German construction sector still in recession, civil engineering only bright spot

Introduction & Market Context

OrthoPediatrics Corp (NASDAQ:KIDS) recently presented its Q2 2025 investor slides, highlighting the company’s continued growth in the pediatric orthopedic market. As the only focused pediatric orthopedic company globally, OrthoPediatrics has treated over 1.2 million pediatric patients since inception and continues to expand its market presence.

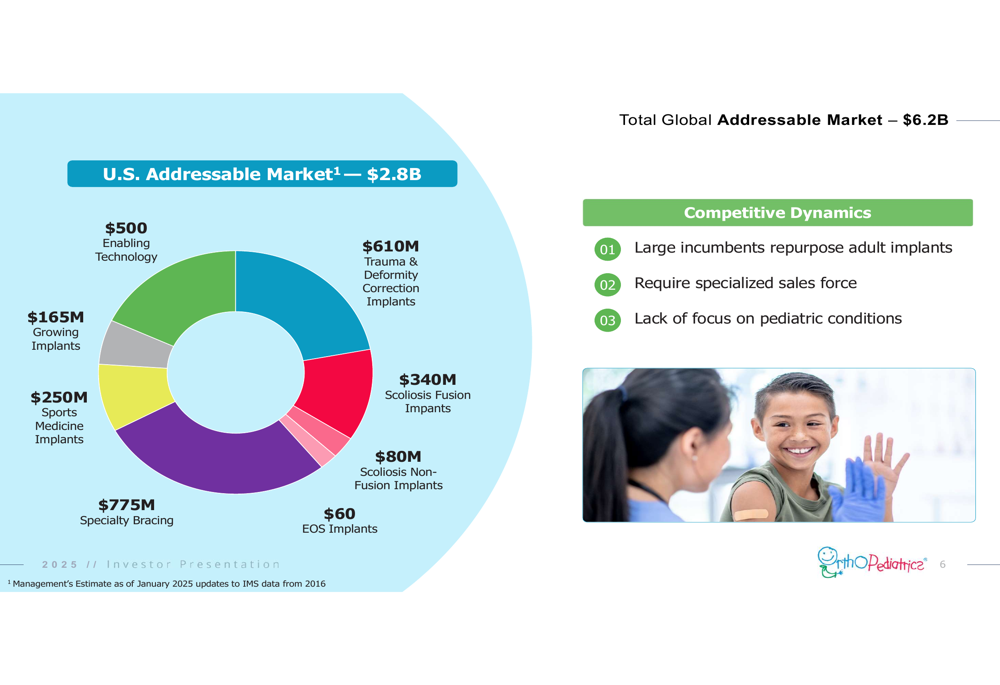

The company operates in a total global addressable market of $6.2 billion, with the U.S. addressable market at $2.8 billion. Despite reporting a 1.66% stock decline to $20.53 following its earnings release on August 5, 2025, the company beat EPS forecasts with better-than-expected adjusted EBITDA.

As shown in the following chart, OrthoPediatrics has identified significant market opportunities across multiple segments:

Strategic Initiatives and Market Expansion

OrthoPediatrics’ growth strategy centers on five key pillars: focusing on high-volume children’s hospitals, providing a broad pediatric-specific product portfolio, deploying instrument sets with unparalleled sales support, expanding through R&D and M&A, and training the next generation of pediatric orthopedic surgeons.

