Stock market today: S&P 500 climbs as health care, tech gain; Nvidia earnings loom

Introduction & Market Context

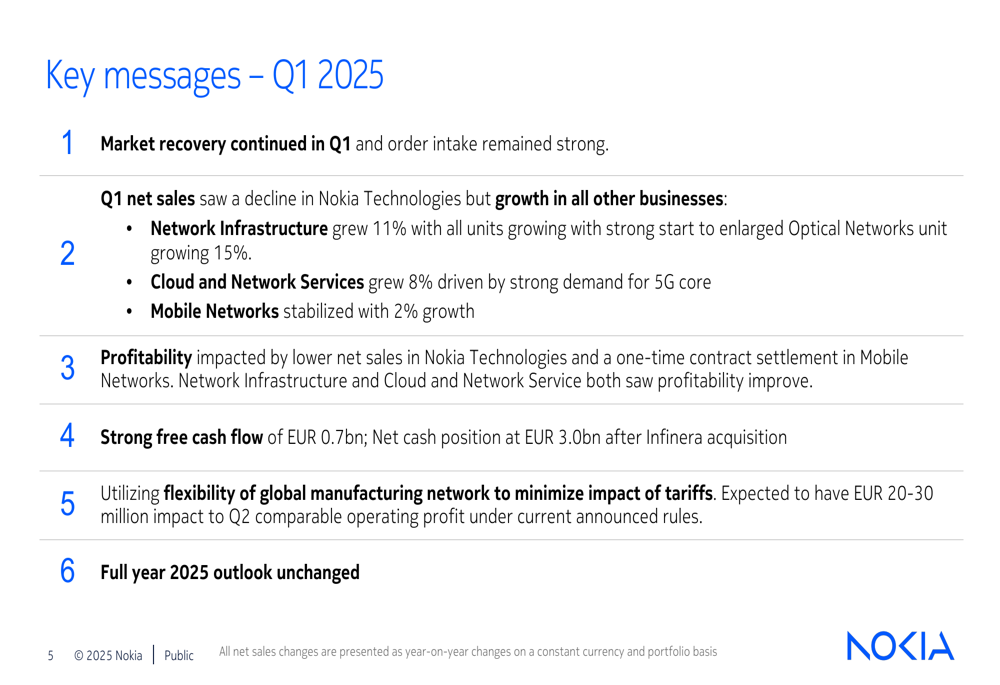

Nokia (NYSE:NOK) presented its Q1 2025 financial results on April 24, 2025, revealing a mixed performance with growth in most business segments offset by challenges in Nokia Technologies and a one-time contract settlement impact. The Finnish telecommunications equipment provider reported that market recovery continued in Q1 with strong order intake, though the company’s stock fell 6.17% following the announcement, suggesting investors may have expected stronger results.

The presentation, led by new President and CEO Justin Hotard, highlighted the company’s strategic progress while acknowledging certain headwinds. Despite the overall positive tone of the presentation, Nokia’s net sales saw a slight decline on a constant currency and portfolio basis, even as individual business segments showed growth.

Quarterly Performance Highlights

Nokia reported varied performance across its business segments in Q1 2025. Network Infrastructure, Cloud and Network Services, and Mobile Networks all posted growth, while Nokia Technologies experienced a decline due to a challenging year-over-year comparison.

As shown in the following key messages summary from the presentation:

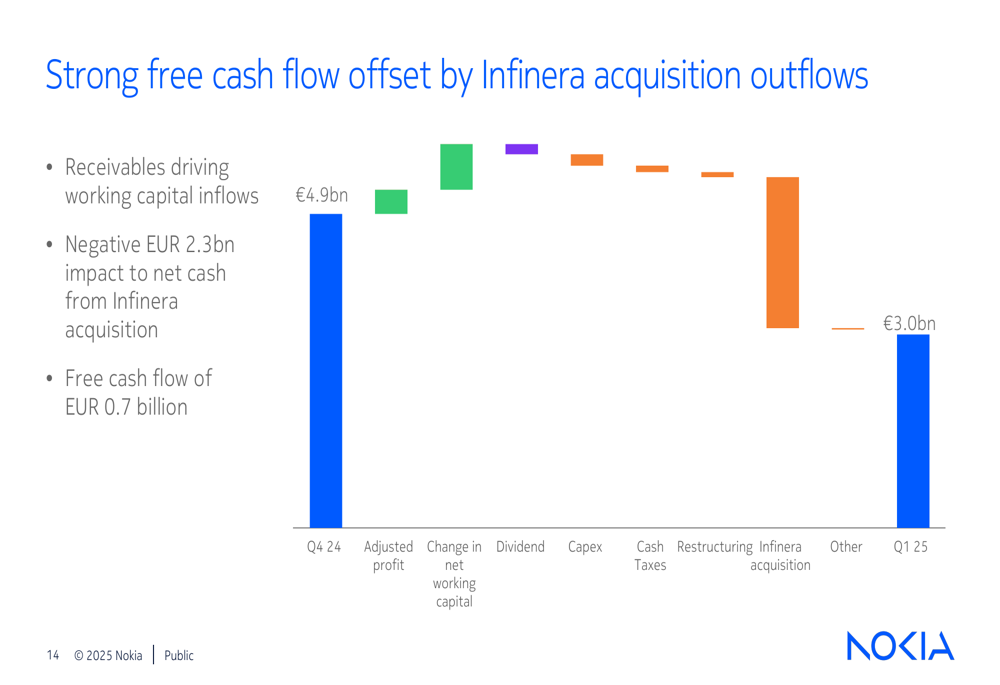

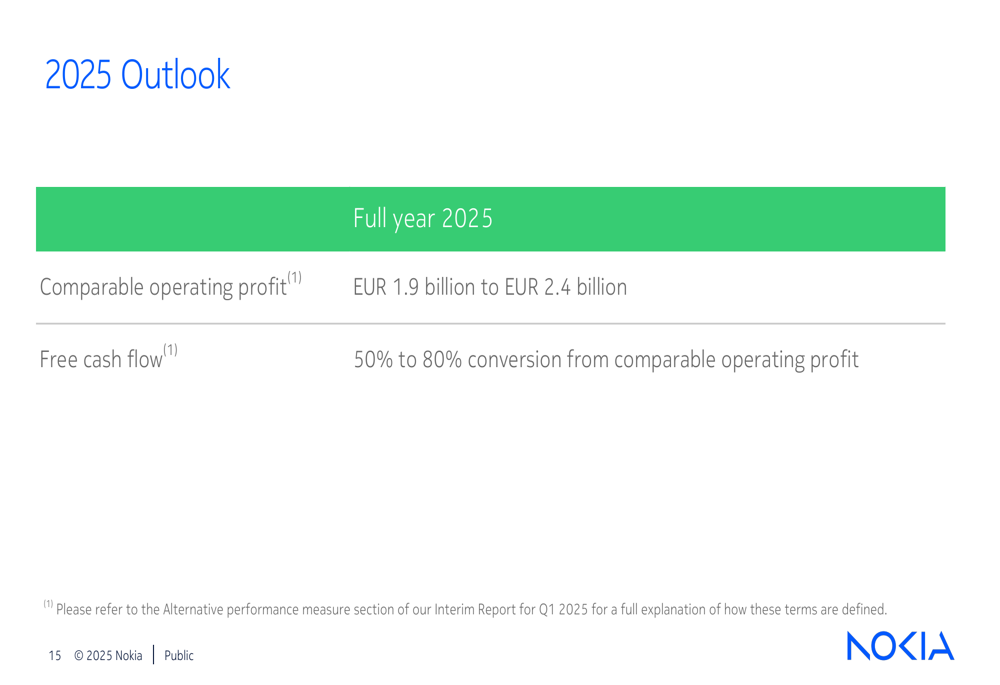

The company achieved strong free cash flow of €0.7 billion in the quarter, though its net cash position decreased to €3.0 billion from €4.9 billion in Q4 2024, primarily due to the completion of the Infinera (NASDAQ:INFN) acquisition. Nokia maintained its full-year 2025 outlook, projecting comparable operating profit between €1.9 billion and €2.4 billion.

