Asia FX moves little with focus on US-China trade, dollar steadies ahead of CPI

Introduction & Market Context

Natera Inc (NASDAQ:NTRA) presented its Q2 2025 earnings results on August 7, 2025, showcasing strong growth across its testing portfolio and raising its full-year guidance. The genetic testing company’s shares responded positively, jumping 13.4% to $159.99 in premarket trading following the announcement.

The company’s performance continues to build on momentum seen in Q1, when it reported a 37% year-over-year revenue increase. Natera’s focus on expanding its oncology testing business while maintaining strength in women’s health appears to be yielding results, with particularly strong growth in its Signatera molecular residual disease (MRD) testing.

Quarterly Performance Highlights

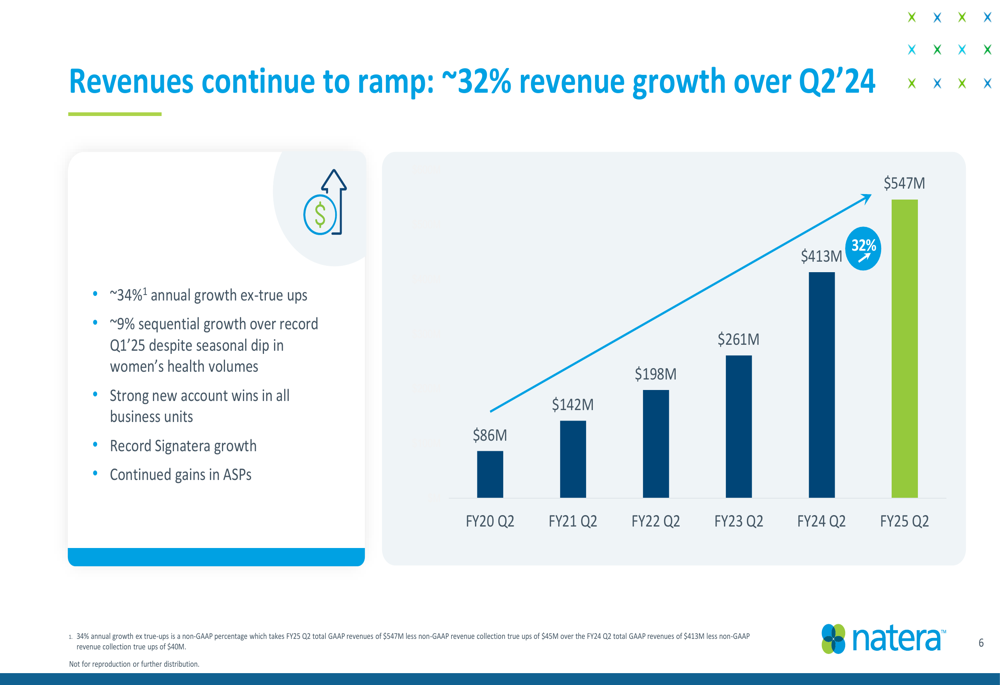

Natera reported Q2 2025 revenue of approximately $547 million, representing a 32% increase from $413 million in the same period last year. The company processed approximately 853,000 total tests during the quarter, up 12% year-over-year, with oncology tests showing particularly strong growth of 51% to reach 189,000 tests.

As shown in the following chart of quarterly revenue growth:

The company’s gross margin improved to 63.4% in Q2 2025, up from 58.8% in Q2 2024, representing a 458 basis point improvement. This margin expansion occurred despite significant growth in first-time Signatera patients, which typically drives higher costs of goods sold.

The gross margin trend demonstrates consistent improvement over multiple quarters:

Notably, Natera generated approximately $24 million in cash inflow during Q2, contributing to a total of $47 million in net cash generated year-to-date. The company’s cash and investments stood at $1.016 billion as of June 30, 2025, up from $968.3 million at the end of 2024.

