Raymond James raises Fulgent Genetics stock price target to $36 on strong performance

Introduction & Market Context

Omnicell Inc (NASDAQ:OMCL), a leader in medication management technology, presented its Q3 2025 investor slides on October 30, 2025, revealing financial results that significantly exceeded market expectations. The company reported a 10% year-over-year revenue increase to $311 million, driving its stock up 14.78% in pre-market trading to $33.94.

The healthcare technology provider has positioned itself as a trusted partner for healthcare systems seeking to implement what it calls the "Autonomous Pharmacy" - a vision for replacing manual, error-prone medication management activities with automated processes. With an installed base that includes more than half of the top 300 U.S. health systems, Omnicell is leveraging its established market presence to accelerate its transition toward recurring revenue streams.

Quarterly Performance Highlights

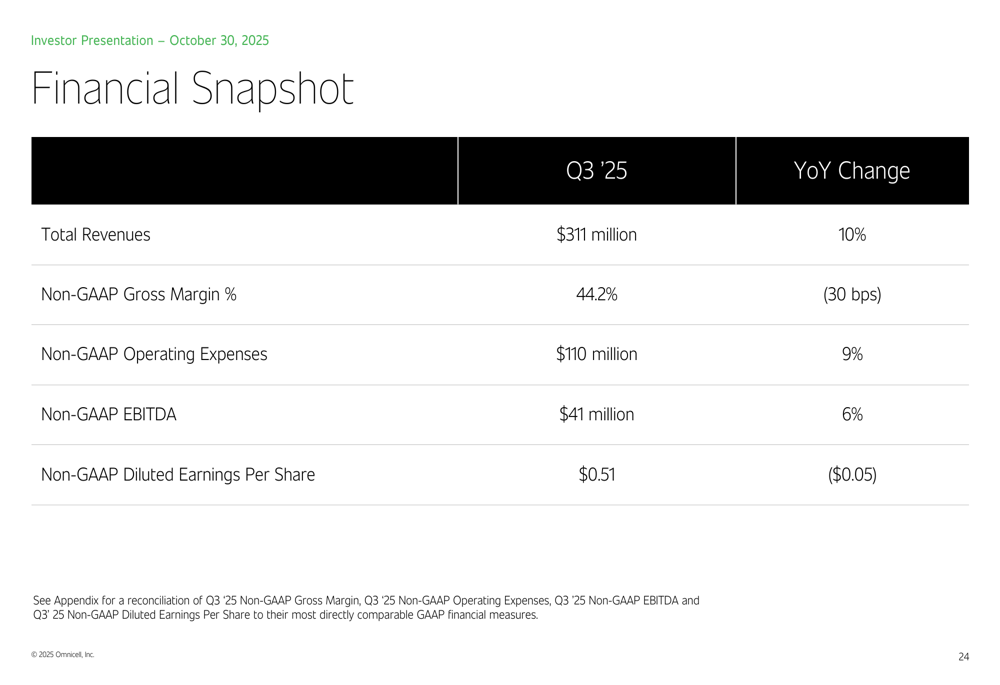

Omnicell’s Q3 2025 financial results demonstrated solid growth across key metrics. The company reported total revenues of $311 million, representing a 10% increase year-over-year. Non-GAAP EBITDA grew to $41 million, up 6% compared to the same period in 2024, while Non-GAAP earnings per share came in at $0.51, slightly down from $0.56 in the prior year.

As shown in the following financial snapshot from the presentation:

The Q3 results significantly exceeded analyst expectations, with actual EPS of $0.51 surpassing forecasts by 41.67% and revenue beating projections by 5.08%. This performance triggered the substantial pre-market stock price increase, reflecting renewed investor confidence in Omnicell’s business model and growth strategy.

