Can anything shut down the Gold rally?

Introduction & Market Context

Open Lending Corporation (NASDAQ:LPRO) released its second-quarter 2025 earnings presentation on August 6, revealing continued financial pressure as the company repositions its business toward what it describes as higher-quality lending partnerships. The auto loan facilitation platform reported declines in both revenue and profitability metrics compared to the same period last year, even as it maintained relatively stable loan volumes.

The company’s stock closed at $2.14 on the day of the announcement, up slightly by 0.94%, but remains significantly below its 52-week high of $6.92. This follows a substantial stock surge after Q1 results, when shares jumped nearly 14% despite similar profitability challenges.

Quarterly Performance Highlights

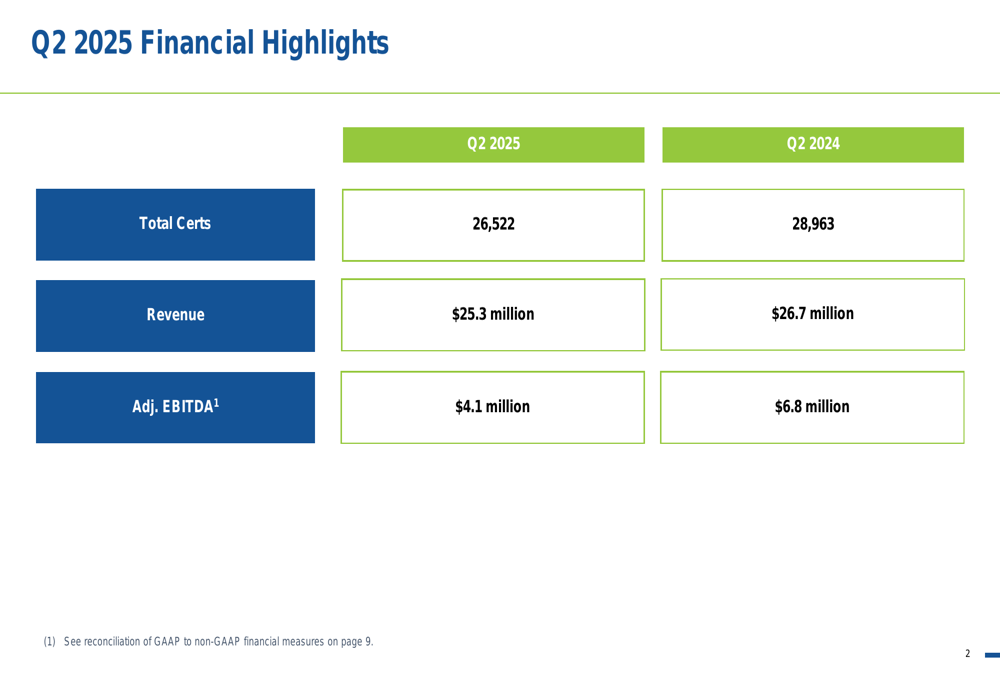

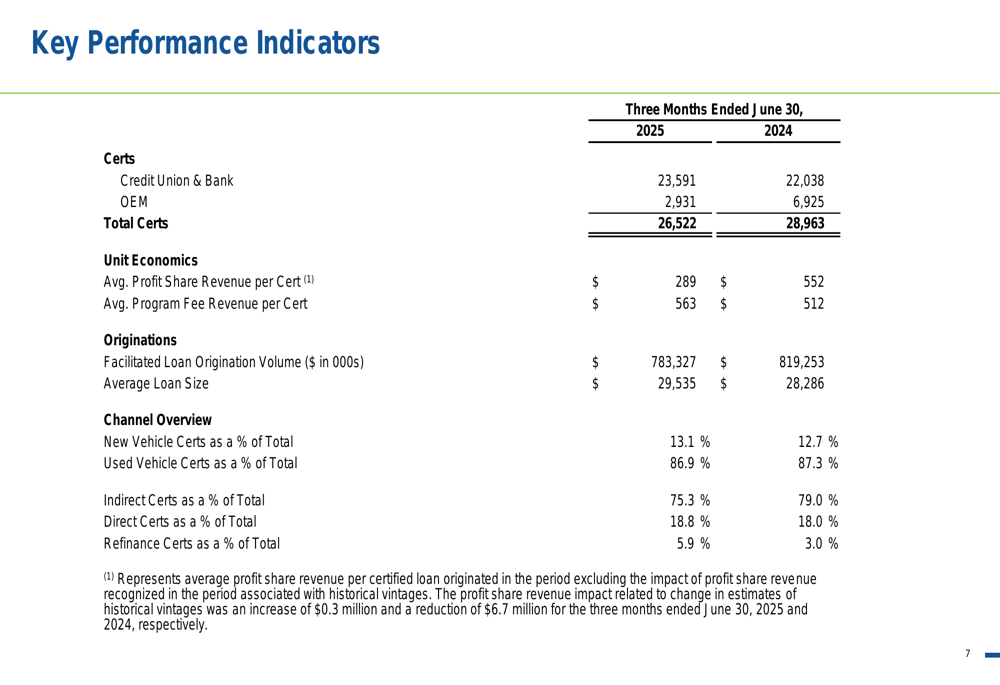

