Stock market today: S&P 500 climbs as health care, tech gain; Nvidia earnings loom

Introduction & Market Context

Orange Polska (WSE:OPL) reported solid second-quarter 2025 results on July 29, showing continued momentum in its core telecom business despite headwinds in equipment sales. The company’s strategic focus on expanding its fiber and 5G infrastructure continues to yield positive results, with strong customer additions across all major segments.

The Polish telecom operator delivered 1.1% year-over-year revenue growth in Q2, slightly decelerating from the 2% growth seen in Q1 2025, but maintained strong profitability with EBITDAaL (EBITDA after Leases) rising 4.3% compared to the same period last year.

Quarterly Performance Highlights

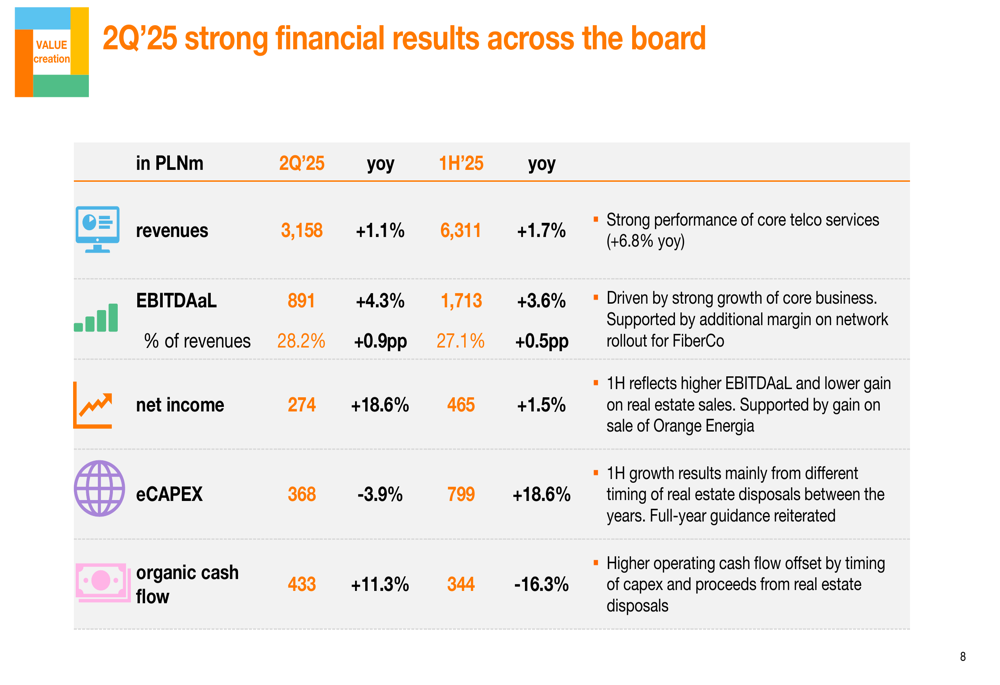

Orange Polska reported revenue of PLN 3,158 million in Q2 2025, up 1.1% year-over-year, driven by a robust 6.8% growth in core telecom services. This strong performance in the company’s main business line helped offset an 8% decline in equipment sales, which management attributed to longer handset replacement cycles by customers.

As shown in the following financial results overview:

