German construction sector still in recession, civil engineering only bright spot

Introduction & Market Context

NGL Energy Partners LP (NYSE:NGL) released its May 2025 investor presentation on May 29, highlighting the company’s strategic transformation into a Water Solutions-focused partnership. The stock closed at $3.22, down 6.67% on the day, but showed a slight recovery of 2.49% in aftermarket trading. According to recent earnings data, NGL missed both EPS and revenue forecasts for Q3 2025, posting an EPS of -$0.12 against expectations of $0.19, and revenue of $1.55 billion versus the projected $1.71 billion.

The presentation comes as NGL continues to navigate a strategic pivot, with Water Solutions now representing 82% of the company’s total EBITDA for fiscal year 2025, up from a smaller proportion in previous years.

Strategic Initiatives

NGL Energy has executed several strategic moves over the past year, as outlined in their presentation timeline. The company completed its final arrearage payment to preferred unitholders in April 2024, amended its Term Loan B agreement in August 2024 to reduce the SOFR margin from 4.5% to 3.75%, and put the LEX II water pipeline project into service in October 2024.

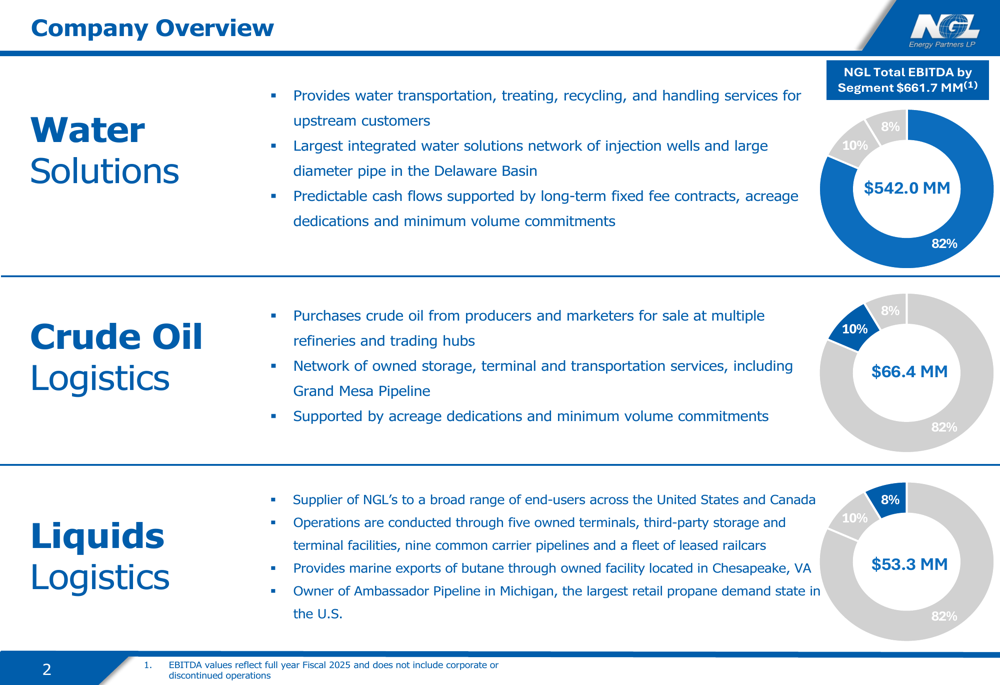

As shown in the following segment breakdown chart:

The company’s strategic shift toward Water Solutions is evident in the EBITDA distribution, with Water Solutions contributing $542.0 million (82%), Crude Oil Logistics $66.4 million (10%), and Liquids Logistics $53.3 million (8%) for fiscal 2025.

This aligns with CEO Mike Crimble’s statement from the recent earnings call: "We are now on our way to becoming a Water Solutions partnership," highlighting the company’s strategic direction. The company also announced non-core asset sales totaling approximately $270 million in May 2025, including the divestment of 17 natural gas liquids terminals mentioned in recent earnings reports.

