Tesla could be a $10,000 stock in a decade, says longtime bull Ron Baron

Introduction & Market Context

Omda AS (OB:OMDA) presented its second quarter 2025 financial results on August 29, 2025, showcasing continued strong performance in line with the company’s guidance. The specialized healthcare and emergency response software provider reported 16% revenue growth compared to the same period last year, maintaining the momentum seen in Q1 2025.

The company’s stock closed at 47.90 on August 28, 2025, down 3.04% ahead of the earnings presentation, but remains significantly above its 52-week low of 26.20. Year-to-date, Omda shares have shown strong performance, reflecting investor confidence in the company’s growth strategy and business model focused on recurring revenue.

Quarterly Performance Highlights

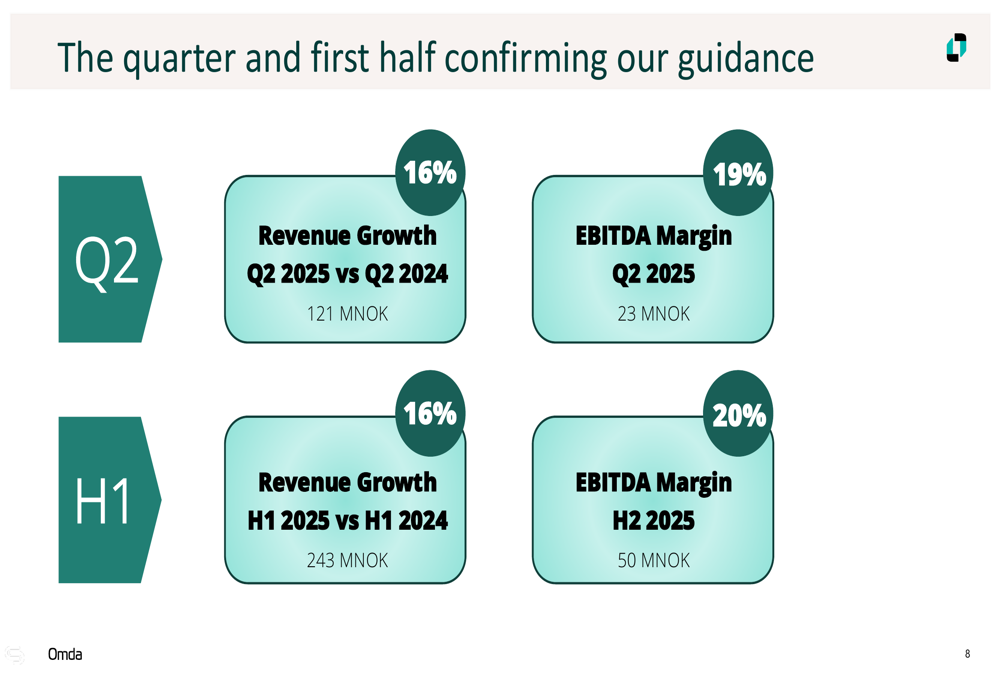

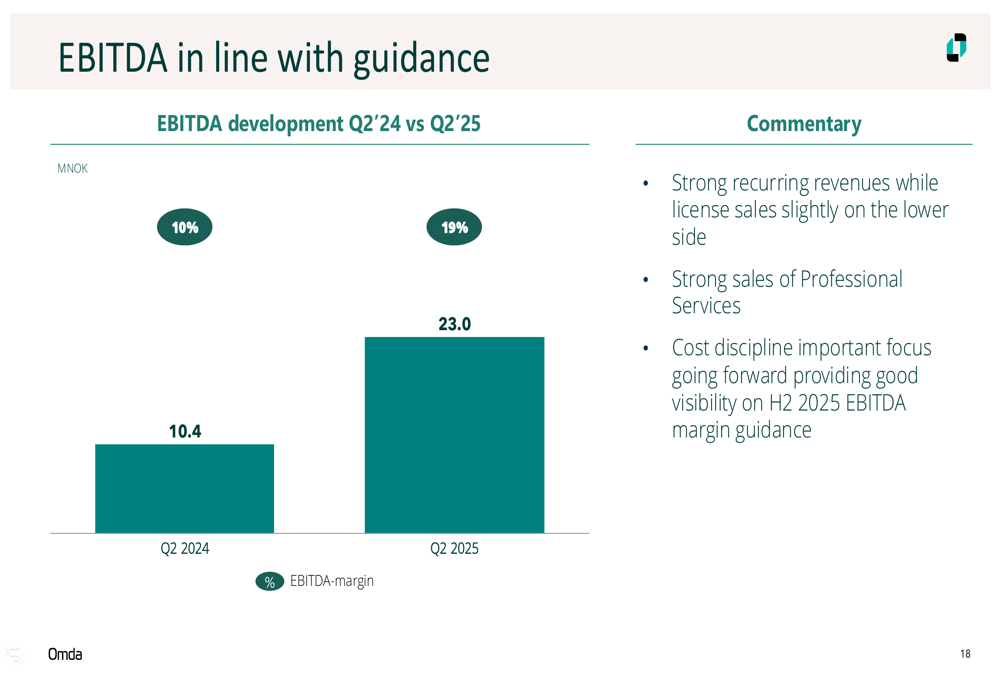

Omda reported Q2 2025 revenue of 121 MNOK, representing a 16% increase compared to Q2 2024. The company’s EBITDA reached 23 MNOK with a 19% margin, nearly doubling from the 10.4 MNOK (10% margin) recorded in the same quarter last year.

