German construction sector still in recession, civil engineering only bright spot

Introduction & Market Context

Nine Energy Service Inc (NYSE:NINE) released its Q1 2025 investor presentation on May 8, 2025, highlighting sequential revenue and margin improvements despite a flat U.S. rig count. The oilfield services provider, which specializes in completion tools and services, reported financial results that exceeded Wall Street expectations while emphasizing its technology-focused strategy and asset-light business model.

The company’s stock, which has traded between $0.602 and $2.065 over the past 52 weeks, showed a modest 3.47% increase to $0.613 following the presentation. Nine Energy continues to navigate a challenging market environment characterized by fluctuating oil prices and potential tariff impacts.

Quarterly Performance Highlights

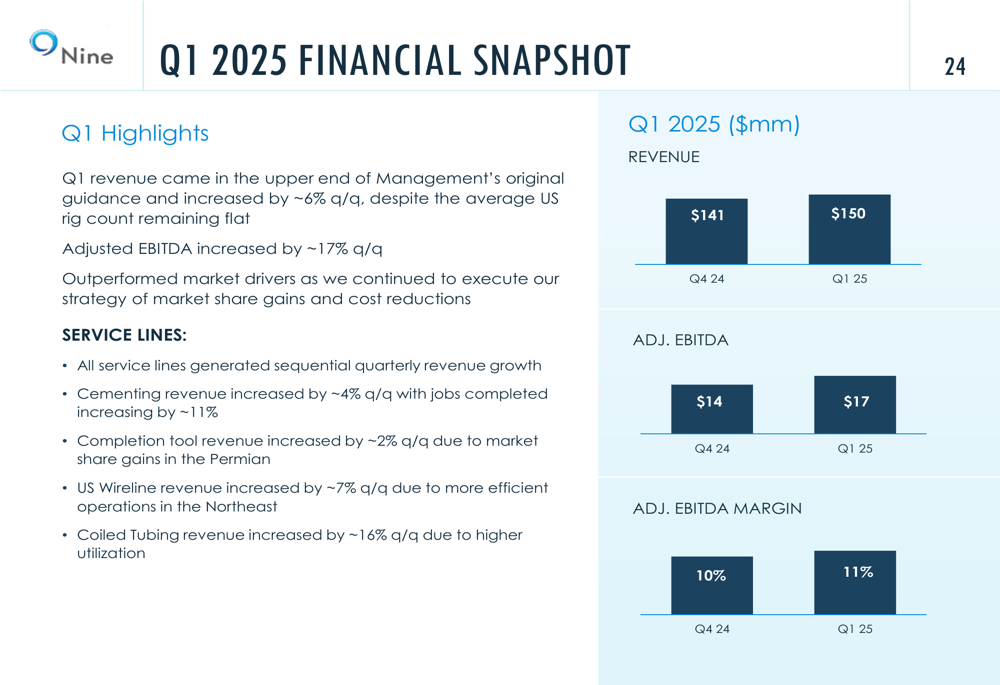

Nine Energy reported Q1 2025 revenue of $150 million, representing a 6% increase from Q4 2024 and exceeding analyst expectations of $135.79 million. Adjusted EBITDA rose more significantly, climbing 17% quarter-over-quarter to $17 million, with margins improving from 10% to 11% during the same period.

As shown in the following quarterly financial snapshot, all service lines contributed to the sequential growth:

The company’s performance is particularly notable given that the average U.S. rig count remained flat during the quarter. Nine Energy’s CEO Ann Fox emphasized a cautious approach to market conditions in the earnings call, stating, "We are trying to be conservative," while highlighting concerns about potential tariffs affecting the service sector.