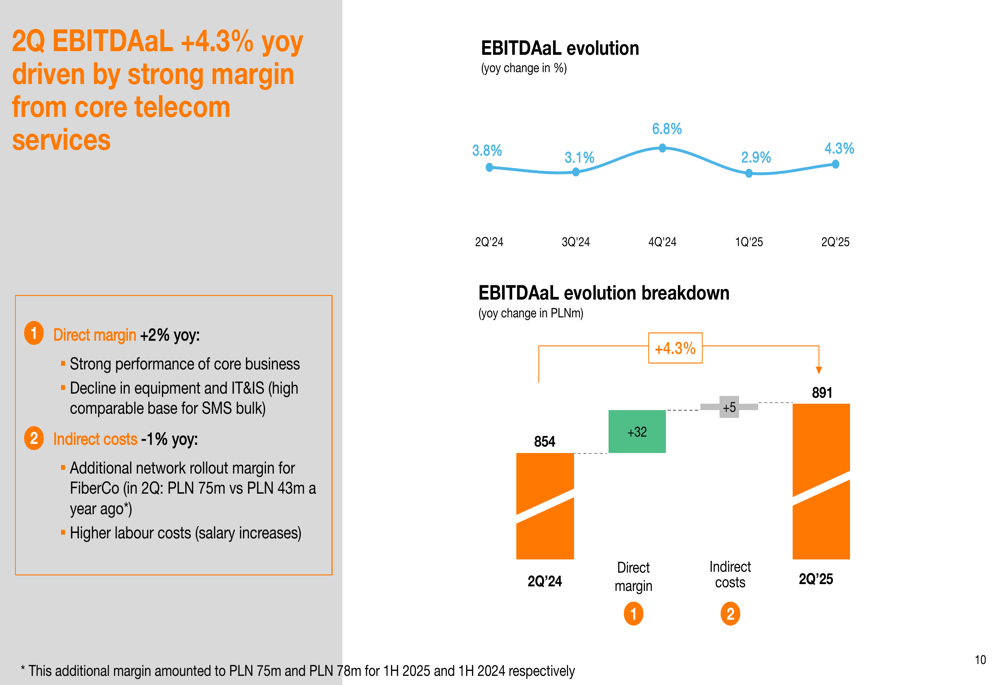

EBITDAaL reached PLN 891 million, representing a 4.3% year-over-year increase and an improved margin of 28.2% (+0.9 percentage points). This profitability enhancement reflects the company’s successful value strategy and operational efficiency. Net income showed particularly impressive growth, jumping 18.6% to PLN 274 million compared to Q2 2024.

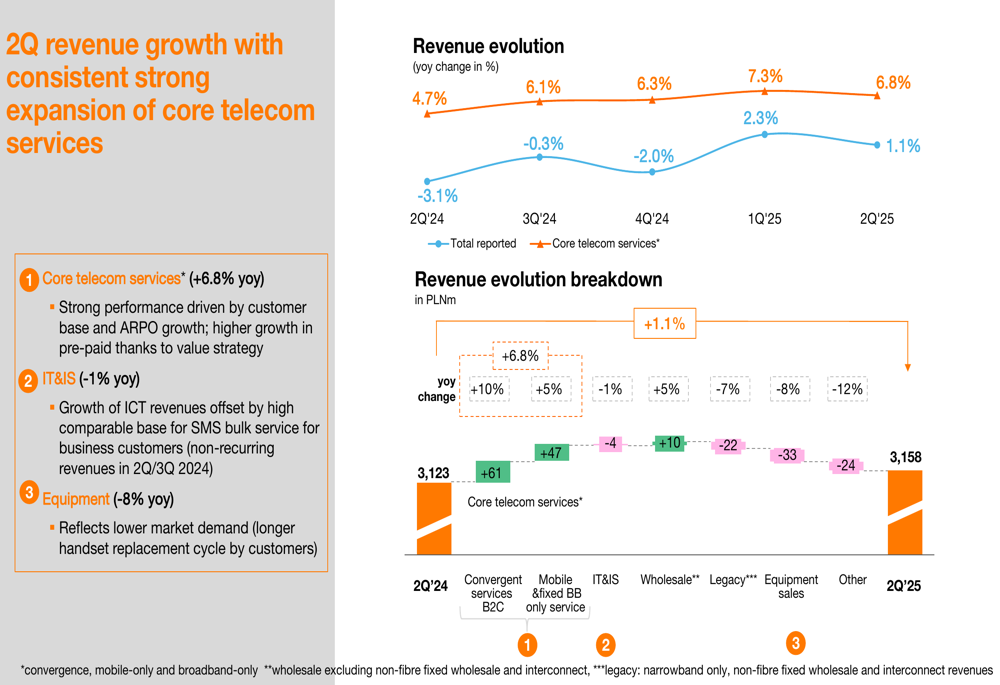

The revenue breakdown reveals the divergent performance across business segments:

While core telecom services delivered strong growth, IT and Integration Services declined slightly by 1% year-over-year. This decrease was primarily due to a high comparable base for SMS bulk service for business customers in the previous year, though partially offset by growth in ICT revenues.

