Procore signs multi-year strategic collaboration agreement with AWS

Introduction & Market Context

Ooma Inc (NYSE:OOMA) presented its Q1 fiscal year 2026 investor presentation on May 28, 2025, highlighting the company’s continued growth in the cloud communications sector. The presentation follows Ooma’s strong Q4 FY2025 performance, where the company reported earnings per share of $0.21, exceeding analyst expectations of $0.14 and driving a 5.24% after-hours stock price increase.

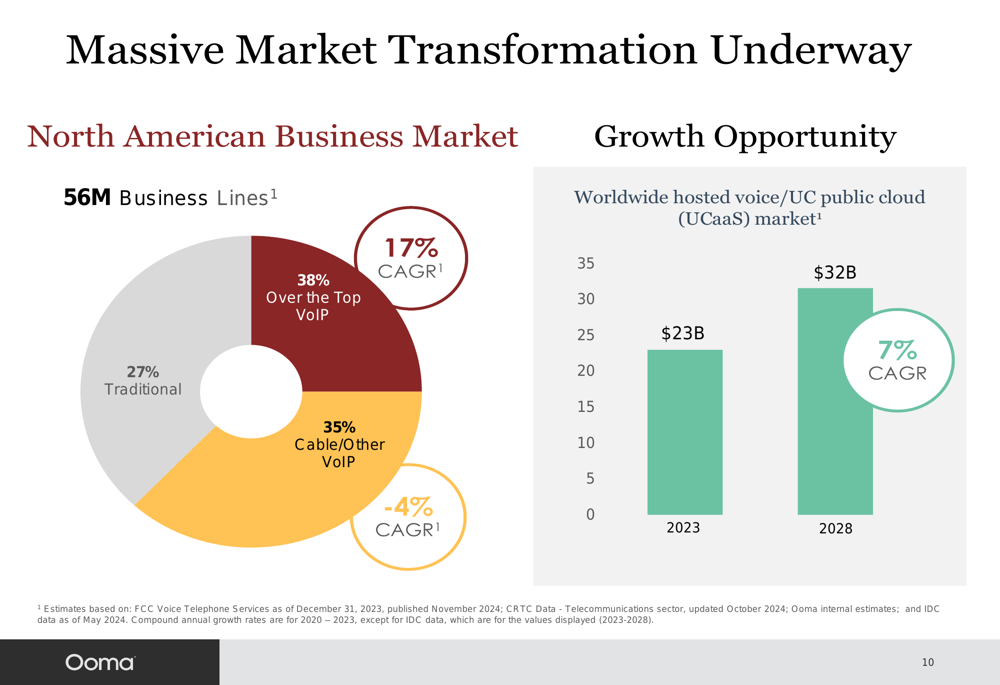

Ooma positions itself as a provider of "Smart Connected Services," transforming sophisticated technology into elegant, simple communications solutions. With over 1.2 million core users and operations in 32 countries, the company continues to capitalize on the ongoing transformation in the North American business communications market, where Over-the-Top VoIP solutions are growing at a 17% CAGR.

