S&P 500 slips, but losses kept in check as Nvidia climbs ahead of results

Introduction & Market Context

Cloud banking software provider nCino (NASDAQ:NCNO) released its first quarter fiscal year 2026 results on May 28, 2025, showing stronger-than-expected performance across key metrics. The company reported total revenues of $144.1 million, exceeding its guidance and representing 13% year-over-year growth. This positive performance comes after a challenging fourth quarter of fiscal 2025, when the company missed EPS expectations, causing a significant stock drop.

nCino’s shares traded at $26.6 in after-hours trading following the earnings release, down slightly by 0.67%. The stock has been trading well below its 52-week high of $43.20, as investors have been cautious about the company’s growth trajectory amid changing market conditions in the banking technology sector.

Quarterly Performance Highlights

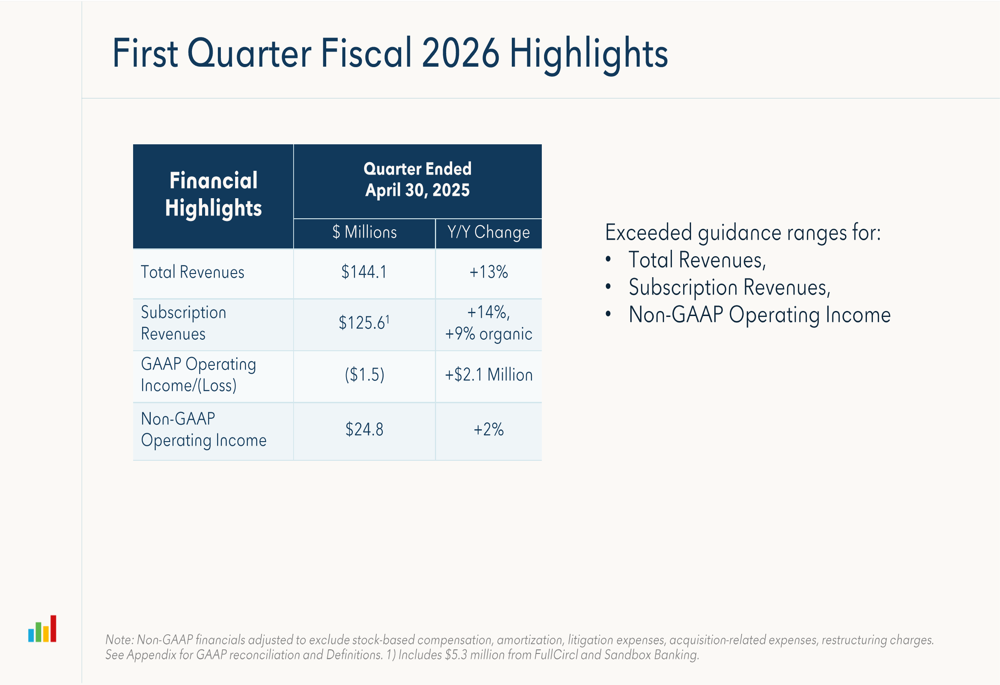

nCino exceeded its guidance ranges for the first quarter across all key metrics. Total (EPA:TTEF) revenues reached $144.1 million, up 13% year-over-year, while subscription revenues grew to $125.6 million, representing a 14% increase (9% organic growth). The company posted a GAAP operating loss of $1.5 million, which was an improvement of $2.1 million compared to the same period last year. Non-GAAP operating income was $24.8 million, up 2% year-over-year.

As shown in the following chart of quarterly financial highlights:

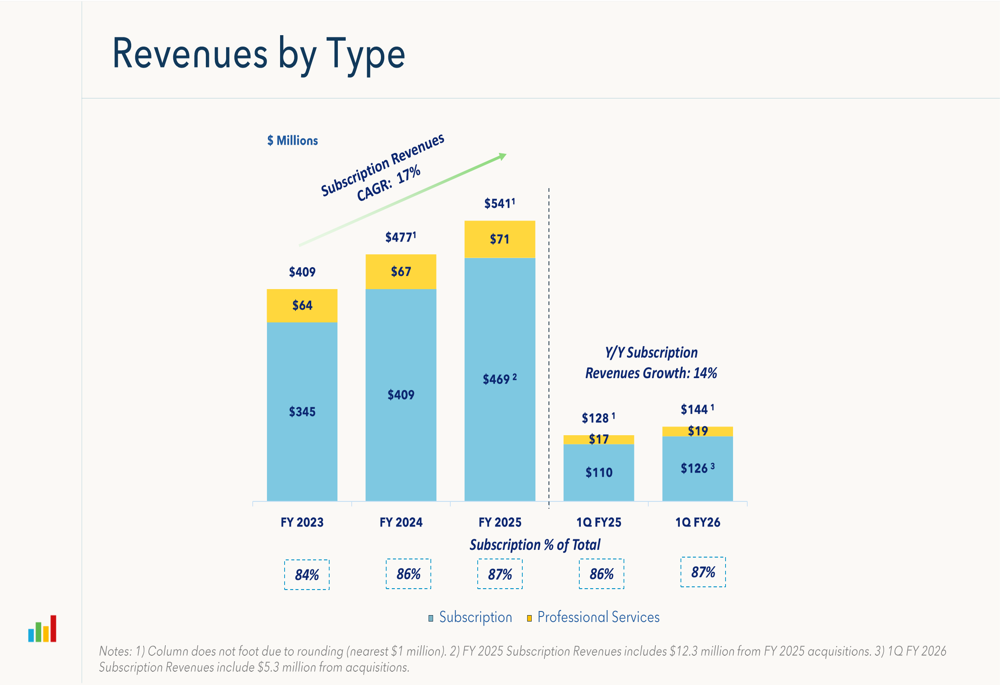

Subscription revenues continued to dominate nCino’s revenue mix, accounting for 87% of total revenues in Q1 FY26, up from 86% in the same quarter last year. This reflects the company’s strategic focus on building a stable, recurring revenue base. Professional services revenues contributed the remaining 13%, reaching $19 million for the quarter.

The following chart illustrates the company’s revenue composition over time:

Detailed Financial Analysis

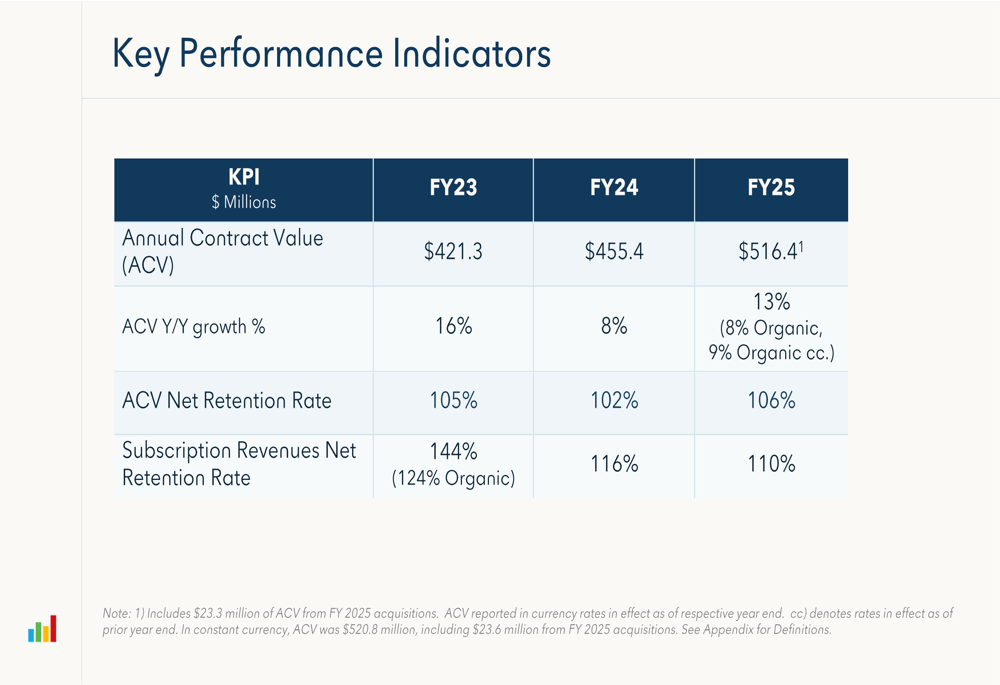

nCino’s Annual Contract Value (ACV) reached $516.4 million in fiscal year 2025, representing 13% year-over-year growth (8% organic). The company’s ACV Net Retention Rate improved to 106% in FY25, up from 102% in FY24, indicating stronger customer retention and expansion.