Strategic Initiatives

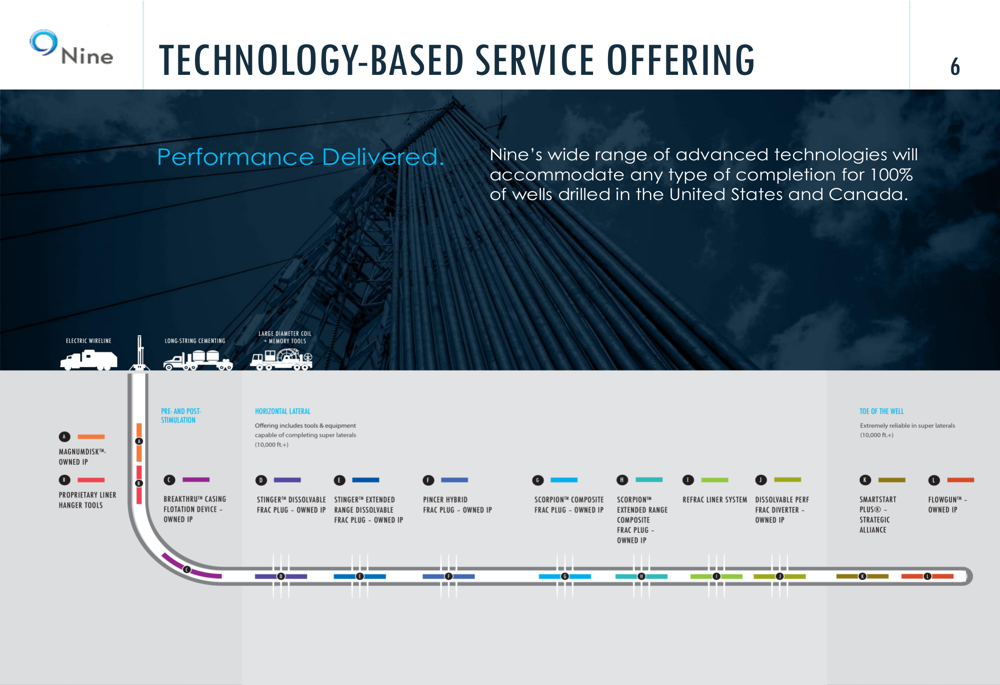

Nine Energy’s presentation emphasized its technology-focused strategy, with approximately 60% of its business driven by technology-based services, primarily completion tools and cementing. The company has positioned itself as a technology leader in the dissolvable plug market, where it claims 20-25% market share.

The following slide illustrates Nine’s comprehensive technology-based service offerings across the wellbore:

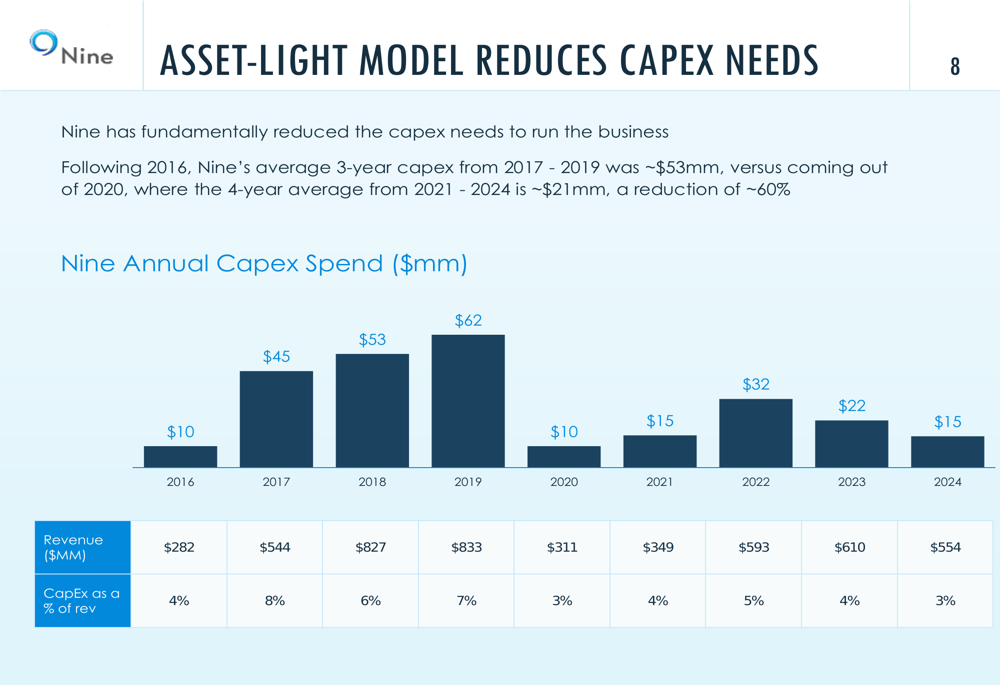

A key component of Nine’s strategy is its asset-light business model, which has significantly reduced capital expenditure requirements. The company has decreased its average annual CAPEX by approximately 60%, from $53 million during 2017-2019 to $21 million during 2021-2024.

