TSX gains on big banks strength

Introduction & Market Context

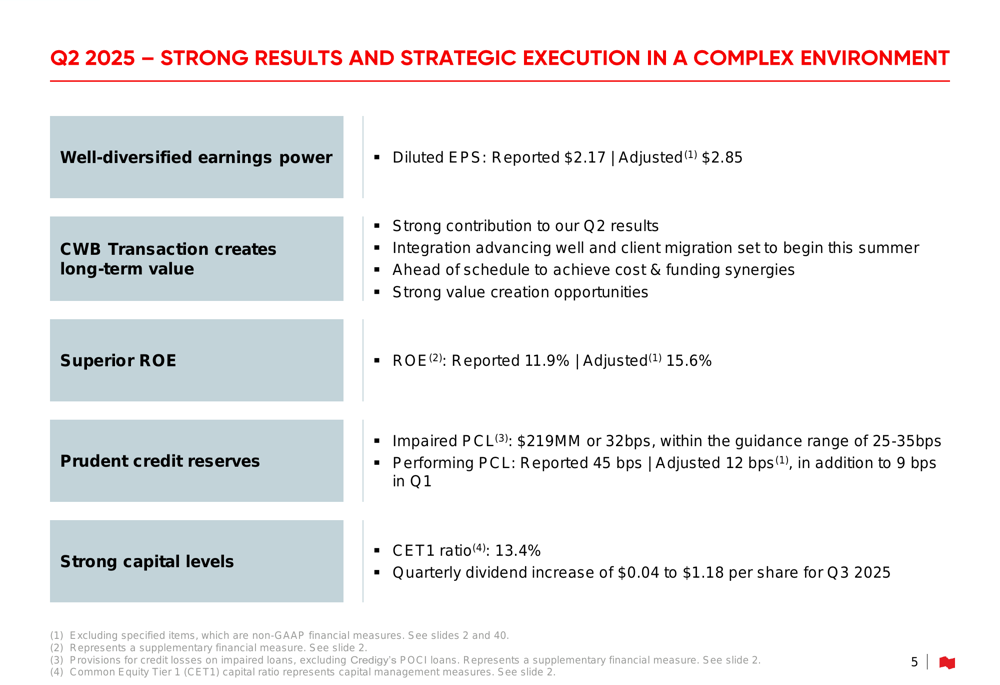

National Bank of Canada (TSX:NA) presented its second quarter 2025 results on May 28, 2025, highlighting strong performance across all business segments. The quarter was notably marked by the integration of Canadian Western Bank (TSX:CWB), following the transaction’s closing on February 3, 2025. The bank reported diluted earnings per share (EPS) of $2.17 on a reported basis and $2.85 on an adjusted basis, with a return on equity (ROE) of 11.9% reported and 15.6% adjusted.

As shown in the following summary of Q2 2025 results, the bank delivered strong performance while advancing its strategic initiatives:

Quarterly Performance Highlights

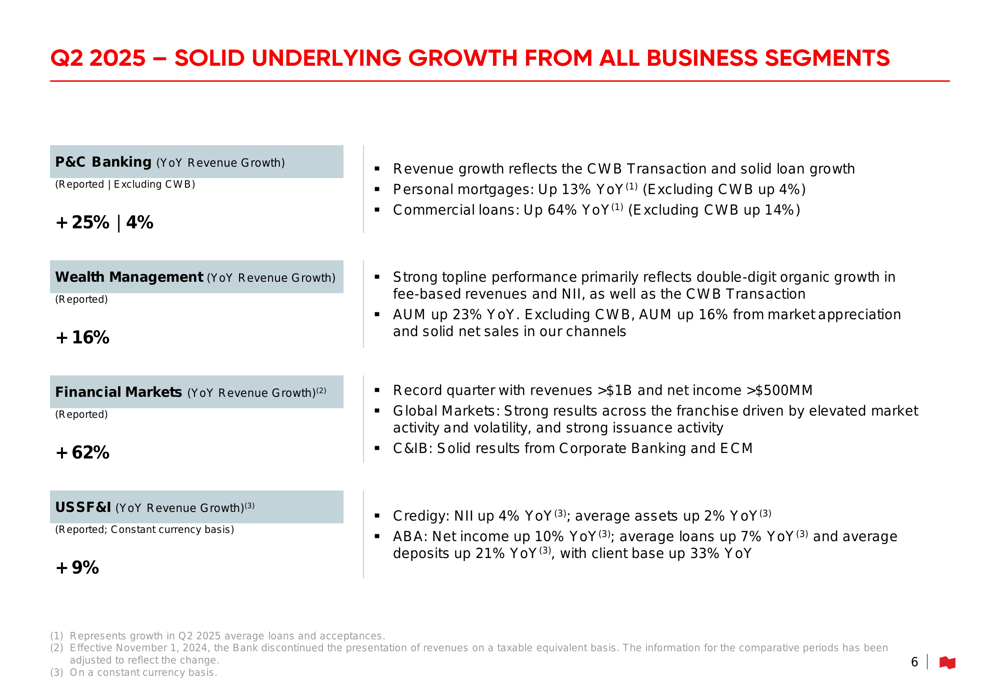

National Bank reported significant revenue growth across all business segments in Q2 2025, with particularly strong performance in Financial Markets, which delivered a record quarter with revenues exceeding $1 billion. The Personal & Commercial (P&C) Banking segment saw revenues increase by 25% year-over-year, while Wealth Management and U.S. Specialty Finance and International (USSF&I) segments grew by 16% and 9% respectively.

The following chart illustrates the underlying growth across all business segments:

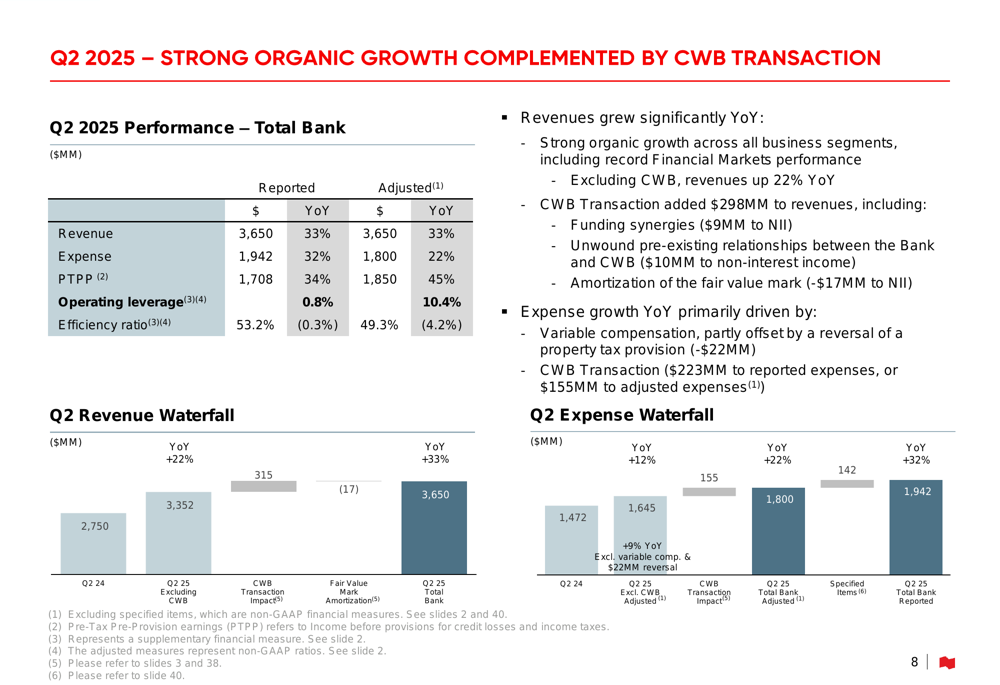

The bank’s strong organic growth was complemented by the CWB transaction, which added $298 million to revenues. Excluding CWB, revenues were up 22% year-over-year, demonstrating robust organic performance. The Financial Markets segment delivered exceptional results, with revenues up 62% year-over-year, driven by elevated market activity, volatility, and strong issuance activity.

