Raymond James raises Fulgent Genetics stock price target to $36 on strong performance

NCR Atleos Corp (NYSE:NATL) reported mixed third-quarter 2025 results, with strong earnings growth counterbalanced by a revenue shortfall that sent shares down 6.48% in regular trading on November 6, with an additional 3.49% decline in after-hours trading.

Quarterly Performance Highlights

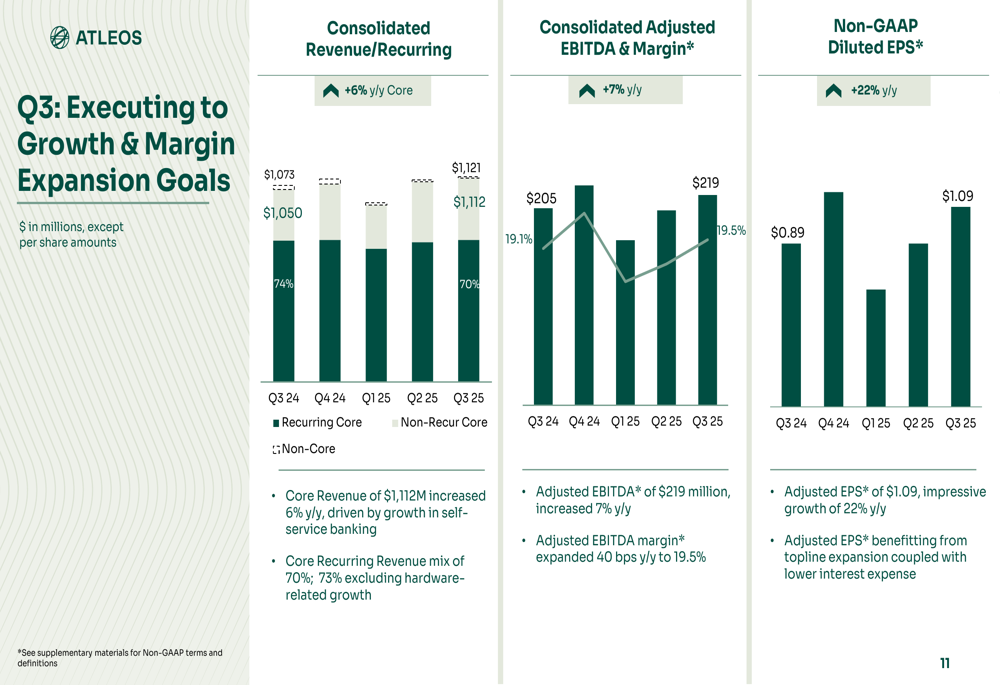

The banking technology provider reported adjusted earnings per share of $1.09, representing 22% year-over-year growth and meeting analyst expectations. However, revenue of $1.12 billion missed forecasts of $1.16 billion, resulting in a 3.45% shortfall that concerned investors.

Despite the revenue miss, NCR Atleos highlighted several positive financial metrics in its earnings presentation. Core revenue grew 6% year-over-year, while adjusted EBITDA increased by 7% to $219 million, with margins expanding by 40 basis points to 19.5%.

As shown in the following chart detailing the company’s financial performance:

The company’s recurring revenue mix reached 70% of total revenue (73% excluding hardware-related revenue), demonstrating progress in the company’s strategic shift toward more predictable revenue streams.

