SoFi stock falls after announcing $1.5B public offering of common stock

Introduction & Market Context

Nykode Therapeutics ASA (NASDAQ:NYKD) presented its Q2 2025 results on August 27, highlighting a strategic refocus on three core assets and a return to profitability despite lower revenue. The immunotherapy company, currently trading at $1.73 per share, has implemented significant cost-cutting measures while maintaining a strong cash position to support its development pipeline through key upcoming milestones.

The company's presentation, delivered by CEO Michael Engsig, CSO Agnete Fredriksen, and CFO Harald Gurvin, outlined a highly focused approach aimed at reaching critical inflection points within the next 24 months across its prioritized assets.

Quarterly Performance Highlights

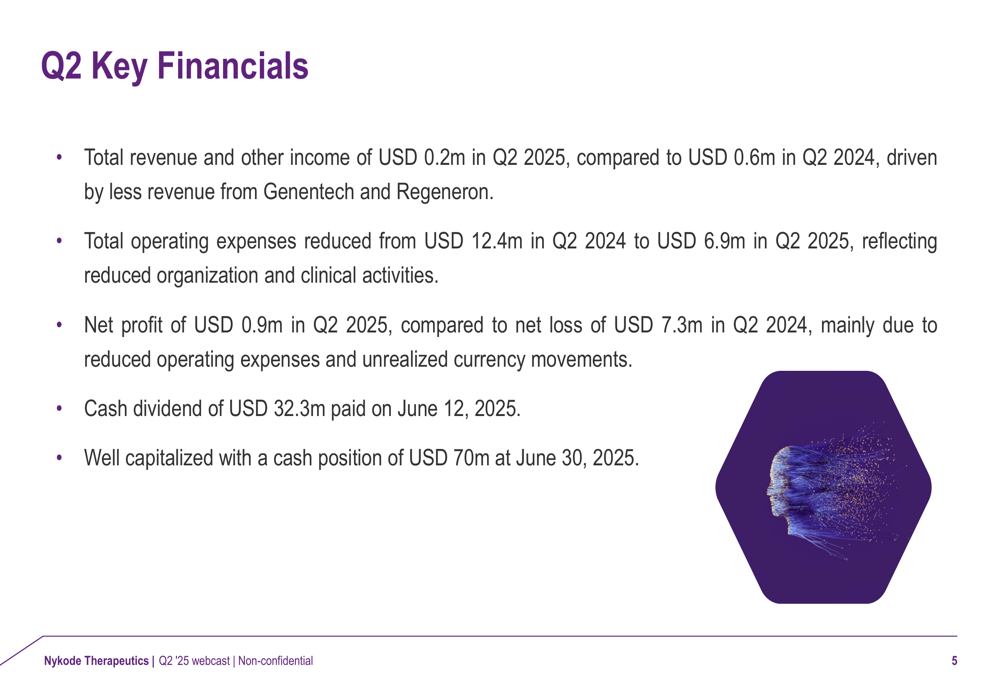

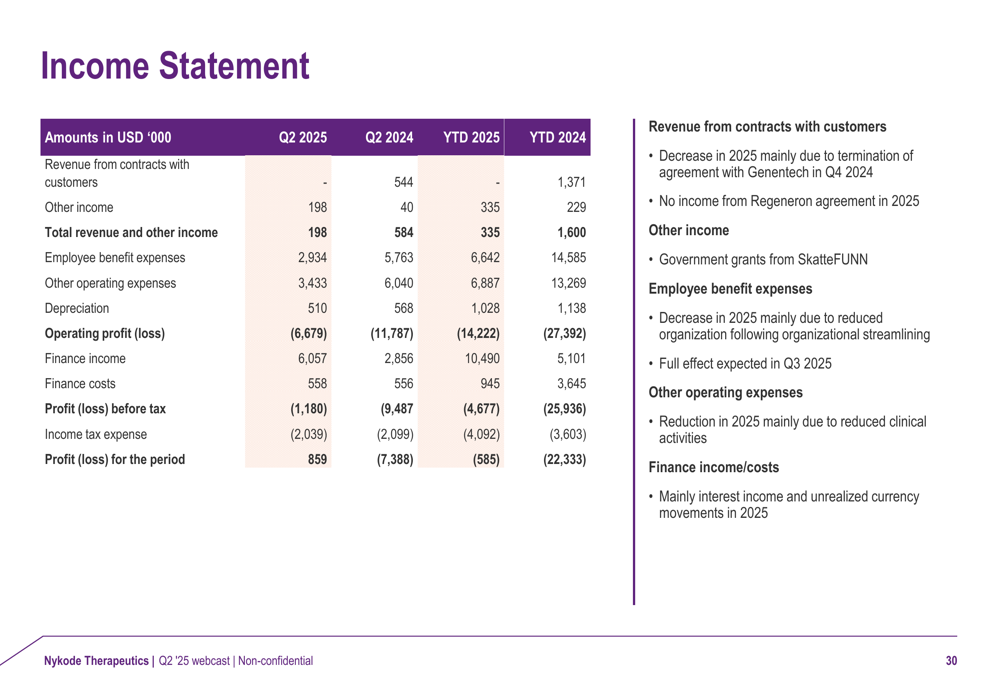