Open Lending reported total certified loans of 26,522 for Q2 2025, representing an 8.4% decrease from 28,963 in Q2 2024. This decline contributed to a revenue drop of 5.3%, with total revenue falling to $25.3 million from $26.7 million in the prior-year period.

As shown in the following financial highlights chart:

The company’s adjusted EBITDA showed a more pronounced decline, falling to $4.1 million in Q2 2025 from $6.8 million in Q2 2024, representing a 39.7% decrease. This resulted in an adjusted EBITDA margin of 16%, down from 25% in the same quarter last year.

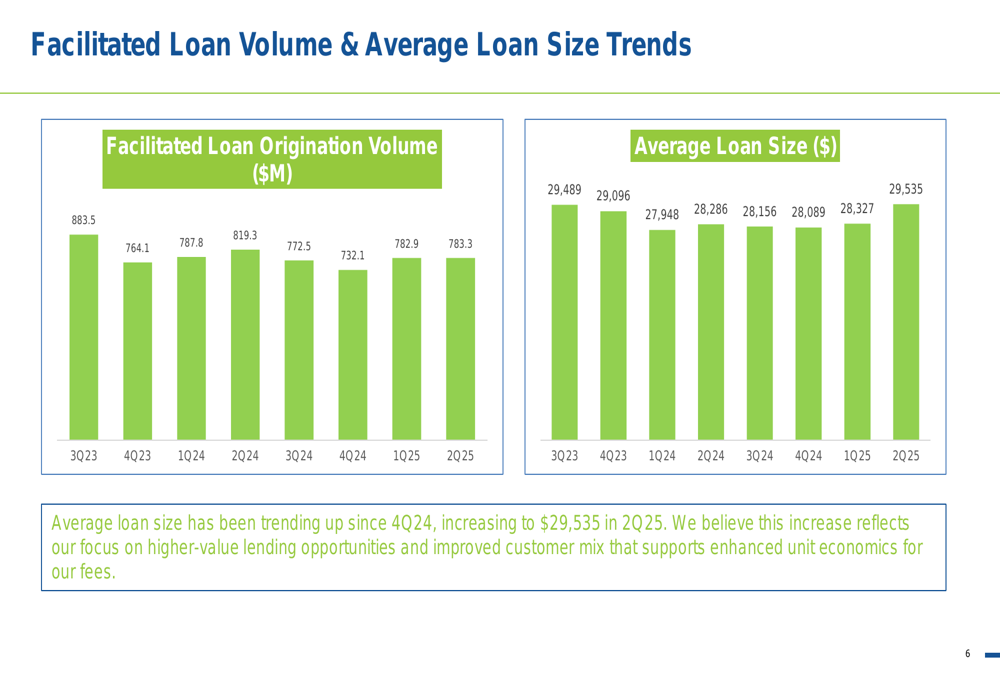

Despite the overall decrease in certified loans, the company’s facilitated loan origination volume remained relatively stable at $783.3 million, compared to $819.3 million in Q2 2024. This stability was supported by an increase in average loan size to $29,535, up from $28,286 in the prior-year period.