Quarterly Performance Highlights

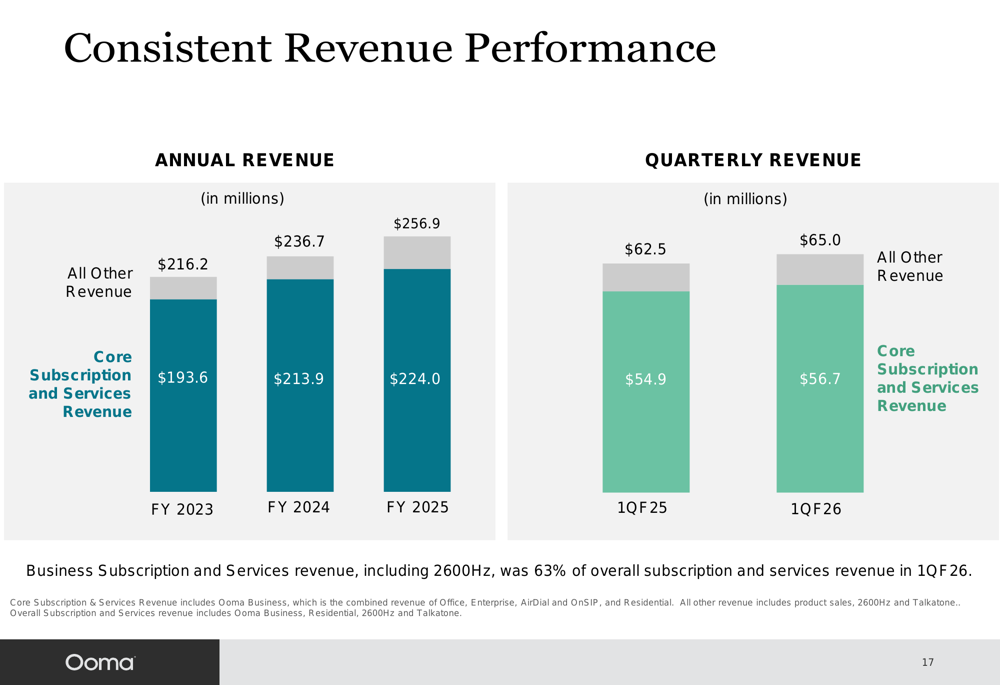

Ooma reported Q1 FY2026 revenue of $65.0 million, consistent with the $65.1 million reported in their recent earnings announcement. The company’s business segment continues to be the primary growth driver, with business subscription and services revenue representing 63% of overall subscription revenue in Q1 FY2026.

As shown in the following chart of quarterly revenue performance, Ooma has maintained consistent growth:

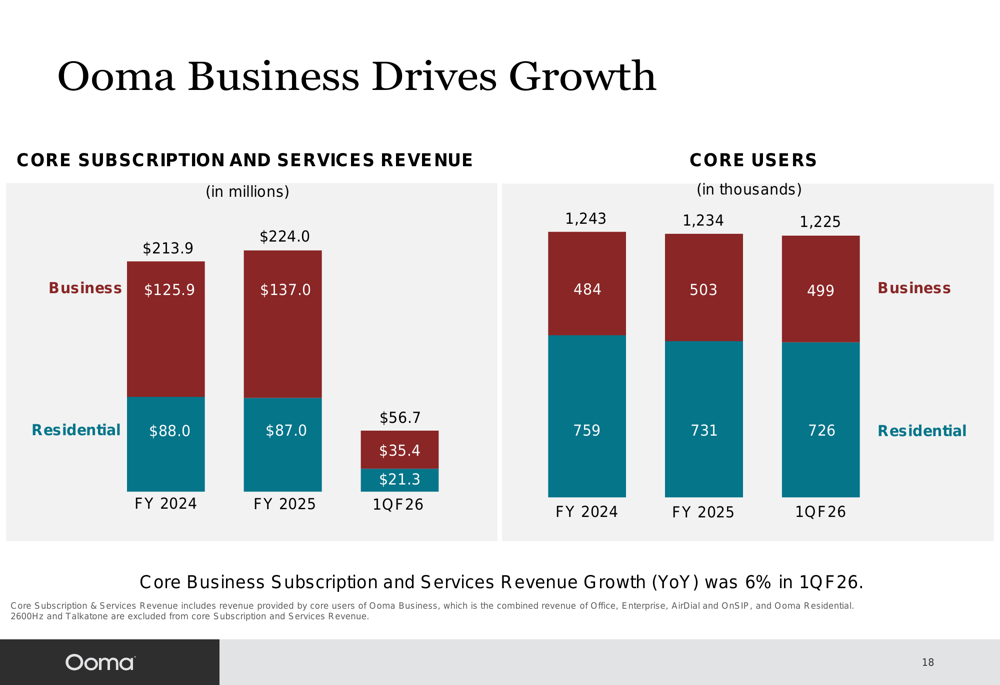

Core business subscription and services revenue grew 6% year-over-year in Q1 FY2026, reaching $35.4 million. Meanwhile, residential revenue continued its gradual decline to $21.3 million, reflecting the company’s strategic shift toward business customers.

