Procore signs multi-year strategic collaboration agreement with AWS

Introduction & Market Context

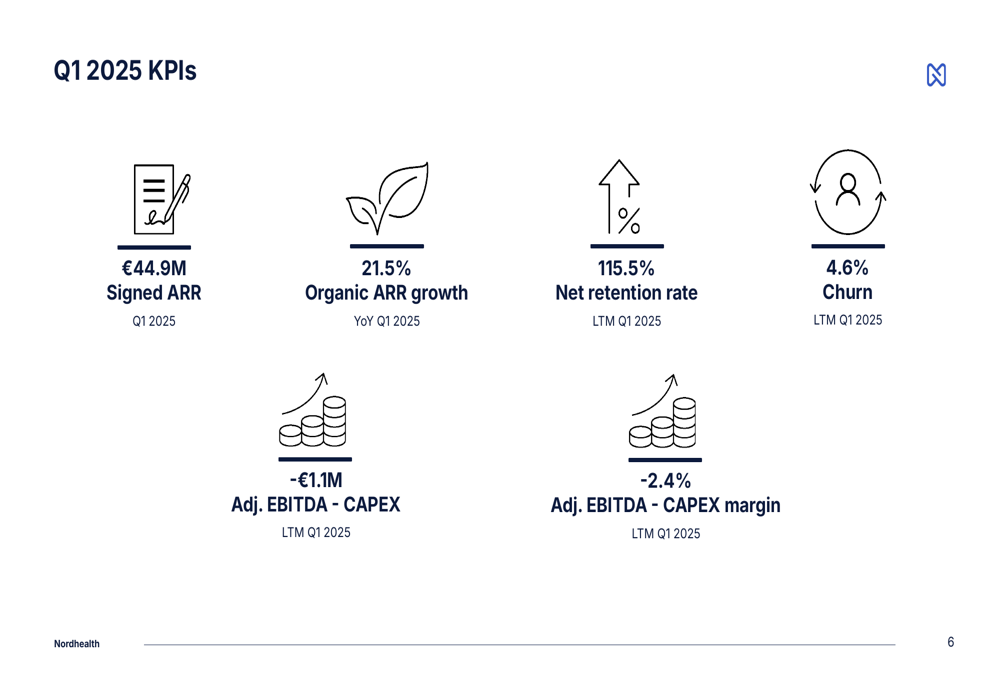

Nordhealth AS (NORDH) presented its Q1 2025 results on May 13, 2025, showcasing continued growth in annual recurring revenue (ARR) and progress toward profitability. The company, which provides practice management software for veterinary and therapy businesses, reported a 21.5% year-over-year increase in signed ARR, reaching €44.9 million. This performance builds on the momentum from 2024, when the company achieved a 24% revenue increase for the full year.

The presentation, led by CEO Charles MacBain and CFO Alexander Cram, highlighted Nordhealth’s strategic focus on expanding its veterinary business, particularly in enterprise clients and international markets, while continuing the migration of customers to cloud-based solutions.