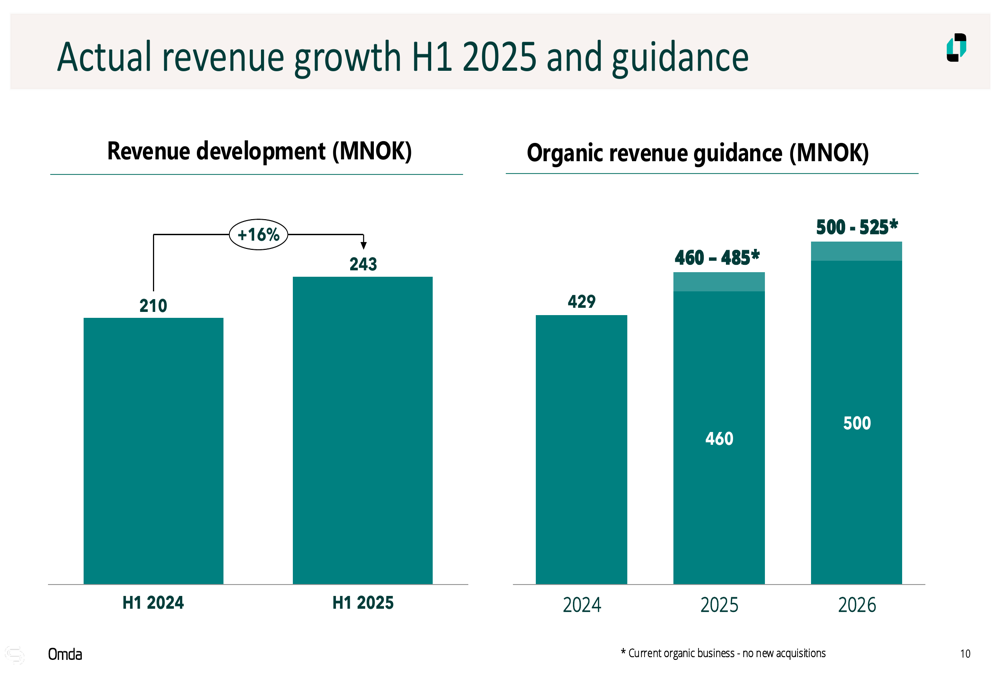

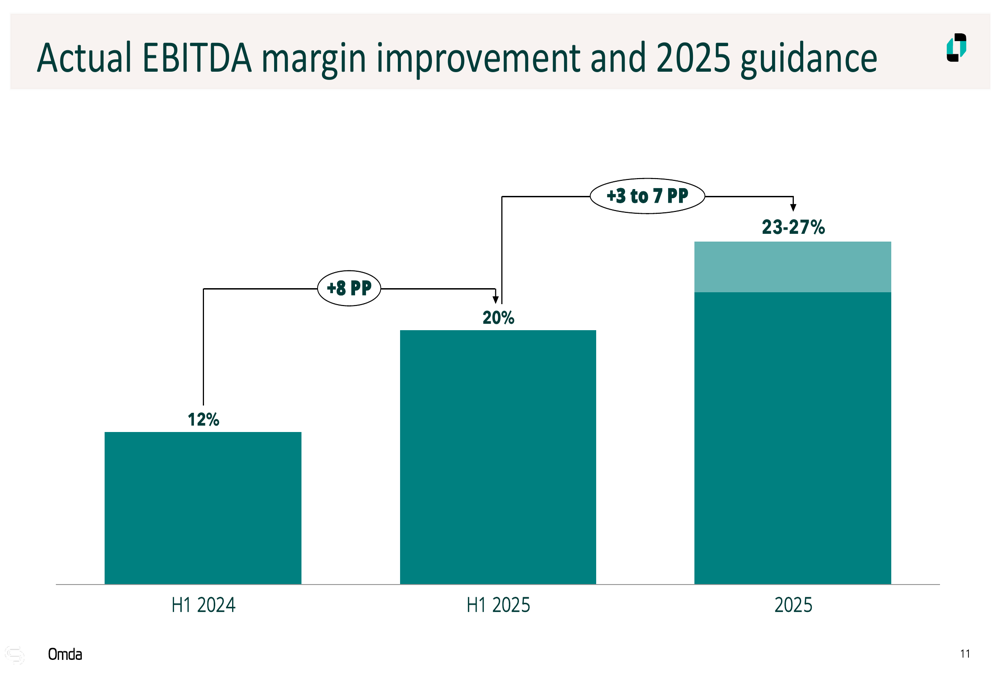

For the first half of 2025, Omda generated revenue of 243 MNOK, up 16% from H1 2024, with an EBITDA of 50 MNOK and a 20% margin, showing an 8 percentage point improvement from the 12% margin in H1 2024.

As shown in the following chart of quarterly performance metrics:

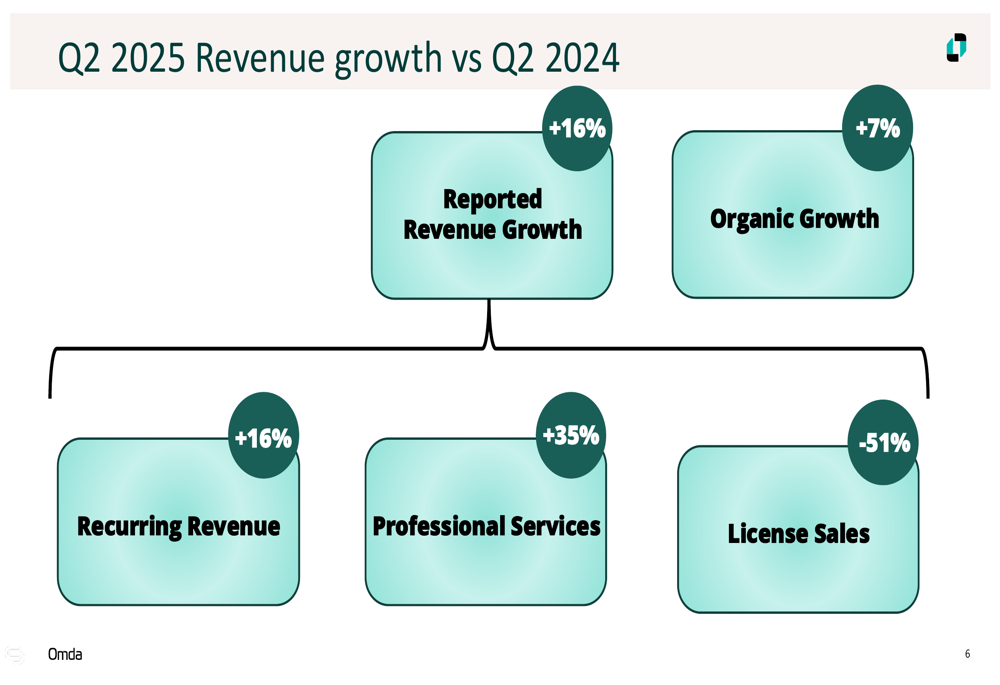

The company’s organic growth rate stood at 7% for Q2 2025, with recurring revenue growing by 16% and professional services surging by 35%. License sales, which now represent only 1% of total revenue, declined by 51% as the company continues its strategic shift toward a recurring revenue model.

As illustrated in this revenue growth breakdown:

Revenue Composition and Business Model

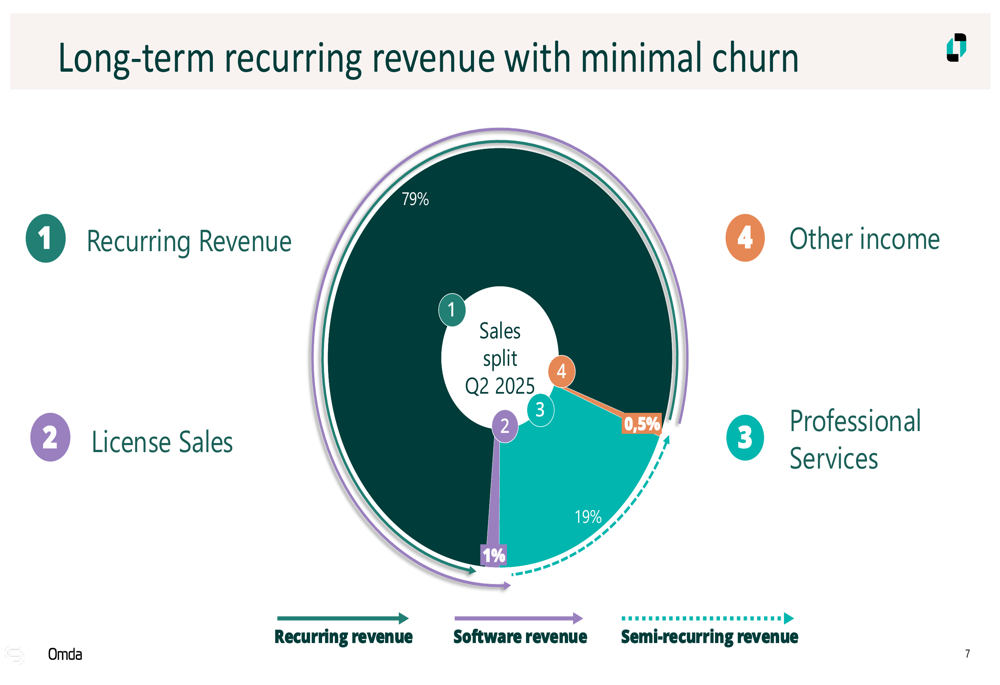

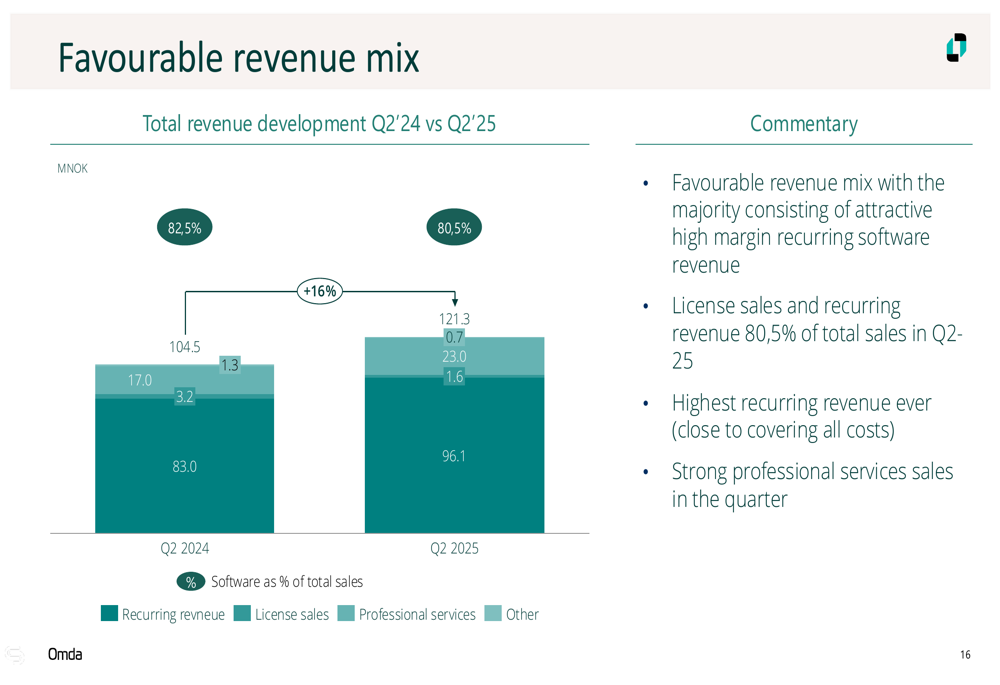

A key highlight of Omda’s Q2 2025 results is the continued strengthening of its recurring revenue base, which now accounts for 79% of total revenue. Professional services contribute 19%, while license sales have diminished to just 1% of revenue, reflecting the company’s successful transition to a subscription-based model.