Segment Performance

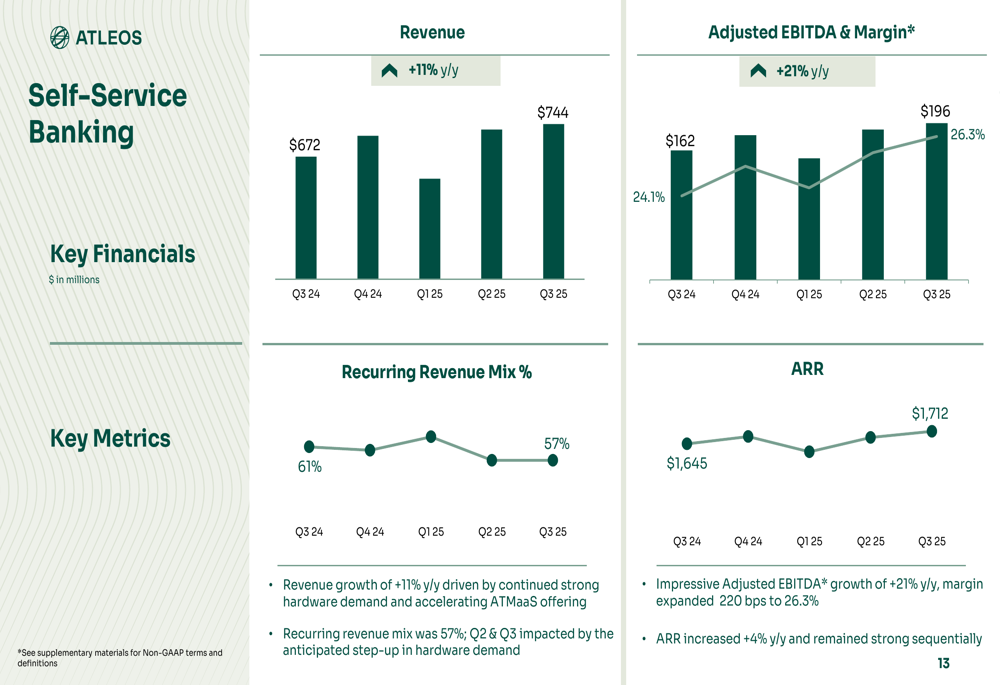

NCR Atleos reported divergent performance across its business segments. The Self-Service Banking segment, which represents the company’s core ATM business, delivered strong results with 11% year-over-year revenue growth to $744 million and a 21% increase in adjusted EBITDA.

The following chart illustrates the Self-Service Banking segment’s performance:

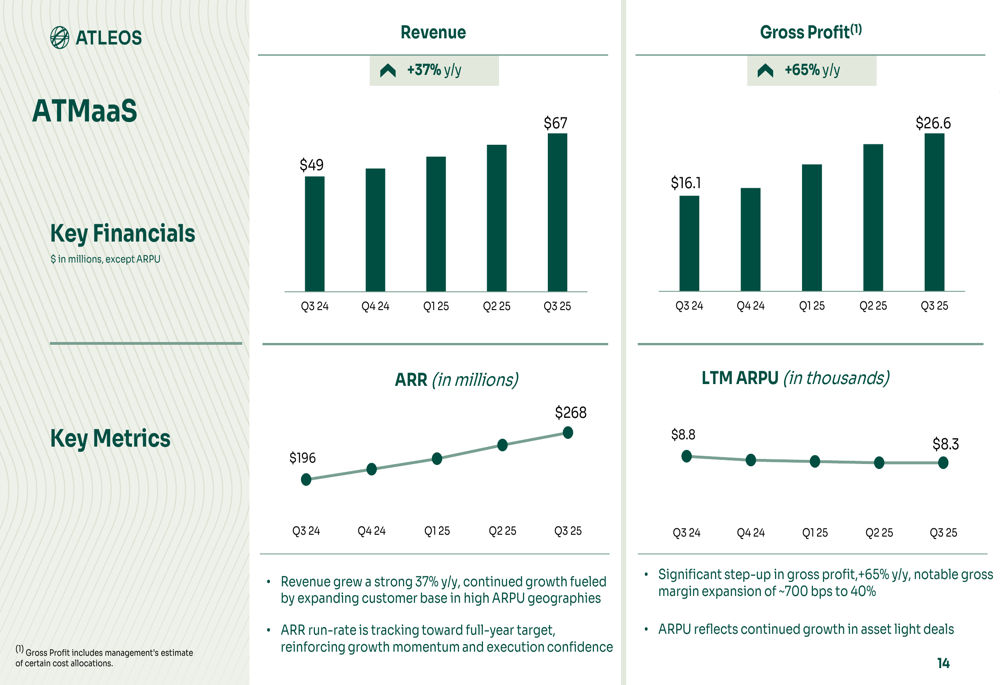

The company’s strategic ATM as a Service (ATMaaS) business showed particularly impressive growth, with revenue increasing 37% year-over-year and gross profit surging 65% to $26.6 million. Annual recurring revenue (ARR) for this segment reached $268 million.

The ATMaaS performance metrics demonstrate the success of this strategic initiative:

However, the Network segment experienced a 1% year-over-year revenue decline to $332 million, which the company attributed to the impact of U.S. immigration policy changes. Despite this challenge, the segment maintained strong ARPU (Average Revenue Per Unit), which increased 2% year-over-year.

Strategic Initiatives

NCR Atleos emphasized its position as a leader in the self-service banking solutions market, highlighting its installed base of over 500,000 self-service ATMs and its status as the #1 ATMaaS and Managed Services Provider.