The following chart demonstrates this CAPEX reduction trend:

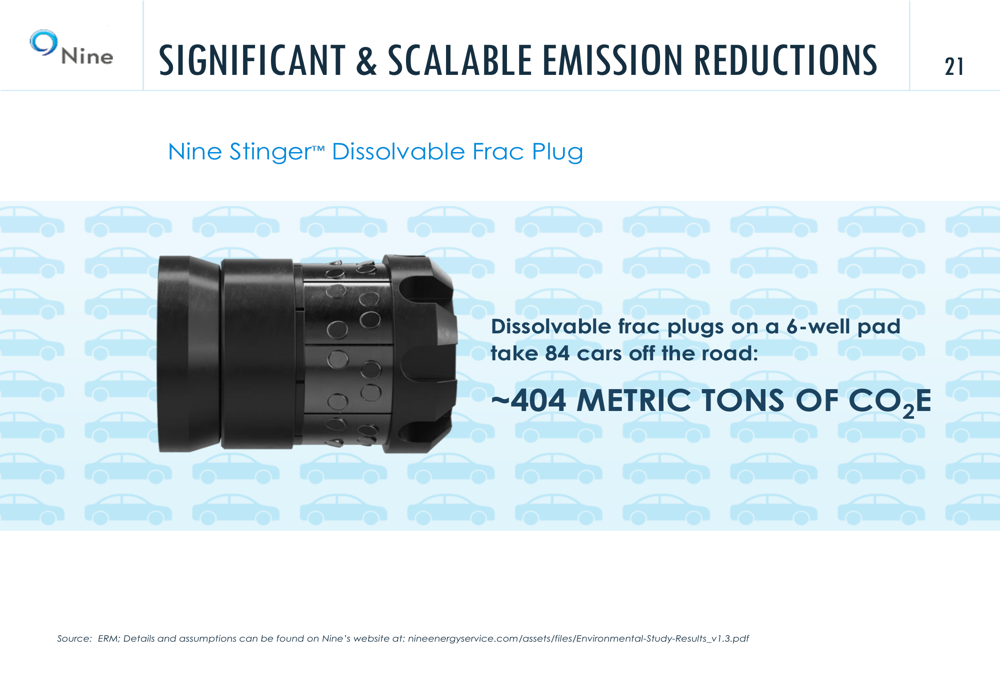

Nine Energy is also expanding its environmental, social, and governance (ESG) technology offerings. The company’s dissolvable frac plugs provide significant emission reductions, with a six-well pad implementation equivalent to taking 84 cars off the road by eliminating approximately 404 metric tons of CO₂ equivalent.

As shown in the following visualization of emission reductions:

Financial Position & Outlook

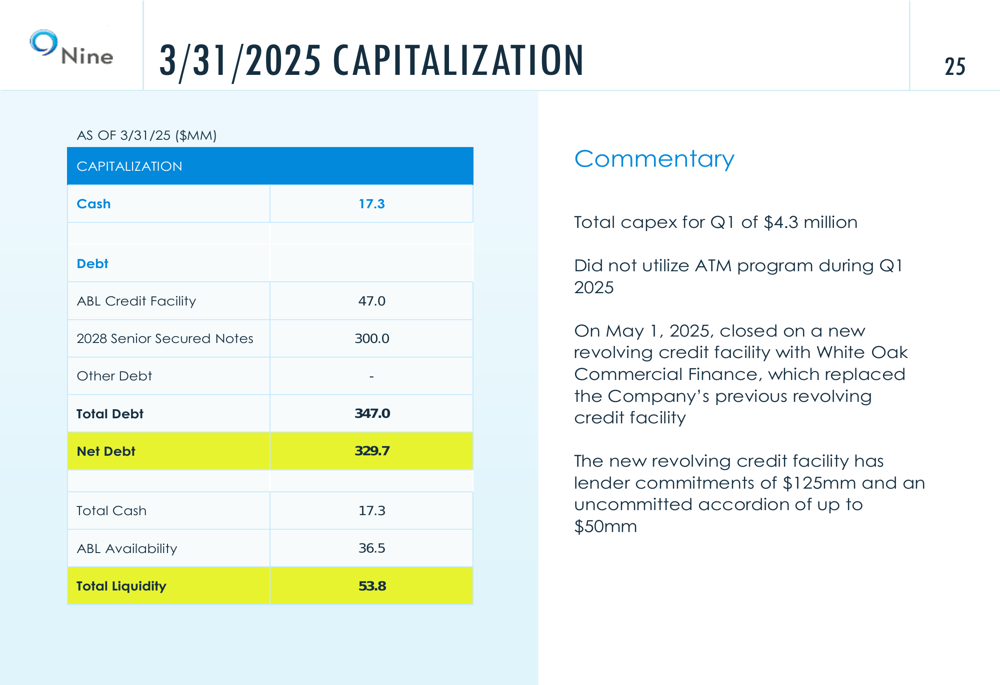

Despite the positive quarterly performance, Nine Energy continues to operate with substantial debt. As of March 31, 2025, the company reported total debt of $347 million against cash and cash equivalents of $17.3 million, resulting in a net debt position of $329.7 million.

The company’s capitalization structure is detailed in the following slide:

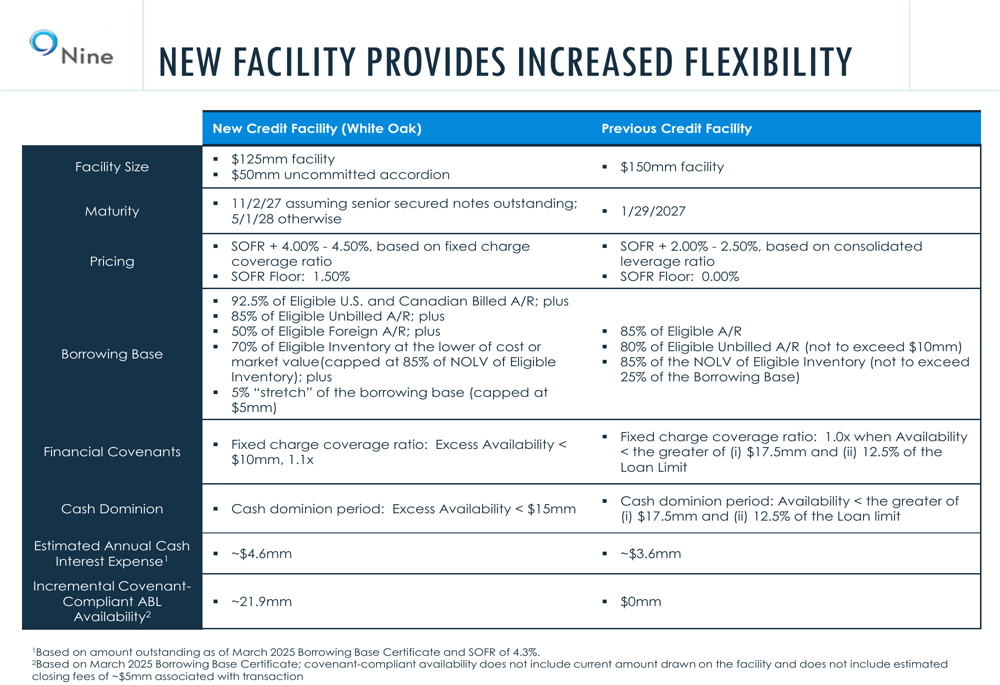

A significant development is Nine Energy’s new revolving credit facility with White Oak Commercial Finance, which closed on May 1, 2025. The new facility provides $125 million in commitments with an uncommitted accordion of up to $50 million, extending the maturity to November 2027 and increasing covenant-compliant availability by approximately $21.9 million.