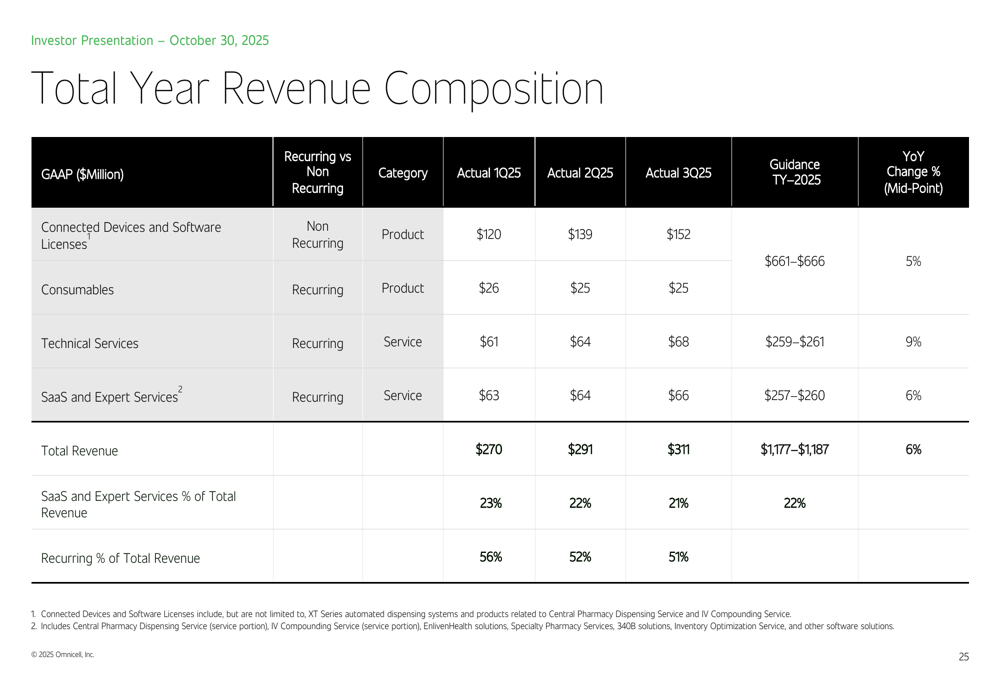

The company’s revenue composition shows a strategic shift toward recurring revenue streams, particularly in SaaS and Expert Services:

Strategic Initiatives

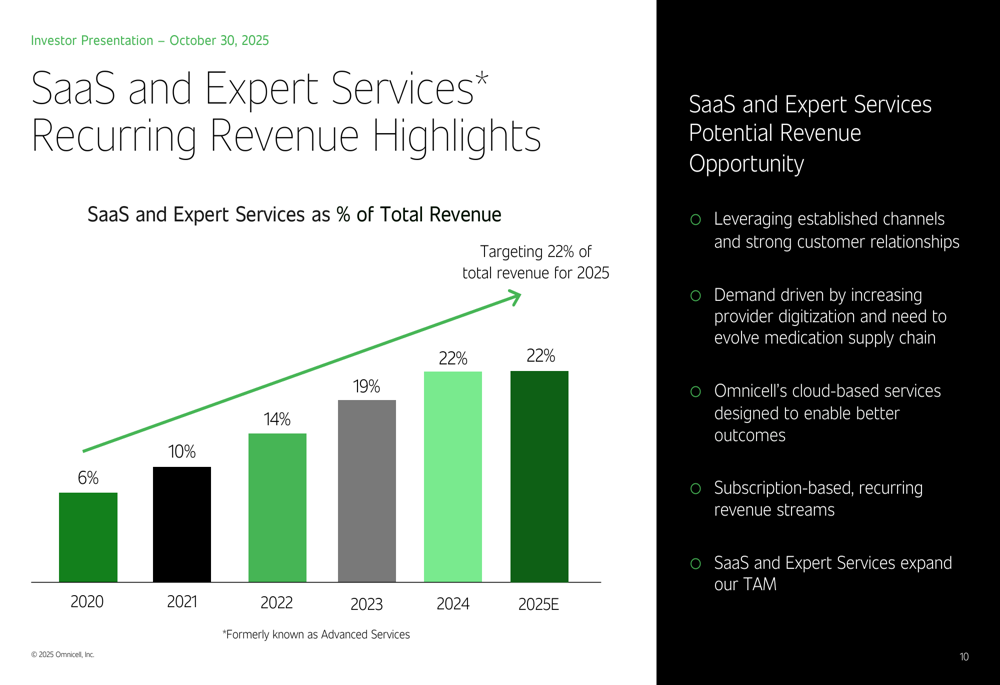

Omnicell’s investor presentation highlighted several key strategic initiatives designed to drive long-term growth. Central to this strategy is the company’s focus on expanding its SaaS and Expert Services offerings, which are projected to reach 22% of total revenue by 2025, up significantly from just 6% in 2020.

The following chart illustrates this strategic shift toward recurring revenue:

CEO Randall Lipps emphasized the company’s transformation into an intelligent medication management technology leader during the earnings call, stating, "We believe our transformation into an intelligence medication management technology company is progressing well."

The company’s growth strategy centers around three key principles: connecting health networks, disrupting pharmacy care with innovation, and growing where care is being delivered. This approach spans multiple healthcare settings, including central pharmacy, IV rooms, points of care, specialty pharmacy, and ambulatory care.

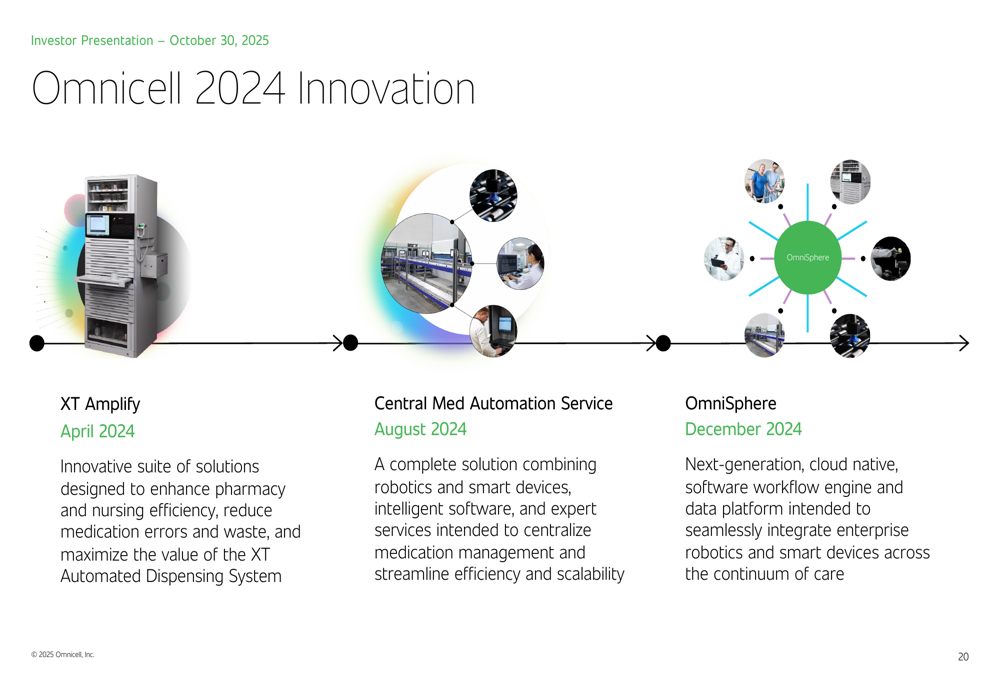

Omnicell’s 2024 innovation roadmap features three major product launches that are expected to strengthen its market position:

The OmniSphere platform, scheduled for release in December 2024, represents a particularly significant advancement. This cloud-native platform is designed to unify all Omnicell products under a single secure infrastructure, providing seamless integration across the medication management ecosystem:

Forward-Looking Statements

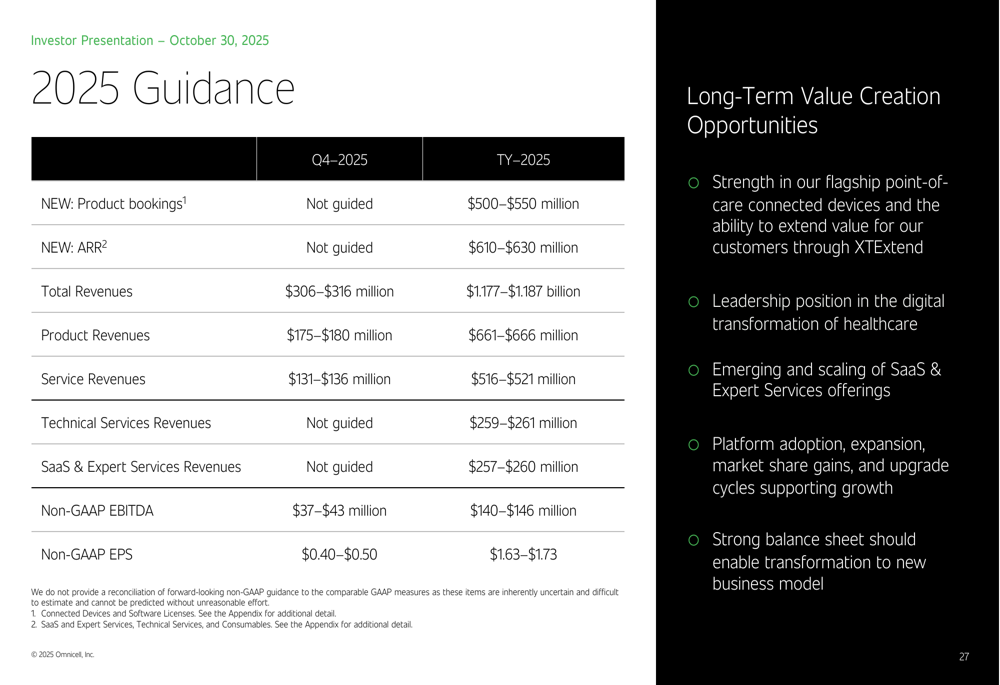

Omnicell provided detailed guidance for Q4 and full-year 2025, projecting continued growth across its business segments:

For Q4 2025, the company expects revenue between $306-316 million, with full-year 2025 revenue projected at $1.177-1.187 billion. Omnicell anticipates product bookings of $500-550 million and expects its Annual Recurring Revenue (ARR) to reach $610-630 million by year-end.

The company highlighted several long-term value creation opportunities, including:

- Strength in flagship point-of-care connected devices

- Leadership position in healthcare digital transformation

- Scaling of SaaS and Expert Services offerings

- Platform adoption and market share gains

- A strong balance sheet enabling business model transformation

While the outlook is generally positive, Omnicell acknowledged some challenges, including potential tariff impacts that it hopes to reduce in 2026. The company also completed a $75 million stock repurchase program, which reduced outstanding shares by approximately 5%.

Analyst Perspectives

During the earnings call Q&A session, analysts focused on Omnicell’s strategies for integrating robotics and AI, the positive outlook on the market refresh cycle, and the ongoing development of the OmniSphere platform. The company also addressed its approach to navigating the 340B market dynamics.

Investment highlights from the presentation underscore why Omnicell believes it is well-positioned for future success:

Despite the overall positive results, some analysts noted potential risks, including economic uncertainties that could influence strategic investments, intense competition in the healthcare technology sector, and possible market saturation in certain product lines.

The slight year-over-year decline in non-GAAP EPS also raised questions, though this was overshadowed by the significant earnings beat relative to analyst expectations. Omnicell’s management attributed this to ongoing investments in innovation and the transition toward a more subscription-based business model, which they believe will drive higher long-term value.

As Omnicell continues its transformation toward becoming a comprehensive medication management technology provider with a growing recurring revenue base, investors appear increasingly confident in the company’s strategic direction, as evidenced by the strong market reaction to its Q3 2025 results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.