Street Calls of the Week

Introduction & Market Context

Orexo AB (STO:ORX) presented its Q3 2025 interim report on October 23, 2025, highlighting its strategic focus on AmorphOX technology amid challenging financial results. The presentation coincided with a significant 14.8% drop in the company’s stock price, which fell to 31.9 SEK following a revenue miss that disappointed investors.

The Swedish pharmaceutical company continues to position its AmorphOX nasal powder delivery technology as a key differentiator in growing markets, including the anti-obesity medication space, which is projected to reach $150 billion by 2032, and the opioid overdose treatment sector, where xylazine-laced products present a growing public health challenge.

Quarterly Performance Highlights

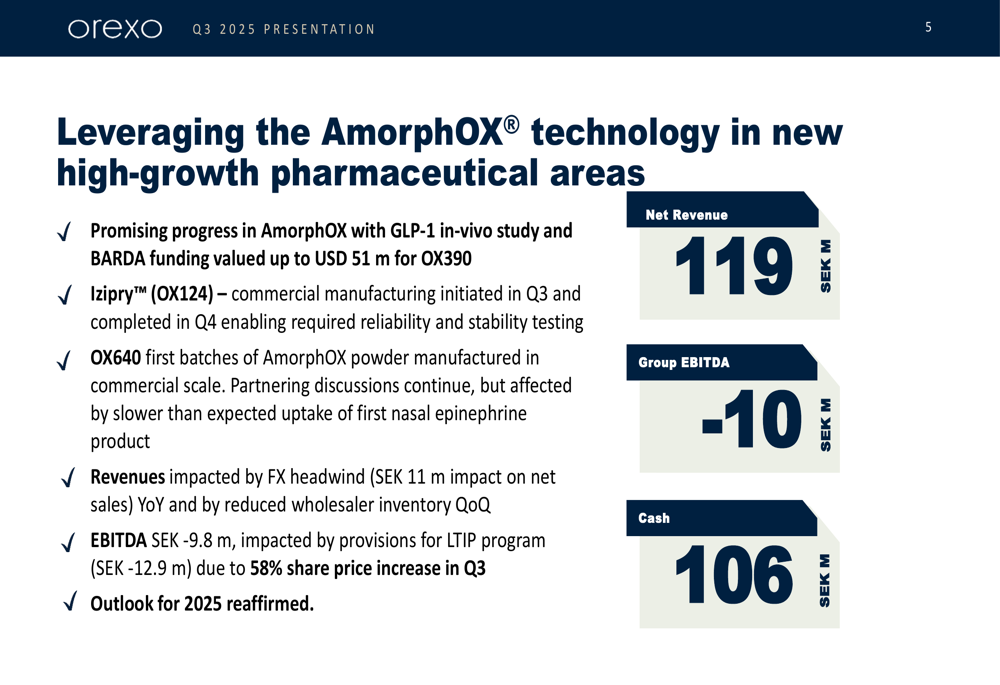

Orexo reported Q3 2025 net revenue of 119 million SEK, falling short of analyst expectations of 128.1 million SEK. The company posted a negative EBITDA of 9.8 million SEK, though management noted this figure would have been positive excluding long-term incentive program provisions.

As shown in the following quarterly highlights slide, the company’s performance was impacted by foreign exchange headwinds (11 million SEK) and reduced wholesaler inventory:

Zubsolv, Orexo’s primary revenue driver, experienced a 4.8% decline in local currency terms. The company attributed this partly to wholesaler inventory fluctuations, which they characterize as seasonal, with inventory build expected in Q4 following historic patterns.