Quarterly Performance Highlights

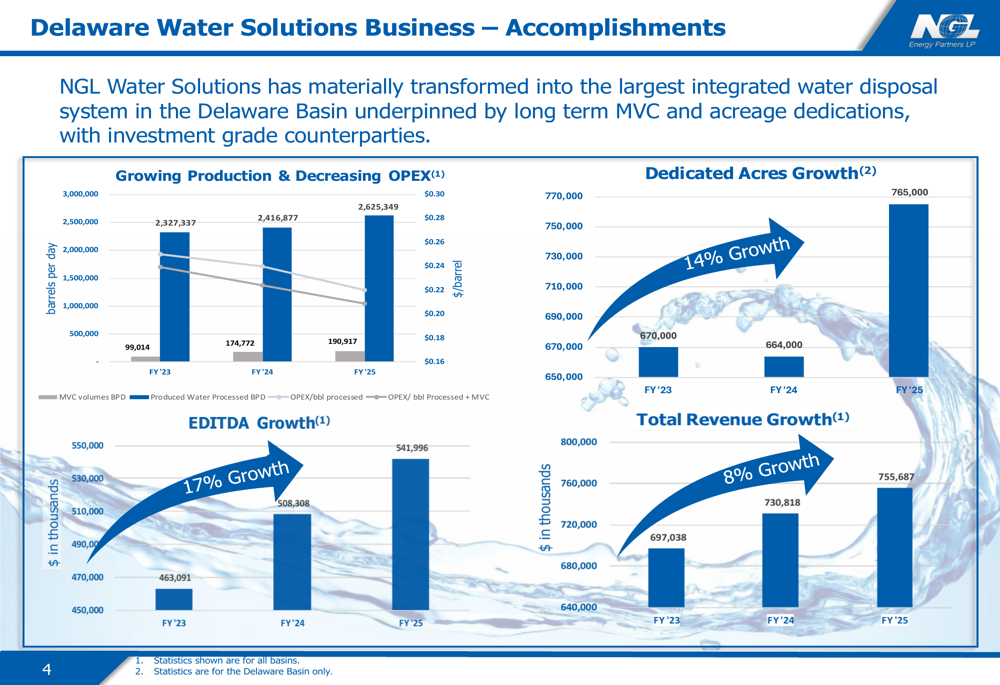

Despite the earnings miss in Q3 2025, NGL’s Water Solutions segment has shown consistent growth. The segment’s accomplishments are illustrated in this performance chart:

Water Solutions has increased production from approximately 2.33 million barrels per day in FY ’23 to 2.63 million barrels per day in FY ’25, while simultaneously decreasing operating expenses. The segment’s EBITDA grew by 17% from $463,091 thousand in FY ’23 to $541,996 thousand in FY ’25, outpacing the 8% growth in total revenue during the same period.

For Q3 2025 specifically, Water Solutions EBITDA reached $132.7 million, up from $121.3 million in the same quarter of the previous year, demonstrating the strength of this core business despite overall company challenges.

Detailed Financial Analysis

NGL’s financial performance shows a mixed picture across segments. The company’s consolidated adjusted EBITDA for FY 2025 reached $617,759 thousand, a slight increase from $610,081 thousand in FY 2024. However, this falls slightly short of the updated guidance of $620 million mentioned in recent earnings communications.