Strategic Initiatives

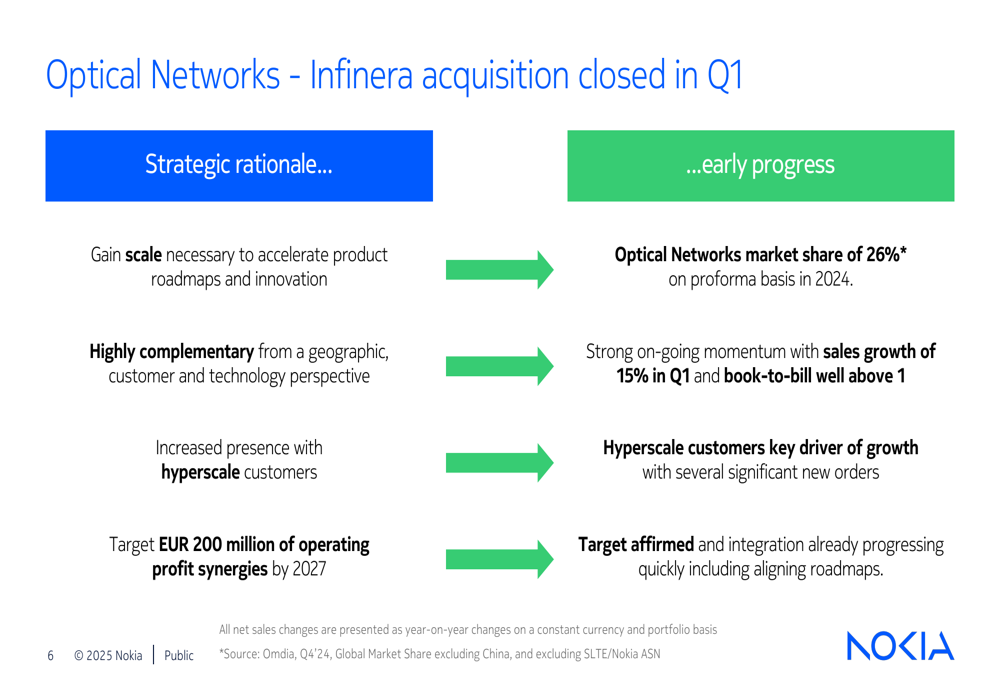

A significant development in Q1 was the completion of Nokia’s acquisition of Infinera, which strengthens the company’s position in the optical networks market. The strategic rationale for this acquisition includes gaining necessary scale to accelerate product roadmaps, complementary geographic and customer reach, and increased presence with hyperscale customers.

The following slide details the strategic benefits and early progress of the Infinera acquisition:

Nokia expects to achieve €200 million in operating profit synergies from the Infinera acquisition by 2027. Early results appear promising, with Optical Networks showing 15% sales growth in Q1 and a book-to-bill ratio well above 1, indicating strong future demand. The combined entity now holds a 26% market share in Optical Networks on a proforma basis, excluding China.

Detailed Financial Analysis

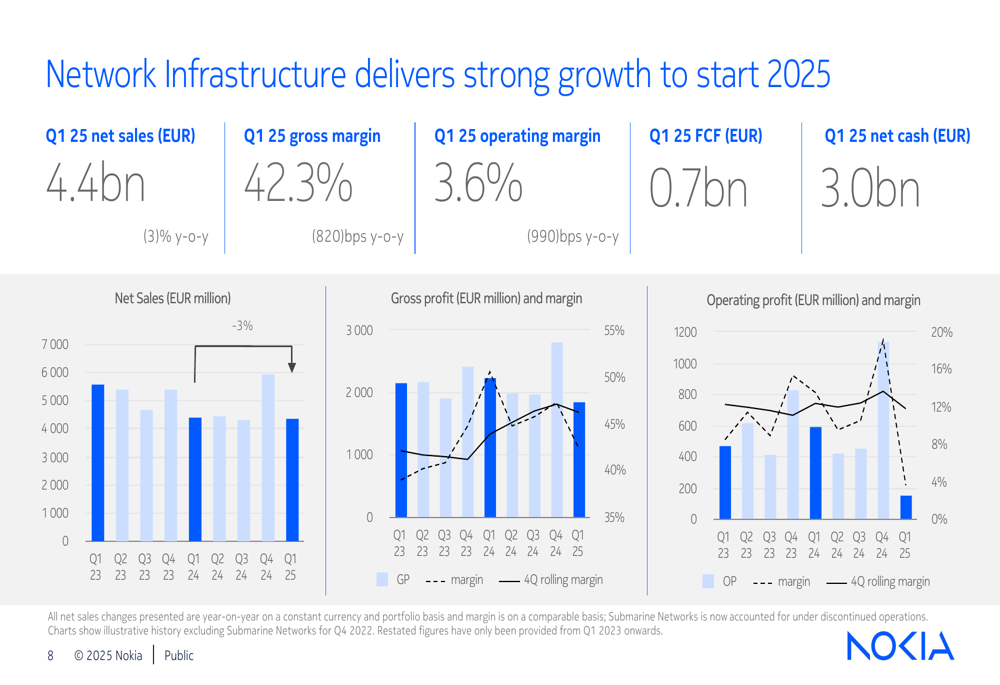

Nokia’s Network Infrastructure segment delivered strong performance in Q1 2025, as illustrated in the following financial summary:

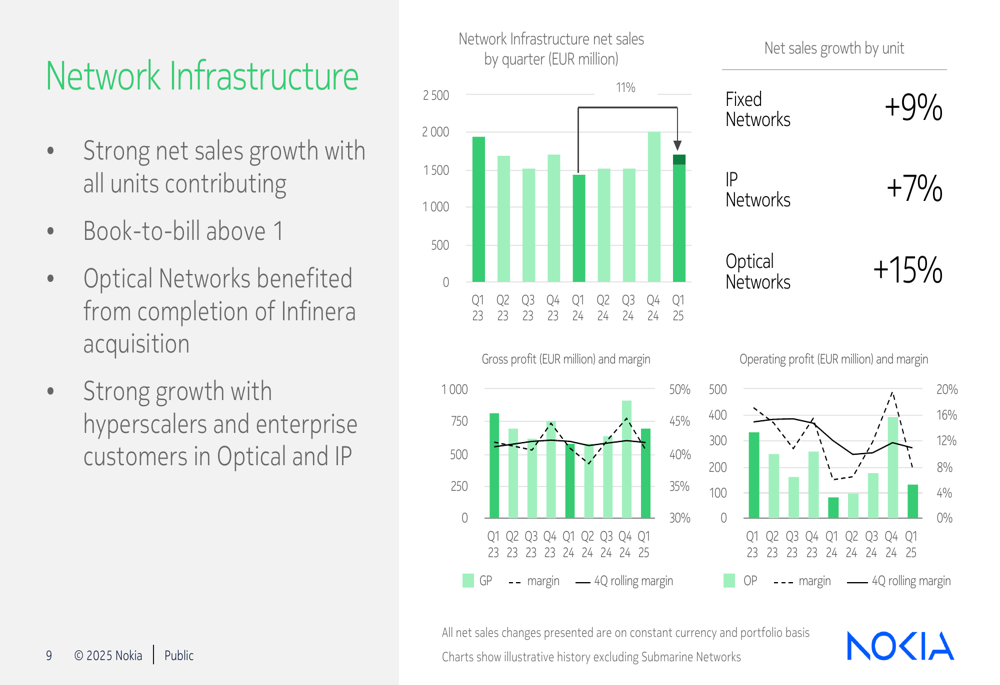

Despite the headline 3% year-on-year decline in net sales, Network Infrastructure showed significant improvements in both gross margin (up 820 basis points to 42.3%) and operating margin (up 990 basis points to 3.6%). The segment’s performance was driven by growth across all units, with Fixed Networks growing 9%, IP Networks 7%, and Optical Networks 15%.

A deeper look at Network Infrastructure performance shows strong momentum with hyperscalers and enterprise customers:

Mobile Networks showed signs of stabilization with 2% net sales growth driven by North America. However, profitability declined due to a one-time contract settlement with a net impact of €120 million. The segment announced an important contract extension with T-Mobile US (NASDAQ:TMUS) during the quarter.

Cloud and Network Services delivered strong growth of 8%, driven by Core Networks. Both gross and operating margins improved due to favorable product mix and operating leverage. The business continued to gain momentum in 5G Core with wins at AT&T (NYSE:T), Boost Mobile, and Ooredoo.