The company’s strategic positioning and growth strategy are illustrated in this overview:

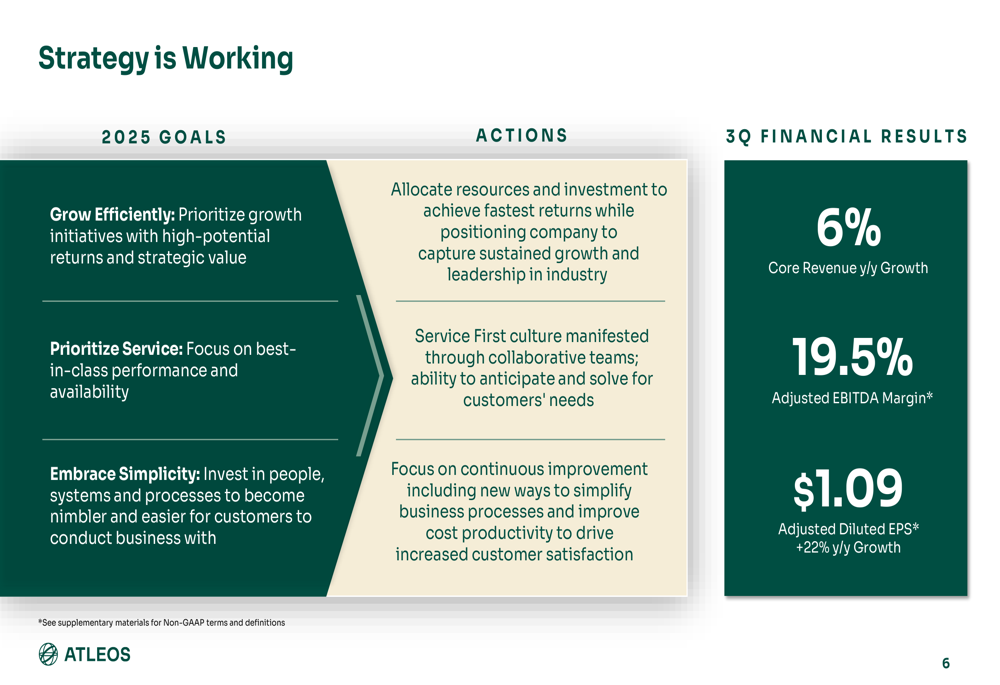

The presentation outlined the company’s three-pronged strategy: Grow Efficiently, Prioritize Service, and Embrace Simplicity. Management reported that this strategy is yielding results, as evidenced by the financial performance metrics.

As shown in the following strategy implementation overview:

A key strategic focus remains the expansion of the ATMaaS business, with the company reporting 40+ new customers and $195 million in new Total Contract Value (TCV) in Q3. During the earnings call, CEO Tim Oliver highlighted the ATMaaS opportunity, stating, "We are the obvious choice to take on [cash ecosystem] work," and noting that the hardware business is "killing it right now."

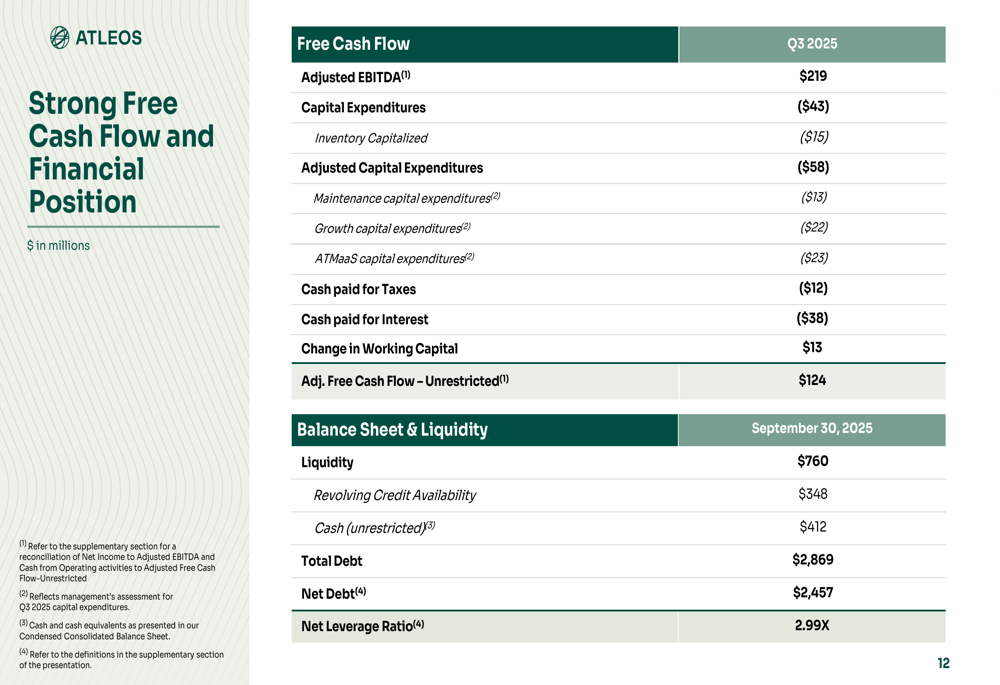

Financial Position and Capital Allocation

NCR Atleos reported strong free cash flow of $124 million for Q3 2025, supporting its improved financial position. The company’s balance sheet showed $760 million in liquidity, including $412 million in cash and $348 million in revolving credit availability.