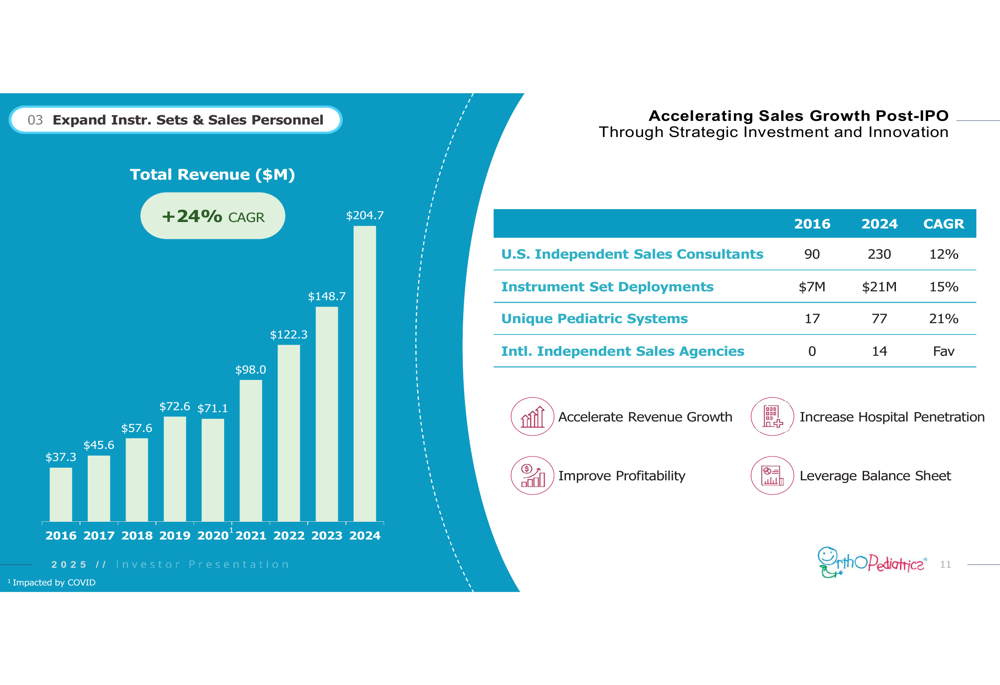

The company has significantly expanded its commercial presence, with U.S. independent sales consultants growing from 90 in 2016 to 230 in 2024, representing a 12% CAGR. Instrument set deployments have also increased at a 15% CAGR during the same period.

The following slide illustrates this commercial expansion:

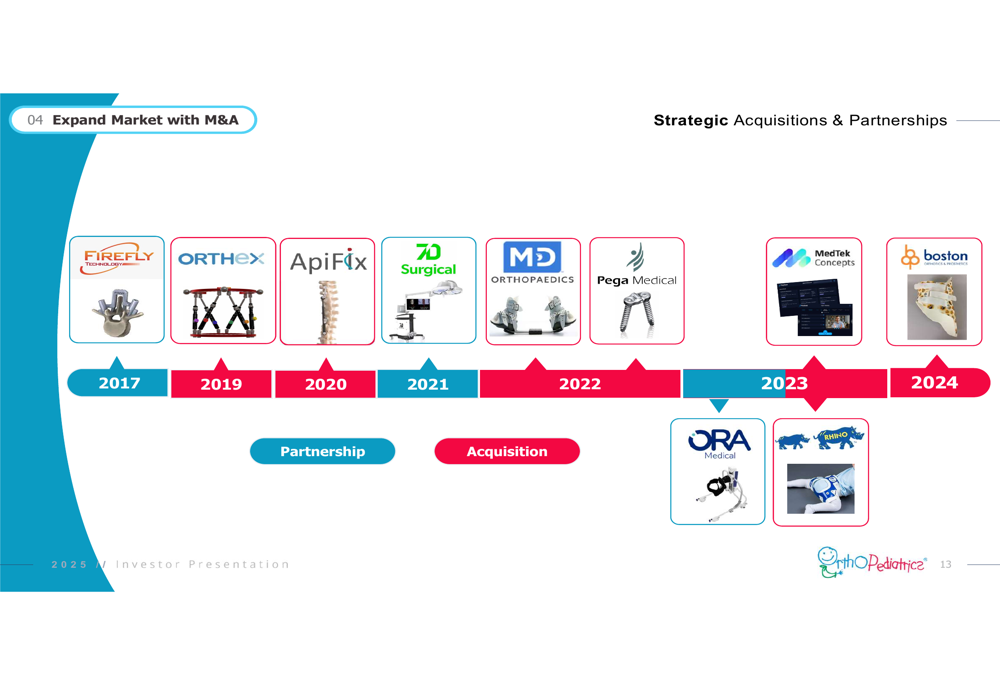

Strategic acquisitions have played a crucial role in OrthoPediatrics’ growth. Most recently, the company acquired Boston Orthotics & Prosthetics for $22 million in January 2024, establishing its OrthoPediatrics Specialty Bracing (OPSB) division. This acquisition has opened up a new $500 million U.S. specialty bracing market opportunity.

The company’s acquisition timeline demonstrates its commitment to expanding capabilities through strategic M&A:

The OPSB division has ambitious growth plans, targeting 18 new markets by 2027 and doubling its sales channel. This expansion is expected to significantly contribute to future revenue growth as the company penetrates the $1.1 billion global specialty bracing market.

Product Portfolio and Innovation

OrthoPediatrics has expanded from 17 unique pediatric systems in 2016 to 77 in 2024, representing a 21% CAGR. The company’s product portfolio spans trauma and deformity correction, scoliosis treatment, and sports medicine, with innovative technologies that address the unique needs of pediatric patients.