Quarterly Performance Highlights

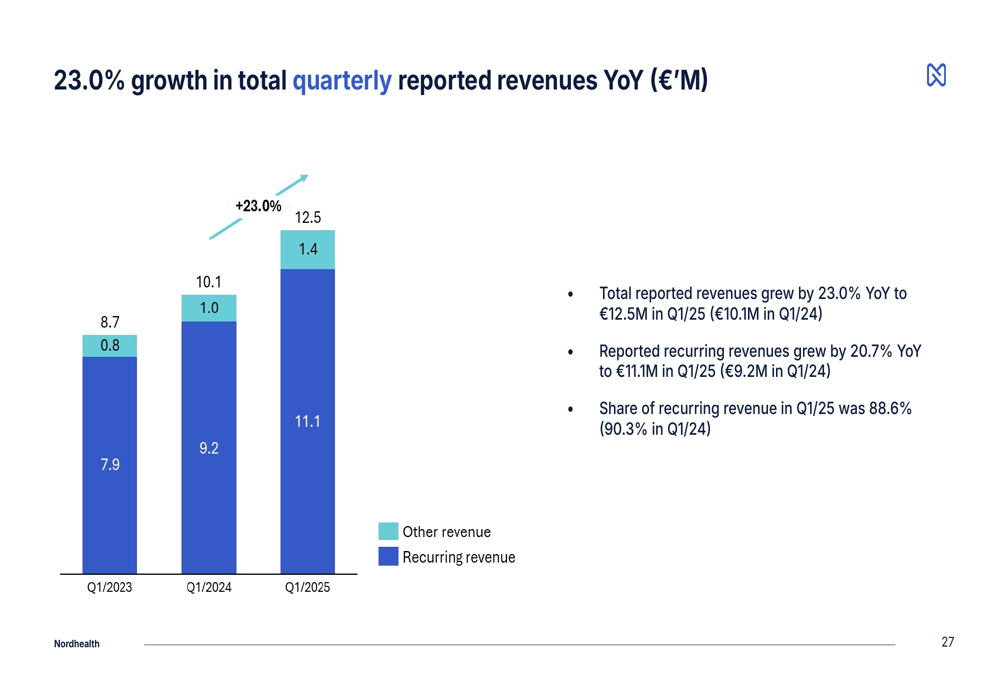

Nordhealth reported strong financial results for Q1 2025, with total revenue growing 23.0% year-over-year to €12.5 million. Recurring revenue, which represents 88.6% of total revenue, increased by 20.7% to €11.1 million compared to Q1 2024.

As shown in the following chart of quarterly revenue growth, both recurring and other revenue streams contributed to the company’s performance:

The company’s key performance indicators for Q1 2025 show solid growth metrics across the board, with a net retention rate of 115.5% and a churn rate of 4.6% for the last twelve months. The adjusted EBITDA minus CAPEX stood at -€1.1 million, representing a -2.4% margin, showing continued progress toward break-even.

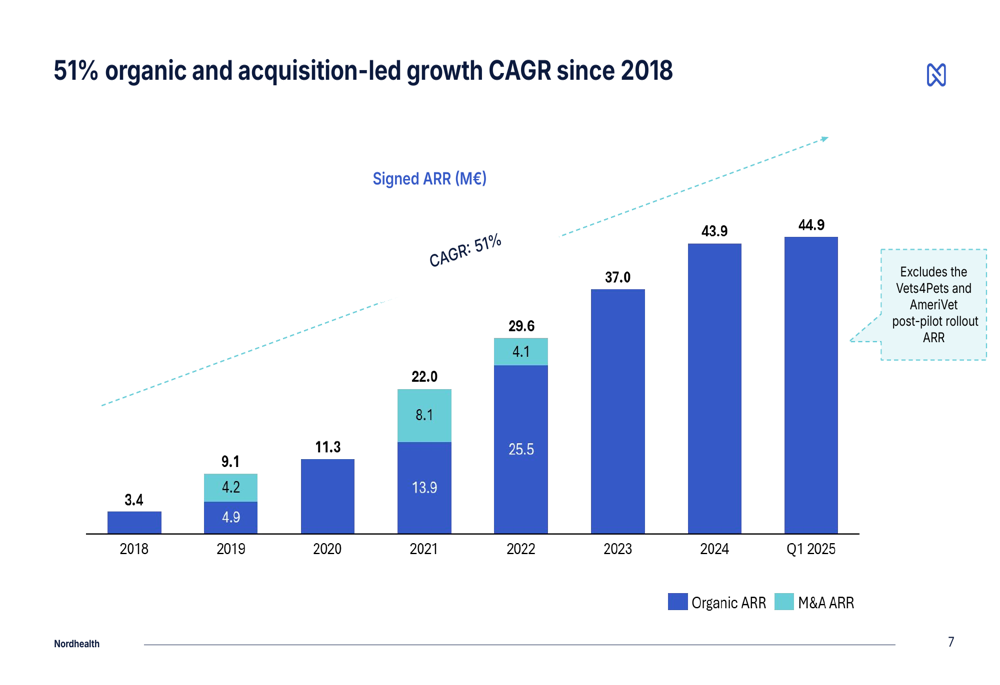

Nordhealth has maintained a consistent growth trajectory since 2018, achieving a 51% compound annual growth rate (CAGR) in signed ARR through both organic growth and acquisitions. The following chart illustrates this long-term growth pattern:

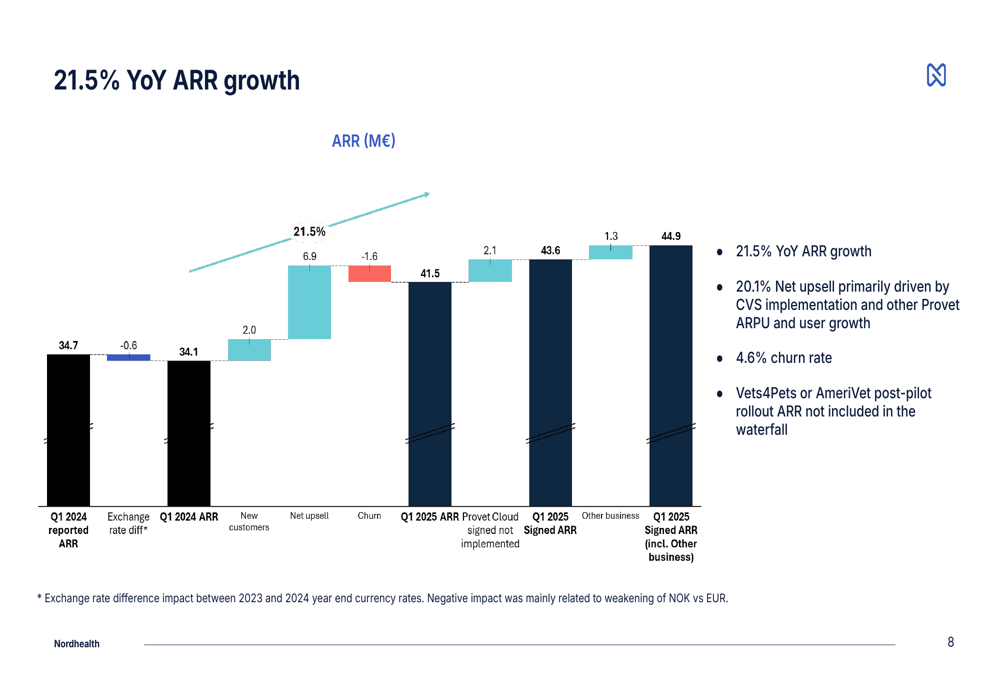

Breaking down the year-over-year ARR growth, the company provided a detailed waterfall chart showing the components contributing to the 21.5% increase:

Veterinary Business Performance

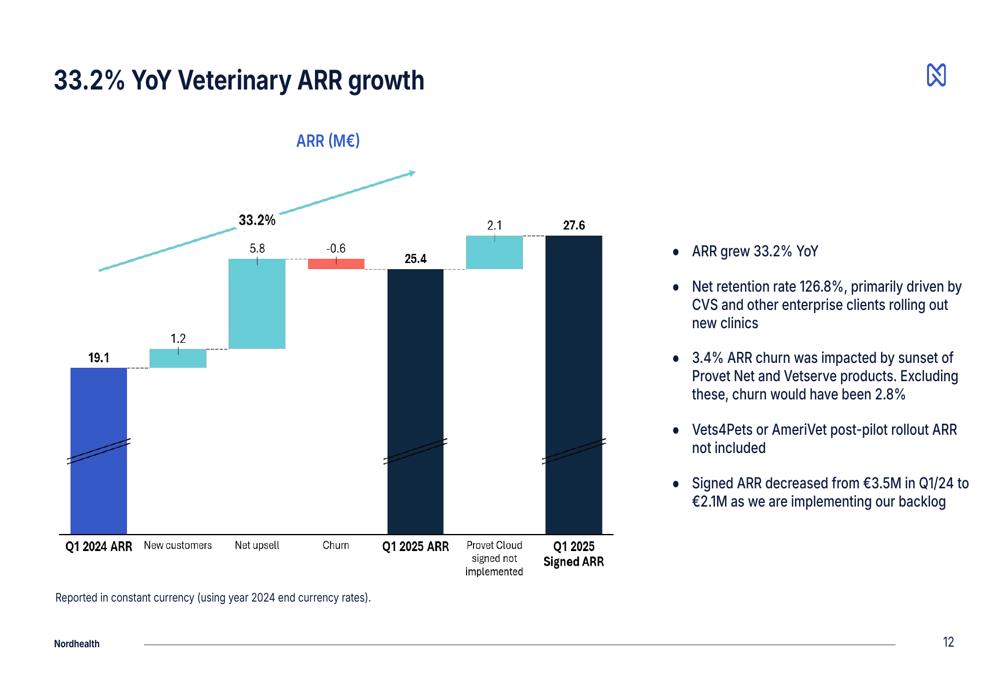

The veterinary segment continues to be Nordhealth’s growth engine, with ARR increasing by 33.2% year-over-year to €25.4 million. This growth was primarily driven by net upsell to existing customers, which contributed €5.8 million to the ARR increase, while new customers added €1.2 million.