The company’s revenue composition is visualized in the following chart:

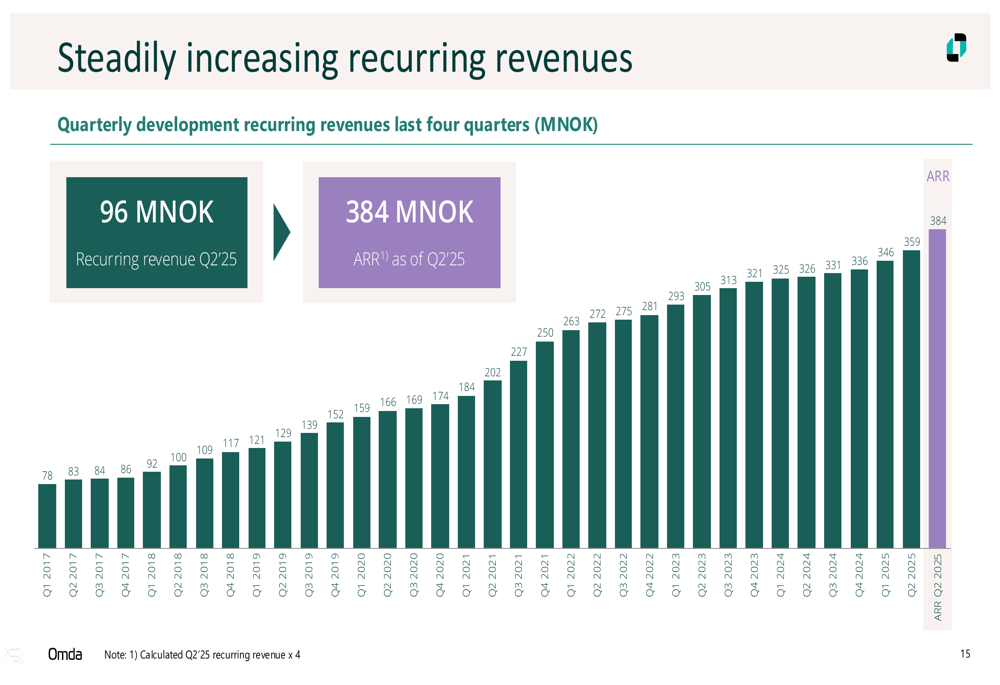

Omda’s recurring revenue reached 96.1 MNOK in Q2 2025, up from 83.0 MNOK in Q2 2024. The Annual Recurring Revenue (ARR) has grown to 384 MNOK as of Q2 2025, compared to 305 MNOK in Q1 2024, demonstrating the company’s ability to consistently expand its recurring revenue base.

