Gold prices buoyed by tariff fears; US duties on 1-kilo bars spur supply concerns

Introduction & Market Context

The New York Times Company (NYSE:NYT) presented its second quarter 2025 earnings results on August 6, revealing substantial profit growth driven by its digital transformation strategy. The company’s stock responded positively in premarket trading, rising 1.9% to $54.64 following the presentation, building on its previous close of $53.62.

The media giant continues to successfully navigate the challenging landscape for traditional publishers by expanding its digital subscriber base and diversifying revenue streams. This quarter’s results demonstrate the company’s ability to grow profitably while continuing strategic investments in its digital future.

Quarterly Performance Highlights

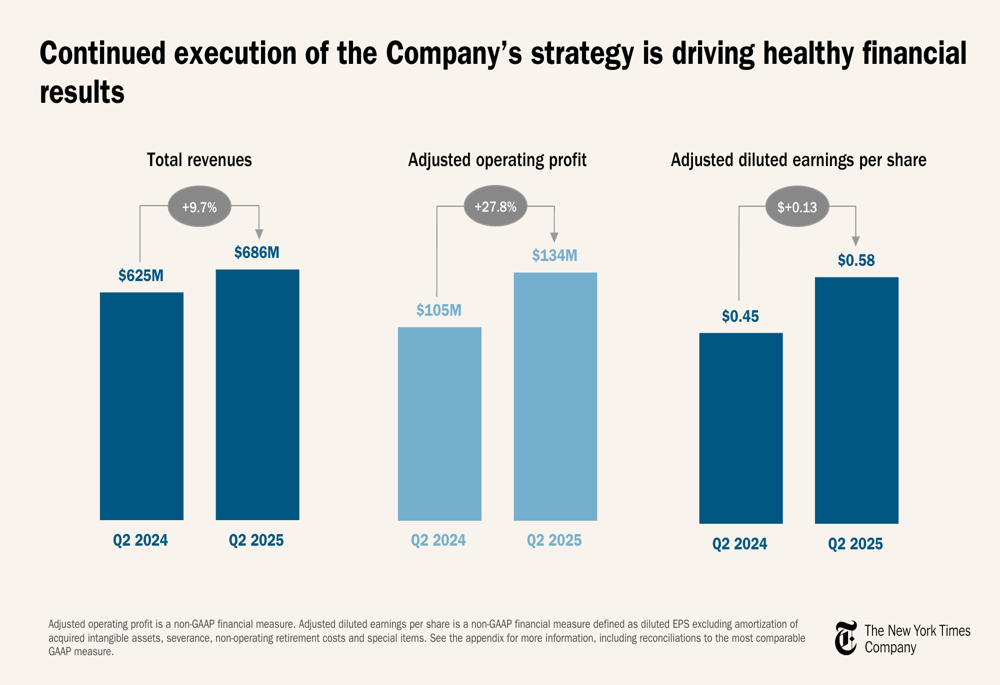

The New York Times reported total revenues of $686 million for Q2 2025, representing a 9.7% increase from $625 million in the same period last year. More impressively, adjusted operating profit surged 27.8% year-over-year to $134 million, with adjusted operating profit margin expanding 280 basis points to 19.5%.

As shown in the following chart of key financial metrics growth:

The company’s adjusted diluted earnings per share increased from $0.45 to $0.58, representing a 28.9% year-over-year improvement. These results exceeded the company’s guidance across most categories, particularly in digital and total advertising revenues, which significantly outperformed expectations.