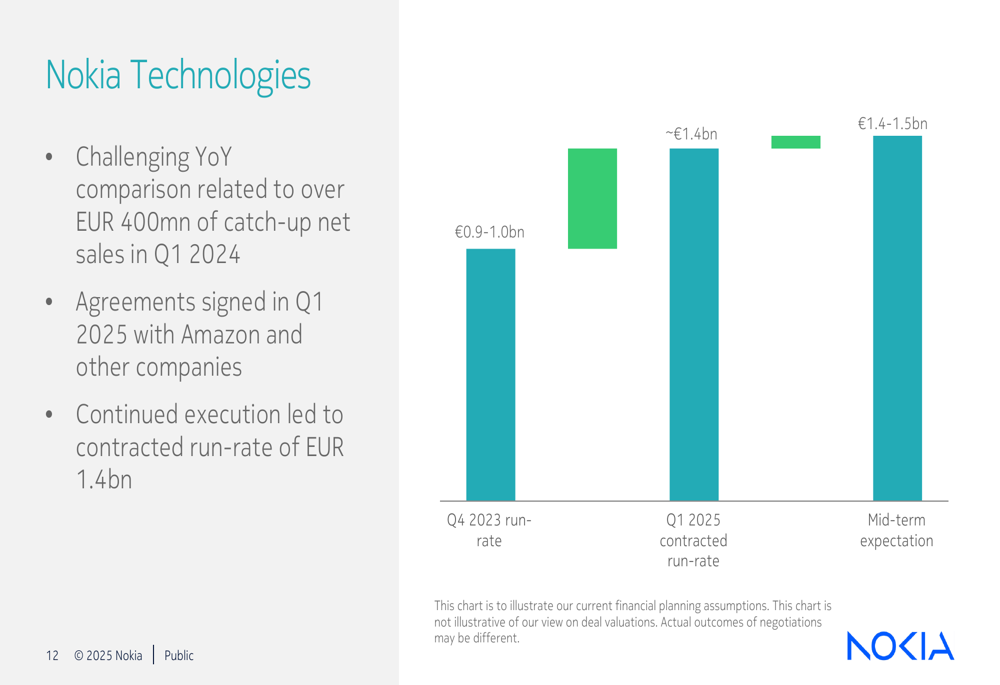

Nokia Technologies faced a challenging year-over-year comparison, as Q1 2024 included over €400 million in catch-up net sales. However, the division signed new agreements with Amazon (NASDAQ:AMZN) and other companies in Q1 2025, achieving a contracted run-rate of €1.4 billion:

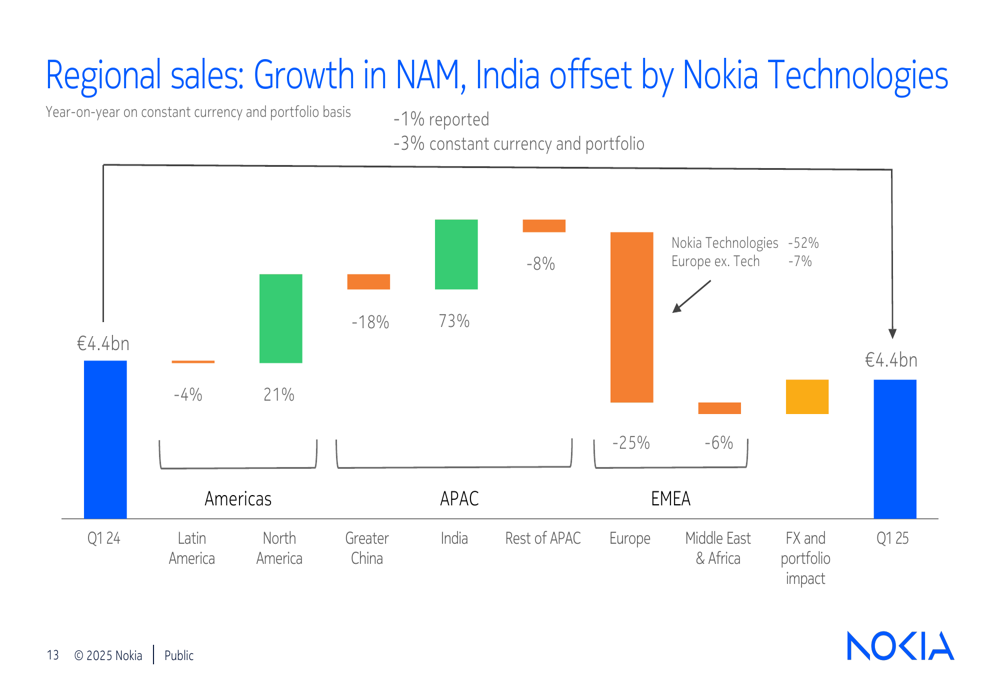

Regional performance varied significantly, with North America and India showing strong growth while Europe and Greater China declined:

The company’s strong free cash flow of €0.7 billion was offset by the €2.3 billion impact of the Infinera acquisition, as shown in this cash flow breakdown:

Forward-Looking Statements

Nokia maintained its 2025 outlook, projecting comparable operating profit between €1.9 billion and €2.4 billion and free cash flow conversion of 50% to 80% from comparable operating profit:

The company noted that it is utilizing the flexibility of its global manufacturing network to minimize the impact of tariffs, which are expected to have a €20-30 million impact on Q2 comparable operating profit under current announced rules.

CEO Justin Hotard emphasized four key areas of focus: leveraging Nokia’s impressive core technology base across its portfolio, maintaining the company’s role as a trusted partner for customers, focusing on capital allocation, and investing for long-term value creation.

With the Infinera acquisition now complete and signs of market recovery continuing, Nokia appears positioned to benefit from growth in Network Infrastructure and Cloud and Network Services, while working to address challenges in other areas of the business. However, investors’ initial reaction suggests concerns about the company’s ability to translate segment growth into overall improved financial performance in the near term.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.