The key performance indicators below show the company’s consistent growth trajectory:

Looking at subscription revenues by source, nCino continues to see growth in both its core banking business and U.S. mortgage segment, though at different rates. Subscription revenues excluding U.S. mortgage reached $107 million in Q1 FY26, while U.S. mortgage subscription revenues were $19 million.

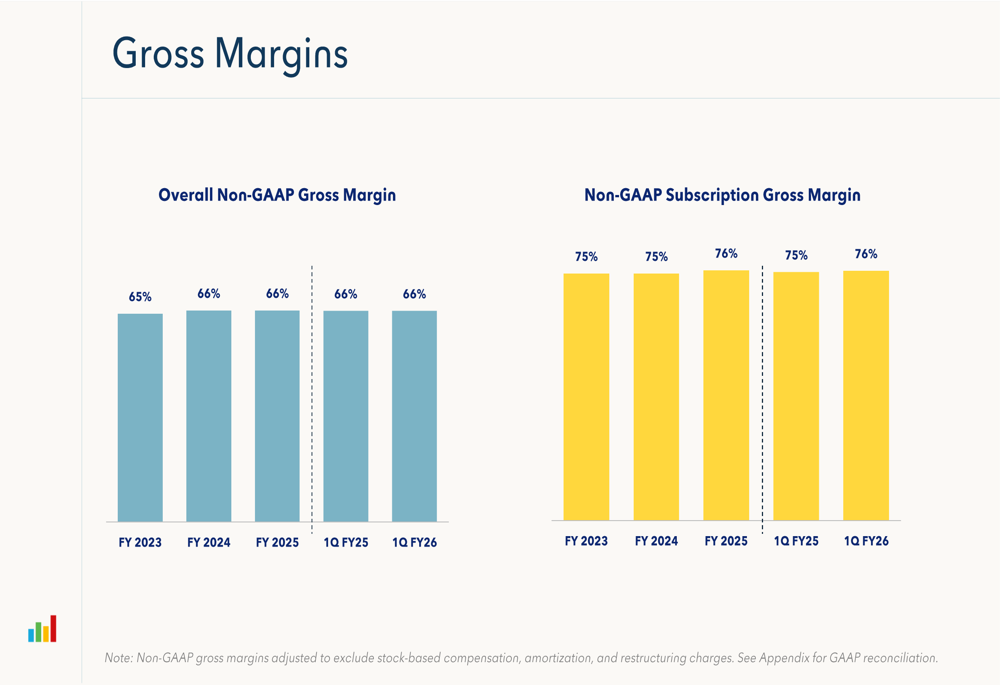

The company’s gross margins remained stable, with overall non-GAAP gross margin at 66% and subscription gross margin at 76% for Q1 FY26. This consistency in margins demonstrates nCino’s ability to scale efficiently while maintaining profitability.

The following chart shows the company’s gross margin performance:

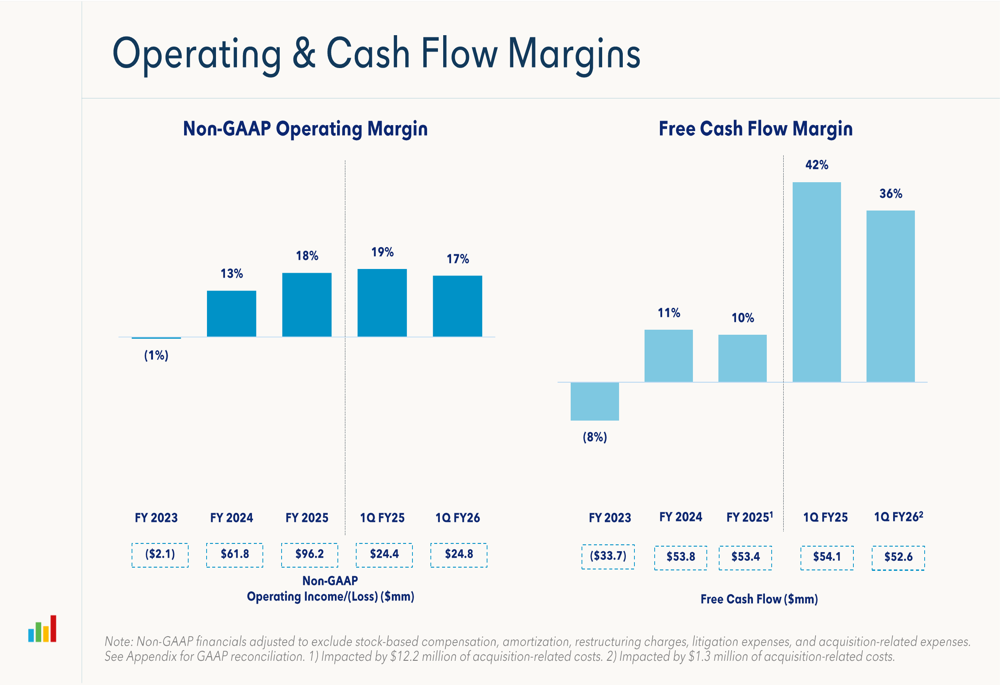

Operating and cash flow margins have shown significant improvement over time. Non-GAAP operating margin was 17% in Q1 FY26, compared to -1% in FY23, reflecting the company’s successful efforts to improve operational efficiency. Free cash flow margin was an impressive 36% in Q1 FY26, though down slightly from 42% in the same quarter last year.

These profitability metrics are illustrated in the following chart:

Strategic Initiatives & Growth Drivers

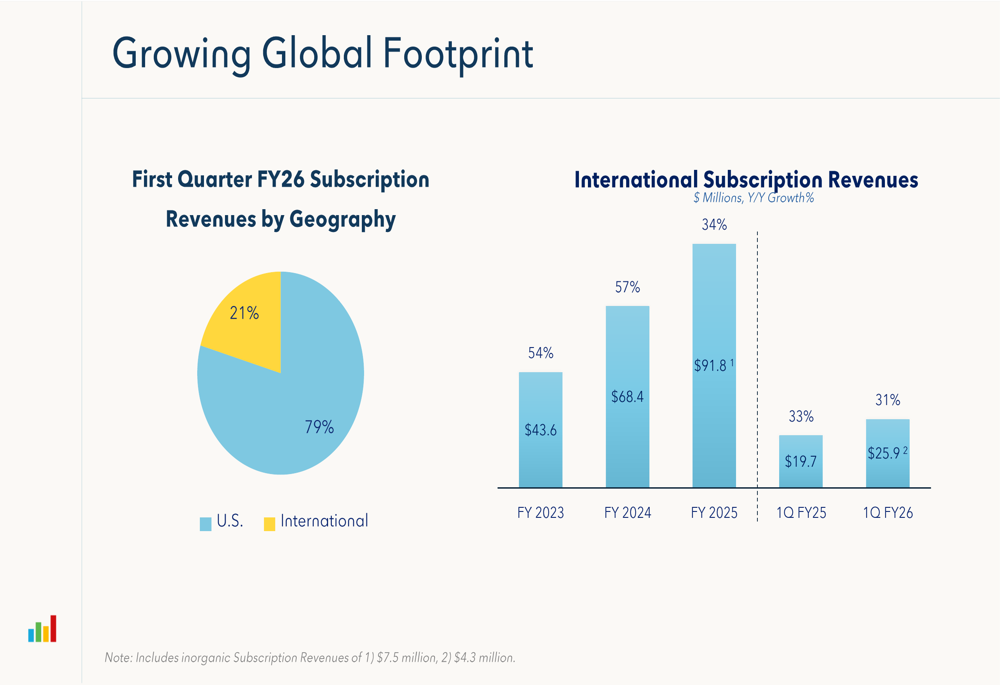

International expansion remains a key growth driver for nCino. International subscription revenues accounted for 21% of total subscription revenues in Q1 FY26, up from previous periods. The company’s international subscription revenues reached $25.9 million in Q1 FY26, compared to $19.7 million in Q1 FY25, representing strong growth in global markets.

