Procore signs multi-year strategic collaboration agreement with AWS

Introduction & Market Context

Nordhealth AS (NORDH) presented its Q2 2025 financial results on August 19, 2025, showcasing steady growth in annual recurring revenue (ARR) and strategic advancements in artificial intelligence capabilities. The company’s stock closed at 35.8 on August 18, representing a 2.29% increase ahead of the earnings announcement.

CEO Charles MacBain and CFO Alexander Cram led the presentation, highlighting the company’s continued expansion in key markets, particularly in the veterinary segment, while maintaining strong unit economics despite increased investments in research and development.

Quarterly Performance Highlights

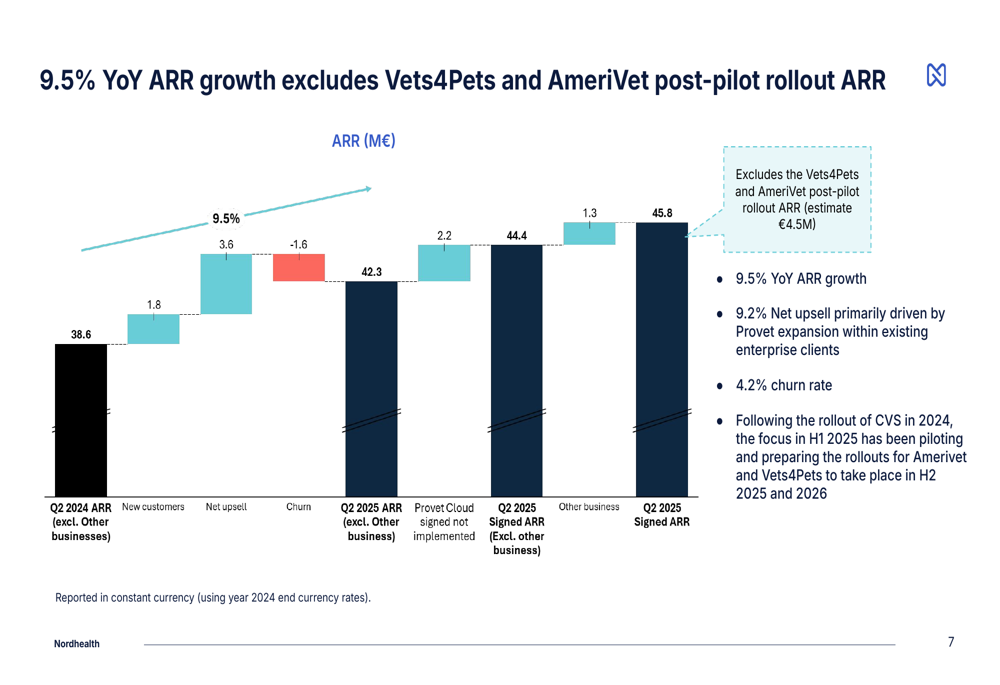

Nordhealth reported a 9.5% year-over-year growth in ARR, reaching €45.8 million in Q2 2025, excluding potential additional revenue from enterprise rollouts. The company’s veterinary business unit outperformed with 13.0% YoY ARR growth, while the therapy segment grew at a more modest 4.3%.

As shown in the following chart of ARR growth components, new customers and net upsell contributed positively, while churn remained manageable at 4.2%:

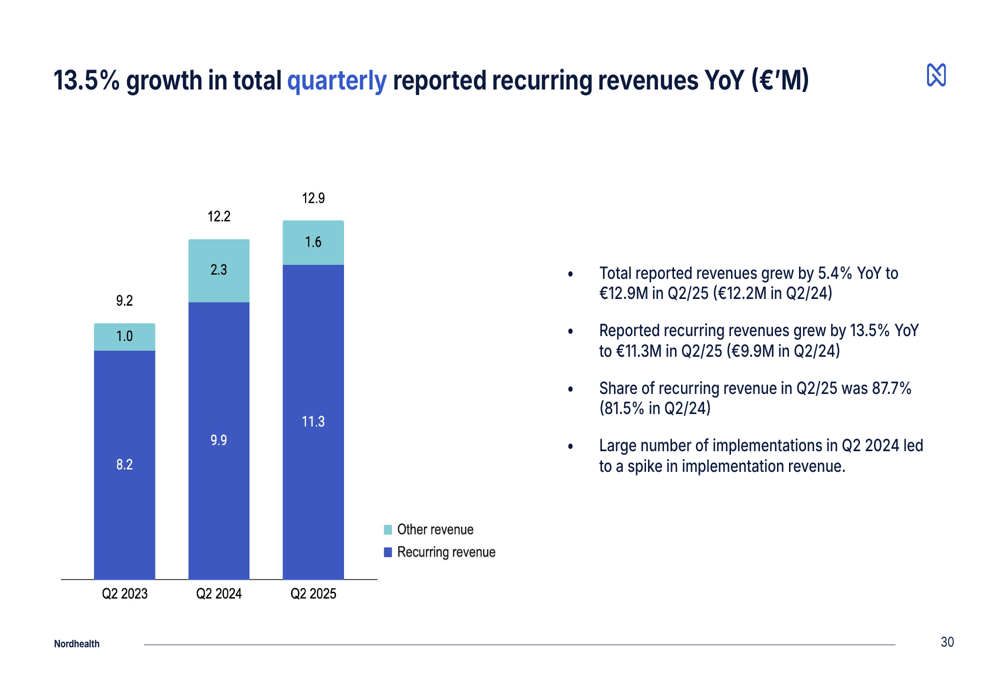

The company’s recurring revenue continues to form the backbone of its business model, with quarterly recurring revenue growing 13.5% year-over-year to €12.9 million in Q2 2025. This represents a continuation of the strong performance seen in Q1, where recurring revenue grew by 20.7% YoY.

The following chart illustrates the steady growth in quarterly recurring revenue:

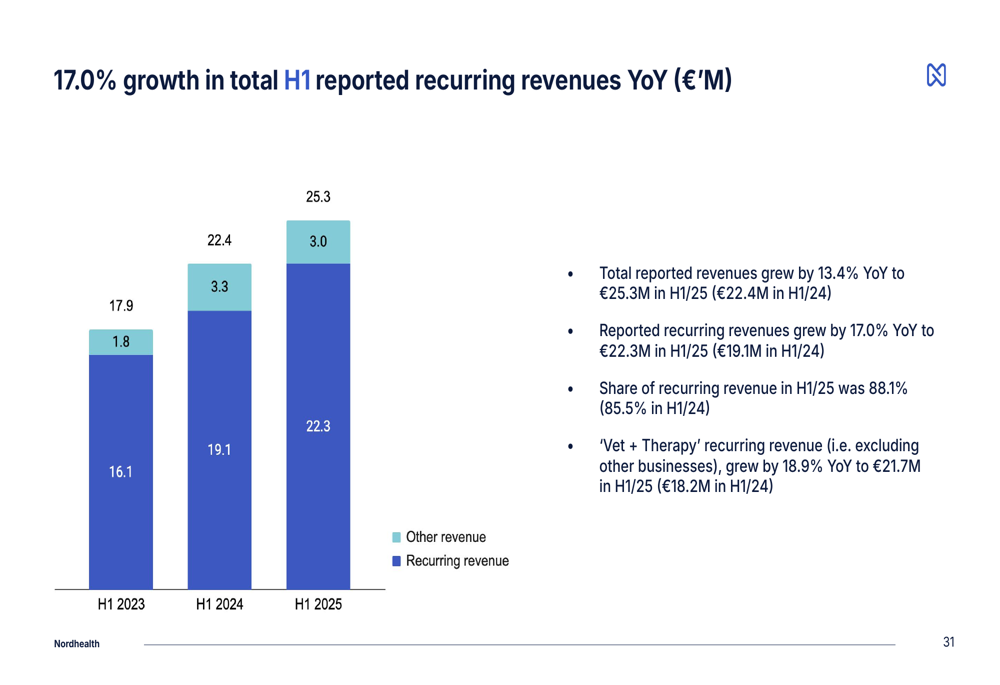

For the first half of 2025, total recurring revenue increased by 17.0% compared to H1 2024, reaching €25.3 million:

Strategic Initiatives

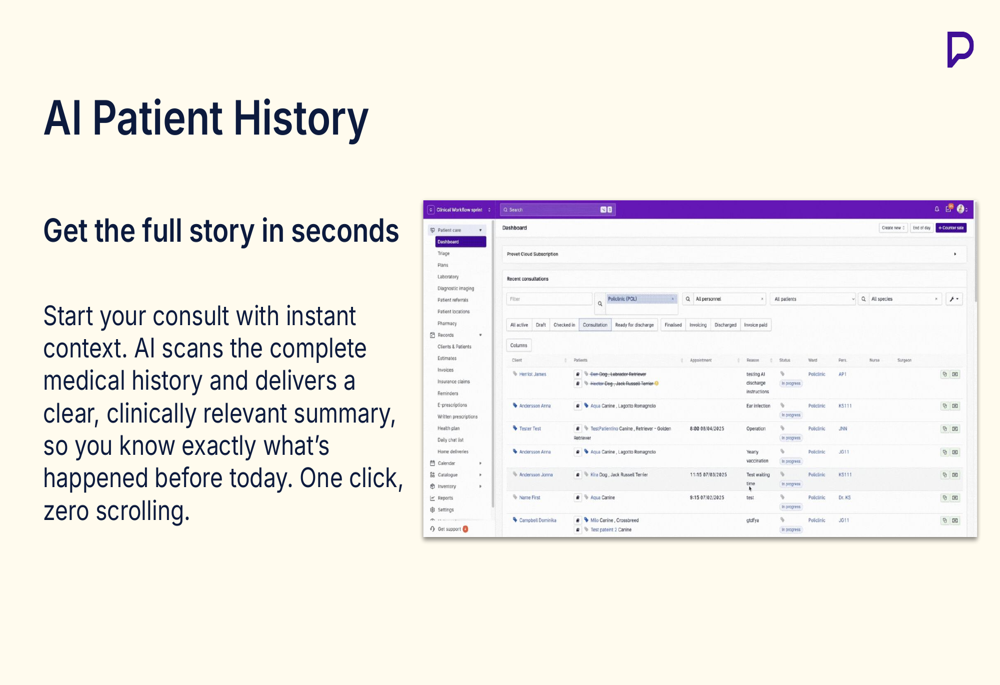

A major highlight of the quarter was the launch of Nordhealth’s first AI features for its Provet Cloud veterinary platform in August 2025, with 44 veterinary practices already signed up before launch. The company introduced three key AI capabilities designed to improve workflow efficiency for veterinary practices.

The AI Patient History feature provides instant summaries of patient medical records:

The AI Scribe functionality, which had already gained traction with over 250 daily active users by Q1 2025, creates real-time narrative notes during examinations:

Additionally, the AI Discharge Instructions feature automatically generates personalized patient instructions:

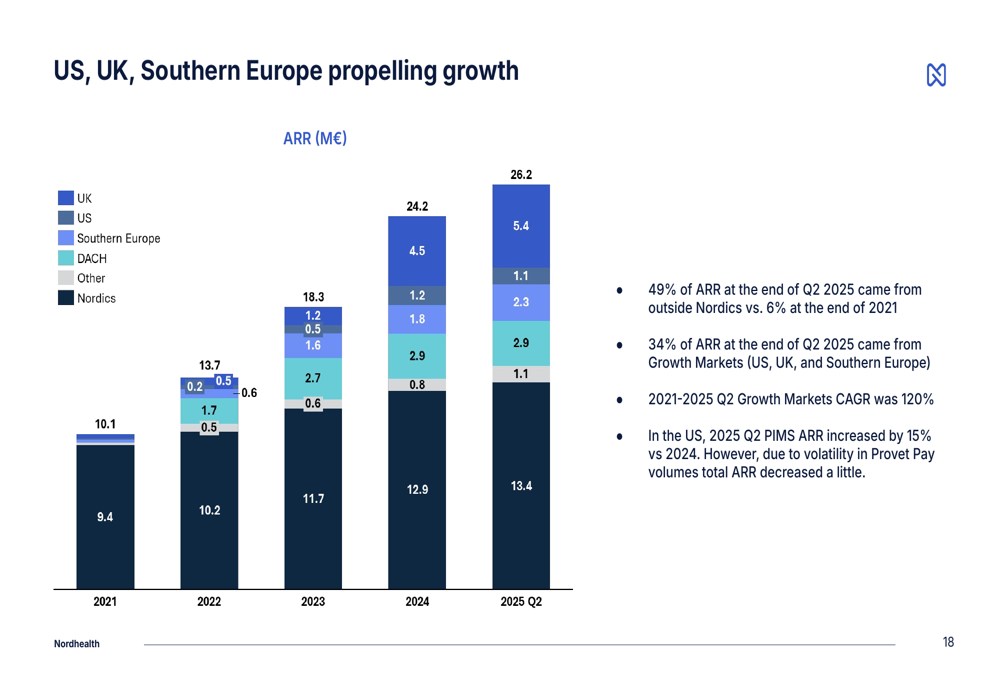

Nordhealth continues to focus on geographic expansion, with 49% of ARR now coming from outside the Nordic region. The US, UK, and Southern European markets are driving significant growth, as illustrated in this market breakdown:

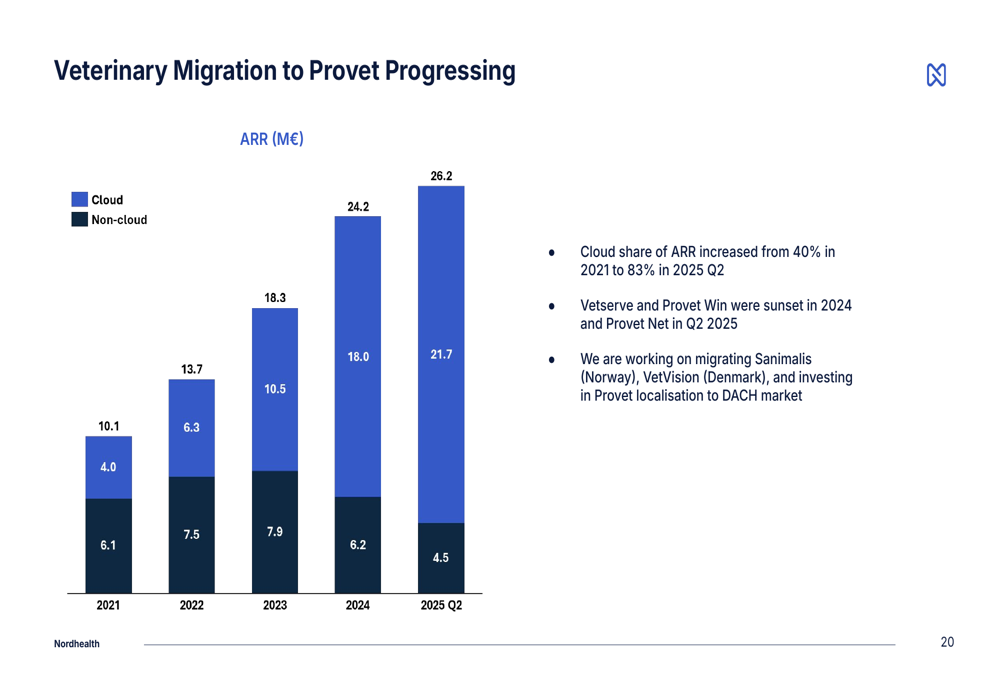

The company is also making progress in migrating customers to its cloud platforms, with cloud solutions now representing 83% of ARR in the veterinary segment, up from 40% in 2021:

Detailed Financial Analysis

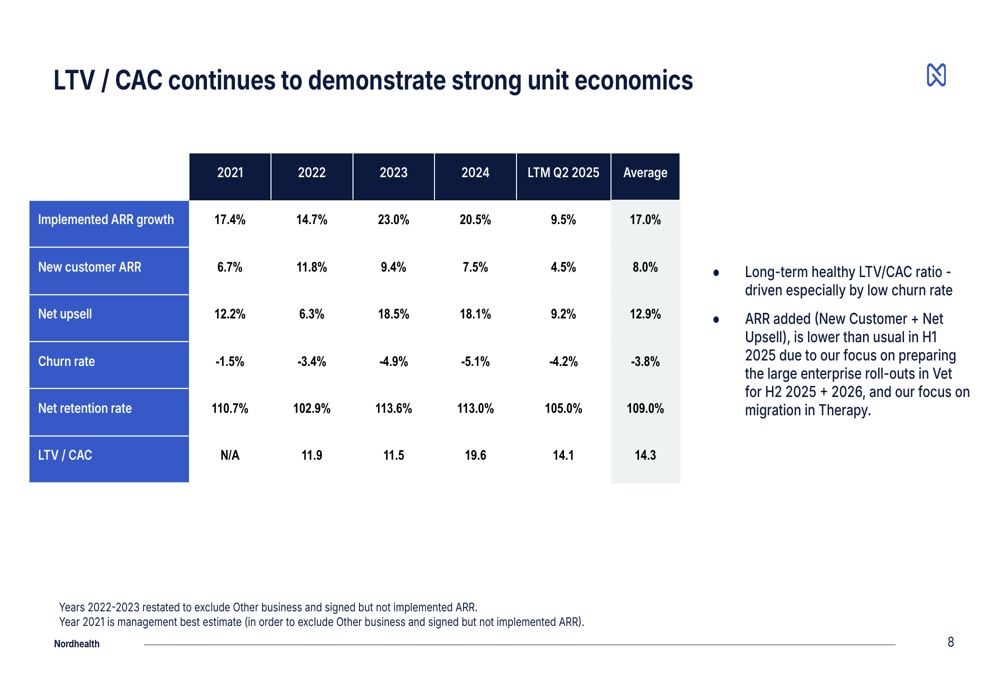

Nordhealth has maintained strong unit economics with an average LTV/CAC ratio of 14.3, indicating efficient customer acquisition:

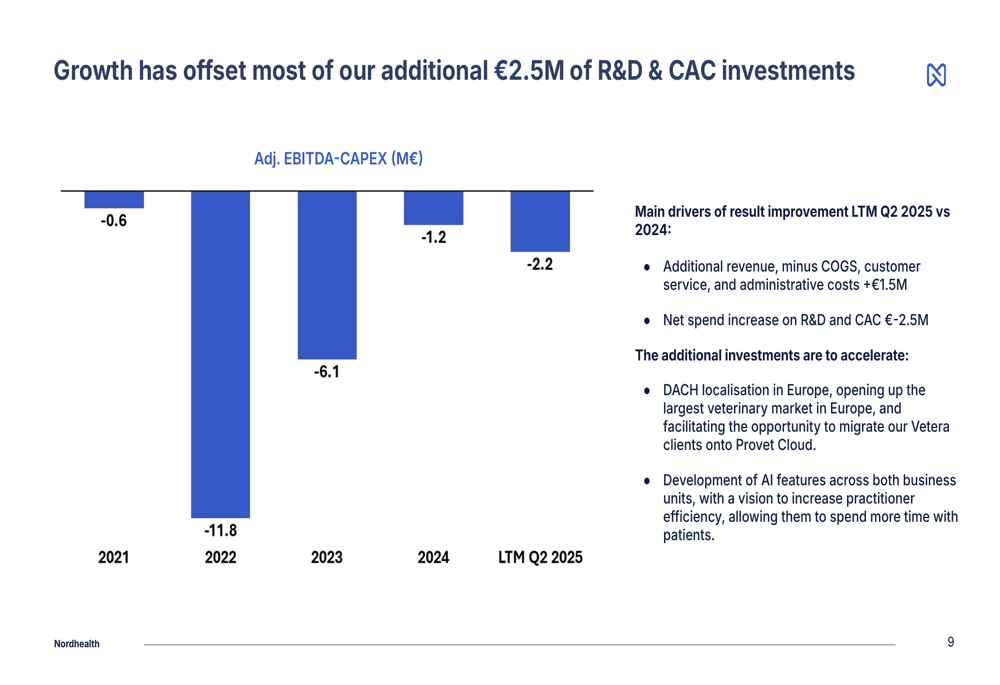

The company’s adjusted EBITDA minus CAPEX has improved significantly since 2022, narrowing to -€2.2 million for the last twelve months ending Q2 2025, compared to -€11.8 million in 2022:

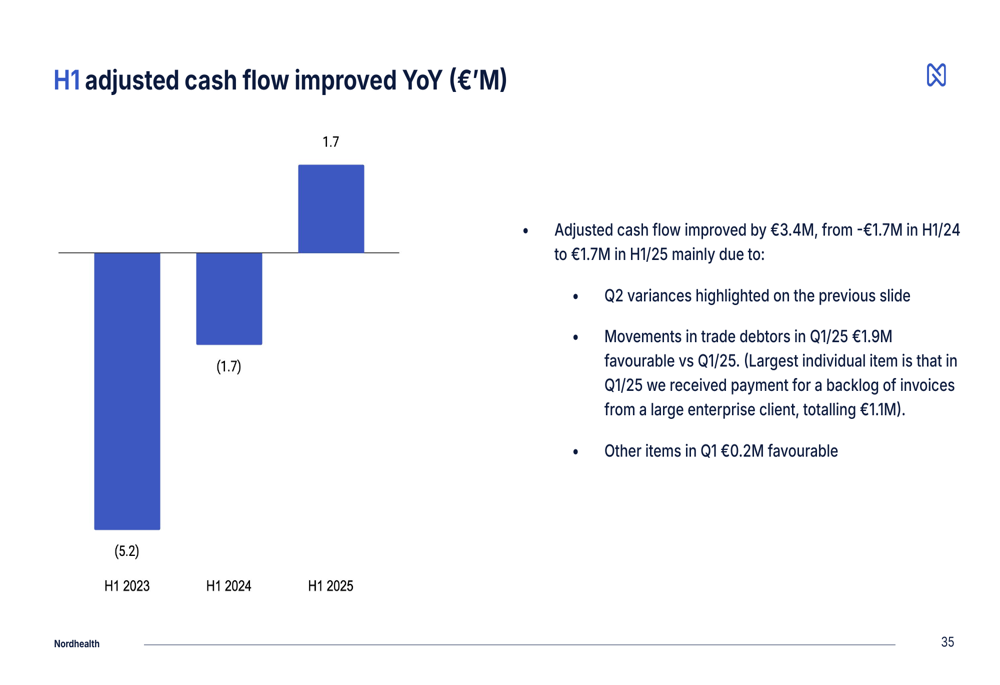

A notable financial achievement was the improvement in adjusted cash flow, which turned positive in H1 2025 at €1.7 million, compared to -€1.7 million in H1 2024 and -€5.2 million in H1 2023:

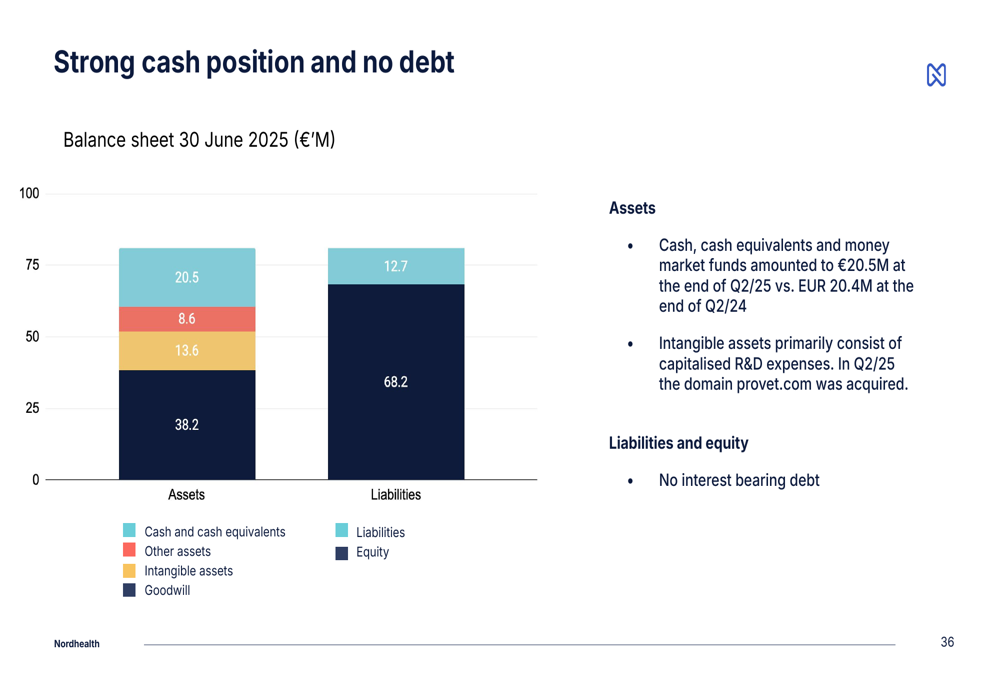

Nordhealth maintains a strong balance sheet with €20.5 million in cash and cash equivalents as of June 30, 2025, and no debt. This represents a slight decrease from the €22.2 million reported at the end of Q1 2025, partly due to a share buyback program completed in July 2025, where the company purchased 300,000 shares at NOK 36 per share.

Forward-Looking Statements

Nordhealth maintained its revenue guidance for 2025, projecting 12-17% organic growth in both veterinary and therapy segments. However, the company updated its adjusted EBITDA minus CAPEX guidance to between -€4 million and -€2 million, excluding acquisitions.

Key growth catalysts for the remainder of 2025 include:

1. The rollout of Provet Cloud to AmeriVet practices following a successful pilot, with an estimated €4.5 million in additional ARR potential not yet included in current figures

2. Continued implementation at PetVet365, where 6 of 27 locations have been completed

3. Expansion of AI features across the customer base

4. Acceleration of Vetera migration to consolidate the veterinary platform

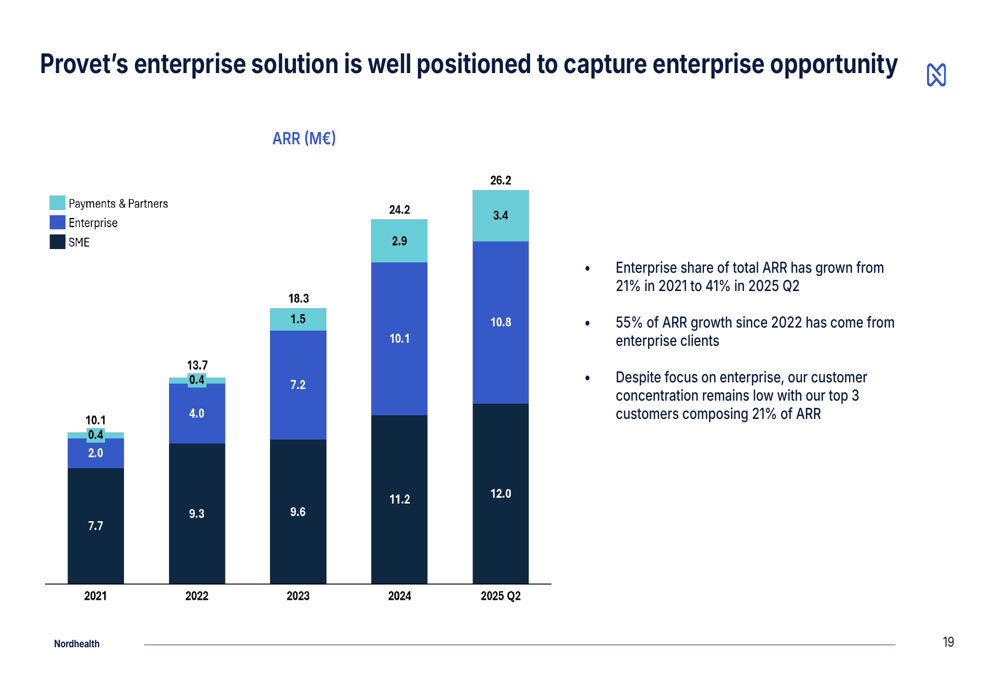

The company’s focus on enterprise customers is yielding results, with enterprise clients now representing 38% of total ARR, up from 26% in 2021:

While Nordhealth faces some challenges, including a slightly higher churn rate in the therapy segment (5.4%) compared to veterinary (3.4%), the company’s diversification across geographies and business segments, combined with its strong cash position and improving cash flow, positions it well for continued growth in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.