The following waterfall chart breaks down the components of the veterinary segment’s ARR growth:

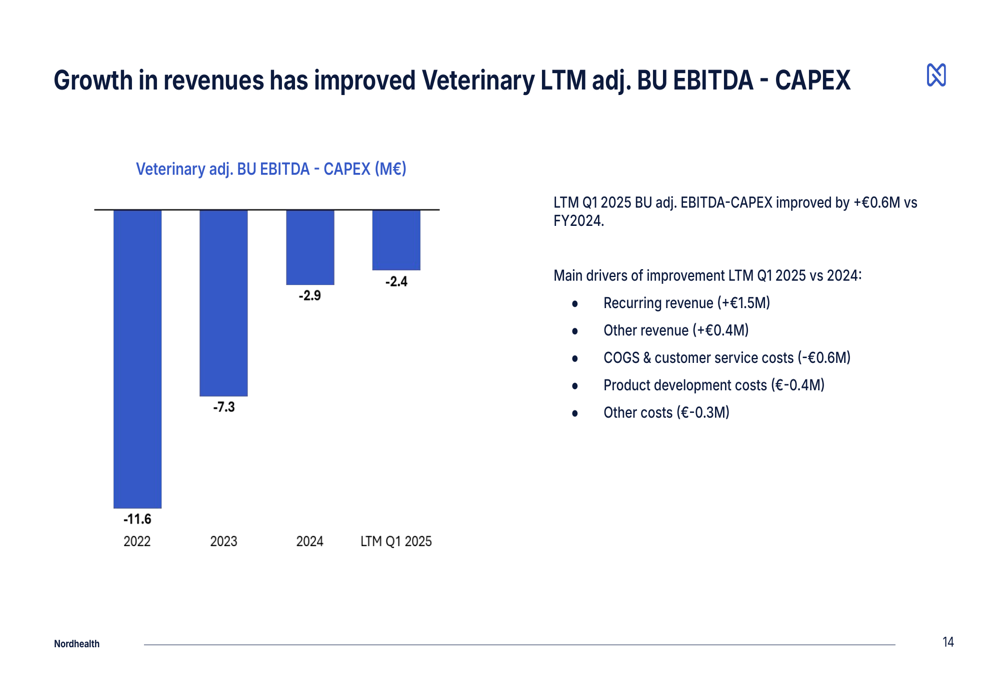

The veterinary business unit’s adjusted EBITDA minus CAPEX improved by €0.6 million compared to FY2024, reaching -€2.4 million for the last twelve months ending Q1 2025. This improvement was driven by increased recurring revenue (+€1.5 million) and other revenue (+€0.4 million), partially offset by higher costs.

Nordhealth reported significant progress in its enterprise strategy within the veterinary segment, with enterprise clients now representing 43% of total veterinary ARR, up from 21% in 2021. The company highlighted new business wins, including a pilot with AmeriVet, a 200+ location US clinic chain, and the signing of PetVet365, a 35-location US clinic chain, in May 2025.

The company also noted that 48% of veterinary ARR now comes from outside the Nordic region, demonstrating successful geographic expansion. Additionally, cloud-based solutions now account for 78% of veterinary ARR, up from 40% in 2021, reflecting the ongoing migration from legacy systems.