The following chart illustrates how the business segment is increasingly driving Ooma’s growth:

Detailed Financial Analysis

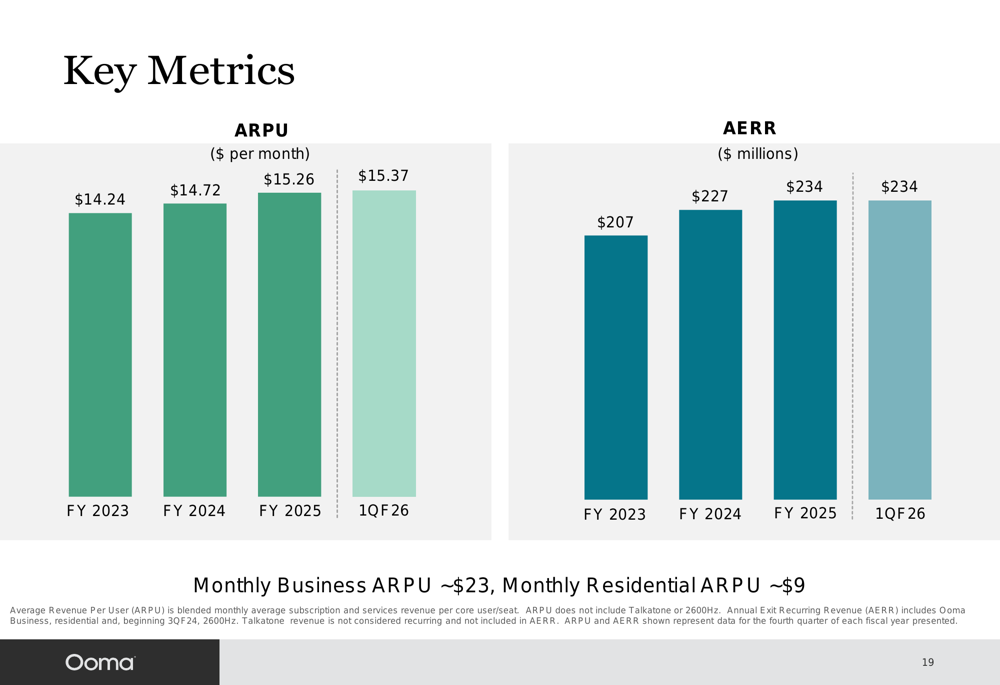

Ooma’s Average Revenue Per User (ARPU) has shown steady improvement, reaching $15.37 per month in Q1 FY2026, up from $15.26 in FY2025. Business ARPU is significantly higher at approximately $23 per month, compared to residential ARPU of around $9, explaining the company’s strategic focus on business customers.

The company’s Annual Exit Recurring Revenue (AERR) has stabilized at $234 million, as shown in this chart:

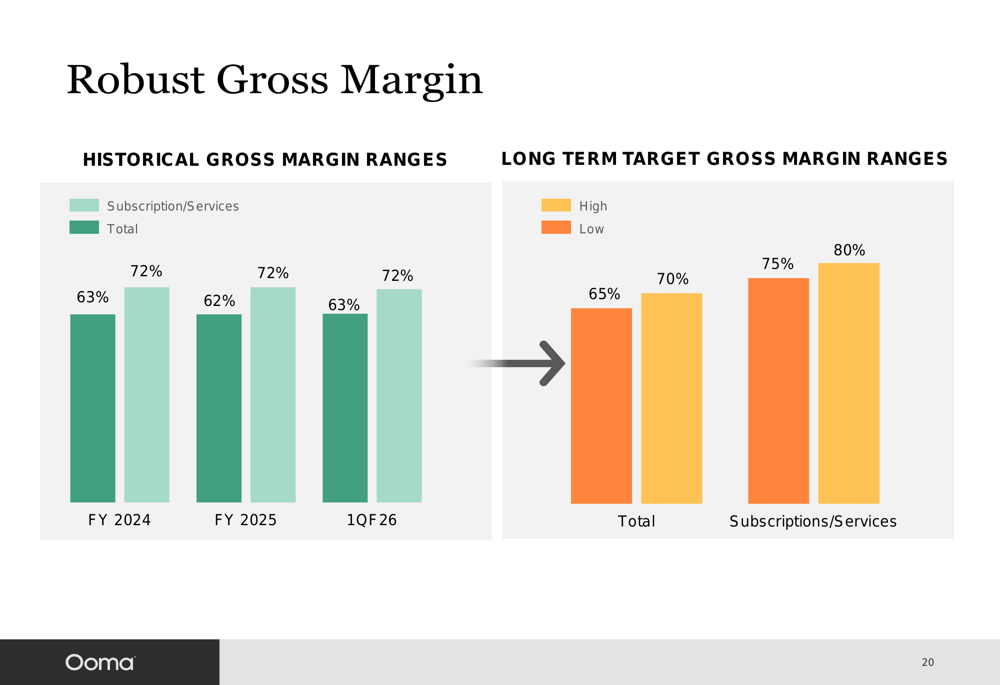

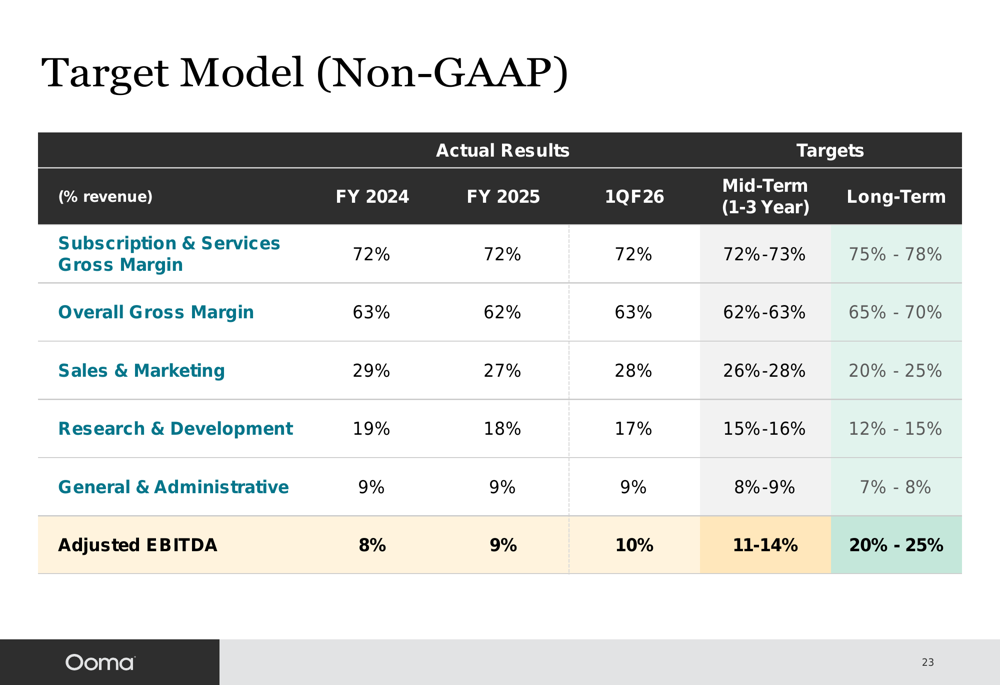

Gross margins have remained robust at 72% for subscription and services revenue, with total gross margin at 63% for Q1 FY2026. This aligns with the company’s mid-term targets and shows consistency with previous quarters.