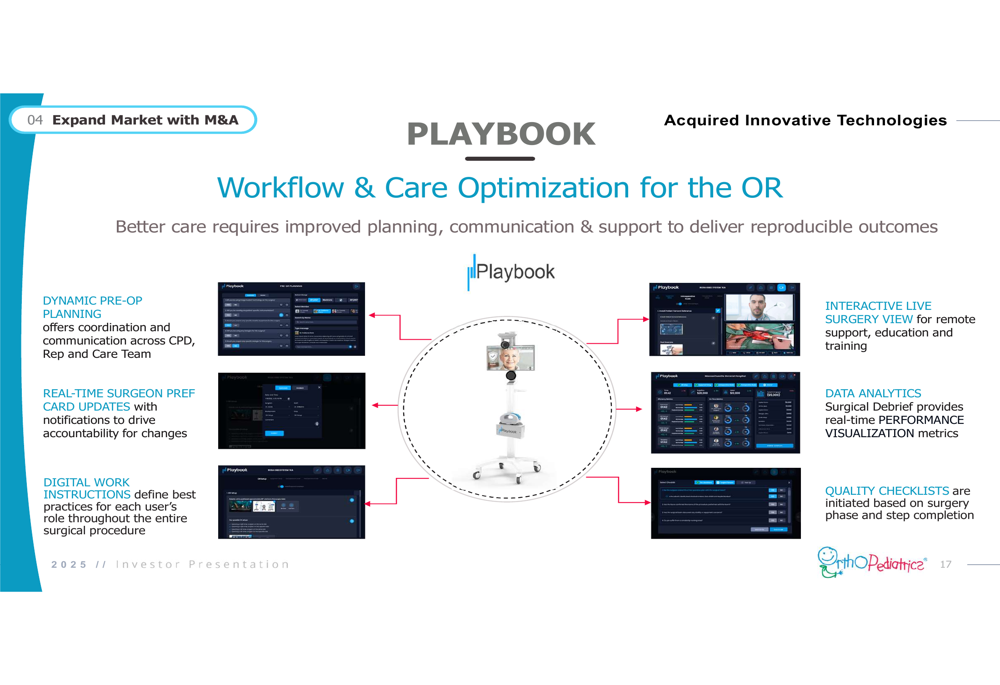

One of the company’s key technological innovations is the PLAYBOOK platform, which optimizes workflow and care in the operating room:

The company continues to invest in R&D, with several new products in the pipeline for 2025 and beyond. These include the 3P Hip system, VerteGlide (FDA approved April 2025), and ELLI (FDA submission expected by early 2026), which are designed to address early-onset scoliosis and other pediatric orthopedic conditions.

Financial Performance and Outlook

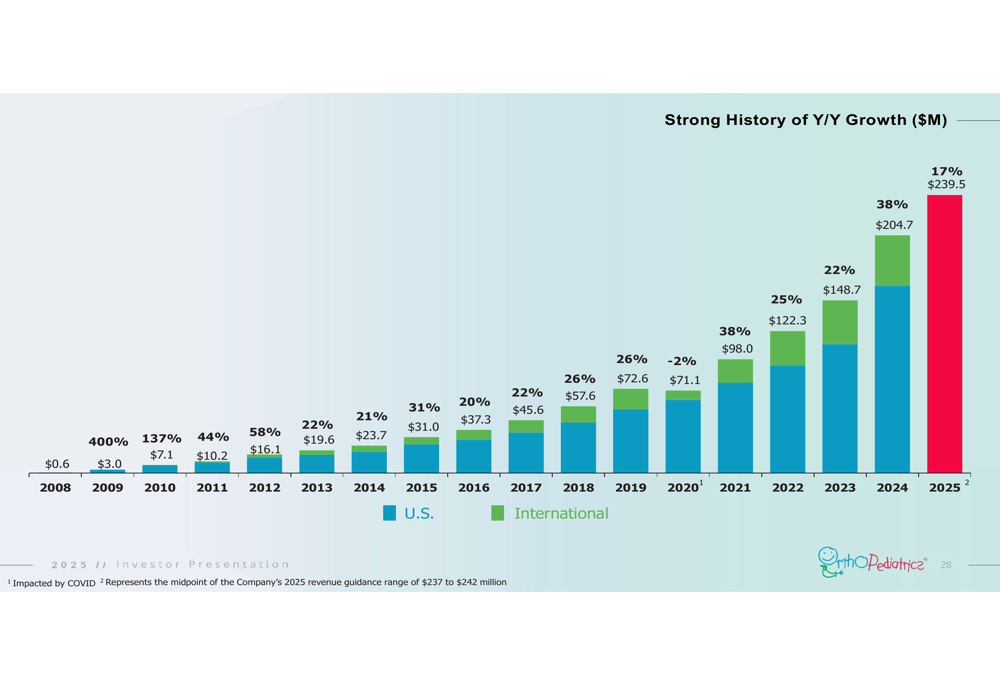

OrthoPediatrics reported Q2 2025 revenue of $61.1 million, representing a 16% year-over-year increase. U.S. revenue grew 17% to $48.1 million, while international revenue increased 12% to $13.0 million.