The quarterly development of recurring revenues shows a steady upward trajectory:

A comparison of revenue mix between Q2 2024 and Q2 2025 further illustrates the company’s evolving business model:

Geographic and Business Area Diversification

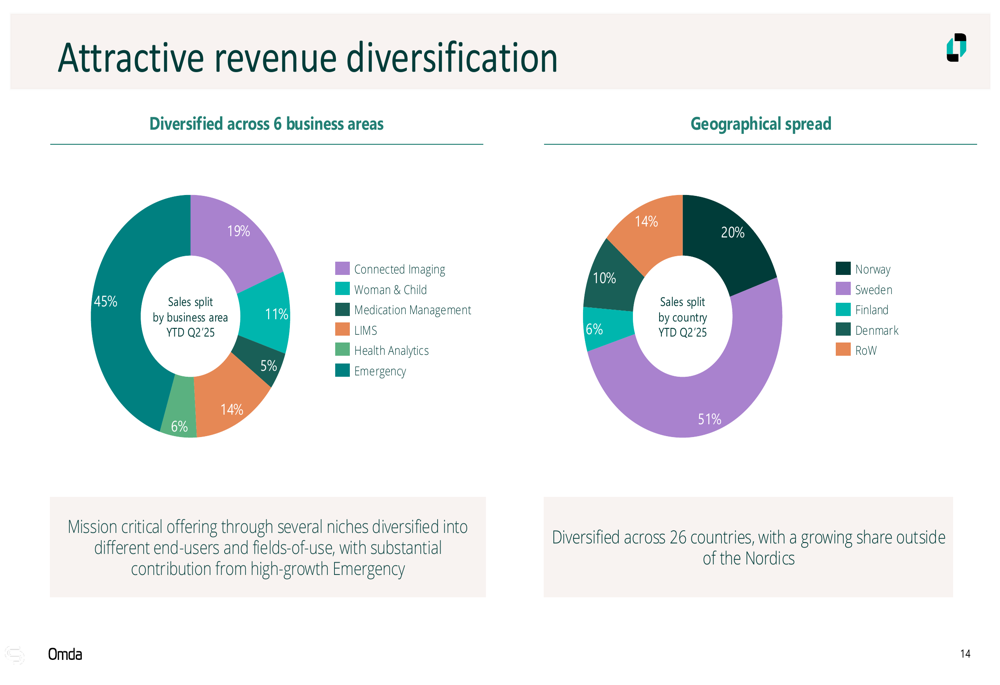

Omda’s revenue is well-diversified across both business areas and geographic regions. Connected Imaging represents the largest segment at 45% of revenue, followed by Woman & Child (19%), Health Analytics (14%), Medication Management (11%), Emergency (6%), and LIMS (5%).

Geographically, the company generates 51% of its revenue outside the Nordic region (categorized as Rest of World), with Sweden accounting for 20%, Norway 14%, Finland 10%, and Denmark 6%. This diversification helps mitigate regional market risks and provides multiple growth avenues.

The company’s revenue diversification is illustrated in these charts:

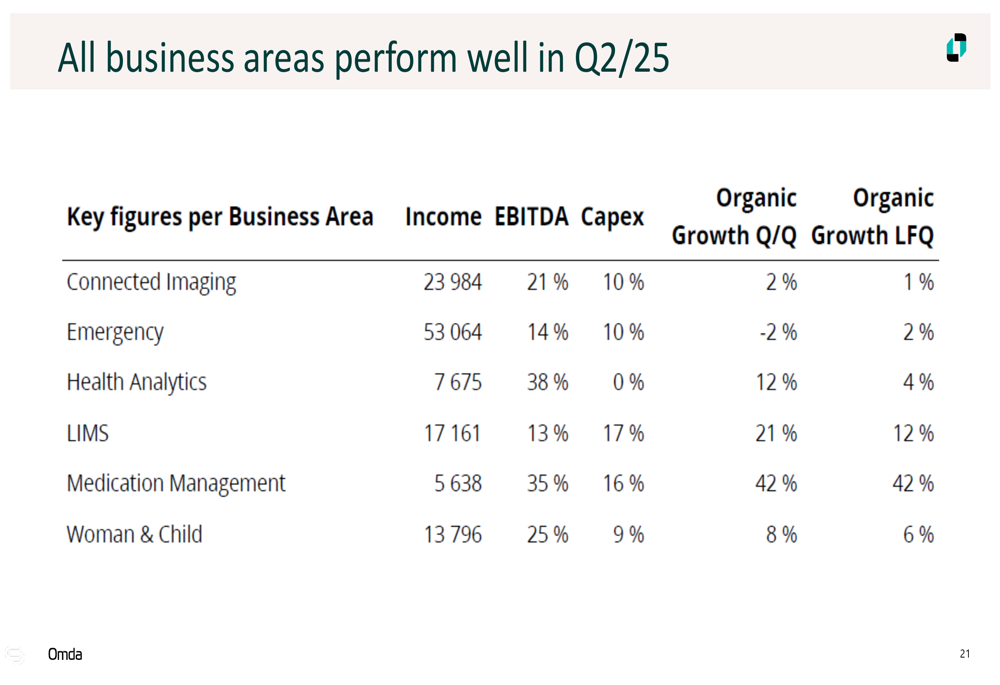

Omda operates in six specialized software niches within healthcare and emergency response, each addressing critical needs in their respective domains. All business areas performed well in Q2 2025, with varying growth rates and profitability levels.

The detailed performance breakdown by business area is shown in this comprehensive table:

Margin Improvement and Cost Management

Omda has made significant progress in improving its EBITDA margin, which reached 19% in Q2 2025, up from 10% in Q2 2024. This improvement reflects the company’s focus on operational efficiency and the increasing share of high-margin recurring revenue.

The EBITDA development is visualized in the following chart:

The company has maintained disciplined cost management, with a total cost base of 293 MNOK in Q2 2025. Personnel costs represent the largest component, followed by other costs and cost of goods sold (COGS). The cost structure appears well-optimized to support Omda’s growth ambitions while improving profitability.

Capital expenditure (Capex) for Q2 2025 was 13.3 MNOK, slightly lower than the 13.8 MNOK in Q2 2024. The company’s target is to maintain Capex at approximately 10% of revenue, balancing investments in growth with financial discipline.

Net Working Capital (NWC) has shown encouraging development, trending at -23% in Q2 2025, an improvement from the -26% low recorded in Q2 2023. This indicates efficient working capital management and strong cash conversion capabilities.

Forward-Looking Statements and Guidance

Omda confirmed its guidance for 2025 and 2026, projecting organic revenue of 460-485 MNOK for 2025 and 500-525 MNOK for 2026, based on the current organic business without new acquisitions. This represents continued growth from the 429 MNOK recorded in 2024.

The company’s revenue guidance is illustrated in this chart:

For 2025, Omda targets an EBITDA margin of 23-27%, an improvement of 3-7 percentage points from the 20% achieved in H1 2025. The long-term ambition is to reach an EBITDA margin of approximately 30%, driven by economies of scale and increasing recurring revenue share.

The EBITDA margin guidance is visualized here:

Omda’s growth strategy combines organic expansion (target:5-10% growth) with strategic acquisitions (target:10-20% growth). The company follows a disciplined approach to M&A, focusing on acquisitions that meet predefined criteria centered around customer relationships, code quality, and team competence.

In summary, Omda’s Q2 2025 results demonstrate continued strong performance with 16% revenue growth, significant margin improvement, and a successful shift toward a recurring revenue model. The company’s diversified business portfolio, geographic reach, and balanced growth strategy position it well for sustainable growth in the specialized healthcare and emergency response software markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.