Nykode reported total revenue of $0.2 million in Q2 2025, down from $0.6 million in the same period last year, primarily due to reduced income from partnerships with Genentech and Regeneron. Despite the revenue decline, the company achieved a net profit of $0.9 million, compared to a net loss of $7.3 million in Q2 2024, marking a significant financial turnaround.

This improvement was largely driven by a substantial reduction in operating expenses, which decreased to $6.9 million from $12.4 million in Q2 2024, reflecting the company's restructuring efforts and more focused clinical activities.

As shown in the following financial summary from the presentation:

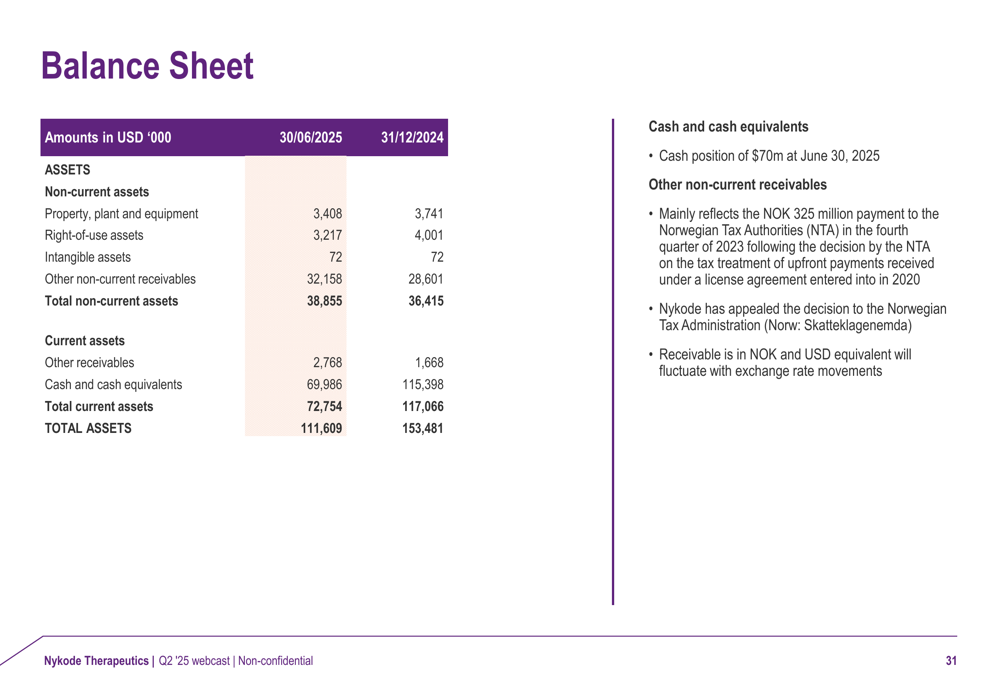

The company paid a cash dividend of $32.3 million on June 12, 2025, while maintaining a cash position of $70 million as of June 30, 2025. This strong financial foundation supports Nykode's strategy of reaching key inflection points within its cash runway, which is estimated to extend into 2028.