The company has demonstrated consistent year-over-year growth since its inception, as illustrated in this revenue chart:

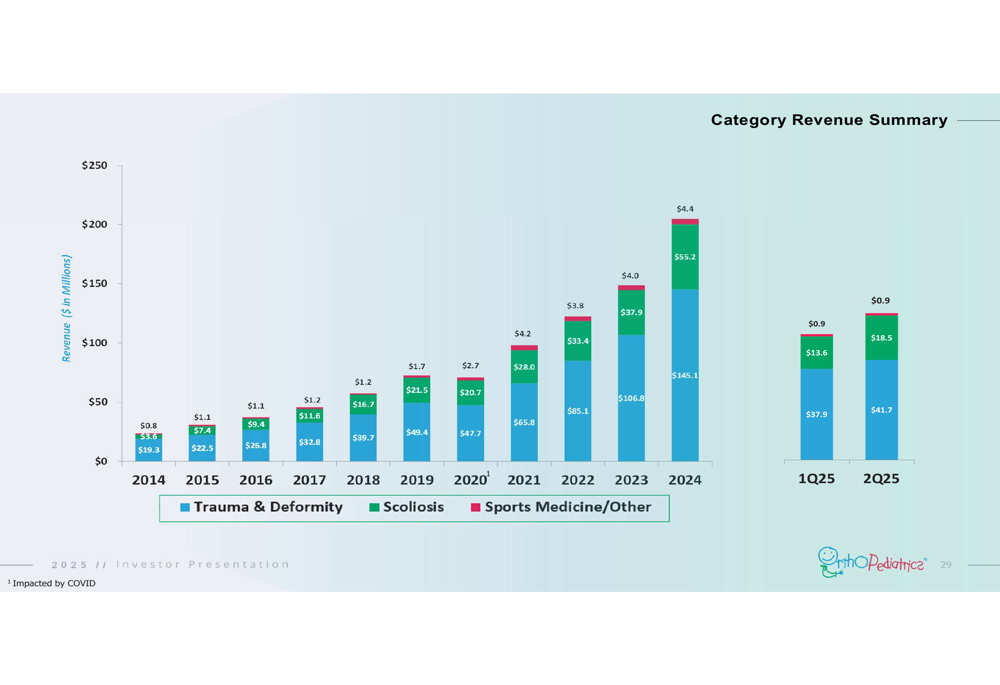

By product category, trauma and deformity products generated $41.7 million in Q2 2025 (up from $37.8 million in Q2 2024), while scoliosis products contributed $18.5 million (up from $13.7 million). Sports medicine and other products accounted for $0.9 million, down from $1.3 million in the prior year.

The company’s revenue by product category shows the following trends:

While revenue growth remains strong, OrthoPediatrics continues to report operating losses. In Q2 2025, the company reported an operating loss of $10.6 million, compared to $5.7 million in Q2 2024. However, adjusted EBITDA improved to $4.1 million from $2.6 million in the prior year period.

Gross profit margin decreased to 72% in Q2 2025 from 77% in Q2 2024, reflecting increased costs and product mix changes. Despite this margin pressure, the company raised its full-year 2025 revenue guidance to $237-242 million, representing 16-18% growth over 2024.

Challenges and Forward-Looking Statements

While OrthoPediatrics continues to grow revenue at a healthy pace, the company faces several challenges. Operating losses have increased year-over-year, and gross margin has declined. The company is implementing restructuring initiatives, with $3.0 million in restructuring charges reported in Q2 2025.

CEO Dave Bailey emphasized the company’s commitment to "helping more children than ever, significantly growing revenue, improving adjusted EBITDA, and reducing cash burn in 2025 and beyond." The company expects to achieve $15-17 million in adjusted EBITDA for the full year and is targeting its first quarter of positive free cash flow in 2025.

OrthoPediatrics’ stock has been under pressure, trading near its 52-week low of $19.52 with a -29.3% return over the past year. However, the company’s continued revenue growth, strategic acquisitions, and product innovation position it well for long-term success in the specialized pediatric orthopedic market.

As the company executes on its specialty bracing expansion strategy and brings new products to market, investors will be watching closely to see if improved operational efficiency can translate into reduced operating losses and eventual profitability.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.