Customer Growth Analysis

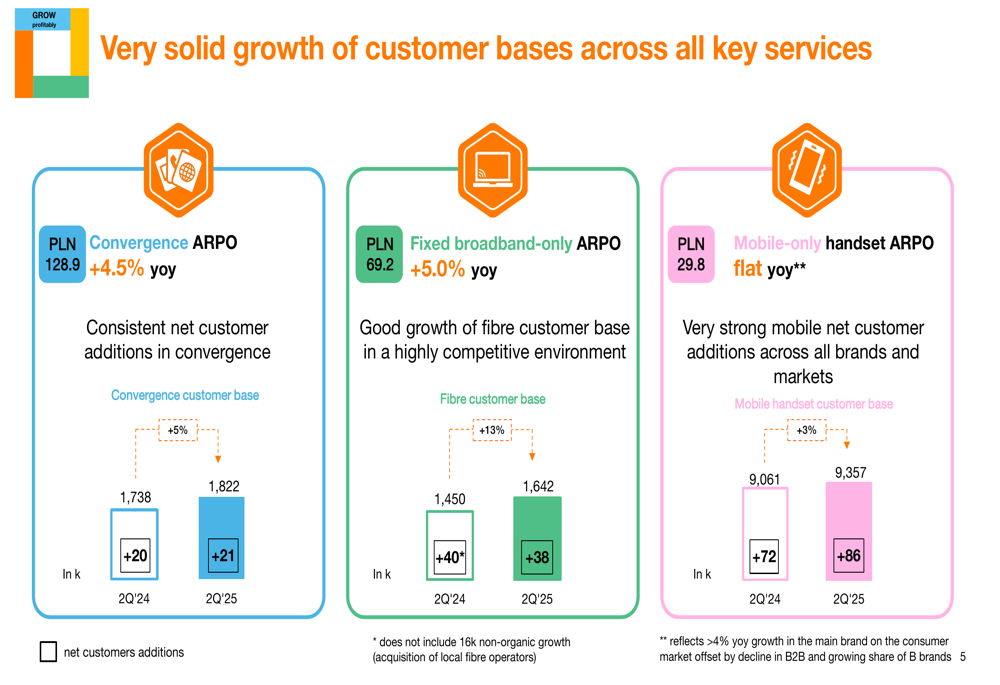

Orange Polska continued to expand its customer base across all key service categories in Q2 2025. The convergence customer base grew to 1,822,000, adding 21,000 net new customers during the quarter, while the ARPO (Average Revenue Per Offer) increased by 4.5% year-over-year to PLN 128.9.

The detailed customer metrics demonstrate solid growth across all segments:

The fiber customer base showed particularly strong momentum, reaching 1,642,000 subscribers after adding 38,000 net new customers in Q2. This represents continued strong demand for high-speed internet services, with fiber ARPO growing 5.0% year-over-year to PLN 69.2.

Mobile handset customers increased by 86,000 during the quarter to reach 9,357,000, reflecting strong additions across all brands and markets. However, mobile-only ARPO remained flat year-over-year at PLN 29.8.