Strategic Initiatives

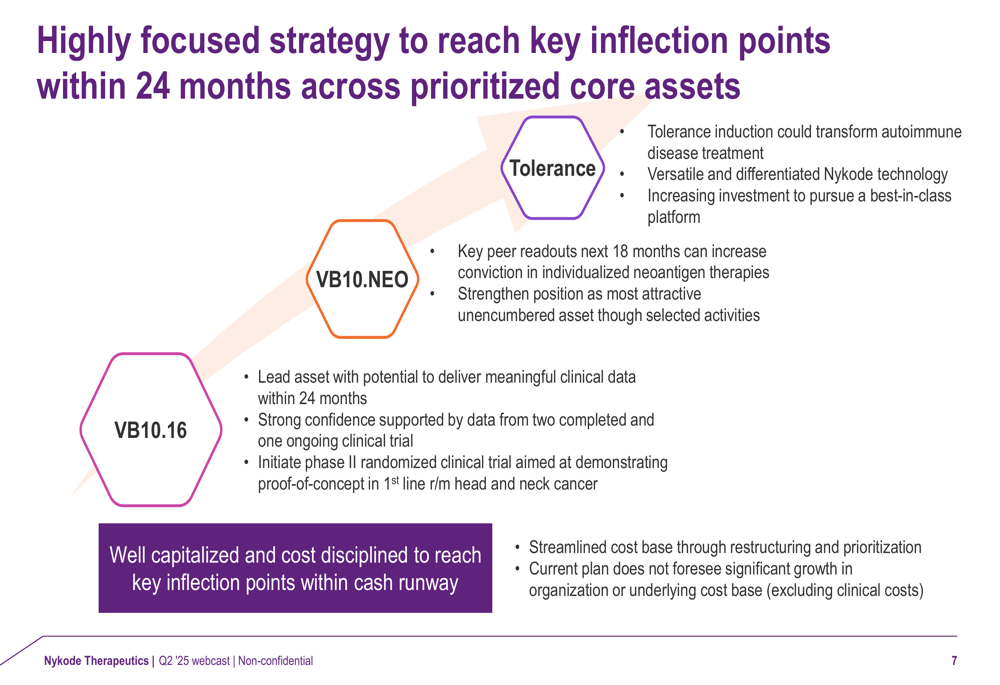

Nykode has implemented a highly focused strategy centered on three core assets: VB10.16 (abipapogene suvaplasmid), VB10.NEO, and its Tolerance platform. The company aims to deliver meaningful clinical data within 24 months while maintaining financial discipline.

The strategic framework is illustrated in the following slide:

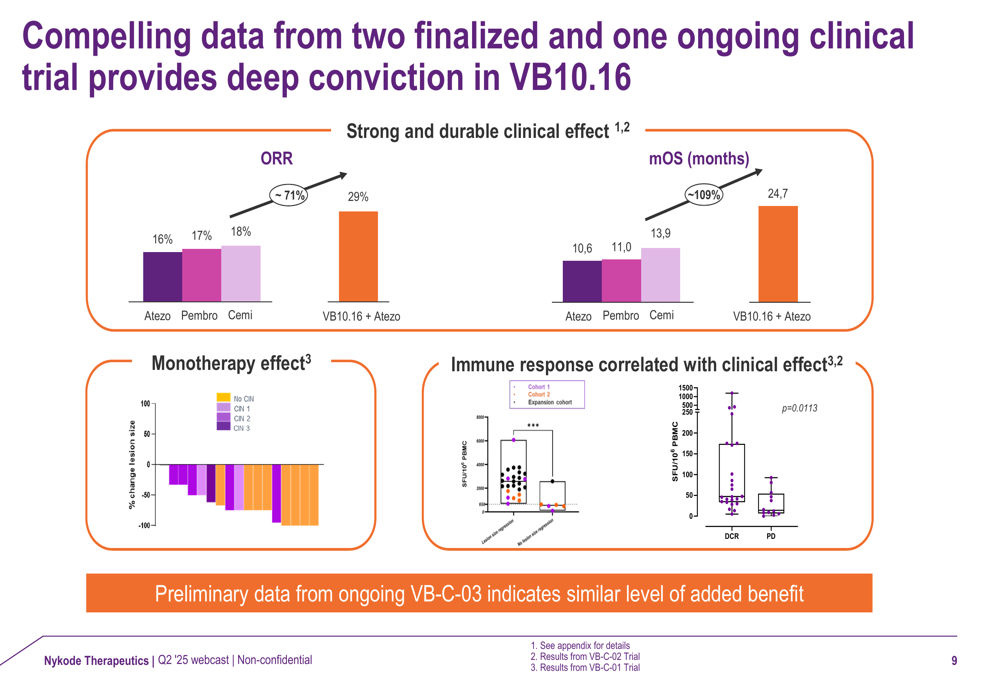

VB10.16 (abipapogene suvaplasmid or abi-suva) has been identified as the company's lead value driver, with plans to initiate a Phase II randomized clinical trial in first-line recurrent/metastatic head and neck cancer. The World Health Organization has accepted abipapogene suvaplasmid as the International Non-Proprietary Name for this asset.

The company presented compelling clinical data supporting VB10.16's potential, showing significantly improved outcomes when combined with atezolizumab compared to checkpoint inhibitor monotherapy:

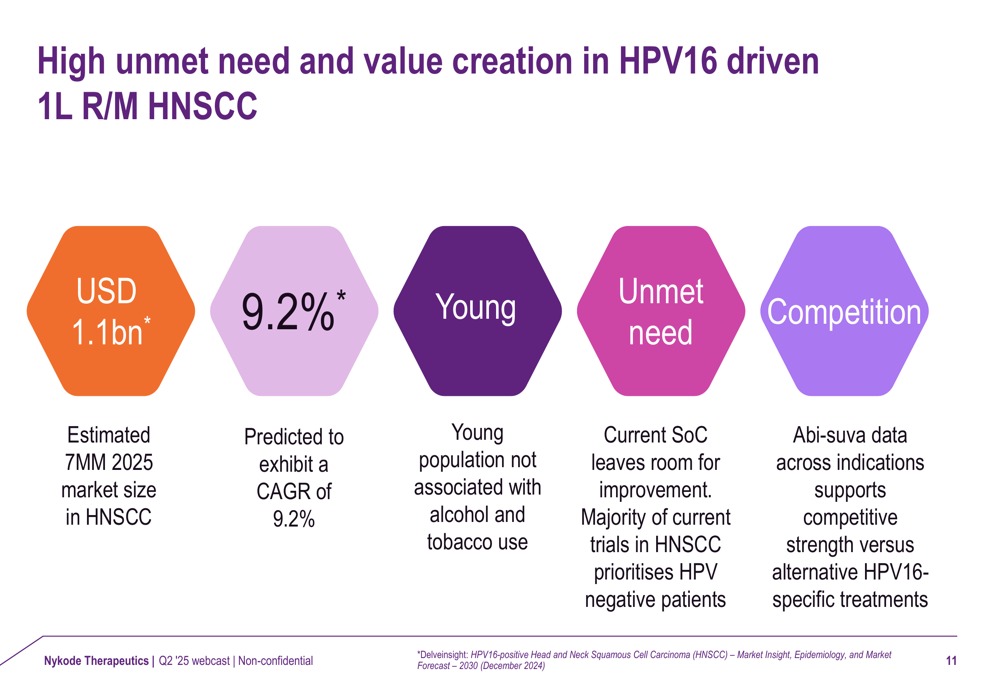

The market opportunity for VB10.16 in HPV16-driven head and neck cancer is substantial, with an estimated 2025 market size of $1.1 billion in major markets, expected to grow at a CAGR of 9.2%.