The detailed breakdown of the company’s cash flow and financial position is shown here:

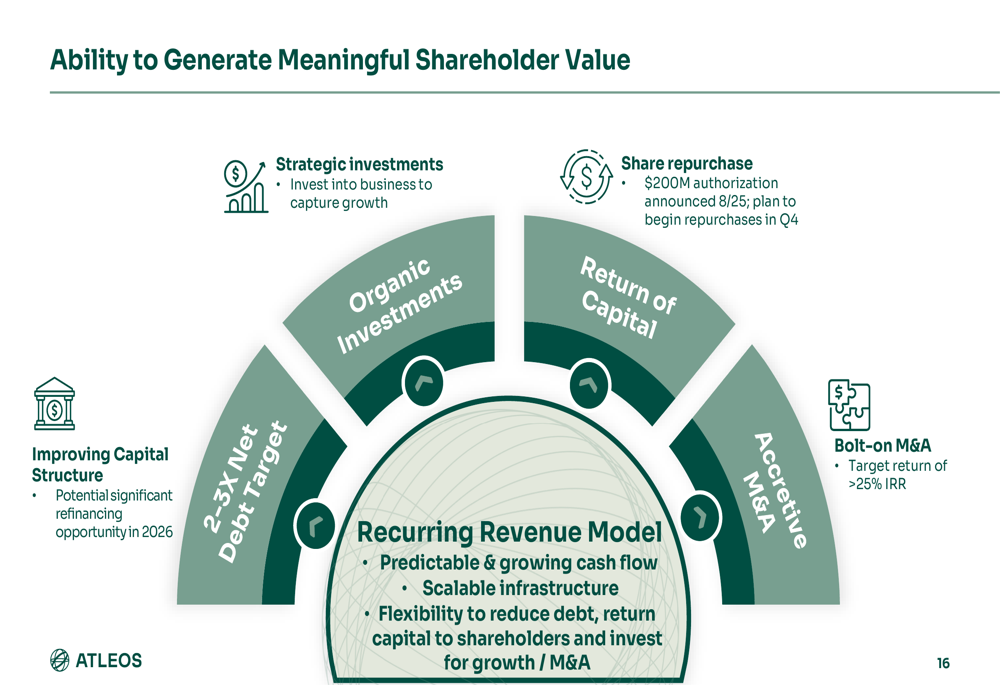

The company’s net leverage ratio improved to 2.99x, reflecting progress in strengthening the balance sheet following its separation from legacy NCR. Management outlined its capital allocation strategy, which includes improving the capital structure, strategic investments, and returning value to shareholders through a $200 million share repurchase authorization announced in August 2025.

The company’s approach to shareholder value creation is illustrated in this overview:

Forward-Looking Statements

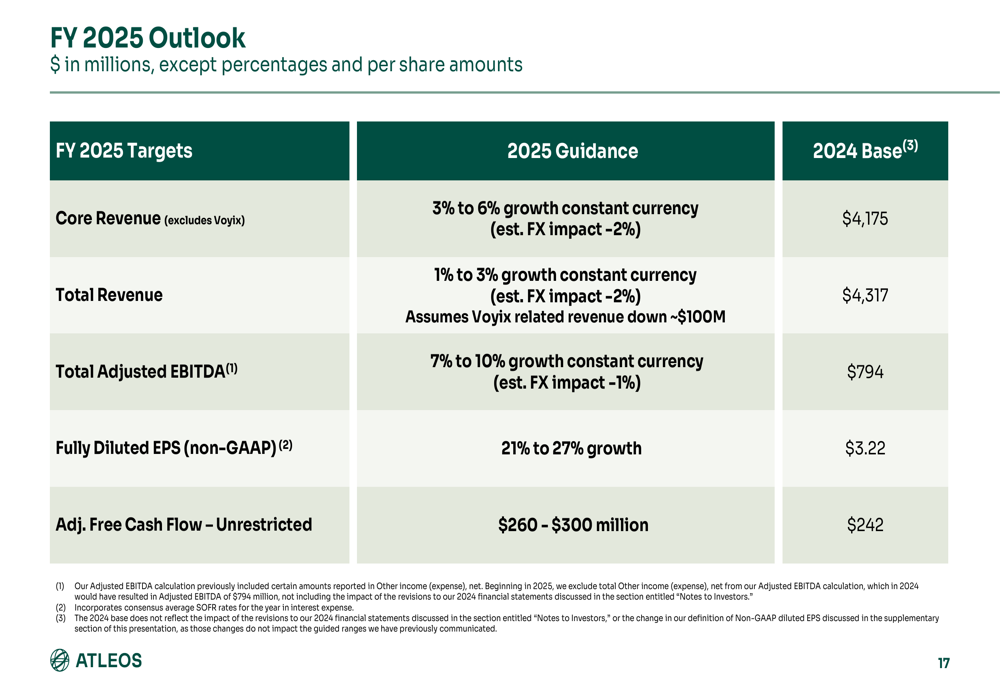

NCR Atleos reaffirmed its full-year 2025 guidance, projecting core revenue growth of 3-6% in constant currency, total revenue growth of 1-3%, and adjusted EBITDA growth of 7-10%. The company expects fully diluted non-GAAP EPS growth of 21-27% and adjusted free cash flow of $260-300 million.

The detailed fiscal year 2025 outlook is presented here:

Looking beyond 2025, management projects continued strong growth in the ATMaaS segment, with expectations of 40% growth in Q4 2025 and into 2026. The company is targeting a free cash flow conversion rate of 35% in 2026 and anticipates potential benefits from tariff reductions.

Investment Thesis

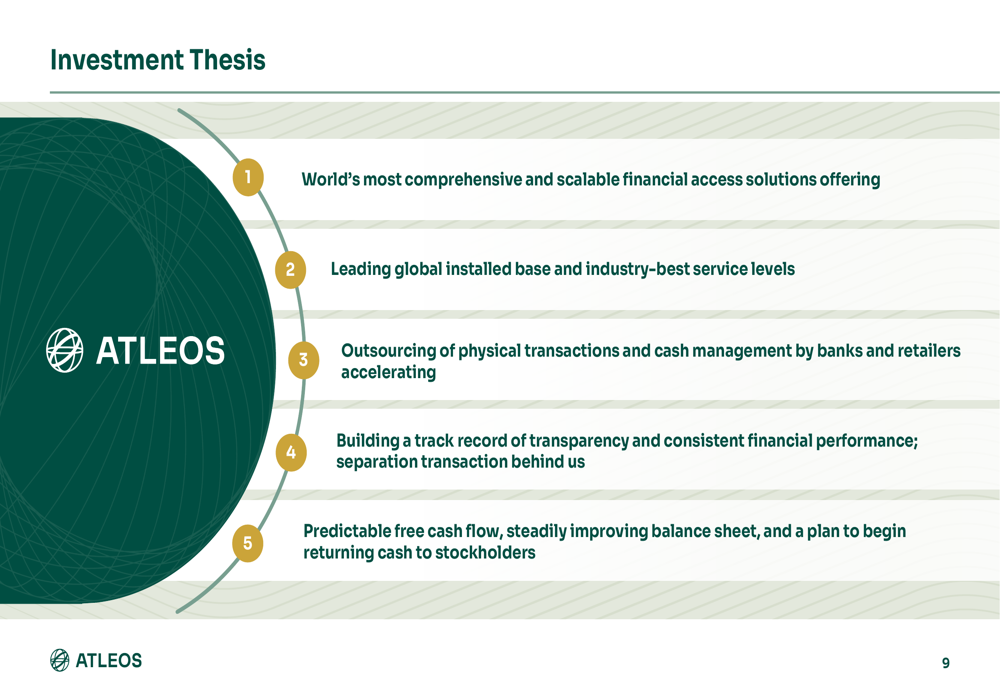

NCR Atleos presented its investment thesis centered on its comprehensive financial access solutions offering, leading global installed base, and the accelerating trend of banks and retailers outsourcing physical transactions and cash management.

The company’s investment case is summarized in this overview:

Management emphasized the company’s track record of transparency and consistent financial performance following its separation transaction, along with predictable free cash flow, an improving balance sheet, and plans to begin returning cash to stockholders.

Despite the positive long-term outlook, investors appeared focused on the near-term revenue miss, as reflected in the stock price decline. NCR Atleos shares closed at $35.37 on November 6, down 6.48% for the day, and fell an additional 3.49% in after-hours trading to $36.50, approaching the lower half of its 52-week range of $22.30 to $42.23.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.