Europe’s Stoxx 600 inches lower amid French political crisis

Introduction & Market Context

Ocean Yield reported improved financial results for the second quarter of 2025, with significant growth in both adjusted EBITDA and net profit compared to the previous quarter. The company, which specializes in vessel ownership and leasing across multiple maritime segments, continues to expand its portfolio with a strategic focus on LNG carriers while maintaining its long-term charter business model.

The Q2 2025 presentation, delivered on August 19, 2025, highlights Ocean Yield’s continued execution of its growth strategy through strategic investments and sale-leaseback transactions, despite a slight decline in available liquidity and equity ratio compared to the previous quarter.

Quarterly Performance Highlights

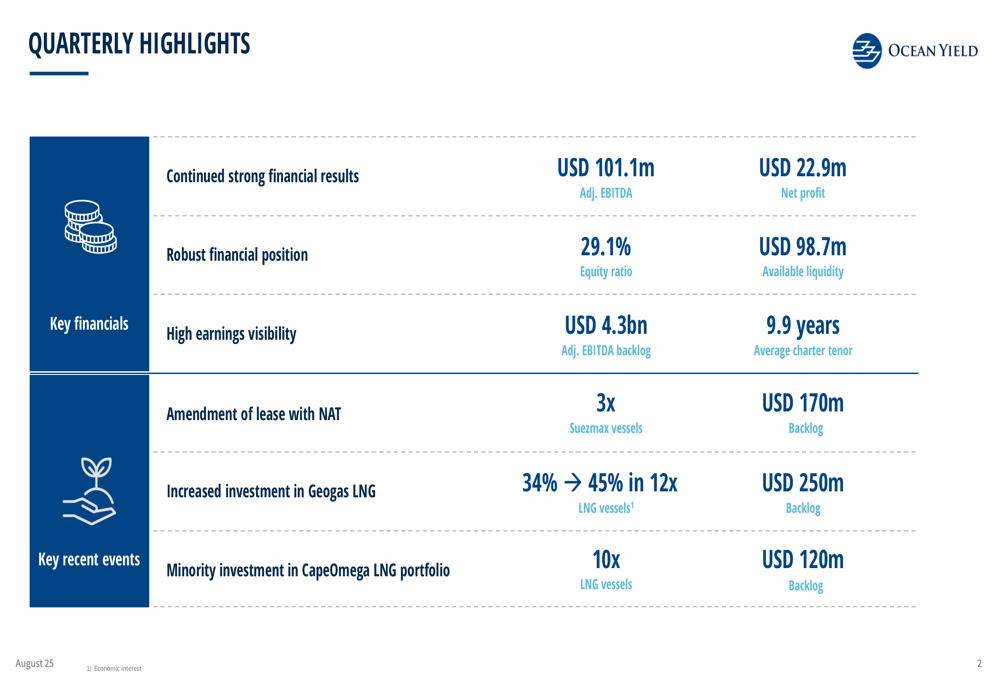