As illustrated in this revenue and expense breakdown, both organic growth and the CWB acquisition contributed to the bank’s performance:

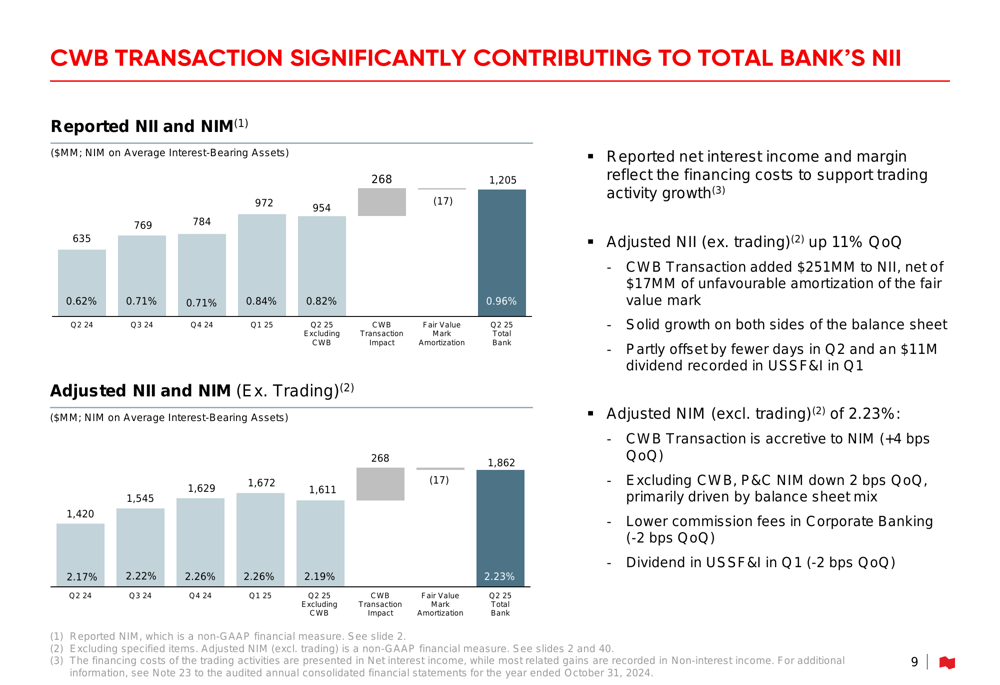

The CWB transaction has significantly contributed to the bank’s net interest income (NII), adding $251 million in the quarter, net of $17 million of unfavorable amortization of the fair value mark. The adjusted net interest margin (NIM) excluding trading was 2.23%, with the CWB transaction being accretive to NIM by 4 basis points quarter-over-quarter.

The following chart shows how the CWB transaction has enhanced the bank’s NII:

Strategic Initiatives

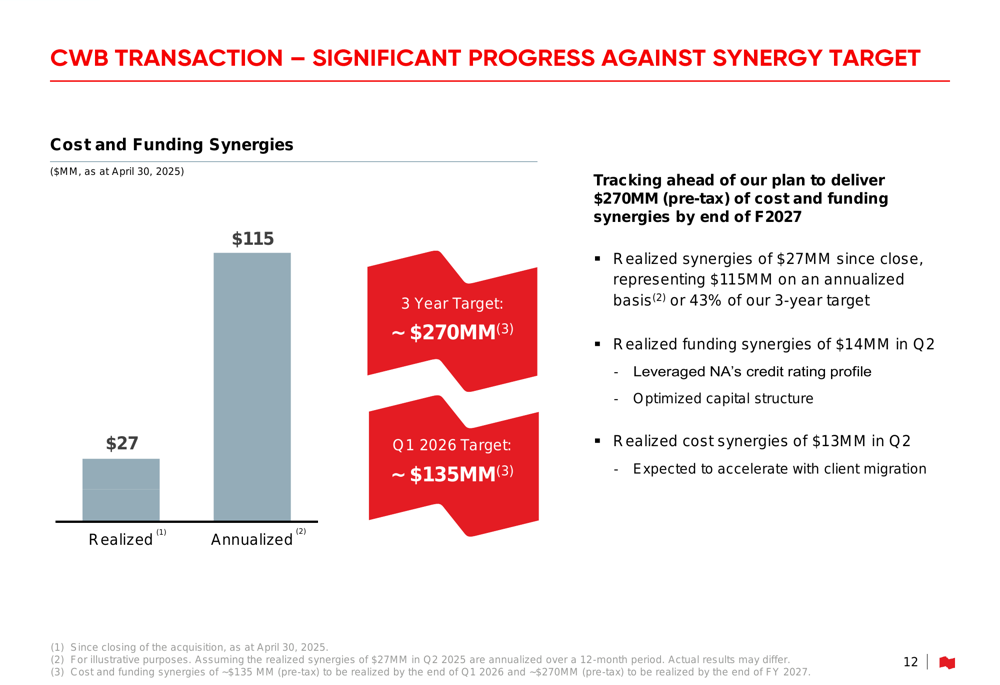

The integration of CWB is progressing well, with client migration set to begin in the summer of 2025. The bank is tracking ahead of plan to deliver $270 million (pre-tax) of cost and funding synergies by the end of fiscal 2027. Since the closing of the transaction, National Bank has realized synergies of $27 million, representing $115 million on an annualized basis or 43% of its three-year target.

The bank has realized funding synergies of $14 million in Q2 through leveraging National Bank’s credit rating profile and optimizing its capital structure. Cost synergies of $13 million were also realized in Q2, with expectations for acceleration as client migration progresses.

As shown in the following chart, the bank is making significant progress against its synergy targets:

Detailed Financial Analysis

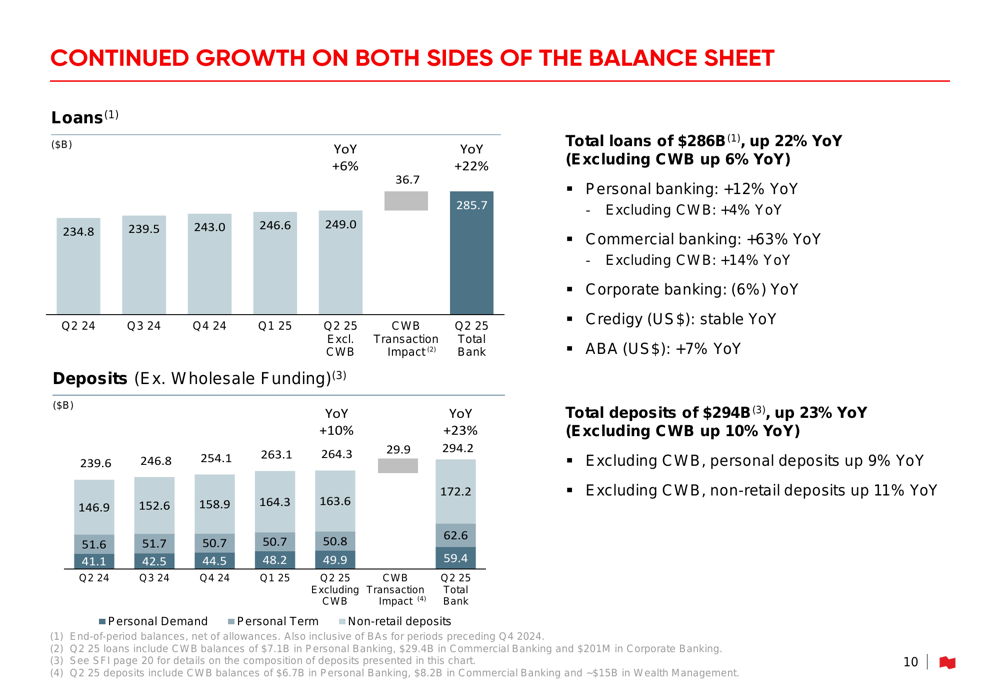

National Bank continues to demonstrate strong growth on both sides of the balance sheet. Total (EPA:TTEF) loans reached $286 billion, up 22% year-over-year (6% excluding CWB), while total deposits grew to $294 billion, up 23% year-over-year (10% excluding CWB). Personal banking loans increased by 12% year-over-year, while commercial banking loans surged by 63% year-over-year, largely due to the CWB acquisition.

The following chart illustrates the growth in loans and deposits:

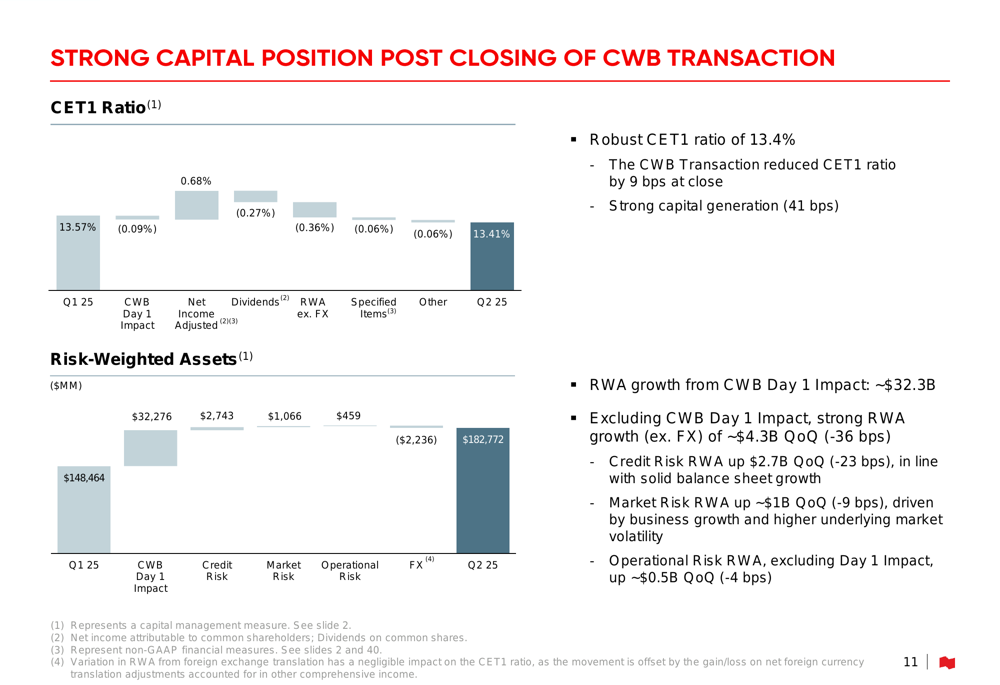

The bank maintains a strong capital position with a Common Equity Tier 1 (CET1) ratio of 13.4%. The CWB transaction reduced the CET1 ratio by only 9 basis points at close, which was more than offset by strong capital generation of 41 basis points during the quarter.

The bank’s robust capital position is illustrated in the following chart:

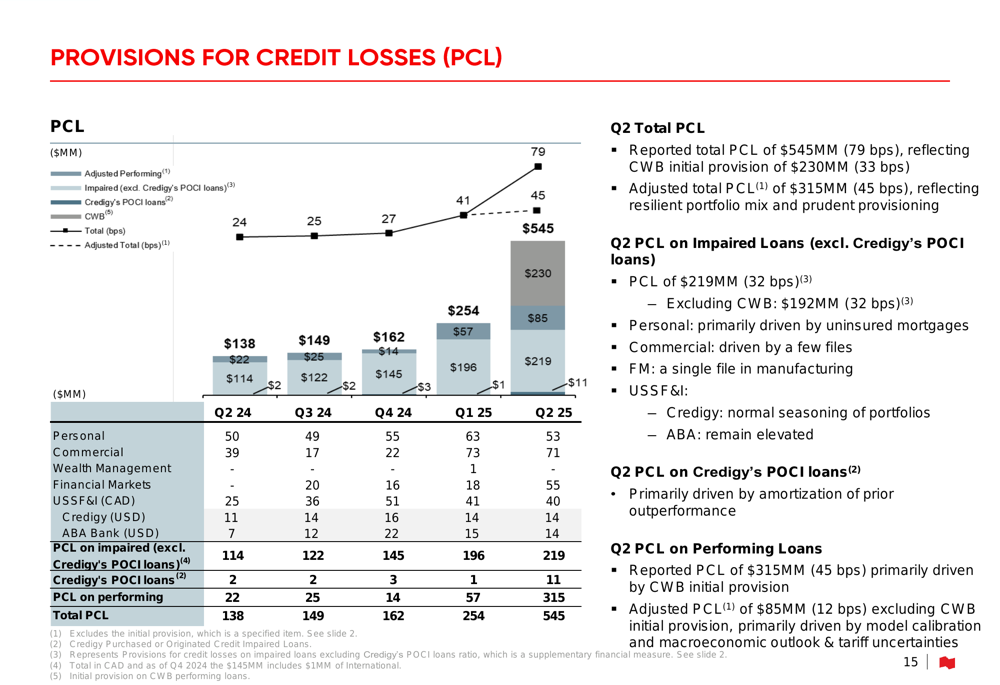

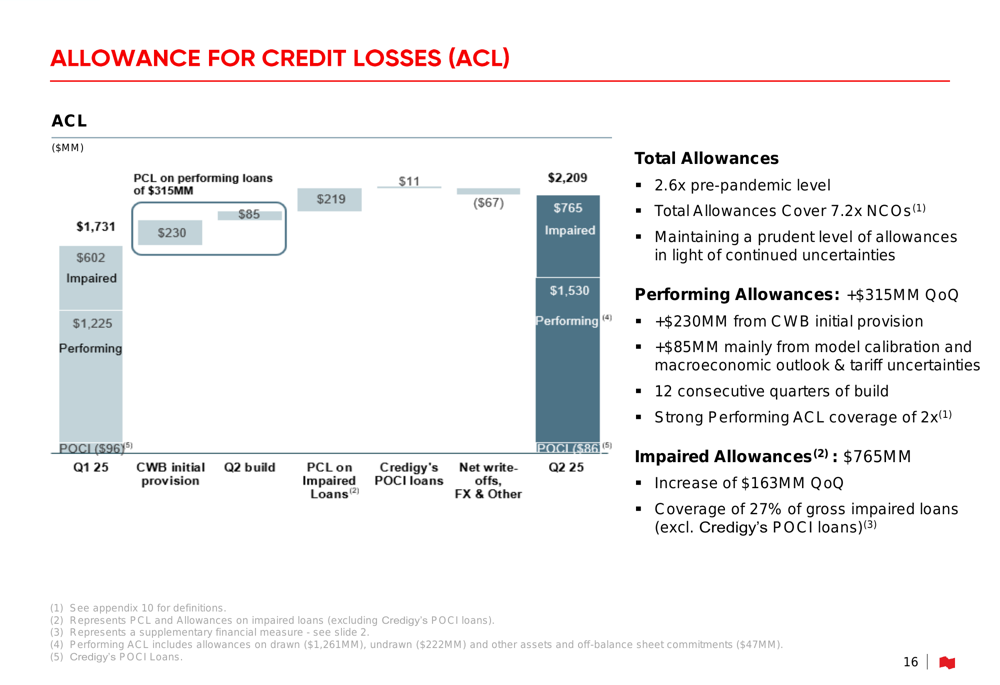

In terms of credit quality, the bank reported total provisions for credit losses (PCL) of $545 million (79 basis points), which includes the CWB initial provision of $230 million (33 basis points). Adjusted total PCL was $315 million (45 basis points). PCL on impaired loans was $219 million (32 basis points), which is within the bank’s guidance range of 25-35 basis points.