Product Expansion and Clinical Evidence

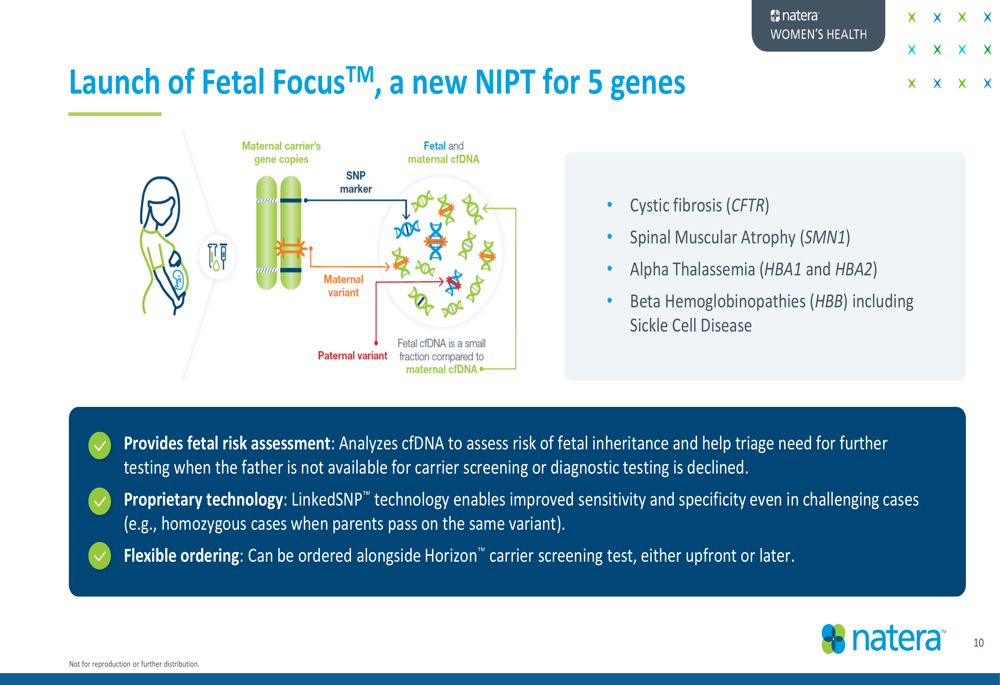

A significant development in Q2 was the launch of Fetal Focus™, a new non-invasive prenatal test (NIPT) for five genes associated with serious genetic conditions. The test screens for cystic fibrosis, spinal muscular atrophy, alpha thalassemia, and beta hemoglobinopathies including sickle cell disease.

The Fetal Focus launch represents an important expansion of Natera’s women’s health portfolio:

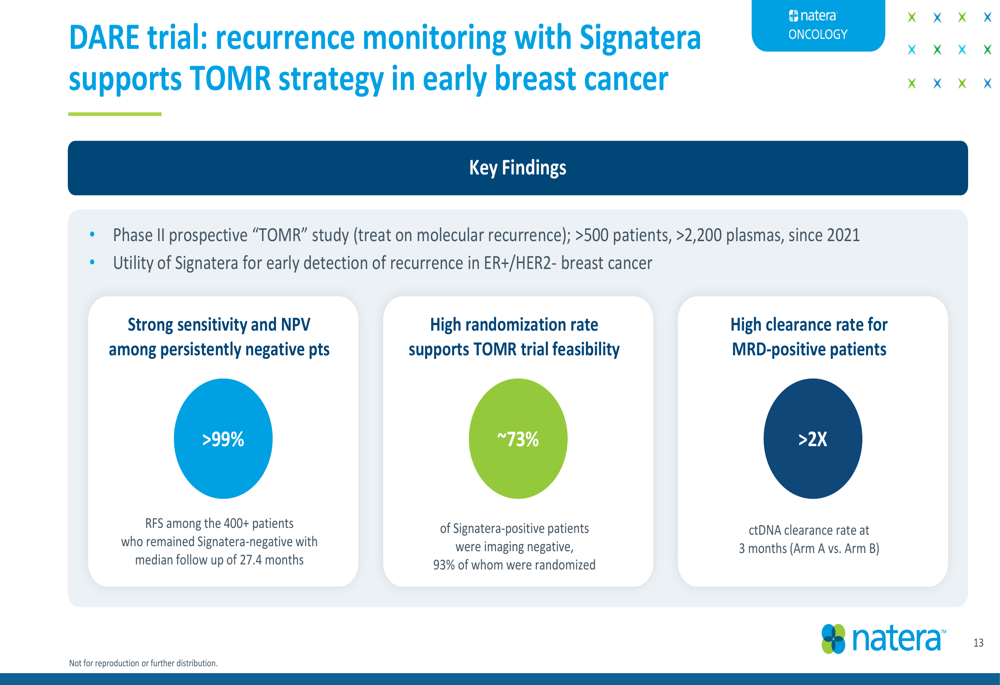

In oncology, Natera reported impressive results from the DARE trial, which examined recurrence monitoring with Signatera in early breast cancer. The trial demonstrated strong sensitivity and negative predictive value among persistently negative patients (>99%), supporting Signatera’s utility in breast cancer monitoring.

The following image highlights key findings from the DARE trial:

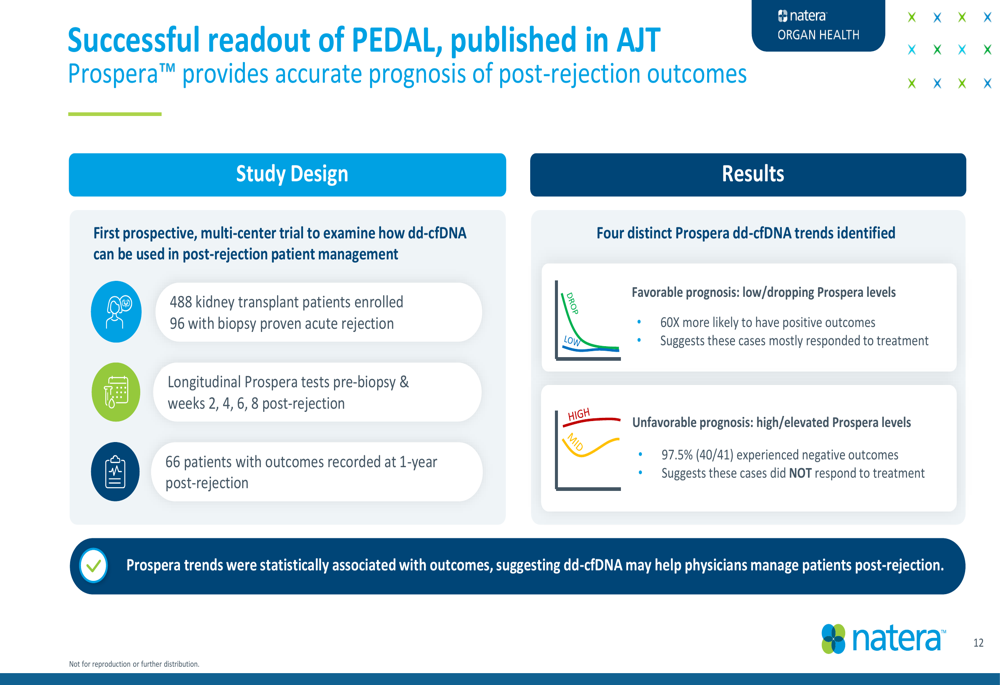

Additionally, the company presented results from the PEDAL trial for its Prospera test in kidney transplant monitoring, showing that patients with favorable Prospera dd-cfDNA trends were 60 times more likely to have positive outcomes.

Natera’s clinical pipeline in gastrointestinal cancers also showed promising results, with recent publications demonstrating Signatera’s effectiveness in gastroesophageal and liver cancers, including diagnostic lead times of 6 months and up to 16.5 months ahead of imaging, respectively.