The following chart shows Ooma’s gross margin performance and targets:

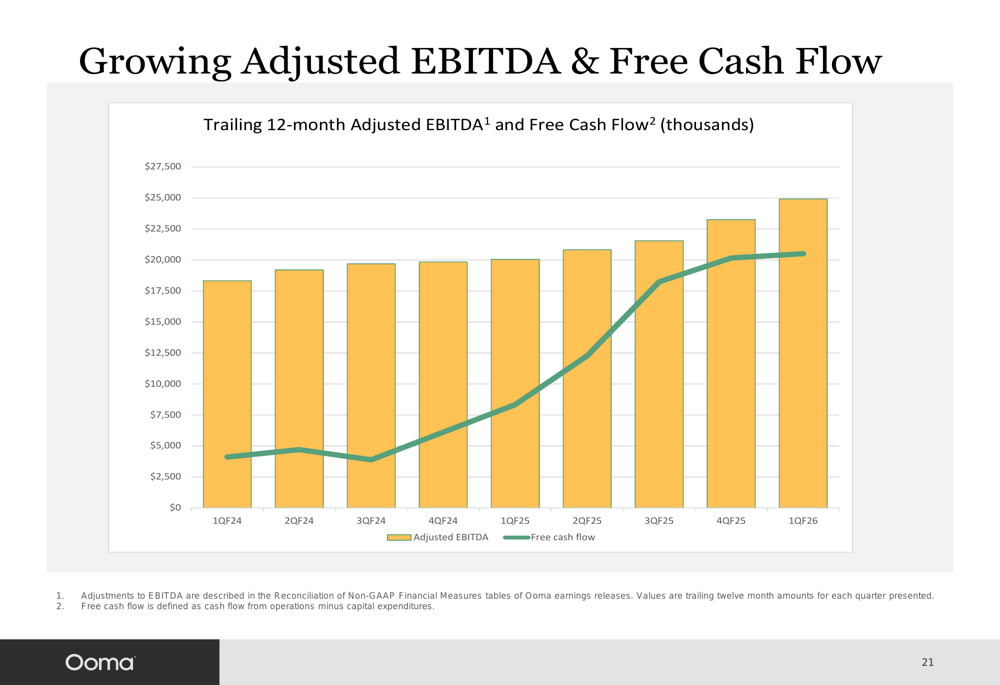

Profitability continues to improve, with Adjusted EBITDA and Free Cash Flow showing steady growth. The company has also strengthened its financial position by eliminating debt while increasing its cash reserves to $19.0 million in Q1 FY2026, up from $17.9 million at the end of FY2025.

The following chart demonstrates Ooma’s improving profitability metrics:

Strategic Initiatives

Ooma’s growth strategy focuses on three main product lines: Ooma Telo for residential customers, Ooma Office for small and medium businesses, and Ooma Enterprise for large businesses. The company is expanding into two significant new markets: POTS (Plain Old Telephone Service) replacement with its AirDial solution and wholesale solutions through its 2600Hz platform.

The POTS replacement market represents a substantial opportunity as traditional copper lines are being phased out, with over 10 million lines in the U.S. market. Ooma’s AirDial solution addresses critical infrastructure needs for elevators, fire alarms, security systems, and other essential services that traditionally relied on copper lines.

