US LNG exports surge but will buyers in China turn up?

Introduction & Market Context

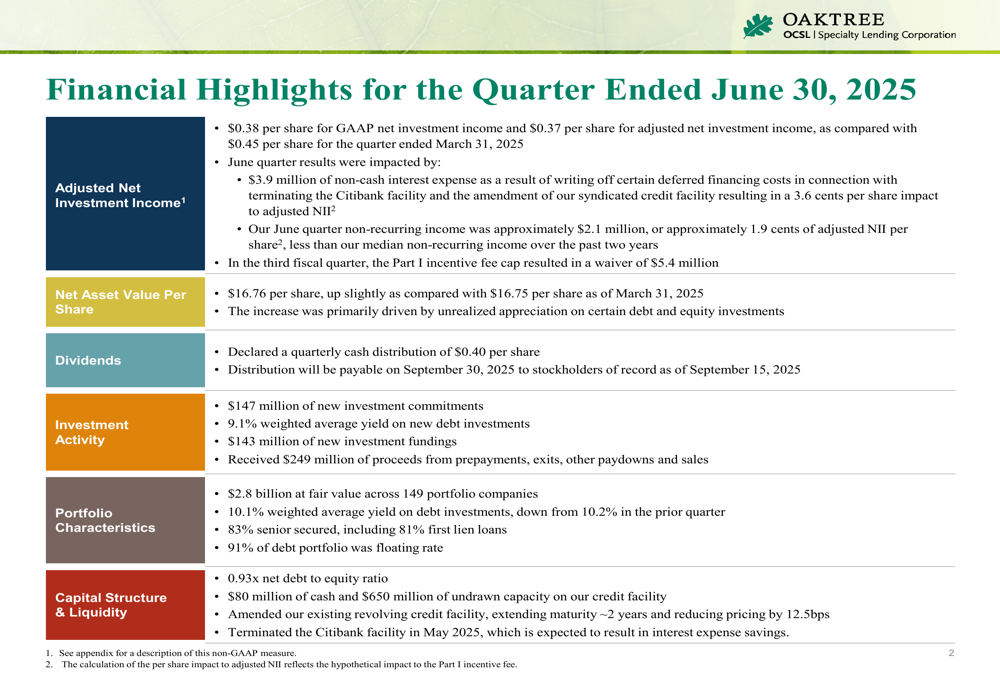

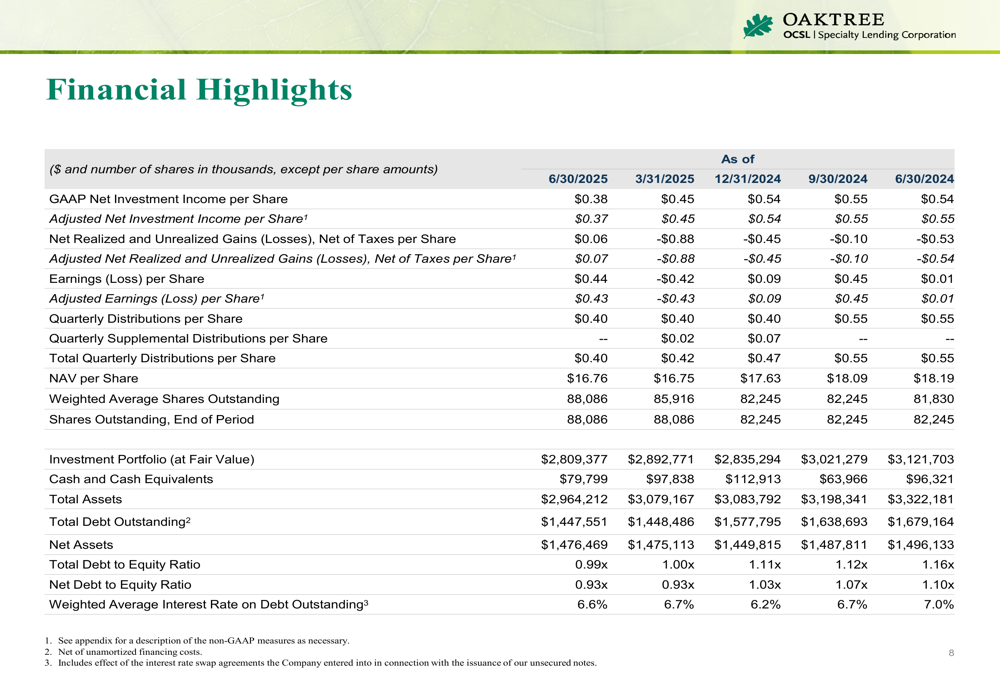

Oaktree Specialty Lending Corporation (NASDAQ:OCSL) released its third quarter 2025 earnings presentation on August 5, revealing mixed results that prompted a 2.59% pre-market stock decline to $13.16. The business development company reported adjusted net investment income of $0.37 per share, down from $0.45 in the previous quarter, while maintaining a slight increase in net asset value (NAV) per share to $16.76 from $16.75.

The company’s performance reflects broader challenges in the direct lending market, with OCSL missing both EPS and revenue forecasts. Despite these headwinds, management emphasized its conservative portfolio approach and strategic initiatives designed to support long-term shareholder value.

Quarterly Performance Highlights

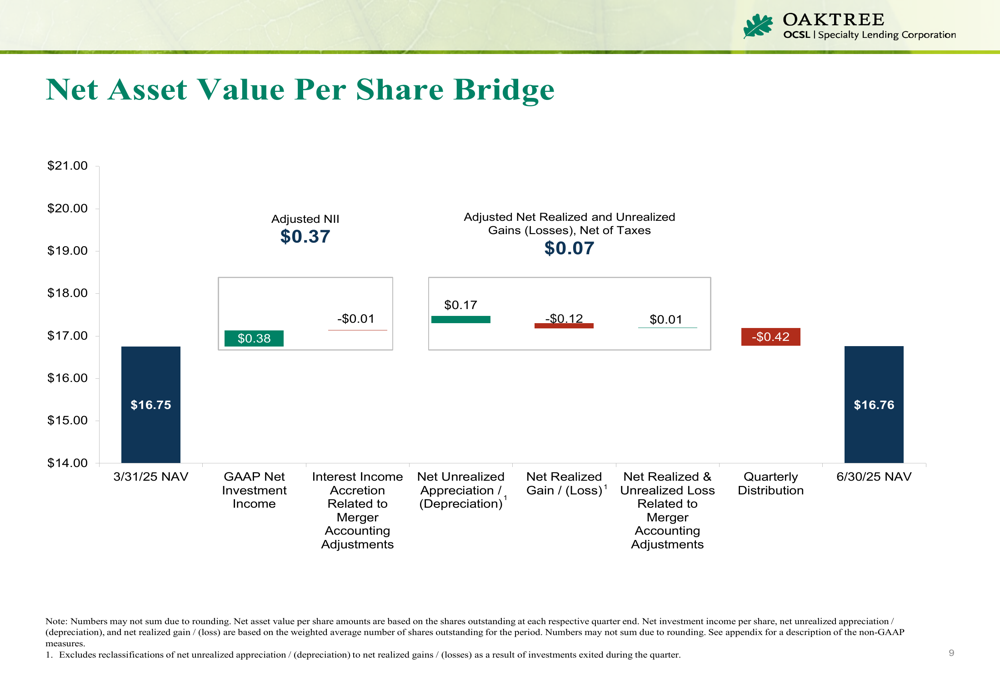

OCSL reported GAAP net investment income of $0.38 per share for the quarter ended June 30, 2025, with adjusted net investment income of $0.37 per share after accounting for non-recurring items. This represents a continued downward trend from $0.45 in the previous quarter and $0.55 a year ago.

The company maintained its quarterly cash distribution of $0.40 per share, resulting in an annualized dividend yield of approximately 22.87% based on current market prices. This distribution level exceeds the current adjusted NII, raising questions about dividend sustainability.

As shown in the following financial highlights chart:

Total (EPA:TTEF) investment income for the quarter was $75.3 million, below analyst expectations of $79.14 million. The company noted that results included a $3.9 million non-cash write-off from the termination of its Citibank facility and $2.1 million in non-recurring income. Additionally, an incentive fee cap resulted in a $5.4 million fee waiver for the quarter.