AI Strategy and Implementation

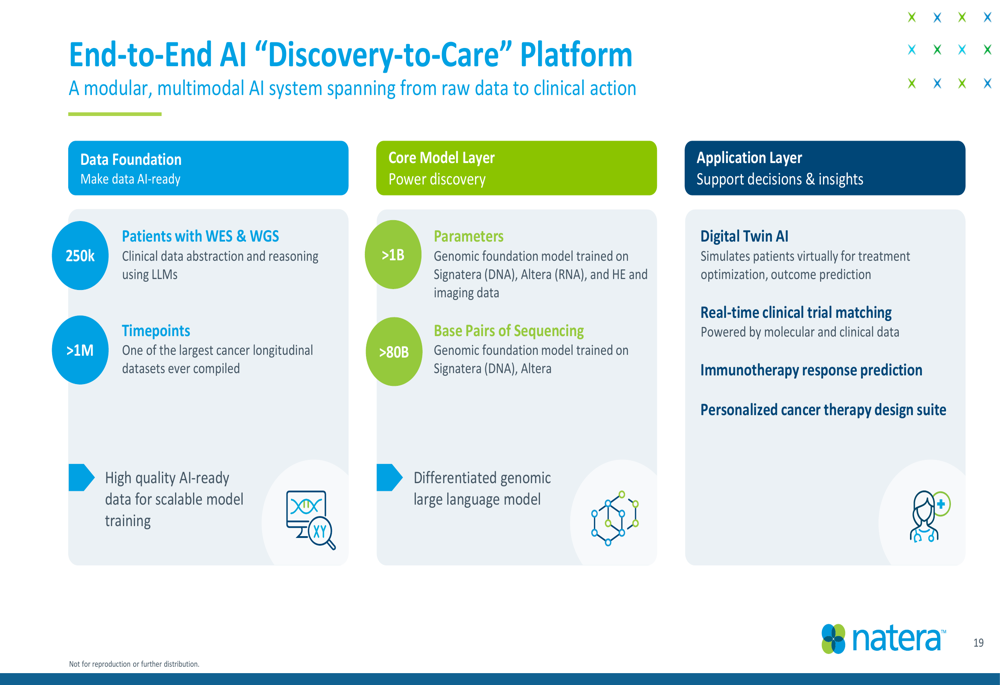

A key strategic focus for Natera is its investment in artificial intelligence across the organization. The company has developed an end-to-end AI "Discovery-to-Care" Platform structured around three main layers: Data Foundation, Core Model Layer, and Application Layer.

The comprehensive AI platform is illustrated here:

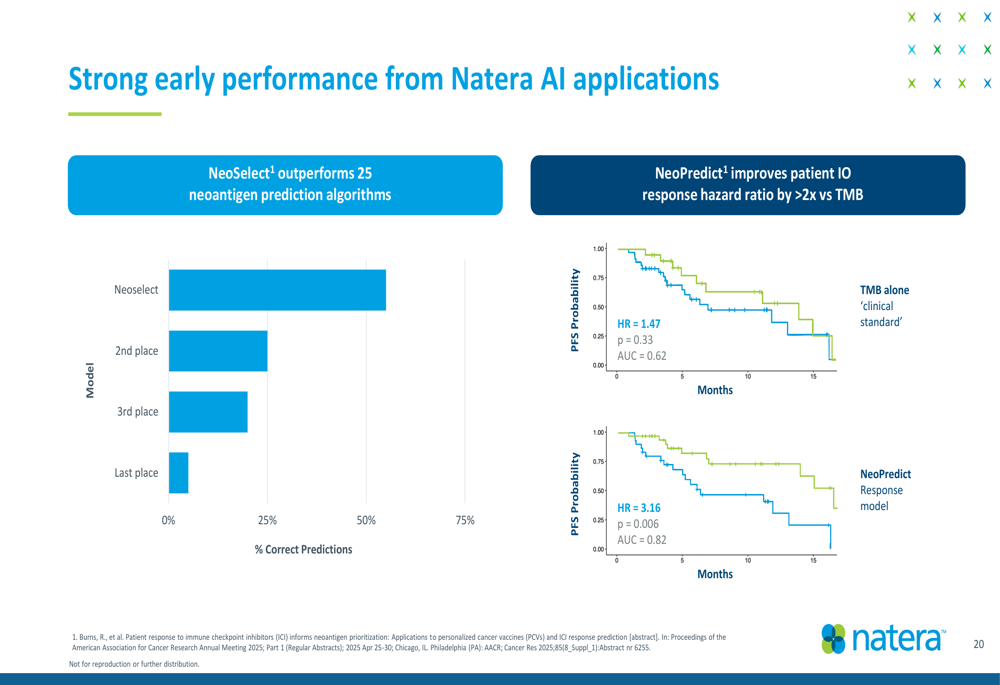

Early results from Natera’s AI applications are promising. The company reported that its NeoSelect algorithm outperforms 25 neoantigen prediction algorithms, while NeoPredict improves patient immunotherapy response hazard ratio by more than 2x compared to tumor mutation burden (TMB), the current clinical standard.