Digital Subscription Strategy

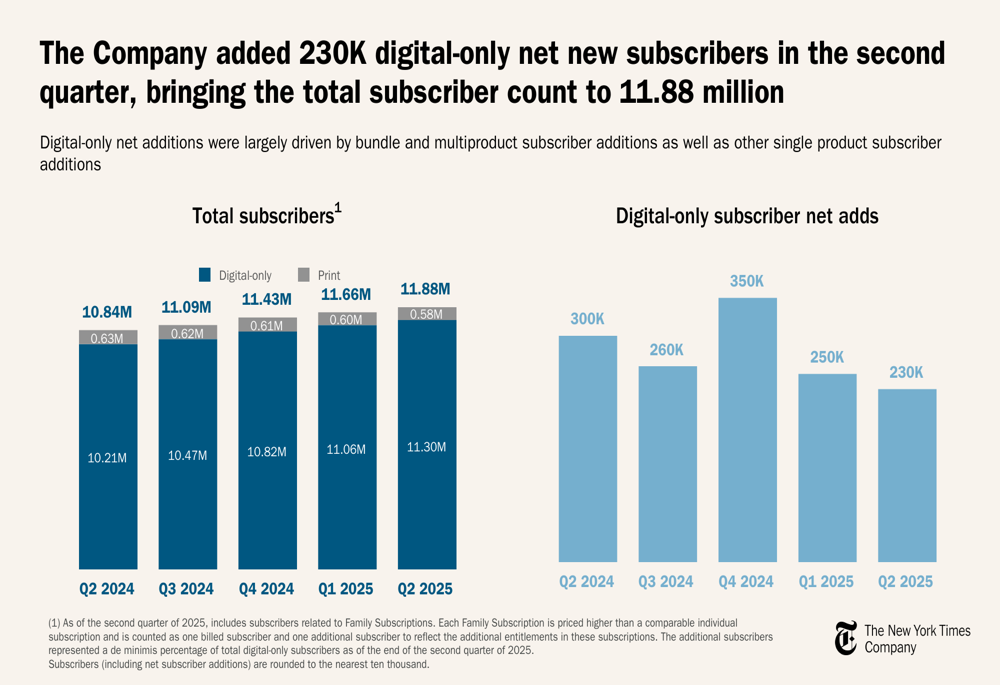

The New York Times added approximately 230,000 net digital-only subscribers in Q2 2025, bringing its total digital-only subscriber count to 11.3 million. The company’s total subscriber base, including print, now stands at 11.88 million.

The following chart illustrates the consistent growth in digital subscribers over the past five quarters:

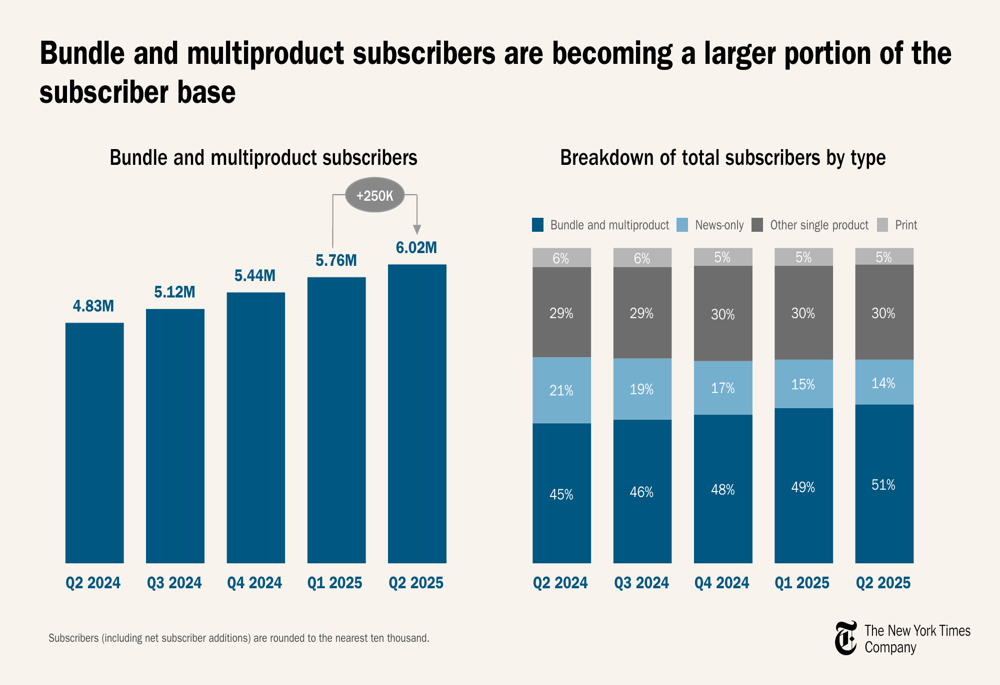

A key driver of the company’s subscription success has been its bundle strategy. Bundle and multiproduct subscribers now represent 51% of the total subscriber base, up from 49% in Q1 2025 and 47% a year ago. This strategic shift is important as bundled subscribers typically generate higher average revenue per user (ARPU) and exhibit better retention rates.

The company’s bundle and multiproduct subscriber growth is visualized here:

Digital-only ARPU increased 3.2% year-over-year to $9.64, reflecting the company’s ability to monetize its subscriber base effectively while continuing to grow it. This balance between growth and monetization has been a consistent strength for the Times in recent quarters.

Revenue Breakdown

Subscription revenues remain the largest contributor to the company’s top line, with total subscription revenues increasing 9.6% year-over-year to $481 million. Within this category, digital subscription revenues grew 15.1% to $350 million, while print subscription revenues declined 2.8% to $131 million.