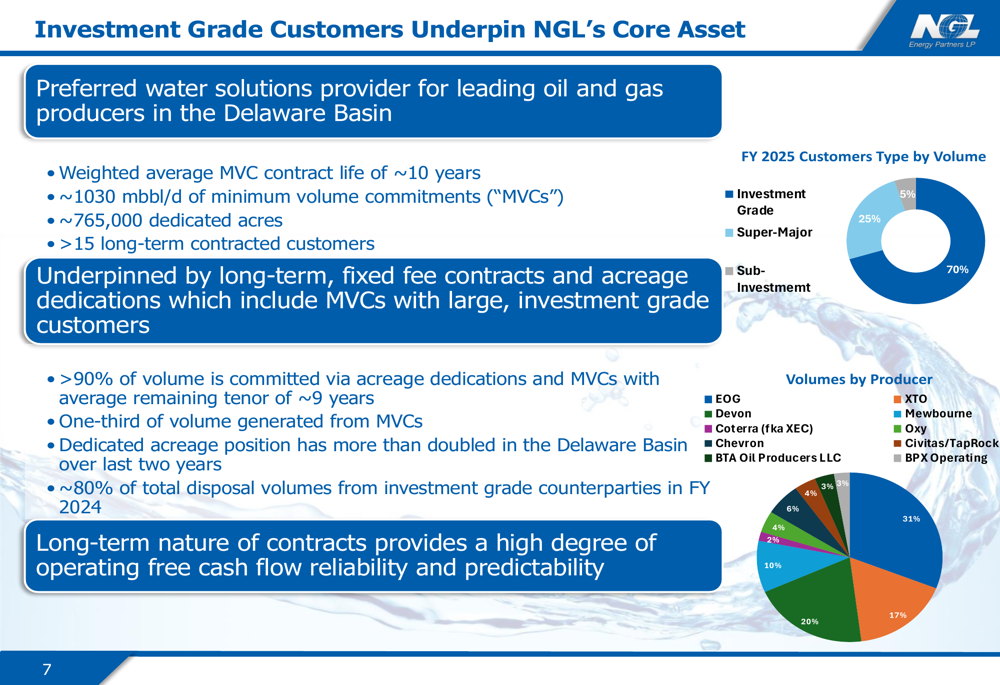

The Water Solutions segment’s growth is underpinned by strong customer relationships and contracted volumes, as illustrated in this customer breakdown:

The segment benefits from a robust customer base with 70% investment grade and 25% super-major clients. NGL has secured approximately 1,030 thousand barrels per day in minimum volume commitments (MVCs) with a weighted average contract life of about 10 years, providing stable cash flow visibility.

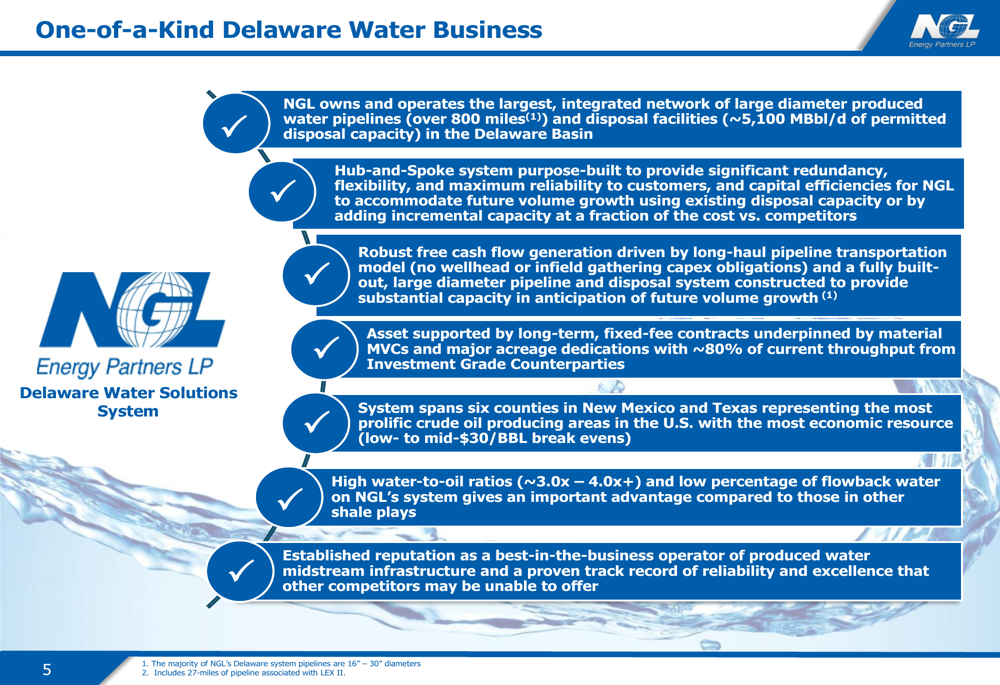

The company’s Delaware Basin water infrastructure represents a significant competitive advantage:

NGL owns and operates the largest integrated network of large diameter produced water pipelines in the Delaware Basin, with a hub-and-spoke system designed for redundancy and flexibility. This infrastructure spans six counties in New Mexico and Texas and is supported by long-term, fixed-fee contracts and major acreage dedications.