Therapy Business Performance

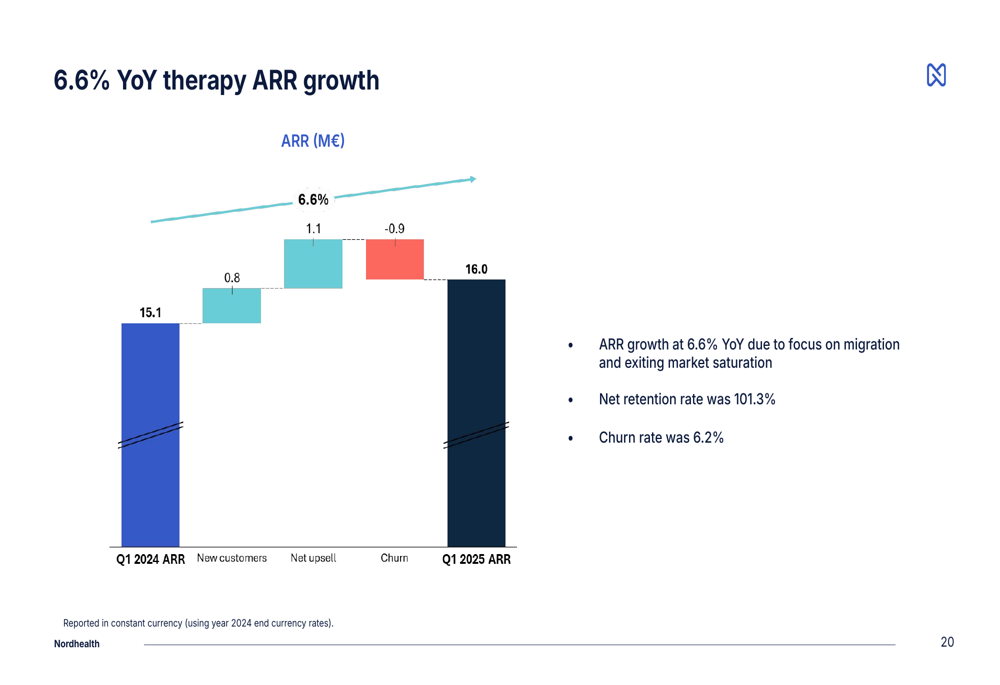

The therapy segment showed more modest growth, with ARR increasing by 6.6% year-over-year to €16.0 million. New customers contributed €0.8 million to ARR growth, while net upsell added €1.1 million, partially offset by €0.9 million in churn.

The following chart details the therapy segment’s ARR growth components:

The therapy business unit’s adjusted EBITDA minus CAPEX decreased slightly to €0.8 million for the last twelve months ending Q1 2025, compared to €1.2 million for FY2024. This decline was primarily due to increased product development costs (-€0.6 million), partially offset by higher recurring revenue (+€0.2 million).

Nordhealth highlighted progress in migrating Aspit users to its Unified Platform, with approximately 160 users migrated and only one user churning. The company also launched AI Scribe in April for Norwegian physiotherapists, attracting over 250 daily active users.