Digital advertising revenues showed particularly strong performance, increasing 18.7% year-over-year to $94 million. This significantly exceeded the company’s guidance, which had projected high-single-digit growth. Total (EPA:TTEF) advertising revenues, including print, grew 12.4% to $134 million, with print advertising remaining essentially flat at $40 million.

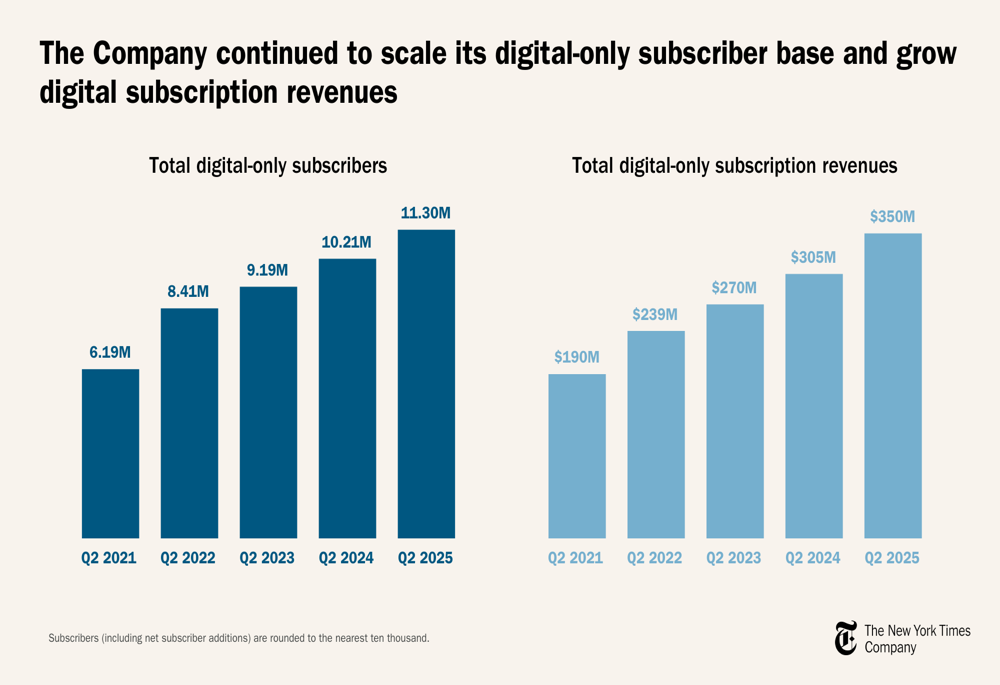

The company’s long-term digital transformation is evident in this chart showing the growth in digital-only subscribers and subscription revenues since 2021:

Affiliate, licensing, and other revenues increased 5.8% year-over-year to $70 million, in line with the company’s mid-single-digit growth guidance for this category.