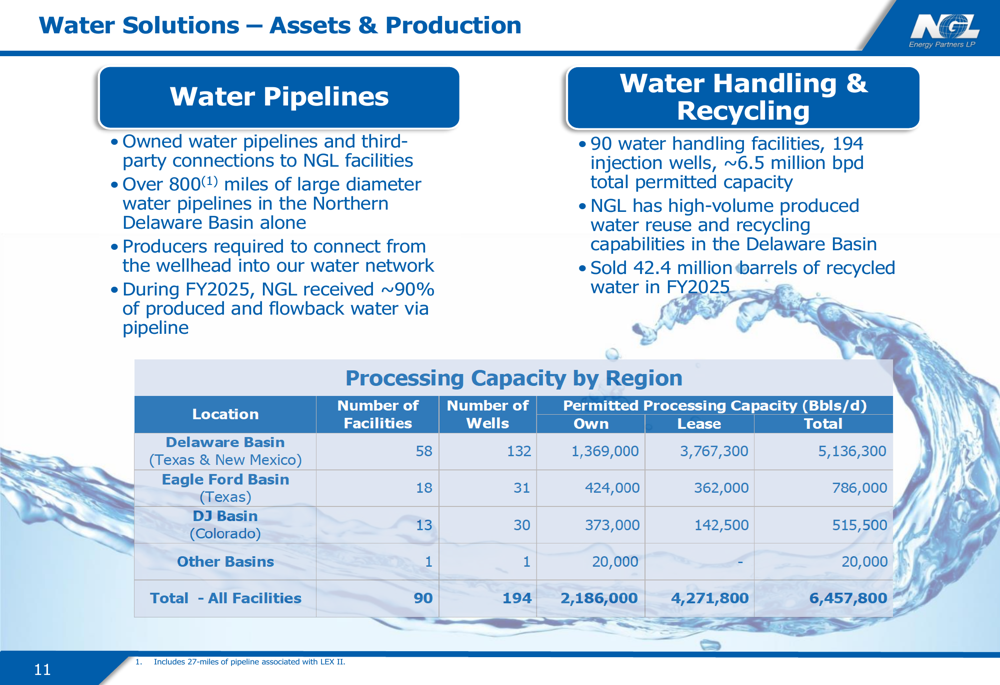

The company’s water handling capacity is substantial, as shown in this asset breakdown:

With processing capacity of over 5.1 million barrels per day in the Delaware Basin alone and a total of 90 water handling facilities across all regions, NGL has positioned itself as a dominant player in the produced water management space.

Forward-Looking Statements

Looking ahead, NGL Energy is focused on completing its transformation into a Water Solutions-centric partnership. The company has updated its full-year EBITDA guidance to $620 million, reflecting both the strategic focus on Water Solutions and the divestment of non-core assets.

The LEX II water pipeline project, which went into service in October 2024 with an initial capacity of 200,000 barrels per day (expandable to 500,000 barrels per day), represents a significant growth driver for the Water Solutions segment. The company continues to explore further asset sales to reduce leverage and improve cash flow predictability.

As CEO Mike Crimble noted in recent communications, "Exiting the biodiesel business and selling substantially all of our wholesale propane business will improve the repeatability of our cash flows," highlighting the strategic rationale behind the company’s transformation.

While NGL faces challenges in meeting overall earnings expectations, as evidenced by the Q3 2025 results, the company’s strategic pivot toward its high-performing Water Solutions segment positions it to potentially deliver more consistent results in the future, particularly as it completes its transformation and reduces exposure to more volatile business lines.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.