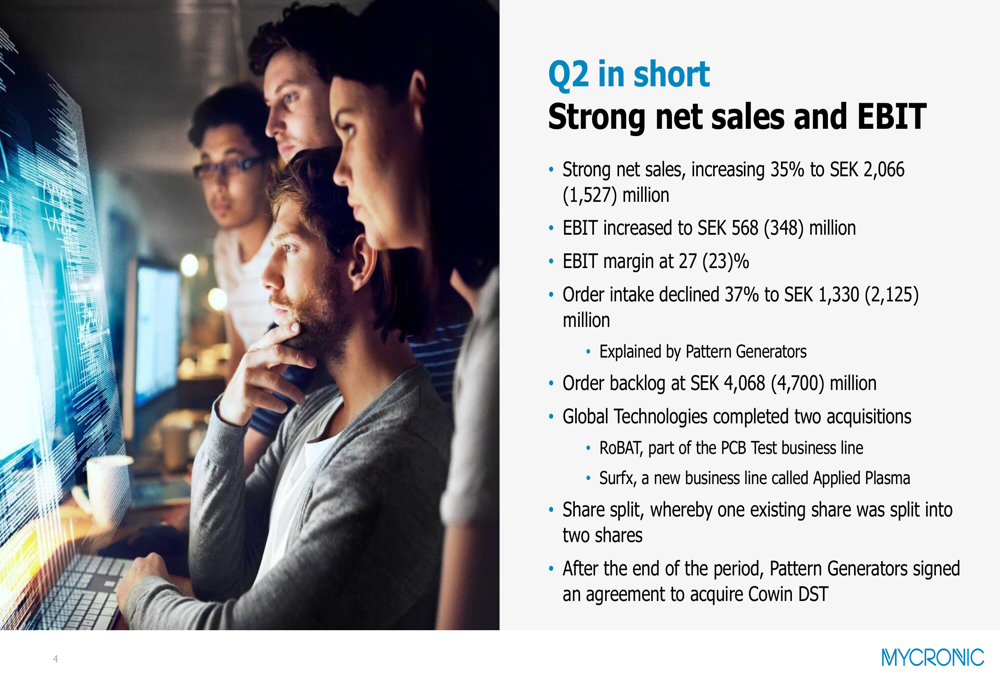

Mycronic delivered impressive financial results for Q2 2025, with net sales increasing 35% year-over-year to SEK 2,066 million (compared to SEK 1,527 million in Q2 2024). The company’s EBIT surged to SEK 568 million, up from SEK 348 million in the same period last year, representing a 63% increase. The EBIT margin improved to 27%, up from 23% in Q2 2024.

As shown in the following summary of key Q2 metrics:

Despite the strong sales and profit performance, order intake declined 37% to SEK 1,330 million (from SEK 2,125 million), primarily due to lower orders in the Pattern Generators division. The order backlog stood at SEK 4,068 million at the end of the quarter, down from SEK 4,700 million a year earlier.