Financial Position and Outlook

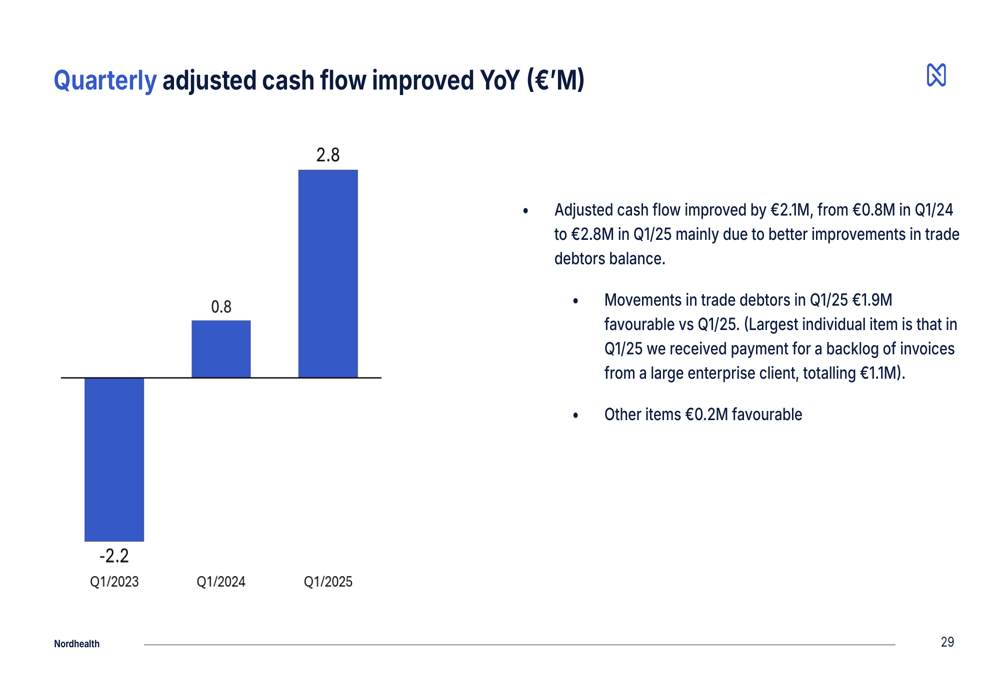

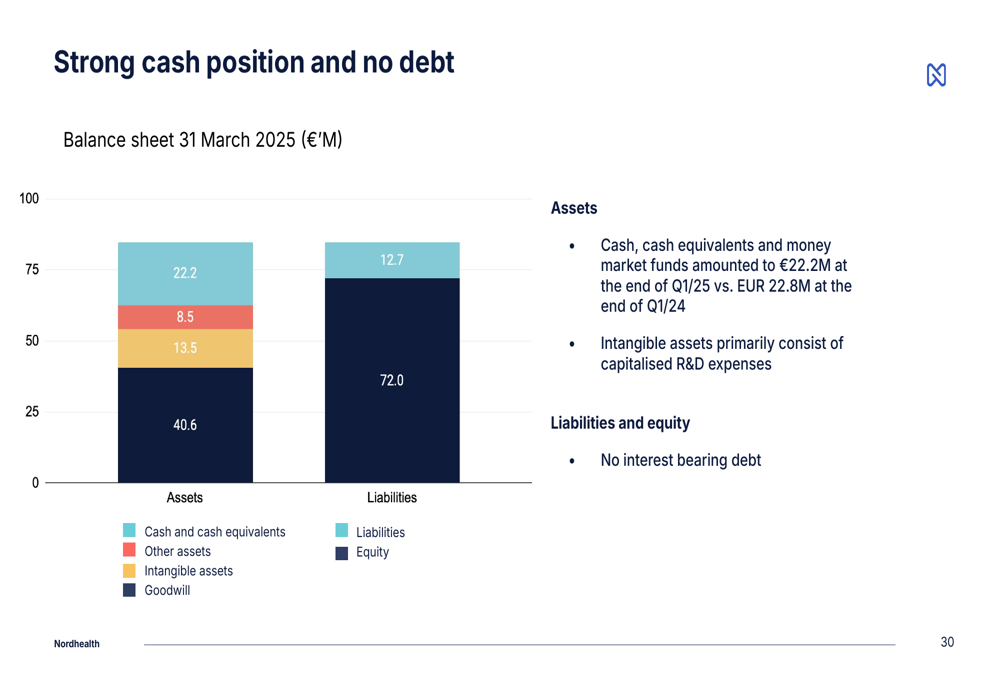

Nordhealth reported a strong financial position with €22.2 million in cash and cash equivalents as of March 31, 2025, and no debt. The company’s adjusted cash flow improved significantly, reaching €2.8 million in Q1 2025 compared to €0.8 million in Q1 2024, a €2.1 million improvement year-over-year.

The company’s balance sheet remains solid, with total assets of €84.7 million and equity of €72.0 million as of March 31, 2025:

Looking ahead, Nordhealth reiterated its guidance for 2025, projecting 12-17% organic growth in veterinary and therapy recurring revenue (at December 31, 2024 constant currency) excluding acquisitions. The company also expects adjusted EBITDA minus CAPEX to be plus or minus €2 million, excluding acquisitions.

This guidance aligns with the company’s statements from its Q4 2024 earnings call, where management indicated a more moderate growth trajectory for 2025 as the company focuses on completing the CVS rollout and platform migrations, particularly in the therapy business.

Nordhealth’s Q1 2025 results demonstrate continued progress on its growth strategy, with strong performance in the veterinary segment and steady improvement in financial metrics. The company’s focus on enterprise clients, cloud migration, and international expansion positions it well for sustainable growth, while its solid financial position provides flexibility for future investments and acquisitions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.