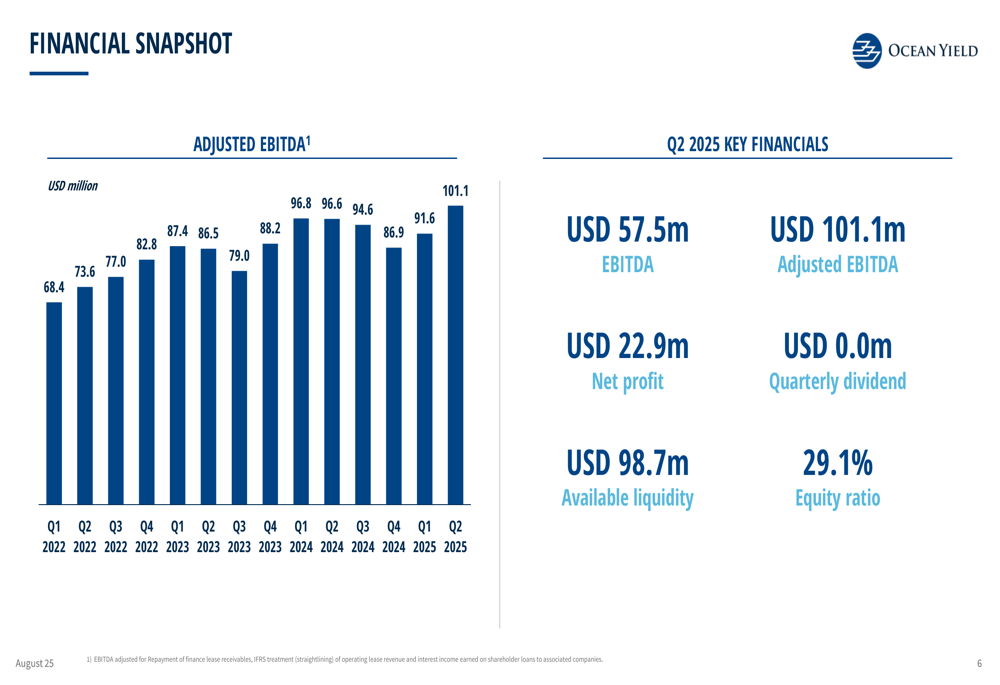

Ocean Yield reported adjusted EBITDA of USD 101.1 million for Q2 2025, representing a 10.4% increase from the USD 91.6 million reported in Q1. Net profit also improved significantly to USD 22.9 million, up from USD 18.3 million in the previous quarter. The company maintains a substantial adjusted EBITDA backlog of USD 4.3 billion, supported by an average charter tenor of 9.9 years.

As shown in the following quarterly highlights:

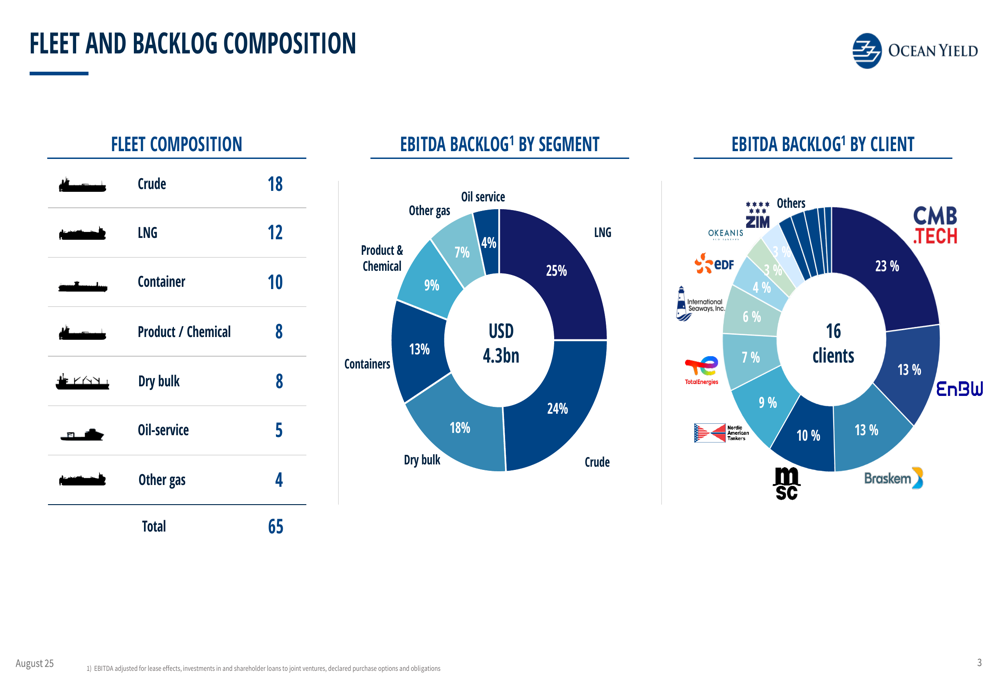

The company’s fleet now consists of 65 vessels spread across multiple segments, providing diversification while maintaining a focus on long-term contracts. The LNG segment represents the largest portion of the EBITDA backlog at 25%, followed closely by crude tankers at 24% and dry bulk vessels at 18%.