Divisional Performance

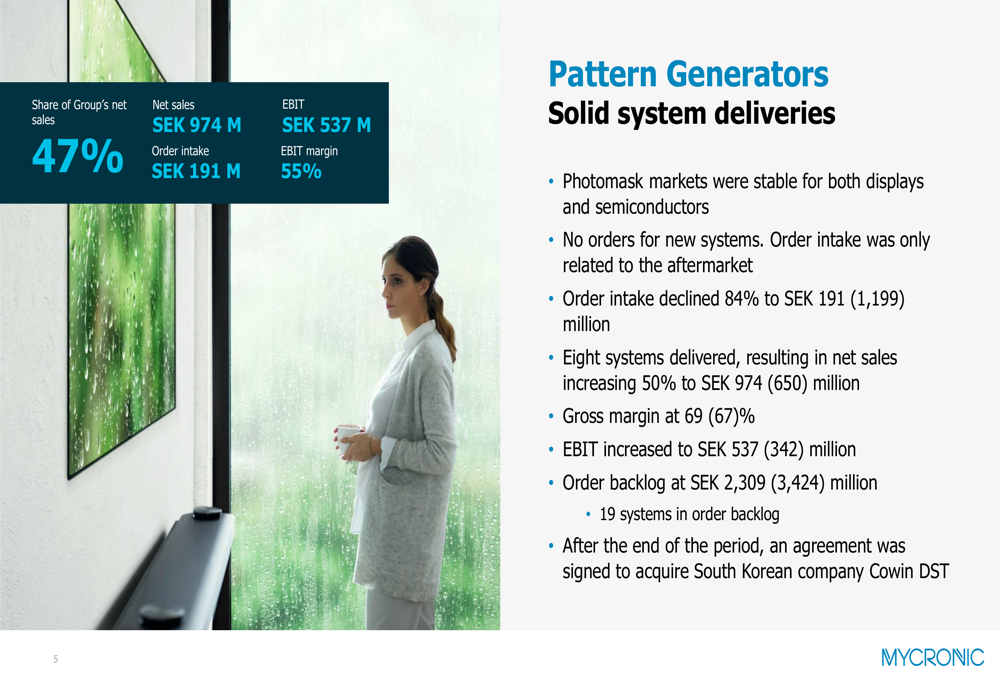

The Pattern Generators division, which accounted for 47% of group net sales, delivered exceptional results with an EBIT margin of 55%. The division saw net sales increase by 50% to SEK 974 million, driven by the delivery of eight systems. However, order intake declined 84% to SEK 191 million as no new system orders were received during the quarter.

The following slide illustrates the strong performance of the Pattern Generators division:

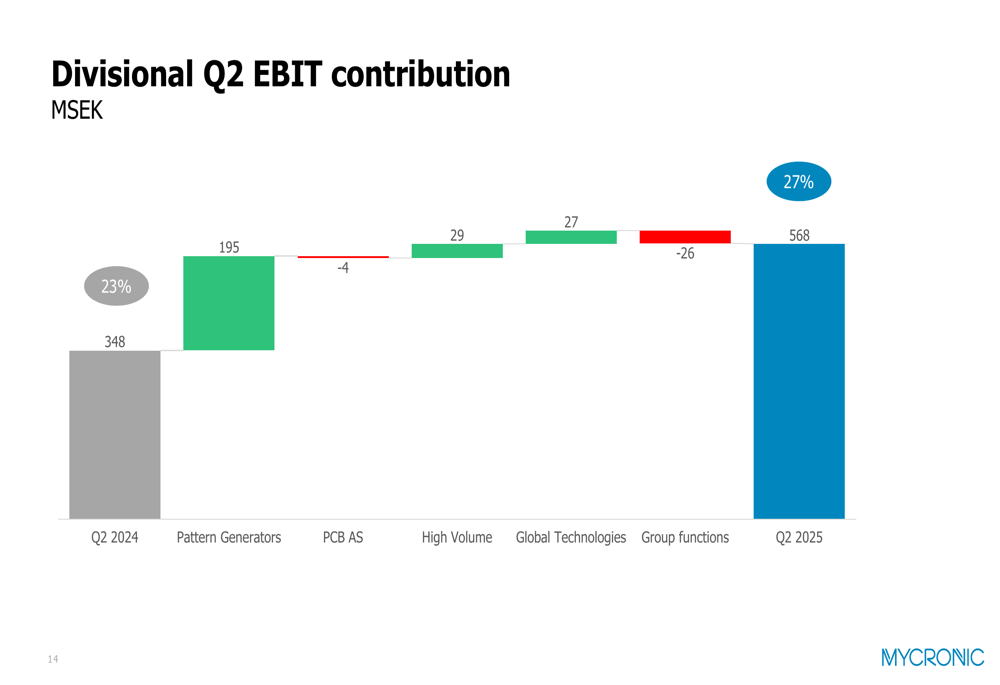

The High Volume division also performed well, with net sales increasing 39% to SEK 443 million and EBIT rising to SEK 74 million, representing a 17% margin. The division benefited from strong demand in the Chinese domestic market and solid performance outside China.