The company’s global footprint is illustrated in the following chart:

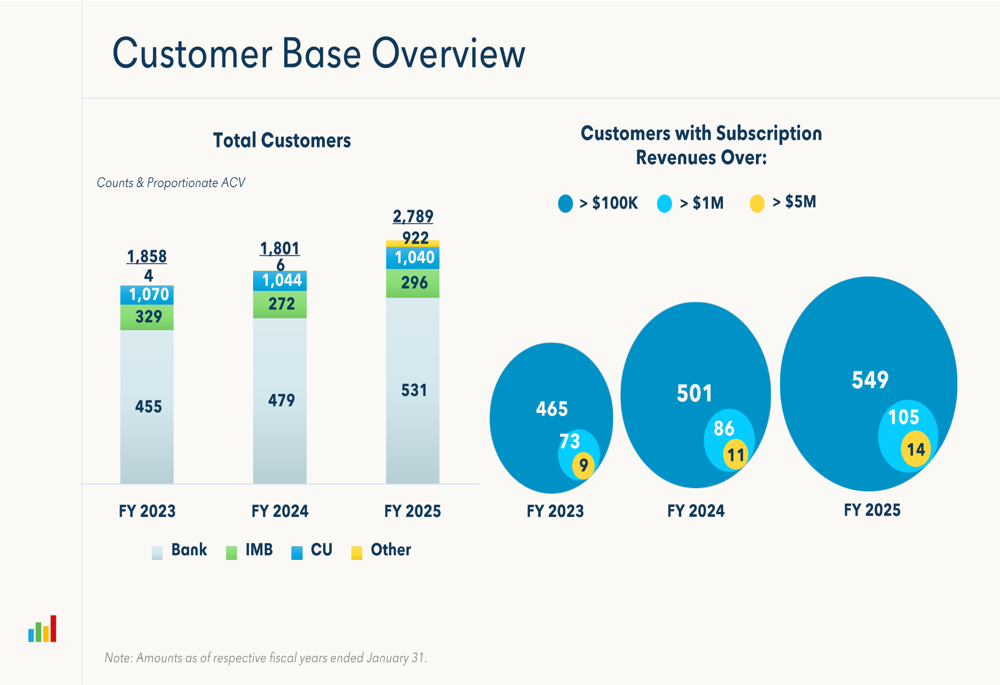

nCino is also focusing on expanding its customer base while increasing the value of existing customer relationships. The company reported 2,789 total customers in FY25, with 105 customers generating subscription revenues over $1 million, up from 86 in FY24. This trend of growing high-value customer relationships is crucial for nCino’s long-term growth strategy.

The customer base overview is shown in the following chart:

The company is strategically investing in growth while maintaining financial discipline. Sales and marketing expenses were 18% of revenues in Q1 FY26, research and development was 20%, and general and administrative expenses were 11%. These investments are designed to support future growth while maintaining the company’s improving profitability profile.