The following chart illustrates the facilitated loan volume and average loan size trends over recent quarters:

Detailed Financial Analysis

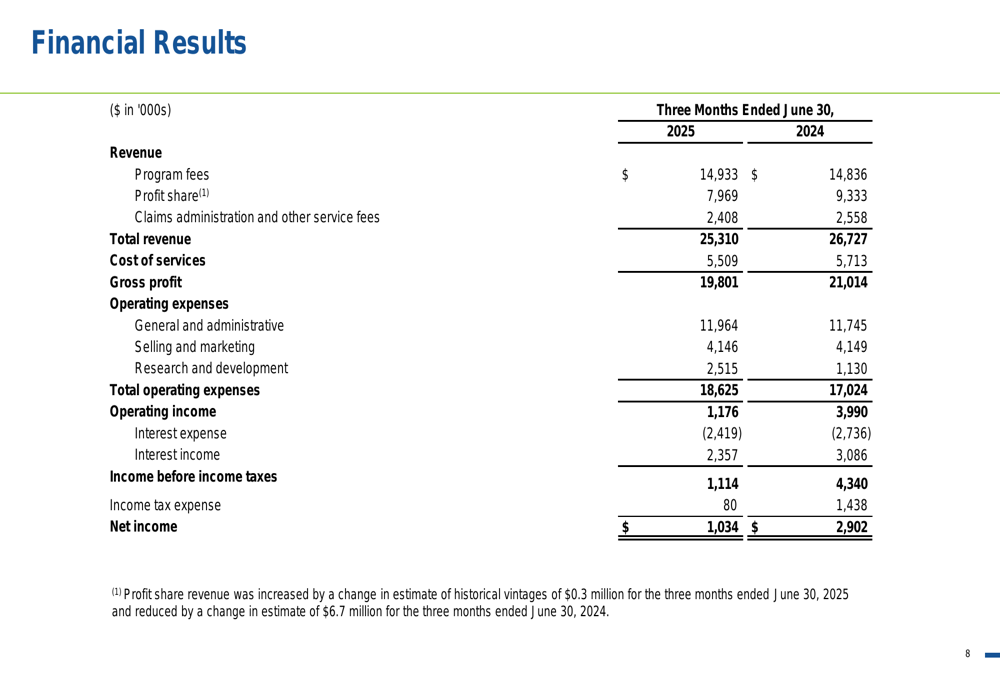

A closer examination of Open Lending’s financial results reveals shifting revenue dynamics. While program fee revenue increased slightly to $14.9 million from $14.8 million in Q2 2024, profit share revenue declined significantly to $8.0 million from $9.3 million. This represents a continuation of the trend observed in Q1 2025, when the company reported similar pressure on profit share revenue.

The comprehensive financial results are presented in the following table:

Net income for the quarter was $1.0 million, down 64.4% from $2.9 million in Q2 2024. This decline was partially offset by lower income tax expenses, which fell to $80,000 from $1.4 million in the prior-year period. Operating expenses increased to $18.6 million from $17.0 million, contributing to the significant drop in operating income from $4.0 million to $1.2 million.

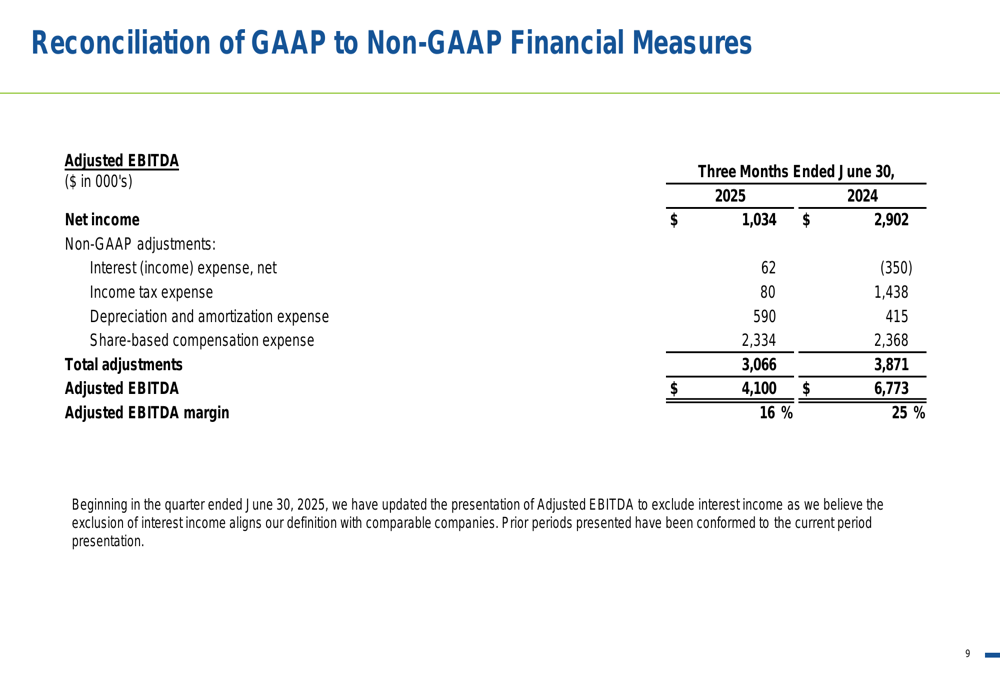

The reconciliation of GAAP to non-GAAP financial measures provides additional insight into the company’s performance:

Strategic Channel Shifts

Open Lending’s presentation emphasized its strategic pivot toward higher-quality credit union and bank partnerships, which now represent a larger portion of its business. Credit union and bank certifications increased to 23,591 in Q2 2025 from 22,038 in Q2 2024, while OEM certifications declined sharply to 2,931 from 6,925.

The following key performance indicators highlight these channel shifts:

The loan origination mix by segment shows a notable increase in refinance activity, which grew to 5.9% of total certifications compared to 3.0% in Q2 2024. This aligns with the company’s commentary about refinance volumes recovering as interest rates decline. Meanwhile, the used vehicle segment continues to dominate at 86.9% of total certifications.

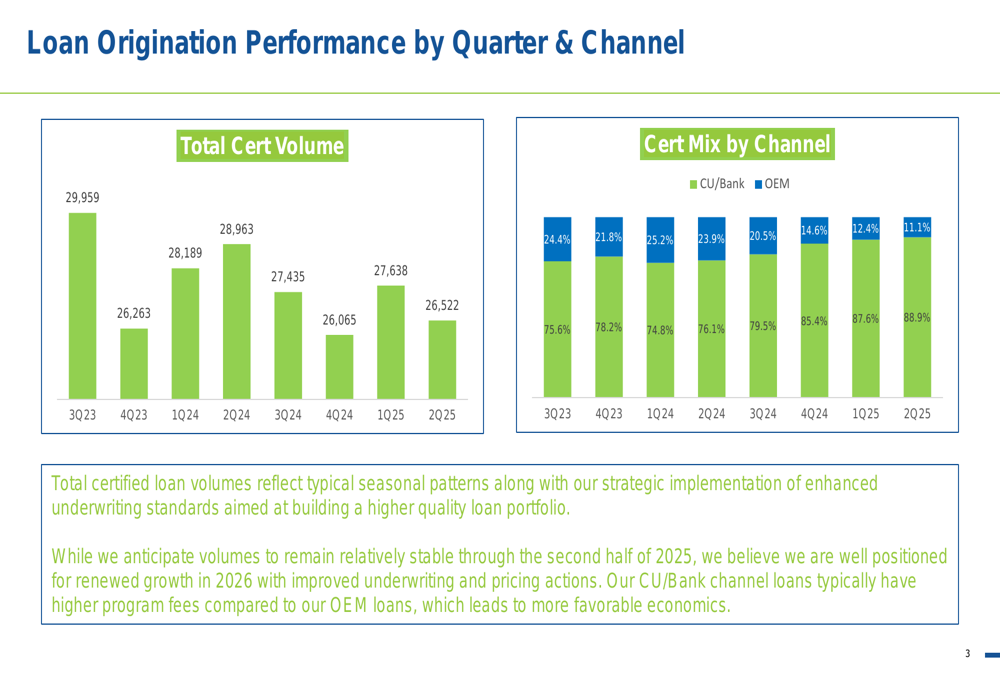

The quarterly loan origination performance by channel illustrates these trends:

Forward-Looking Statements

Open Lending’s presentation suggests that loan volumes reflect typical seasonal patterns and the strategic implementation of enhanced underwriting standards. The company anticipates stable volumes for the second half of 2025 and projects renewed growth in 2026, though these forecasts come amid several quarters of declining metrics.

The presentation also notes potential impacts from changing tariffs on the mix between used and new vehicles, with the company positioned to benefit from its strong focus on the used vehicle market. Additionally, Open Lending highlighted its focus on higher-value lending opportunities and an improved customer mix as factors contributing to the recent increase in average loan size.

These forward-looking statements align with CEO Jessica Buss’s comments from the Q1 earnings call, where she emphasized the company’s focus on operational excellence and becoming "a stronger, leaner, more agile organization." The Q2 presentation continues this narrative of strategic repositioning, though investors may question whether the current financial pressures represent temporary growing pains or more persistent challenges in the company’s business model.

As Open Lending navigates this transition period, the market will be watching closely for signs that its strategic shift toward higher-quality partnerships can eventually translate into improved financial performance and sustainable growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.