The PCB Assembly Solutions division, which changed its name during the quarter, saw a 7% decrease in net sales to SEK 328 million, with EBIT at SEK 14 million. The European market showed signs of recovery, while the US market remained uncertain due to tariff concerns.

Global Technologies, the company’s innovation-focused division, increased net sales by 59% to SEK 323 million and improved EBIT to SEK 11 million from a loss of SEK 15 million in the previous year. This improvement came despite a SEK 23 million negative EBIT impact from recent acquisitions.

The following chart breaks down each division’s contribution to the overall EBIT growth:

Strategic Acquisitions and Growth Initiatives

During Q2 2025, Mycronic completed two strategic acquisitions through its Global Technologies division. The company acquired ROBAT, which has developed technology for fast and reliable testing of signal quality on PCBs, and Surfx Technologies, which provides atmospheric plasma solutions.

After the end of the quarter, the Pattern Generators division signed an agreement to acquire South Korean company Cowin DST, further strengthening Mycronic’s market position.

The company also highlighted its sustainability initiatives, renewing its SEK 1 billion credit facility with Handelsbanken until 2030. The facility is linked to specific requirements related to the company’s science-based climate targets and supply chain due diligence, underscoring Mycronic’s commitment to sustainable operations.

Financial Analysis

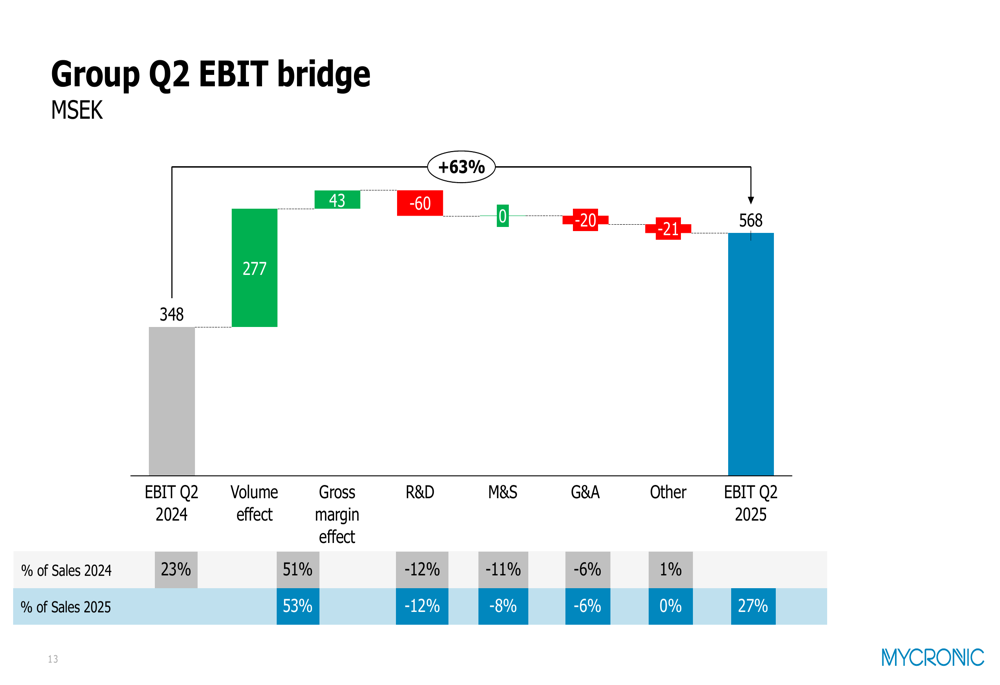

A deeper look at Mycronic’s Q2 performance reveals that the EBIT improvement was primarily driven by volume effects (SEK 277 million) and gross margin improvements (SEK 43 million), partially offset by increased R&D expenses (SEK 60 million) and G&A costs (SEK 20 million).