Forward-Looking Statements

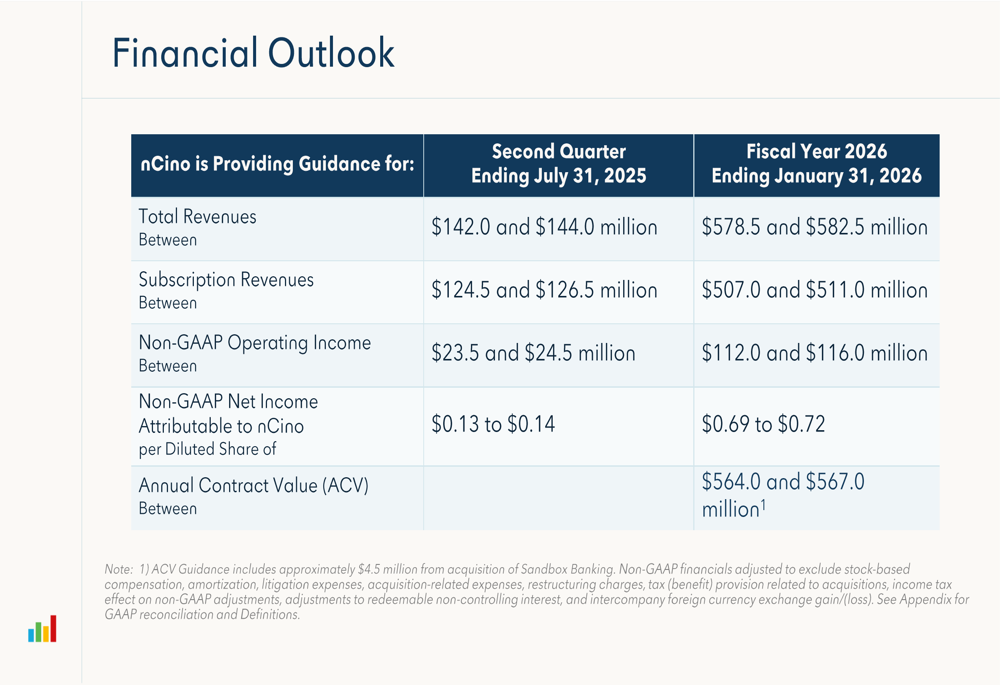

nCino provided guidance for both the second quarter of fiscal 2026 and the full fiscal year. For Q2 FY26, the company expects total revenues between $142.0 and $144.0 million and subscription revenues between $124.5 and $126.5 million. For the full fiscal year 2026, nCino projects total revenues of $578.5 to $582.5 million and subscription revenues of $507.0 to $511.0 million.

The company’s financial outlook is summarized in the following chart:

For fiscal year 2026, nCino expects ACV growth of 9-10% (8-9% organic) and subscription revenue growth excluding U.S. mortgage of 9-10%. The company is planning to invest $10 million in sales and marketing initiatives to drive future growth, while maintaining 0% growth in professional services revenues.

These guidance figures suggest that nCino is taking a measured approach to growth expectations, focusing on sustainable expansion rather than aggressive targets. This aligns with statements from the company’s new CEO, Sean Desmond, who in the previous earnings call emphasized a focus on execution and AI opportunities rather than "selling a dream."

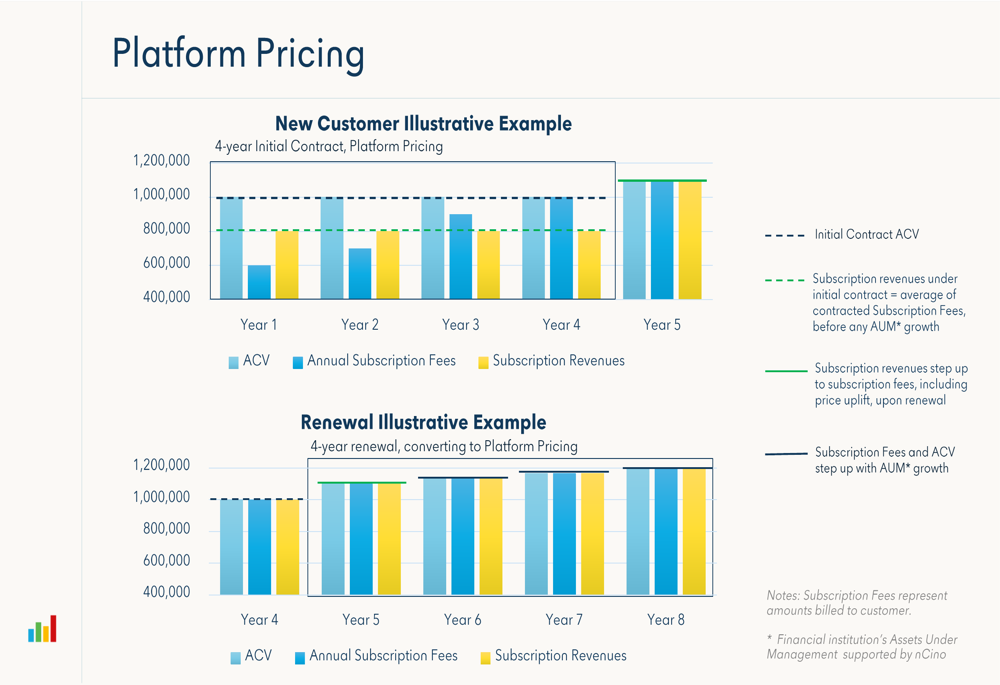

The company’s approach to platform pricing, which is illustrated in the presentation, shows how nCino is working to optimize revenue recognition and customer value over multi-year contracts:

nCino’s Q1 FY26 results demonstrate that the company is making progress on its strategic initiatives while maintaining strong financial discipline. The focus on subscription revenue growth, international expansion, and improving profitability metrics positions the company well for sustainable long-term growth in the competitive cloud banking software market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.