The market transformation underway presents significant growth opportunities for Ooma, as illustrated in this chart:

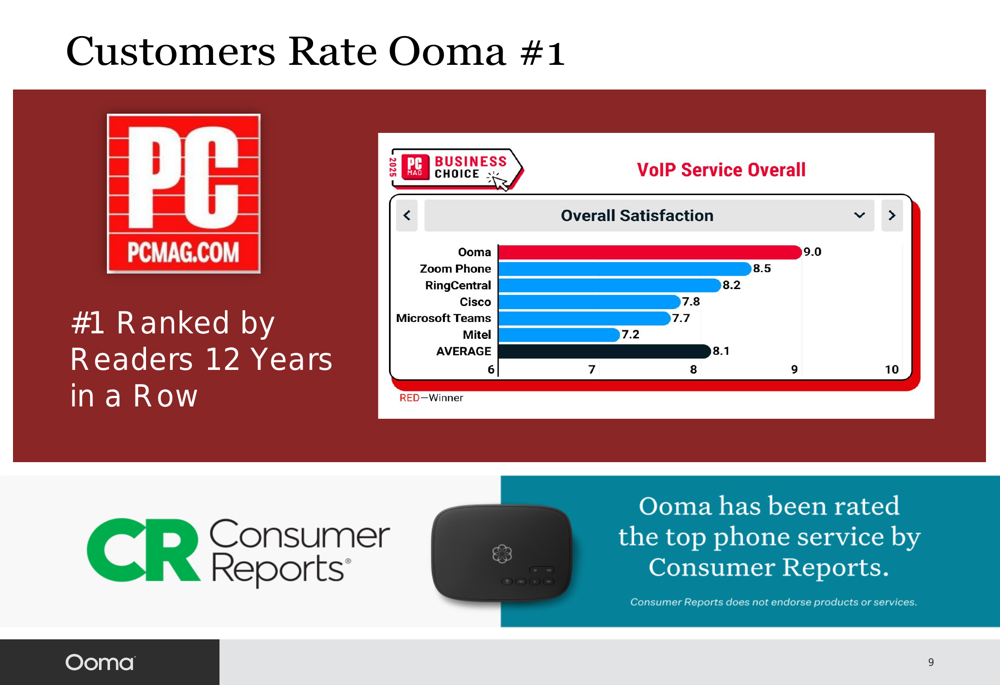

Ooma’s customer satisfaction is reflected in its industry recognition, including being ranked #1 by PCMag.com readers for 12 consecutive years and receiving top ratings from Consumer Reports:

Competitive Industry Position

Ooma maintains a strong competitive position with a comprehensive platform that drives customer satisfaction through dependable voice quality, ease of use, tailored solutions, and enhanced reliability. The company’s 99% retention rate underscores its strong value proposition in a competitive market.

The company’s integrated growth strategy includes multiple channels: advertising, customer referrals (with a Net Promoter Score of 73%), geographic expansion, direct sales, resellers and partners (including T-Mobile and U.S. Cellular), and retailers (Walmart (NYSE:WMT), Costco (NASDAQ:COST), Best Buy (NYSE:BBY), and Amazon (NASDAQ:AMZN)).

Ooma’s platform is designed to address untapped opportunities in the market, including small businesses with underserved needs, large businesses with custom requirements, businesses affected by the copper line sunset, telecom resellers modernizing their platforms, and geographic expansion.

Forward-Looking Statements

Ooma has outlined ambitious long-term financial targets, including improving subscription and services gross margins to 75-78% (from the current 72%) and overall gross margins to 65-70% (from the current 63%). The company aims to achieve Adjusted EBITDA margins of 20-25% in the long term, compared to the current 10%.

The following table details Ooma’s target financial model:

These targets align with the guidance provided in Ooma’s recent earnings report, which projected FY2026 revenue between $267 million and $270 million, with business subscription revenue growth of 5-6%. The company anticipates a non-GAAP net income of $22-$23.5 million and an adjusted EBITDA of $27.5-$29 million for the fiscal year.

As the cloud communications market continues to evolve, with the worldwide hosted voice/UC public cloud market projected to grow from $23 billion in 2023 to $32 billion by 2028 (7% CAGR), Ooma appears well-positioned to capitalize on this transformation with its diversified product portfolio and strategic focus on high-growth segments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.