The following EBIT bridge illustrates the factors contributing to the year-over-year improvement:

The company’s cash flow was significantly impacted by acquisitions and dividend payments. Cash flow from operations before changes in working capital was strong at SEK 1,263 million for the first half of 2025, compared to SEK 1,004 million in the same period of 2024. However, the cash position decreased to SEK 1,804 million at the end of the period, down from an opening balance of SEK 3,014 million, primarily due to investing activities of SEK 993 million and financing activities of SEK 784 million.

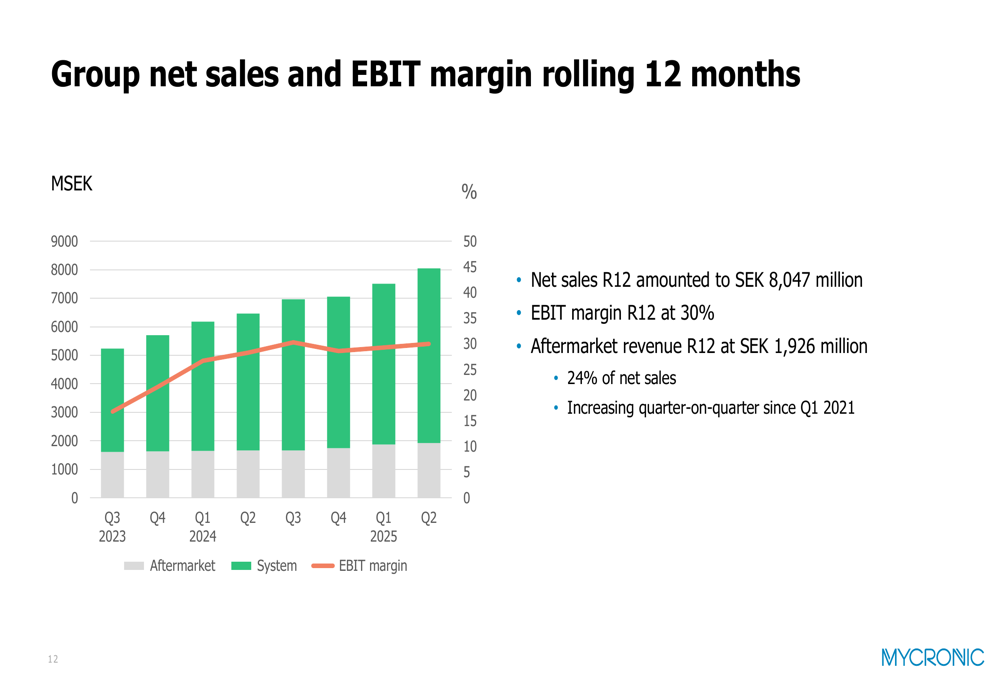

Looking at longer-term trends, Mycronic’s rolling 12-month performance shows net sales of SEK 8,047 million with an impressive EBIT margin of 30%. Aftermarket revenue for the rolling 12 months reached SEK 1,926 million, representing 24% of net sales and showing consistent quarter-on-quarter growth since Q1 2021.

Outlook and Forward-Looking Statements

Following the strong second quarter performance and recent acquisitions, Mycronic revised its outlook for 2025, projecting net sales of SEK 7.5 billion. This represents an upward revision from the previous guidance range of SEK 7.0-7.5 billion provided after Q1 2025, indicating increased confidence in the company’s growth trajectory.

The company’s optimism is supported by positive industry forecasts, with the global electronics industry expected to grow by 7.4% in 2025. The semiconductor industry is projected to expand by 11.8%, while the display market is forecast to grow by 4.8%.

However, Mycronic noted that all market forecasts were made before recent tariff announcements, suggesting potential uncertainty in the market outlook. The company’s diversified business model, with operations across multiple segments and geographies, positions it well to navigate potential market challenges while capitalizing on growth opportunities in high-performance data centers, AI, 5G/6G, electric vehicles, and IoT applications.

With a strong order backlog of SEK 4,068 million and strategic acquisitions enhancing its technology portfolio, Mycronic appears well-positioned to deliver on its revised outlook for 2025 despite the decline in order intake during Q2.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.