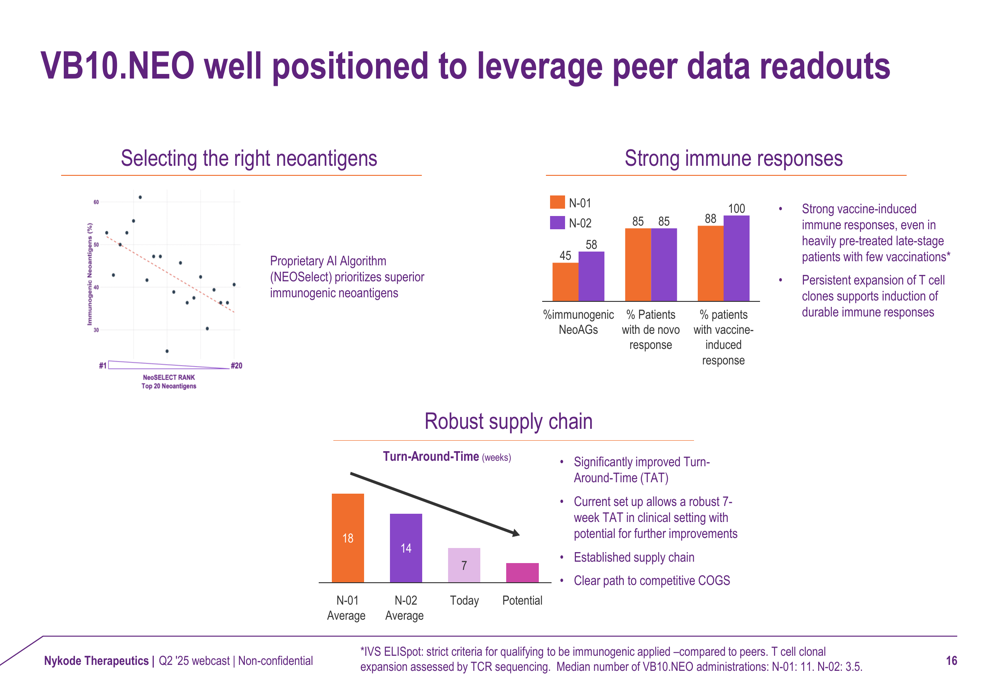

Nykode's second priority, VB10.NEO, is positioned as an individualized neoantigen therapy with potential applications across multiple tumor types. The company highlighted its proprietary AI algorithm for neoantigen selection and robust manufacturing capabilities:

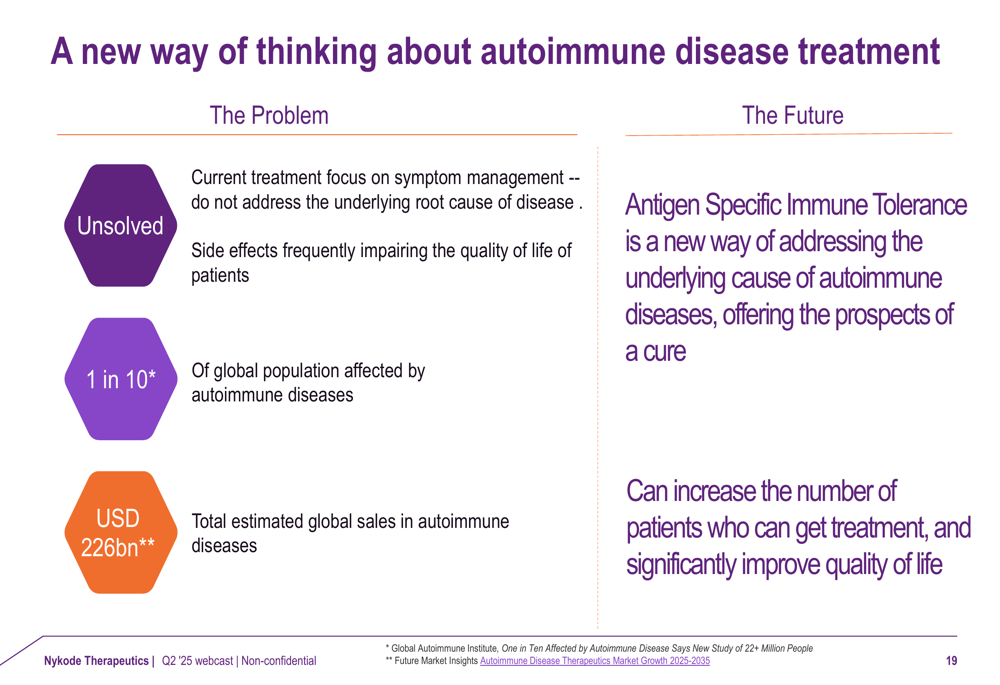

The third pillar of Nykode's strategy focuses on developing a best-in-class platform for antigen-specific immune tolerance in autoimmune diseases, a market estimated at $226 billion globally. The company believes this approach could address the root cause of autoimmune conditions rather than just managing symptoms.