The breakdown of provisions for credit losses is shown in the following chart:

The bank continues to maintain prudent allowances for credit losses, which are now 2.6 times the pre-pandemic level. Total allowances cover 7.2 times net charge-offs, reflecting the bank’s conservative approach to credit risk in light of continued economic uncertainties. Performing allowances increased by $315 million quarter-over-quarter, with $230 million from the CWB initial provision and $85 million mainly from model calibration and macroeconomic outlook considerations.

The following chart details the allowance for credit losses:

Forward-Looking Statements

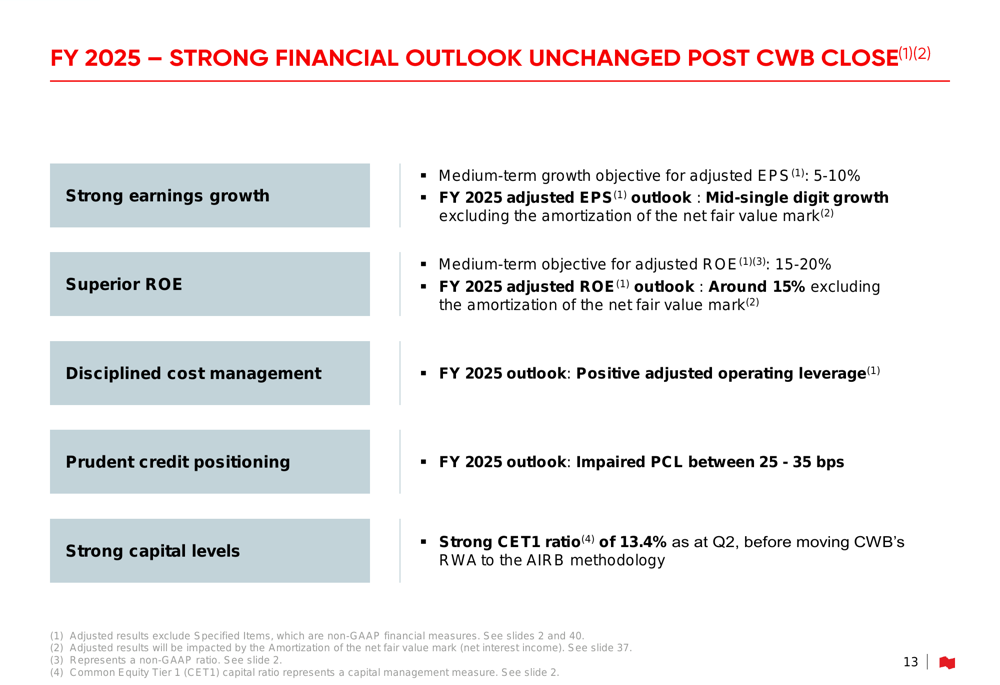

National Bank’s financial outlook for fiscal 2025 remains strong and unchanged following the CWB acquisition. The bank maintains its medium-term growth objective for adjusted EPS at 5-10%, with fiscal 2025 adjusted EPS expected to show mid-single-digit growth excluding the amortization of the net fair value mark.

The medium-term objective for adjusted ROE is 15-20%, with fiscal 2025 adjusted ROE expected to be around 15% excluding the amortization of the net fair value mark. The bank also anticipates positive adjusted operating leverage for fiscal 2025 and expects impaired PCL to remain between 25-35 basis points.

The bank’s financial outlook is summarized in the following chart:

In conclusion, National Bank of Canada delivered strong second quarter results for 2025, with robust performance across all business segments. The successful integration of CWB is progressing ahead of schedule, contributing significantly to the bank’s growth while maintaining a strong capital position and prudent approach to credit risk. The bank’s diversified business model and strategic execution position it well for continued growth in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.