Strategic Initiatives

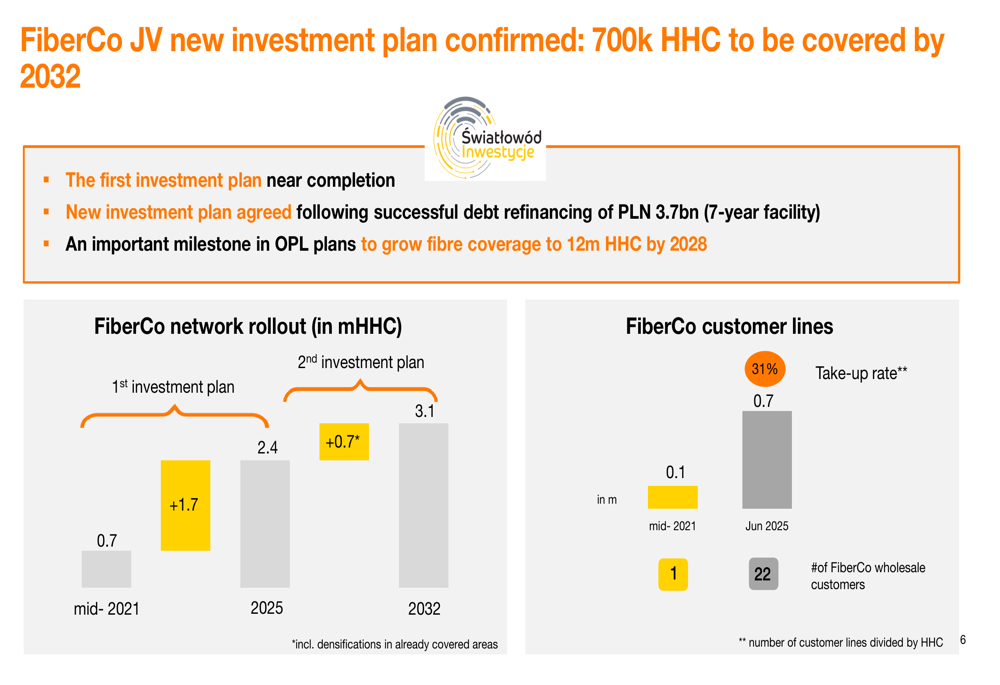

A key strategic development announced during the quarter was the new investment plan for FiberCo JV, which aims to build an additional 700,000 fiber-connected households by 2032. This follows the successful debt refinancing of PLN 3.7 billion through a seven-year facility.

The FiberCo expansion plan is illustrated in the following chart:

This new investment represents an important milestone in Orange Polska’s broader strategy to expand fiber coverage to 12 million households by 2028. The company reported that FiberCo’s customer take-up rate has reached 31%, with 22 wholesale customers now using the network.

Another strategic move highlighted in the presentation was the sale of Orange Energia, which management described as confirming the company’s focus on its core telecommunications business.

Financial Analysis

Orange Polska’s EBITDAaL growth of 4.3% in Q2 2025 continues a positive trend, following 2.9% growth in Q1 2025 and 6.8% in Q4 2024. This performance was driven by a 2% increase in direct margin, partially offset by a 1% rise in indirect costs.

The EBITDAaL evolution is detailed in the following chart:

The increase in indirect costs was primarily attributed to additional network rollout margin for FiberCo (PLN 75 million in Q2 2025 versus PLN 43 million a year ago) and higher labor costs.

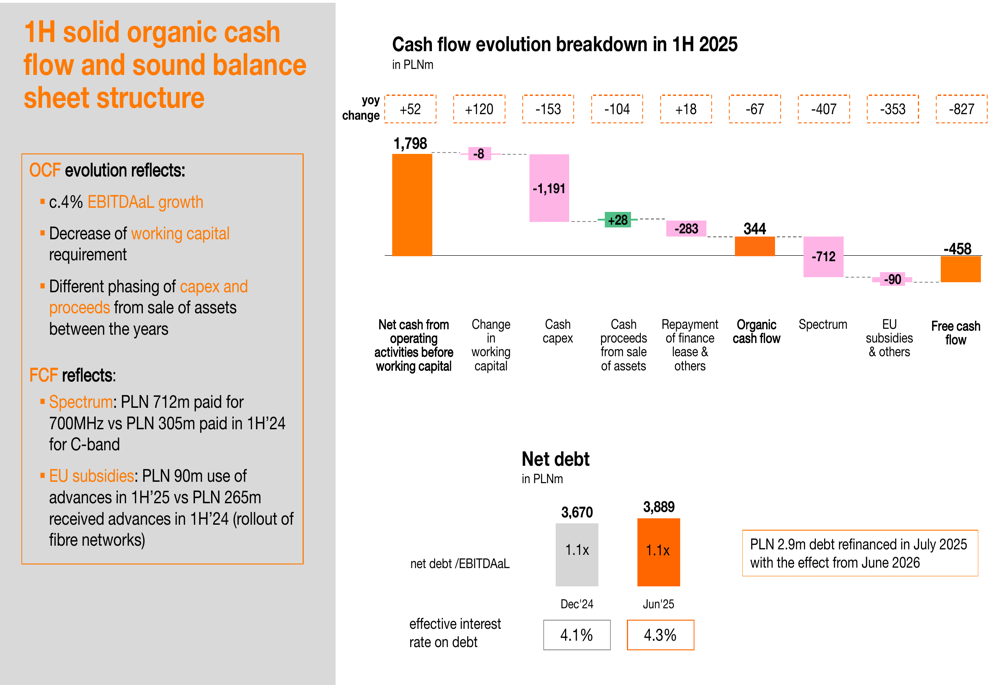

Capital expenditure (eCAPEX) decreased by 3.9% year-over-year to PLN 368 million in Q2, though the half-year figure showed an 18.6% increase to PLN 799 million. This reflects investments in mobile and fiber networks, as well as different timing of proceeds from property disposals between years.