The NAV bridge illustrates how OCSL maintained stable NAV despite distributing more than it earned:

Portfolio and Investment Activity

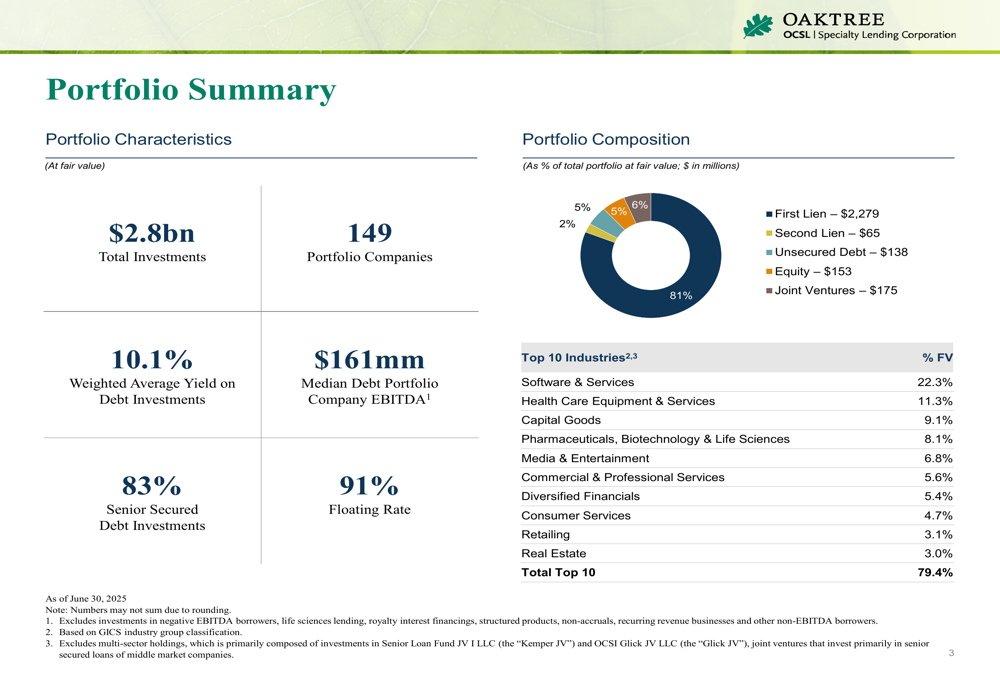

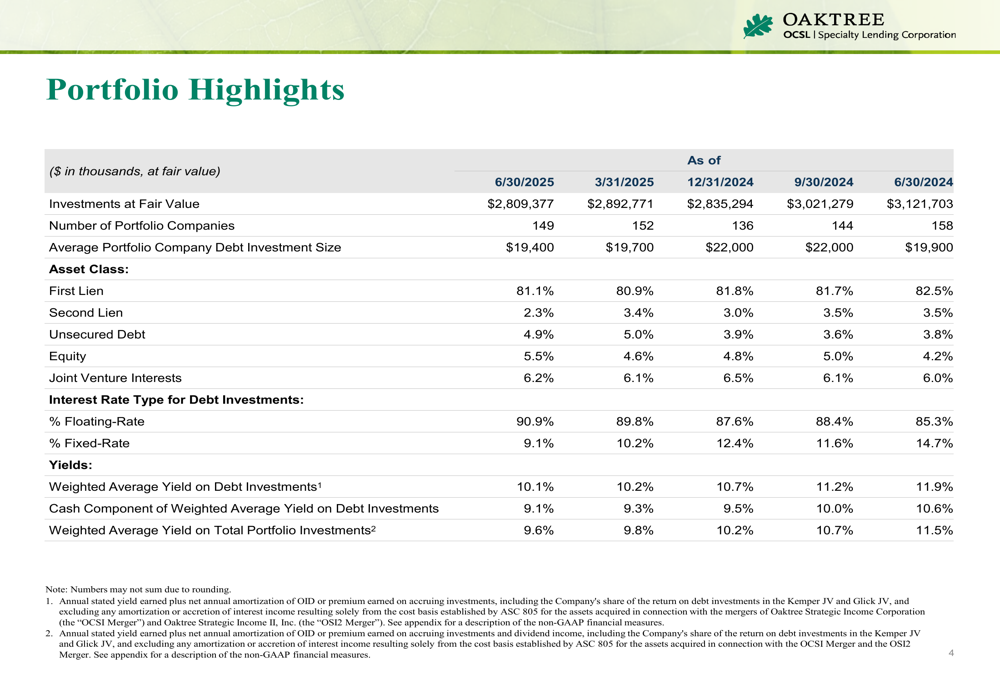

OCSL’s investment portfolio totaled $2.8 billion across 149 companies as of June 30, 2025. The portfolio remains defensively positioned with 83% in senior secured investments (81% first lien) and 91% in floating rate instruments, providing some protection against interest rate fluctuations.

The portfolio composition shows a strong emphasis on first lien debt, with significant exposure to software and healthcare sectors:

Investment activity slowed considerably during the quarter, with $147 million in new investment commitments and $143 million in new fundings, compared to $407 million and $406 million, respectively, in the previous quarter. The company also reported $249 million in proceeds from exits and prepayments, resulting in net negative investment activity of $106 million.

The following chart illustrates the recent investment activity trends:

New investments carried a weighted average yield of 9.1%, continuing a downward trend from 11.1% a year ago, reflecting the competitive lending environment and lower interest rate expectations. All new investments were first lien senior secured loans, and 100% were also held by other Oaktree funds, demonstrating alignment with the broader Oaktree platform.