The following comparison highlights the improved terms of the new facility:

Looking ahead, Nine Energy projects Q2 2025 revenue between $138 million and $148 million, suggesting a potential sequential decline. Management cited fluctuating oil prices, potential tariffs, and broader commodity market dynamics as factors influencing this cautious outlook.

Competitive Industry Position

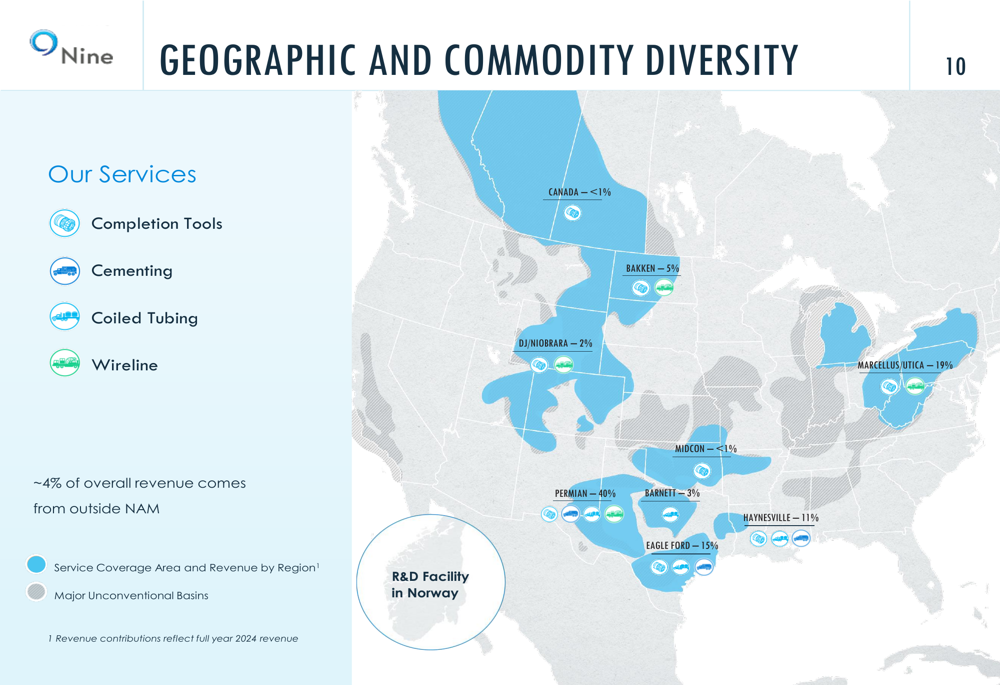

Nine Energy maintains a diversified geographic presence across major U.S. basins, with the Permian Basin accounting for 40% of revenue, followed by Marcellus/Utica (19%), Eagle Ford (15%), and Haynesville (11%). This diversification helps mitigate regional market fluctuations.

The following map illustrates Nine’s geographic revenue distribution:

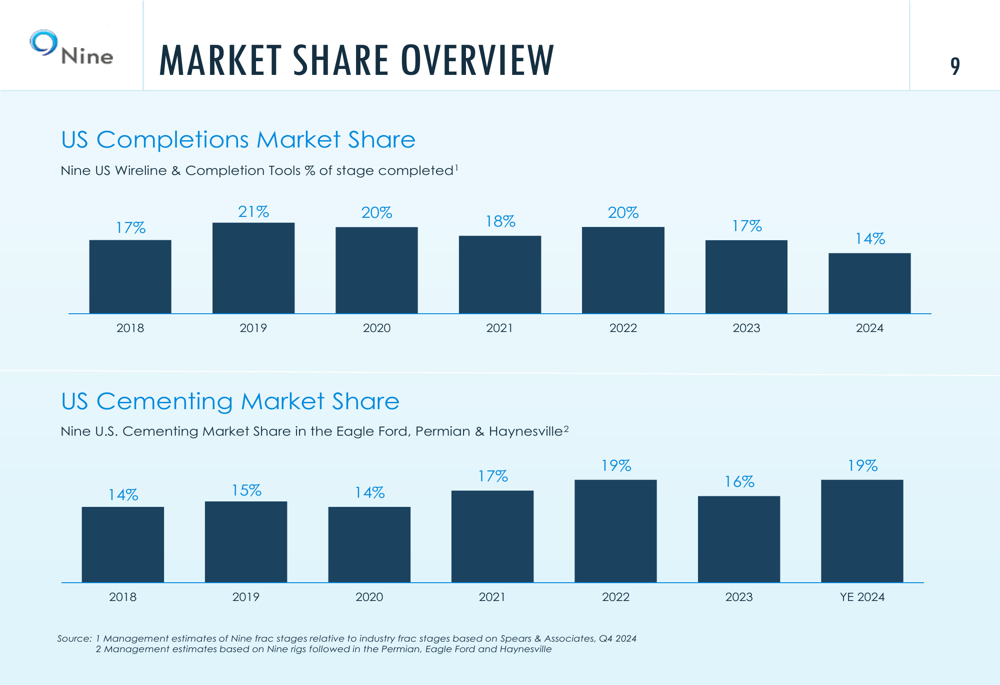

In terms of market share, Nine Energy has experienced mixed trends. While its U.S. completions market share declined from 17% in 2023 to 14% in 2024, its cementing market share in key basins increased from 16% to 19% during the same period.

The company’s market position is detailed in the following chart:

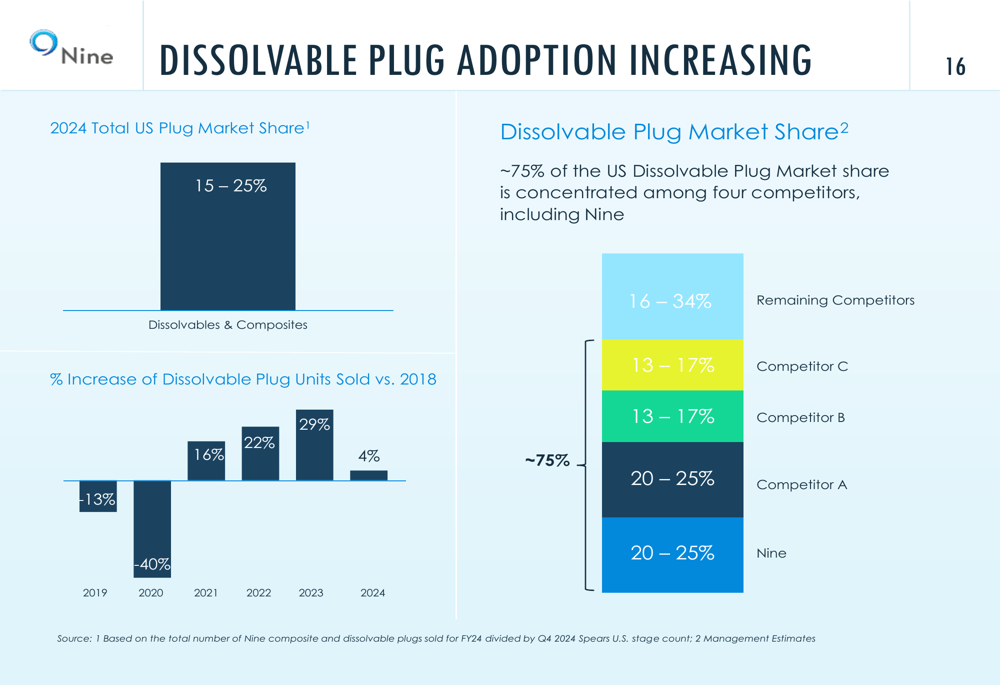

Nine Energy’s dissolvable plug technology represents a significant competitive advantage. The company holds 20-25% of the U.S. dissolvable plug market, positioning it as one of the top four competitors that collectively control approximately 75% of this market.

The following chart shows the dissolvable plug market share distribution and adoption trend:

Nine Energy’s investor presentation portrays a company navigating market challenges through technological innovation and financial discipline. While the sequential improvements in revenue and margins are encouraging, the substantial debt burden and cautious Q2 outlook suggest ongoing challenges. The new credit facility provides increased financial flexibility, but investors should monitor whether the company’s technology-focused strategy can drive sustainable growth and debt reduction in the quarters ahead.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.