The following chart illustrates Ocean Yield’s fleet composition and EBITDA backlog distribution:

Strategic Initiatives

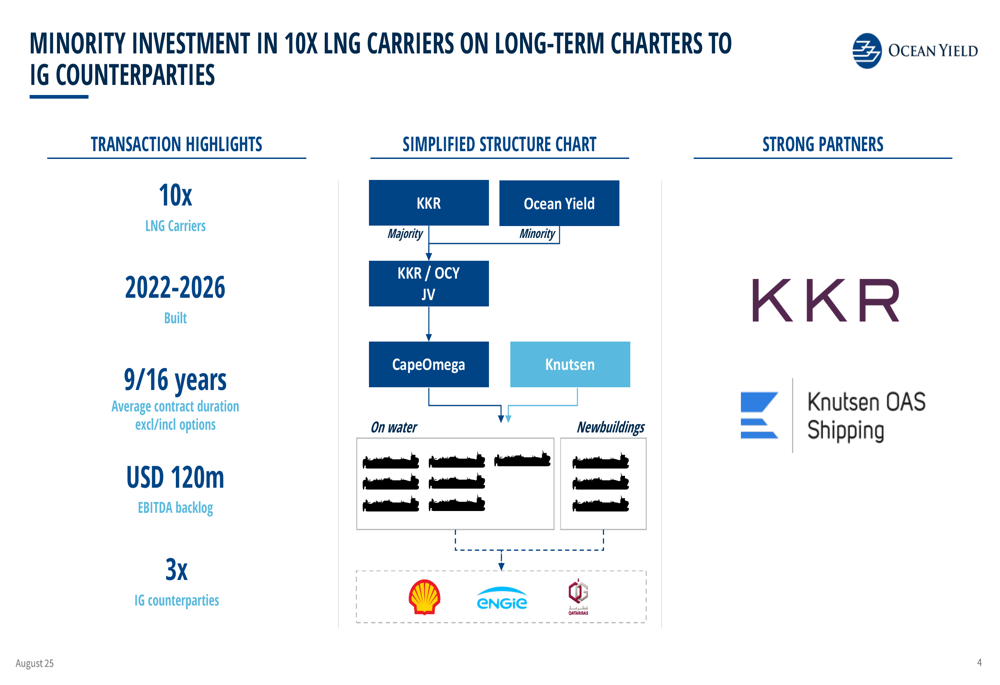

During Q2 2025, Ocean Yield continued its strategic expansion in the LNG sector with several key investments. The company increased its ownership stake in Geogas LNG from 34% to 45%, encompassing 12 LNG vessels with a backlog of USD 250 million. Additionally, Ocean Yield made a minority investment in CapeOmega’s LNG portfolio, which includes 10 LNG carriers with an EBITDA backlog of USD 120 million.

The following diagram illustrates the structure of the CapeOmega LNG investment:

The transaction involves vessels built between 2022 and 2026 with contract durations of 9 to 16 years (including options) and three investment-grade counterparties, aligning with Ocean Yield’s strategy of securing long-term, stable cash flows.

Ocean Yield also amended its lease agreement with NAT for three Suezmax vessels, adding USD 170 million to its backlog. The company continued to optimize its portfolio by exercising purchase options for six VLCCs and three LR2 product tankers, while also selling the vessel Hafnia Aronaldo.