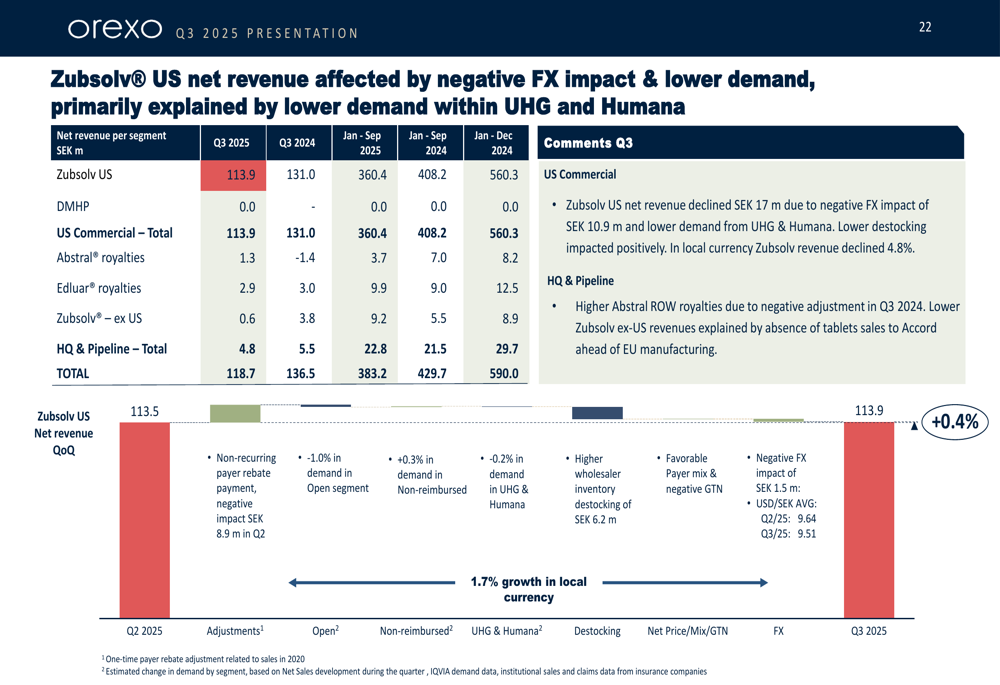

As illustrated in the following revenue analysis, Zubsolv US net revenue declined by 17 million SEK year-over-year, with nearly 11 million SEK attributed to negative currency effects:

Pipeline and Product Development

Despite financial challenges, Orexo highlighted several promising developments in its product pipeline, particularly around its AmorphOX technology platform.

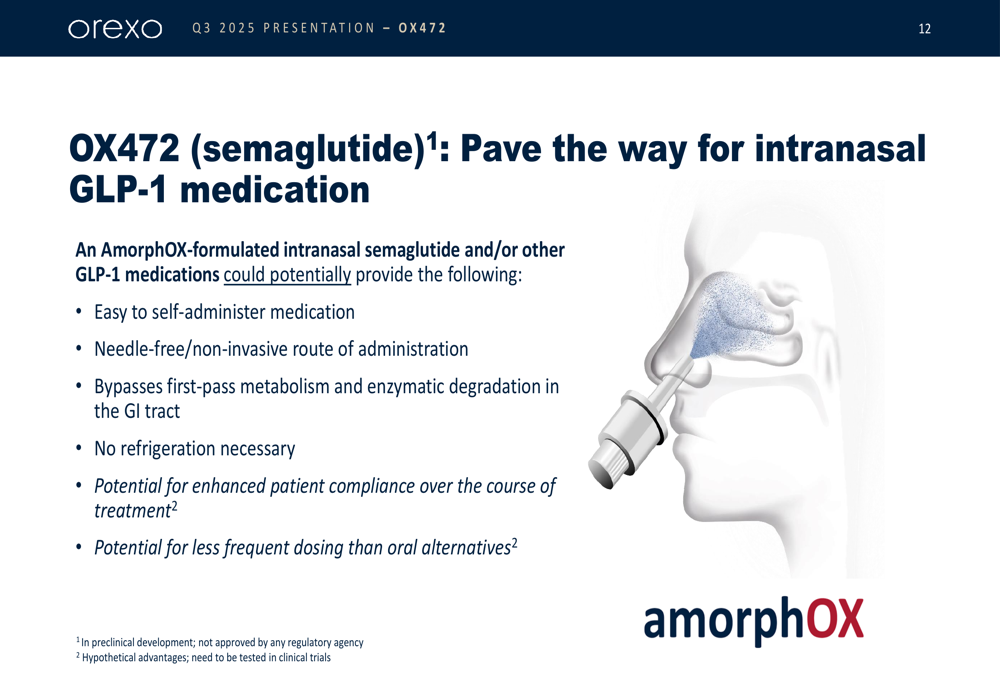

The company’s most notable advancement is in the application of AmorphOX technology to deliver GLP-1 receptor agonists nasally. Their OX472 program, focused on intranasal semaglutide formulation, shows potential advantages over existing products:

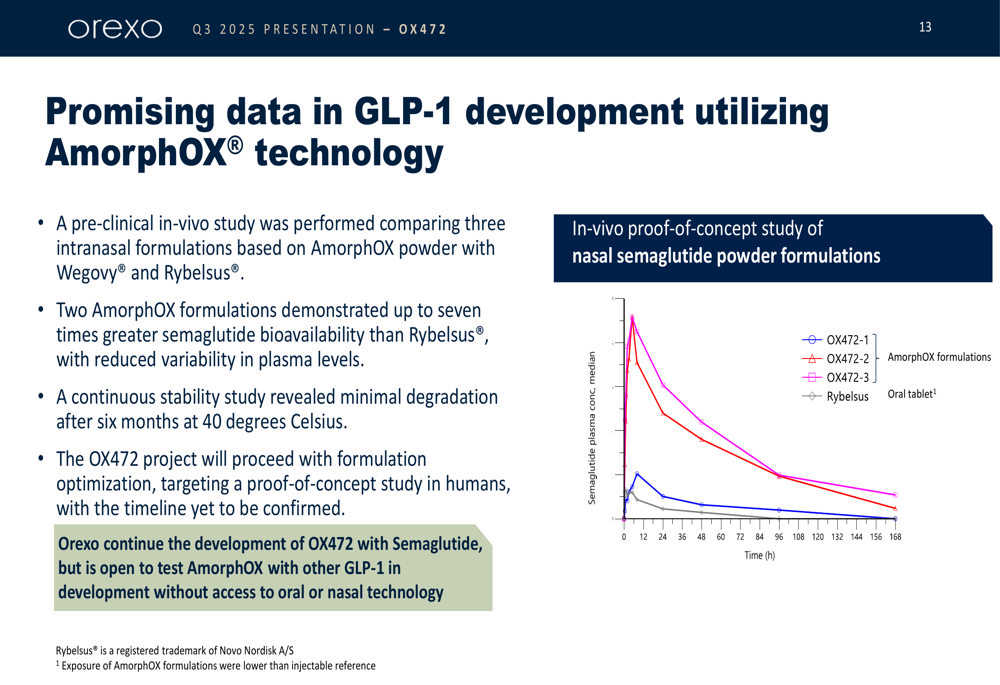

Preclinical data for OX472 appears promising, with the company reporting that two AmorphOX formulations demonstrated up to seven times greater semaglutide bioavailability than Rybelsus:

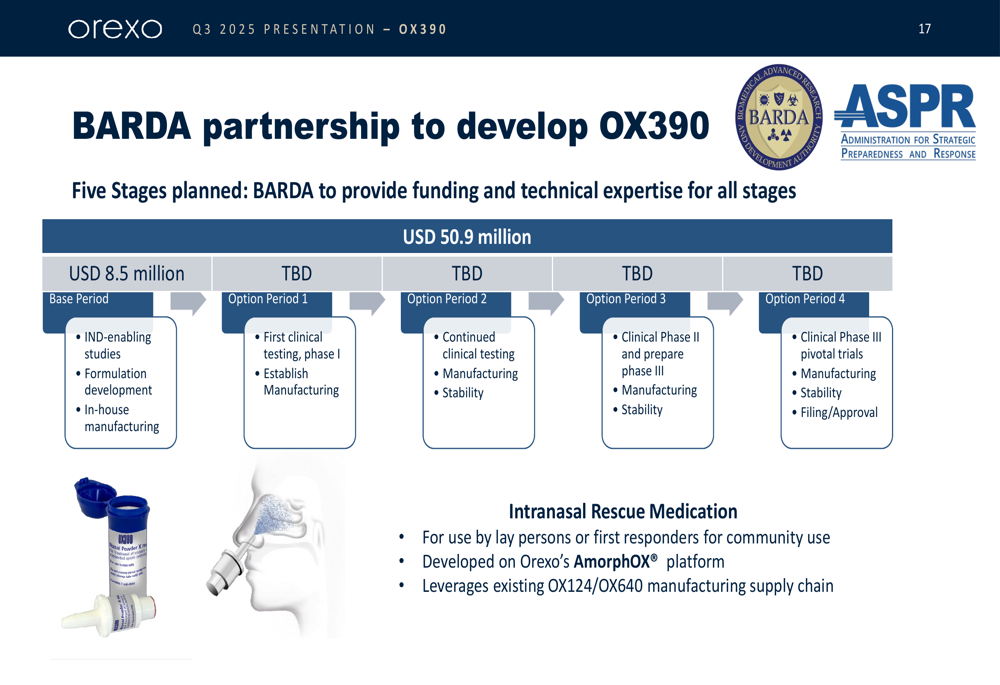

Another significant development is the BARDA partnership for OX390, an intranasal rescue medication for xylazine-related overdoses. This partnership provides substantial funding of $50.9 million through a five-stage development process:

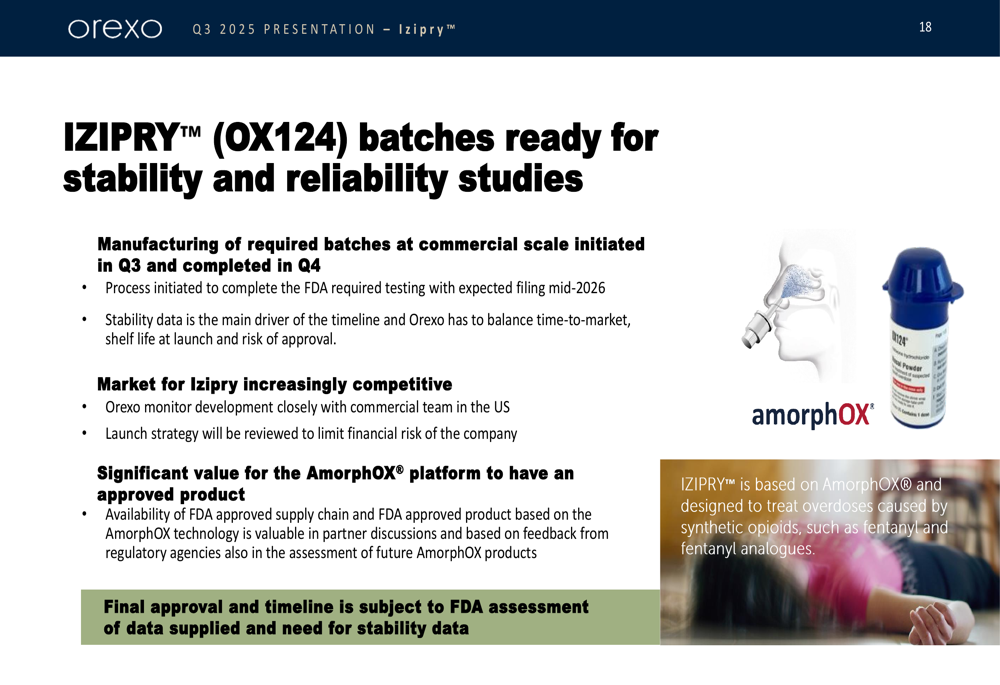

The company also reported progress with IZIPRY (OX124), with commercial manufacturing initiated in Q3 and completed in Q4. The product’s timeline is primarily driven by stability data requirements:

Financial Analysis

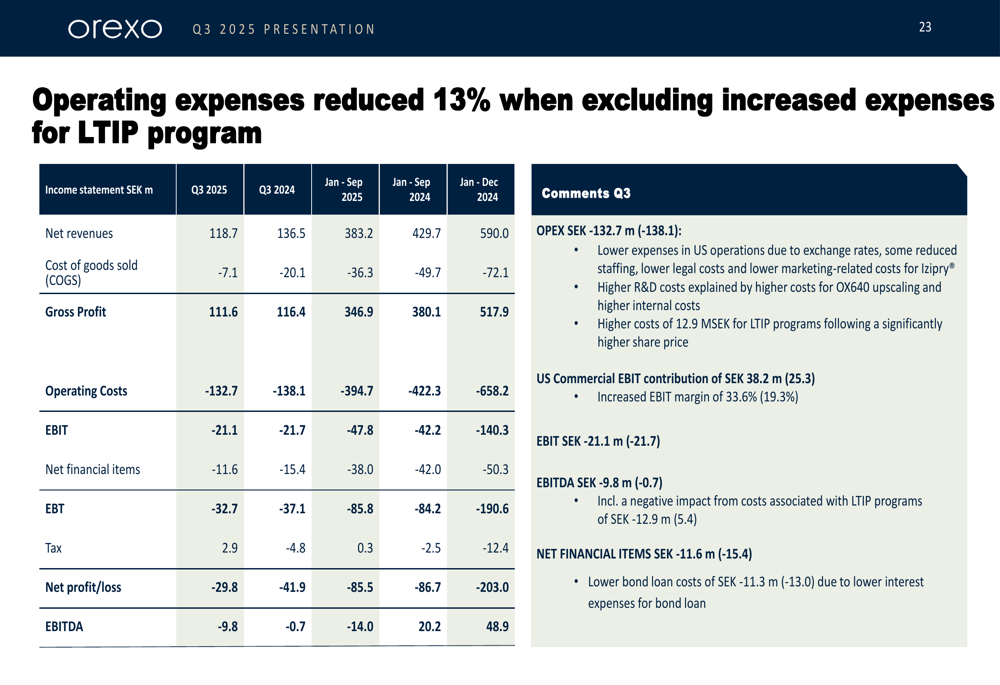

Orexo’s operating expenses and income statement reveal the financial challenges the company faces. While operating expenses were reduced by 13% when excluding increased expenses for the LTIP program, the company still reported negative EBIT and EBITDA figures:

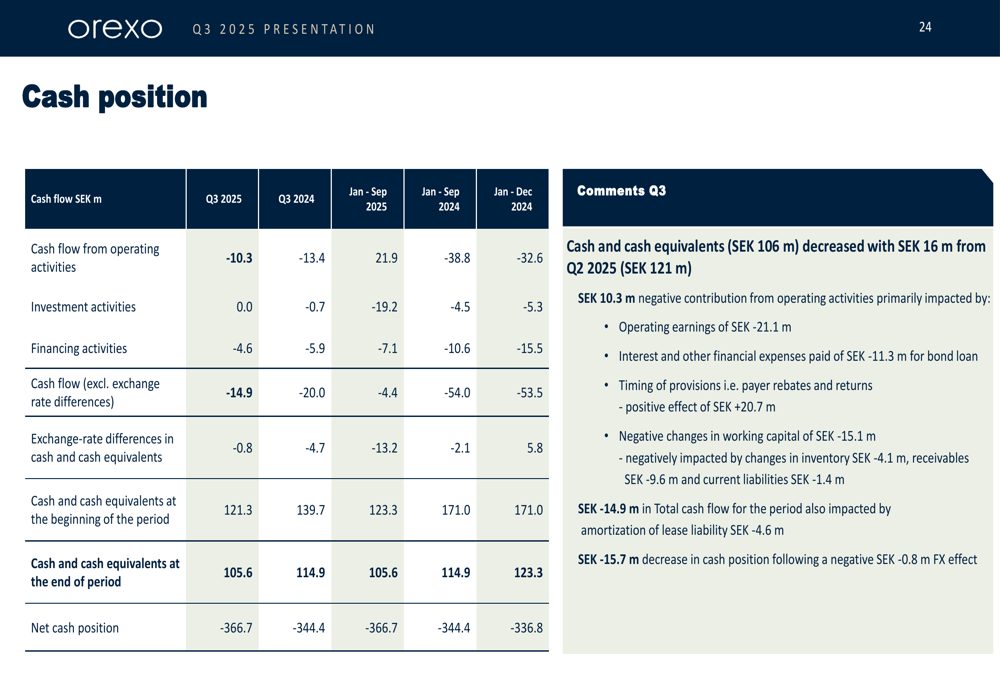

The cash position analysis shows a decrease of 16 million SEK during the quarter, with the company ending Q3 with 105.6 million SEK in cash and cash equivalents:

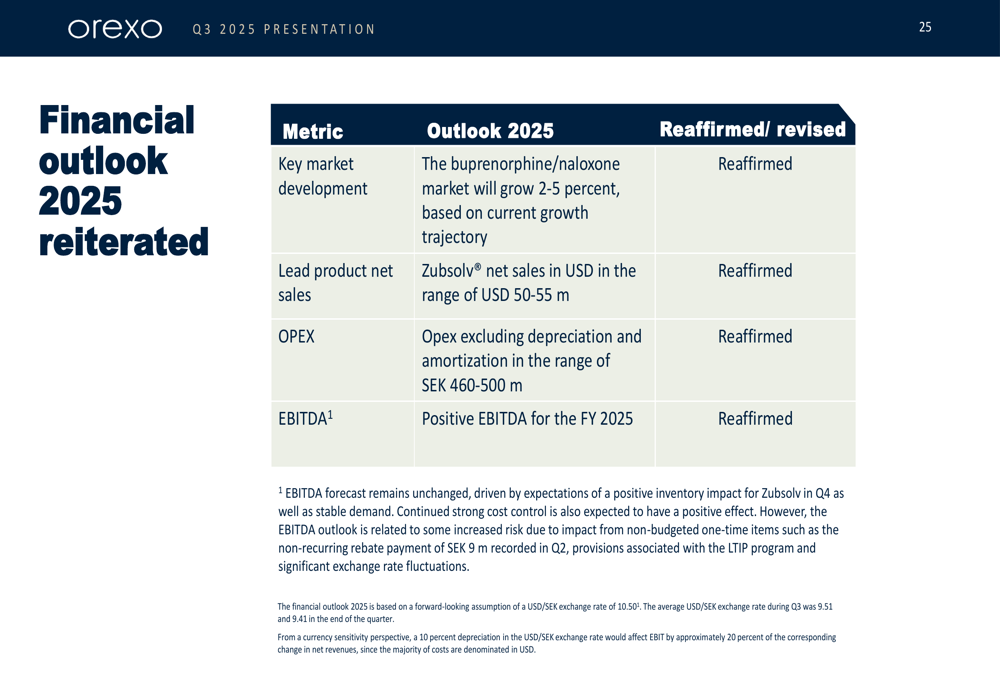

Despite current challenges, Orexo reiterated its financial outlook for 2025, maintaining guidance for positive EBITDA for the full year:

Strategic Initiatives and Outlook

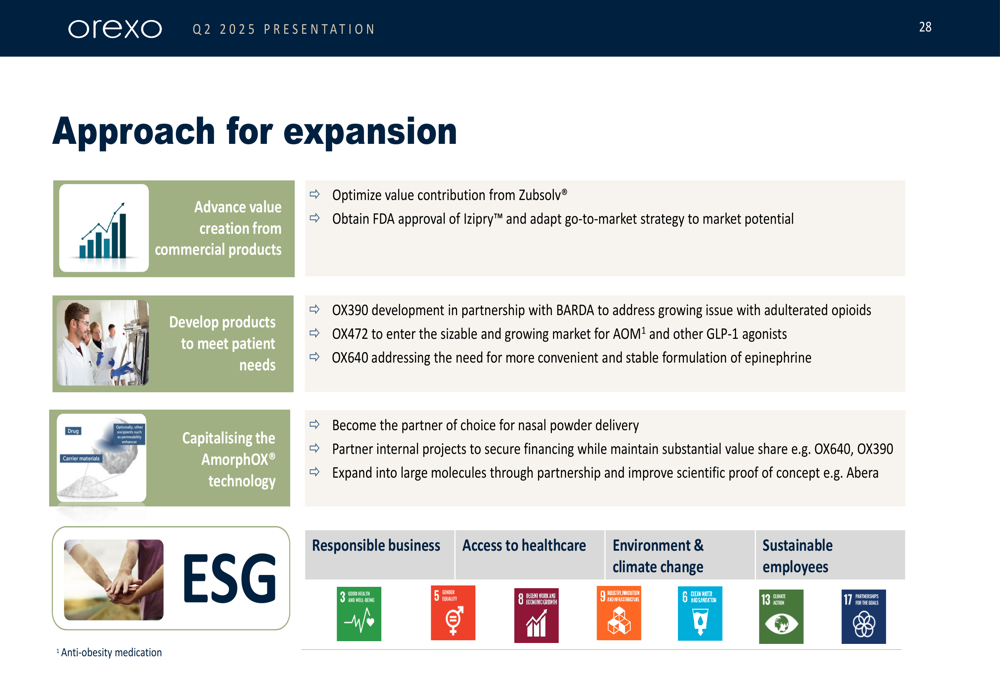

Orexo outlined its approach for expansion, focusing on four key areas: optimizing value from commercial products, developing products to meet patient needs, capitalizing on AmorphOX technology, and advancing ESG goals:

The company faces significant challenges, as reflected in its stock performance. Following the earnings announcement, Orexo’s stock fell by 14.8% to 31.9 SEK, moving closer to its 52-week low of 9.2 SEK rather than its high of 43.4 SEK.

While current financial results disappointed investors, Orexo’s management remains confident in the company’s long-term strategy, particularly regarding its nasal delivery technology. CEO Nikolaj Sørensen emphasized during the earnings call that Orexo has "the world’s leading nasal powder delivery" technology, suggesting that pipeline developments could eventually offset current revenue challenges.

The contrast between immediate financial pressures and potential future growth through innovative pipeline products presents a complex picture for investors evaluating Orexo’s prospects moving forward.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.