Capital Structure and Liquidity

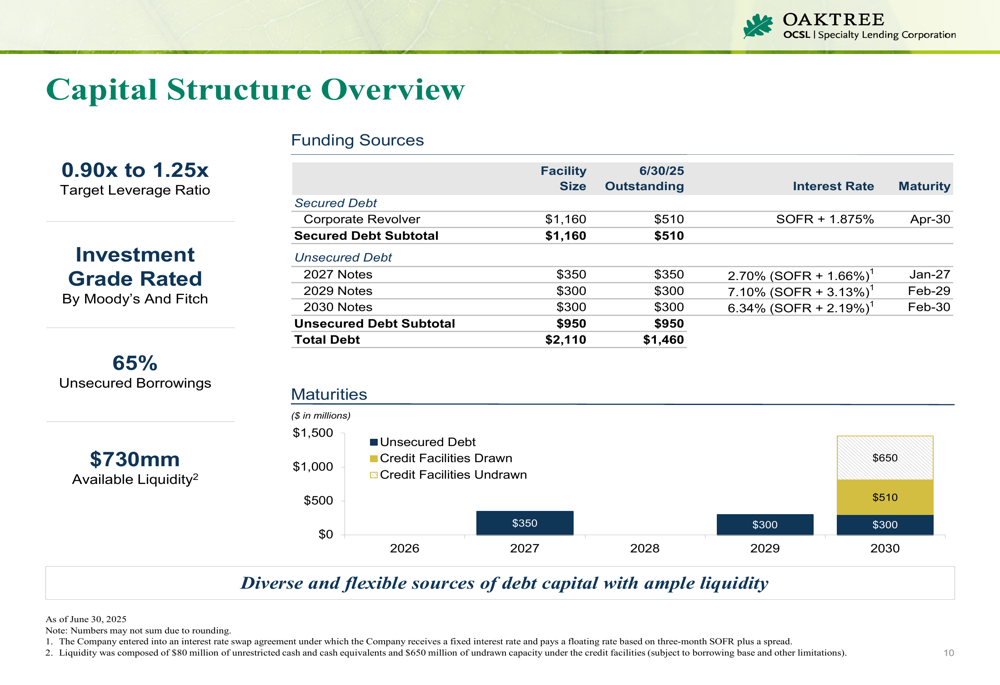

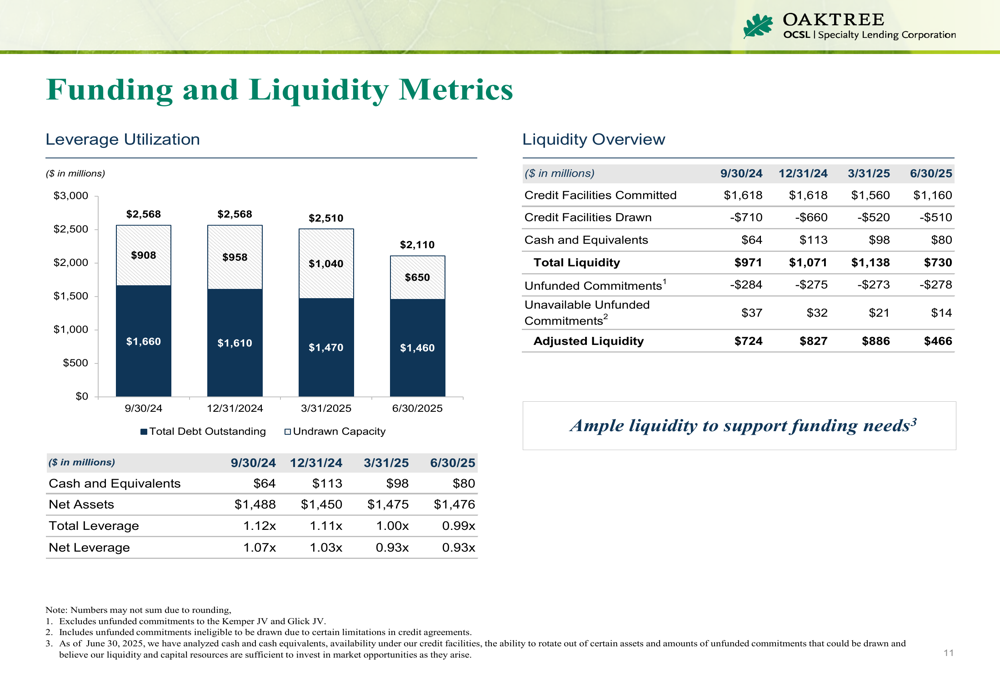

OCSL maintained a conservative leverage profile with a net debt-to-equity ratio of 0.93x, at the lower end of its target range of 0.90x to 1.25x. The company reported $730 million in available liquidity, including $80 million in cash and $650 million in undrawn capacity on its credit facilities.

During the quarter, OCSL amended its credit facility to extend maturity and reduce pricing, while terminating its Citibank facility. The company’s debt maturity profile is well-structured with no significant near-term maturities:

The company’s funding and liquidity position has evolved over recent quarters, with a strategic shift toward unsecured borrowings, which now represent 65% of total debt:

Strategic Initiatives

OCSL highlighted two significant strategic actions taken to support shareholder value. In February 2025, Oaktree purchased $100 million of newly issued OCSL shares at $17.63 per share, representing a 10% premium to NAV at the time and increasing net assets by approximately 7%.

Additionally, the company implemented an incentive fee cap with a lookback provision beginning October 1, 2024. This structure has resulted in $18.5 million in waived Part I incentive fees to date, including $5.4 million in the current quarter.

The company’s joint ventures continue to provide accretive returns, with both the Kemper (NYSE:KMPR) JV and Glick JV generating approximately 10.5% returns on OCSL’s investments:

Forward Outlook

Despite the earnings miss and revenue shortfall, OCSL’s management remains cautiously optimistic about the company’s positioning. During the earnings call, CEO Armen Panossian stated, "The long-term outlook for direct lending will remain favorable," while Co-CIO Raghav Khanna emphasized the company’s selective approach to "deploying capital into mature market-leading businesses with solid fundamentals and consistent cash flows."

The company faces several challenges, including tariff uncertainties impacting M&A activity, tightening credit spreads affecting lending margins, and competition from robust CLO issuance. Management is focusing on asset-backed and infrastructure investments to navigate these headwinds.

With its current stock price of $13.16 significantly below the NAV of $16.76 per share, OCSL trades at approximately a 21.5% discount to book value. This discount has widened following the earnings miss, potentially reflecting investor concerns about the sustainability of the current dividend level and continued pressure on net investment income.

President Matt Pendo reiterated the company’s leverage target, stating, "Our target leverage ratio remains unchanged at 0.9 times to 1.25 times, and we are currently at the low end of that range," suggesting potential capacity for additional investments should attractive opportunities arise.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.