Detailed Financial Analysis

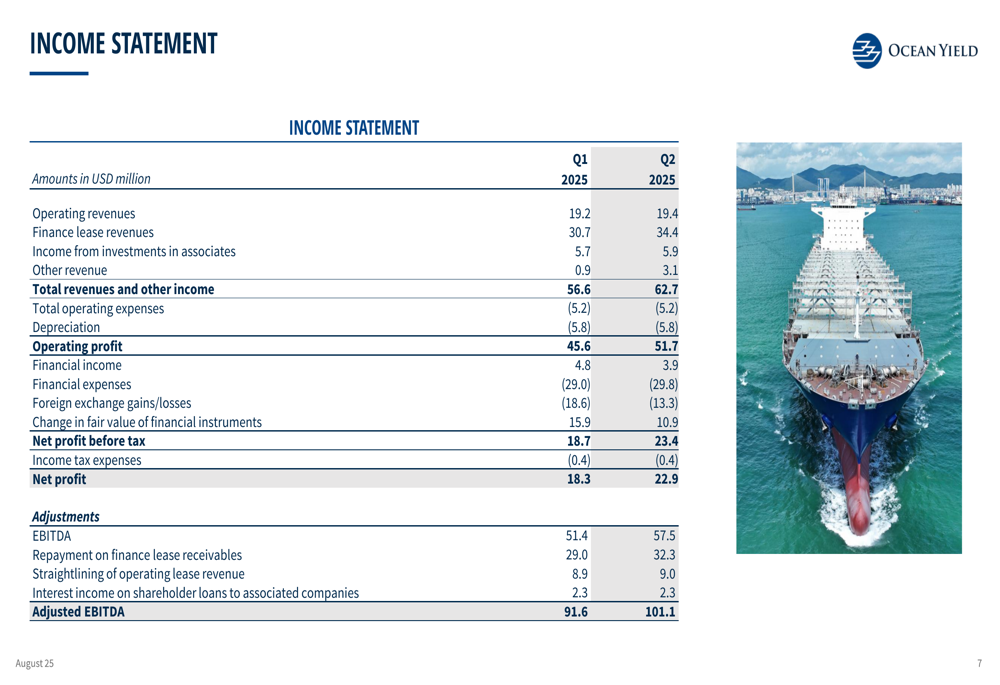

Ocean Yield’s financial performance shows positive momentum in Q2 2025, with total revenues increasing to USD 62.7 million from USD 56.6 million in Q1. This growth was primarily driven by higher finance lease revenues, which rose to USD 34.4 million from USD 30.7 million in the previous quarter.

The following chart shows the company’s adjusted EBITDA trend:

The income statement reveals operating profit of USD 51.7 million for Q2 2025, up from USD 45.6 million in Q1, reflecting improved operational efficiency:

Despite the improved earnings, Ocean Yield’s available liquidity decreased to USD 98.7 million at the end of Q2, down from USD 137 million in Q1 and significantly lower than the USD 201.1 million reported in the Q1 earnings call. This reduction in liquidity likely reflects the company’s continued investments in vessel acquisitions and stake increases. Similarly, the equity ratio declined to 29.1% from 31.7% in the previous quarter.

During the quarter, Ocean Yield secured financing for one LR1 newbuilding and three Suezmax vessels, with an additional loan agreement signed after quarter-end for another LR1 newbuilding.

Forward-Looking Statements

Ocean Yield’s outlook emphasizes three key strategic pillars: maintaining low portfolio risk with a robust balance sheet, pursuing growth through sale-leaseback transactions and strategic investments, and leveraging its strong access to capital at attractive costs to enhance its competitive position.

The company’s strategy is illustrated in the following outlook slide:

While Ocean Yield continues to focus on growth opportunities, particularly in the LNG segment, investors should note the declining liquidity position and equity ratio, which may limit future expansion capacity without additional capital raising. The company’s significant backlog of USD 4.3 billion and average charter tenor of 9.9 years provide substantial visibility for future cash flows, supporting its business model of providing long-term, predictable dividends to shareholders.

The company’s strategic investments in LNG carriers align with the global transition toward cleaner energy sources and position Ocean Yield to benefit from the growing demand for LNG transportation services in the coming years.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.