Organic cash flow showed strong growth of 11.3% year-over-year to PLN 433 million in Q2, though the half-year figure declined by 16.3% to PLN 344 million due to timing differences in capital expenditure and proceeds from asset sales.

The company maintained a stable financial position with a net debt to EBITDAaL ratio of 1.1x as of June 2025, unchanged from December 2024. The effective interest rate on debt increased slightly to 4.3% from 4.1% at the end of 2024.

Forward-Looking Statements

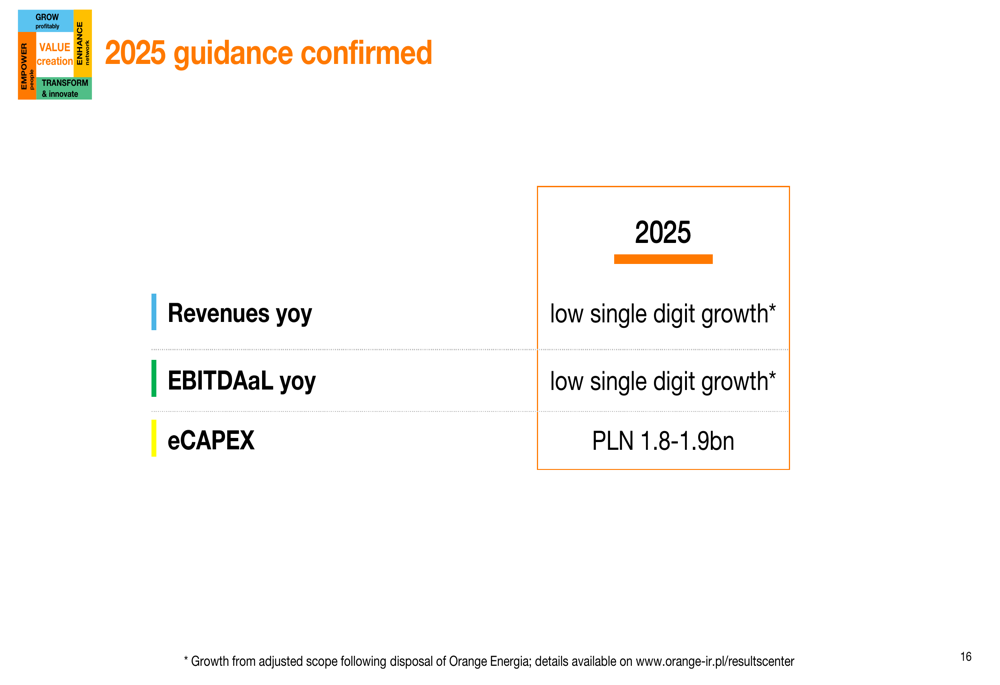

Orange Polska confirmed its full-year 2025 guidance, projecting low single-digit growth for both revenues and EBITDAaL, with eCAPEX expected to be between PLN 1.8-1.9 billion.

Management indicated that the company will focus on the high commercial season in the second half of 2025 and on progressive turnaround in the B2B segment. Additionally, Orange Polska is preparing transformation initiatives for 2026 and beyond, suggesting ongoing efforts to optimize operations and enhance competitiveness.

Conclusion

Orange Polska’s Q2 2025 results demonstrate continued solid performance, particularly in core telecom services, despite challenges in equipment sales. The company’s strategic focus on expanding fiber and mobile infrastructure continues to drive customer growth across all major segments.

With stable financial metrics, ongoing network investments, and confirmed full-year guidance, Orange Polska appears well-positioned to maintain its growth trajectory through the remainder of 2025. However, the company will need to navigate changing consumer behavior patterns, as evidenced by longer handset replacement cycles, and successfully execute its transformation initiatives to sustain long-term growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.