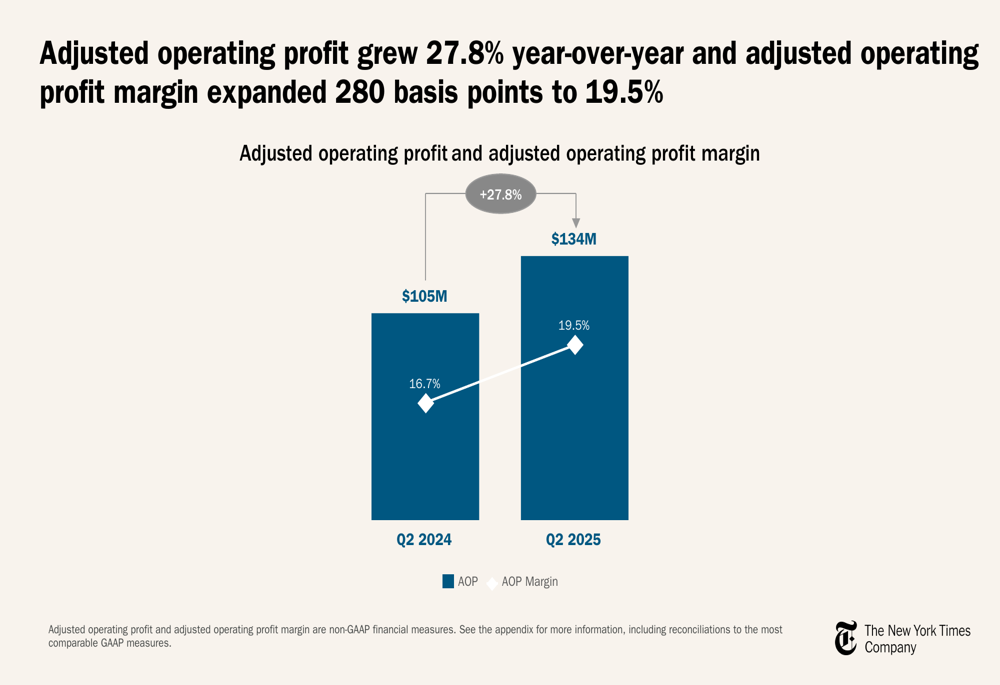

Profitability and Margin Expansion

Despite a 6.1% increase in adjusted operating costs to $552 million, The New York Times achieved significant margin expansion through revenue growth that outpaced expenses. Adjusted operating profit grew 27.8% to $134 million, with adjusted operating profit margin expanding to 19.5%.

The following chart illustrates this profit and margin expansion:

The company continues to generate strong free cash flow, which reached $455 million for the twelve months ended June 30, 2025. This represents a steady increase from $348 million in the comparable period a year earlier, providing the company with financial flexibility to invest in growth initiatives and return capital to shareholders.

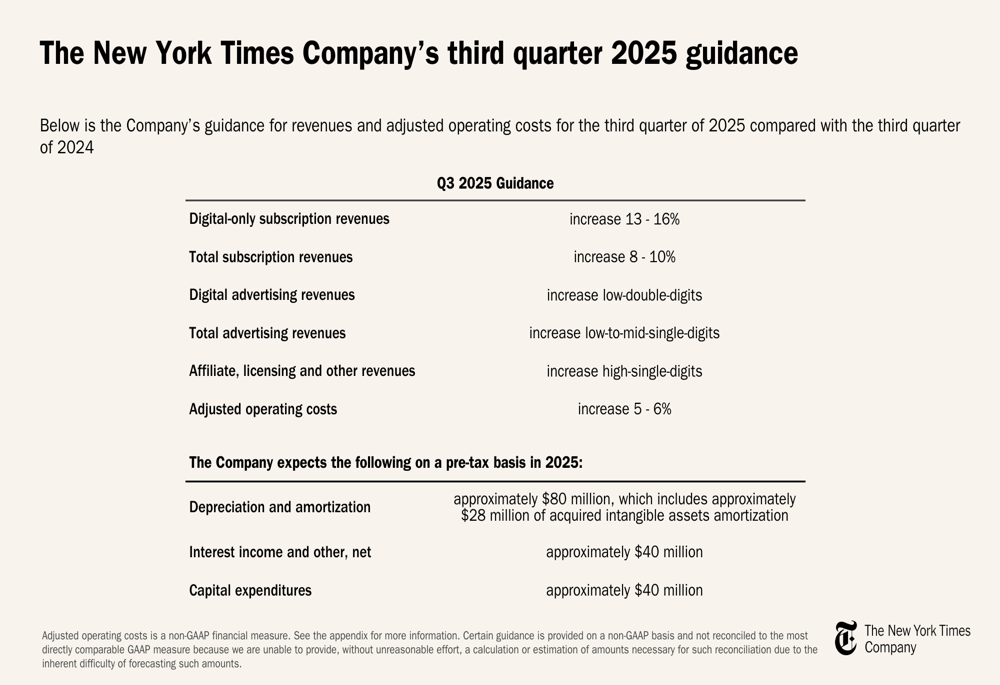

Forward Guidance

Looking ahead to the third quarter of 2025, The New York Times provided guidance that suggests continued strong performance. The company expects:

- Digital-only subscription revenues to increase 13-16%

- Total subscription revenues to increase 8-10%

- Digital advertising revenues to increase low-double-digits

- Total advertising revenues to increase low-to-mid-single-digits

- Affiliate, licensing and other revenues to increase high-single-digits

- Adjusted operating costs to increase 5-6%

This guidance is detailed in the following slide:

The company also provided full-year 2025 expectations for depreciation and amortization of approximately $80 million, interest income and other of approximately $40 million, and capital expenditures of approximately $40 million.

Conclusion

The New York Times’ Q2 2025 results demonstrate the continued success of its digital transformation strategy. The company’s focus on bundle subscriptions is driving both subscriber growth and improved monetization, while digital advertising revenues are showing strong momentum.

The significant expansion in operating profit margin, despite continued investments in the business, highlights the scalability of the company’s digital model. With consistent free cash flow generation and a clear strategic direction, The New York Times appears well-positioned to continue its growth trajectory in the coming quarters.

As digital revenues continue to comprise a larger portion of the company’s overall business, the declining print segment has less impact on total performance, allowing the Times to fully embrace its identity as a digital-first media company while maintaining its journalistic excellence.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.