The performance comparison is visualized in the following chart:

Natera is deploying AI across three main areas: efficiency (targeting ~$200 million in value), user experience (improving patient and provider interactions), and clinical applications (developing biomarkers and clinical decision-making tools).

Financial Outlook and Guidance

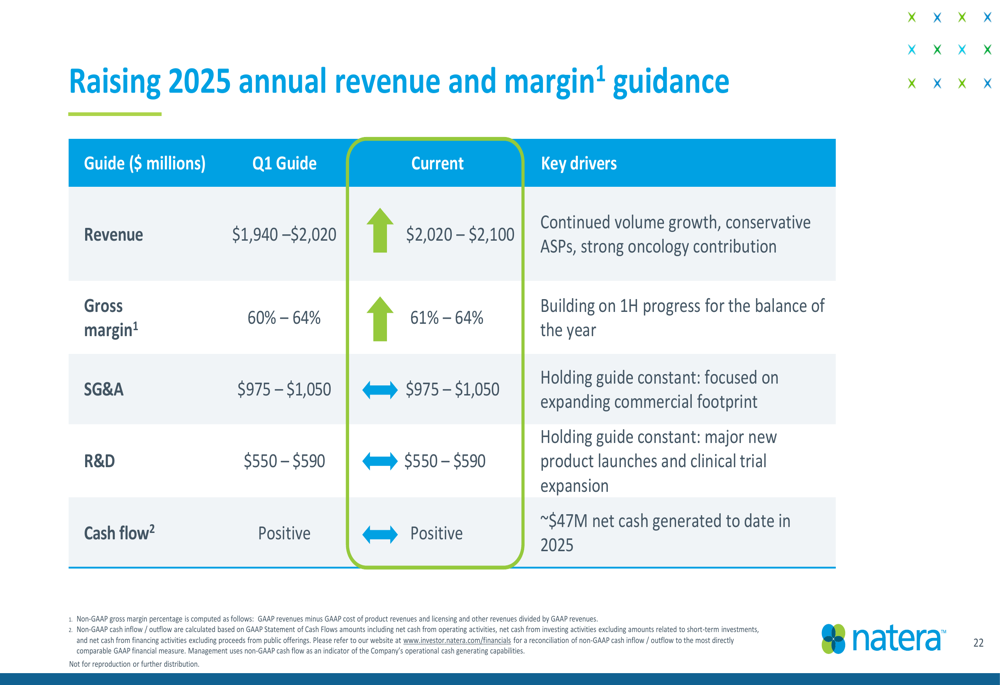

Based on its strong Q2 performance, Natera raised its full-year 2025 guidance. The company now expects annual revenue between $2.02 billion and $2.1 billion, up from its previous guidance of $1.94 billion to $2.02 billion provided after Q1 results.

The updated guidance is summarized in the following slide:

Gross margin guidance was also improved to 61%-64% (from 60%-64%), while SG&A and R&D expense projections remained unchanged at $975-$1,050 million and $550-$590 million, respectively. The company continues to expect positive cash flow for the full year.

Natera identified several drivers for future margin expansion, including revenue cycle operations (which have generated ~$300 million in recurring revenues and cash flow since 2022), coverage expansion for additional tumor types (representing a $250-$300 million opportunity), cost of goods sold reduction programs, and AI-driven efficiencies.

The company’s strong financial position and growth trajectory, combined with its expanding product portfolio and clinical evidence base, appear to be resonating with investors, as evidenced by the significant premarket stock movement following the earnings release.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.