Detailed Financial Analysis

Nykode's income statement shows the company's shift to profitability, with a net profit of $0.9 million in Q2 2025 compared to a net loss of $7.3 million in Q2 2024. This improvement was achieved despite lower revenue, primarily through significant cost reductions.

The balance sheet reveals a strong financial position with total assets of $111.6 million as of June 30, 2025, down from $153.5 million at the end of 2024, largely due to the dividend payment. The company maintains an equity ratio of 92%, reflecting its solid financial foundation.

Management emphasized that the company is well-positioned to execute its strategy with an estimated cash runway into 2028, potentially extending into 2029 with a positive outcome in a pending tax case.

Forward-Looking Statements

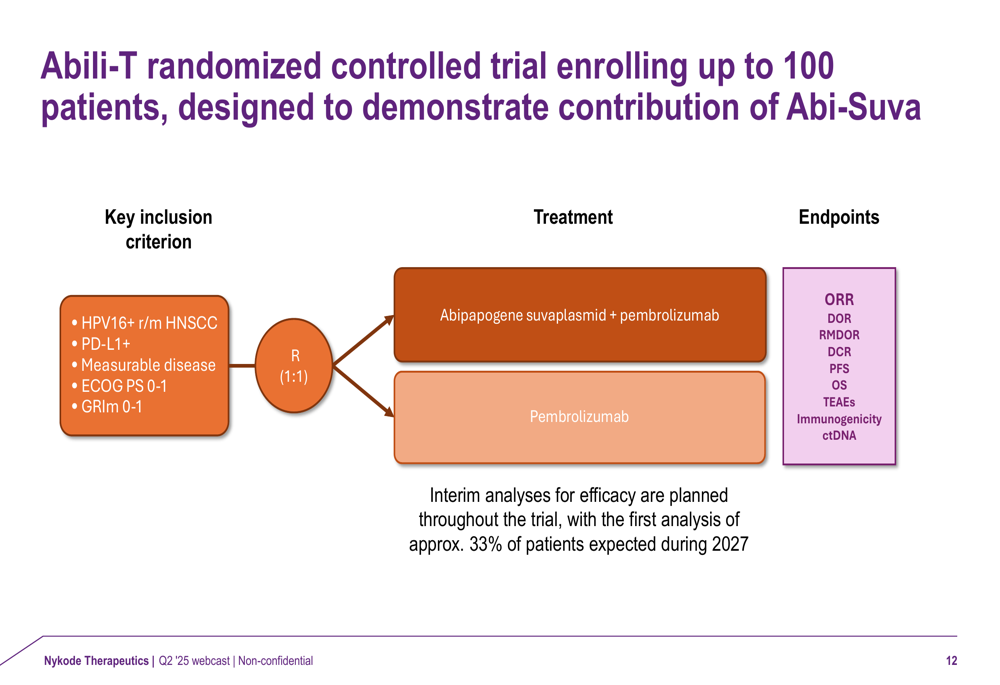

Looking ahead, Nykode plans to focus on advancing its lead asset, VB10.16, through the Abili-T randomized controlled trial in HPV16-positive recurrent/metastatic head and neck cancer. The trial will enroll up to 100 patients and is designed to demonstrate the contribution of abipapogene suvaplasmid when added to standard of care.

The company also noted that it is no longer including Regeneron collaboration programs in its updated strategy or financial forecasts, following discussions with the partner about the future of these programs.

For VB10.NEO, Nykode plans to leverage upcoming peer data readouts expected within the next 18 months to strengthen its position as "the most attractive unencumbered asset" in the individualized neoantigen therapy space.

In the Tolerance platform, the company is increasing investments to develop what it believes could be a best-in-class technology for treating autoimmune diseases by addressing their root causes rather than just managing symptoms.

Management emphasized that its current financial plan does not foresee significant growth in organization or underlying cost base (excluding clinical costs), maintaining the disciplined approach that has enabled its return to profitability while advancing key strategic programs.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.