Procore signs multi-year strategic collaboration agreement with AWS

Introduction & Market Context

Otis Worldwide Corporation (NYSE:OTIS) released its Q1 2025 earnings presentation on April 23, 2025, revealing a mixed performance as the company continues to navigate challenges in the new equipment market while driving growth in its service business. The stock was down 2.98% in premarket trading, suggesting investors may have concerns about certain aspects of the results despite some positive metrics.

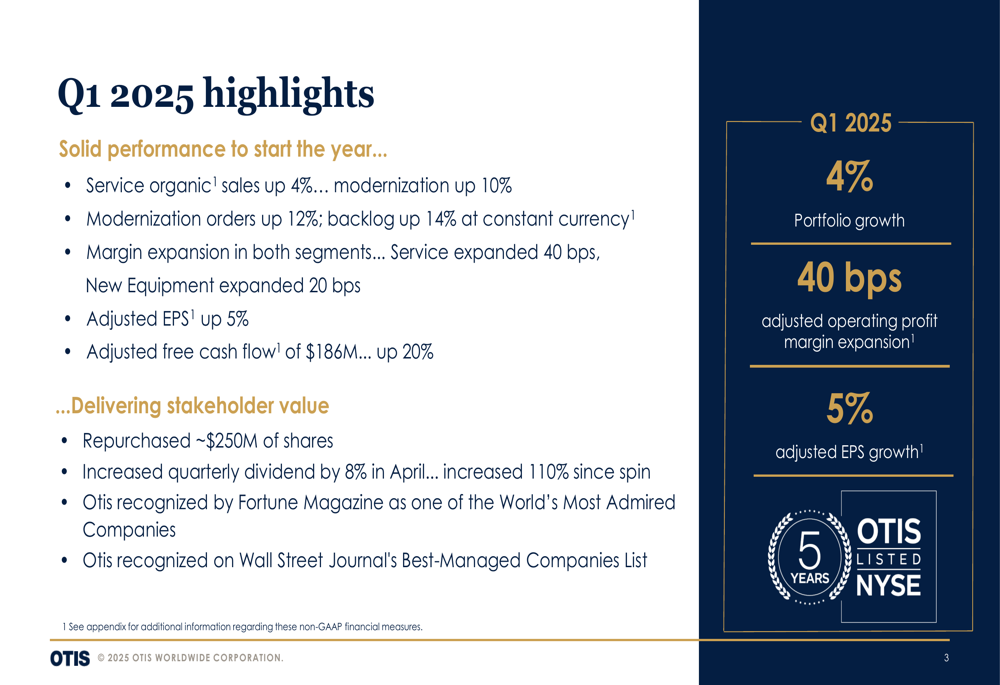

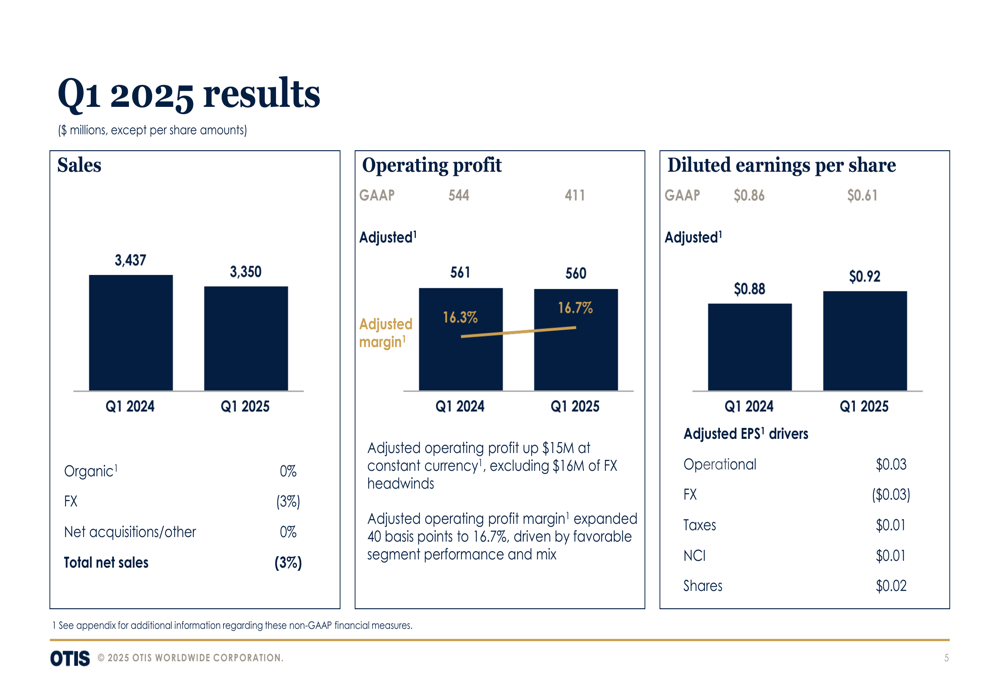

The elevator and escalator manufacturer reported adjusted earnings per share of $0.92, up 5% year-over-year, on net sales of $3.35 billion, which declined 3% compared to Q1 2024. While organic growth was flat, foreign exchange headwinds impacted total sales by 3%.

Quarterly Performance Highlights

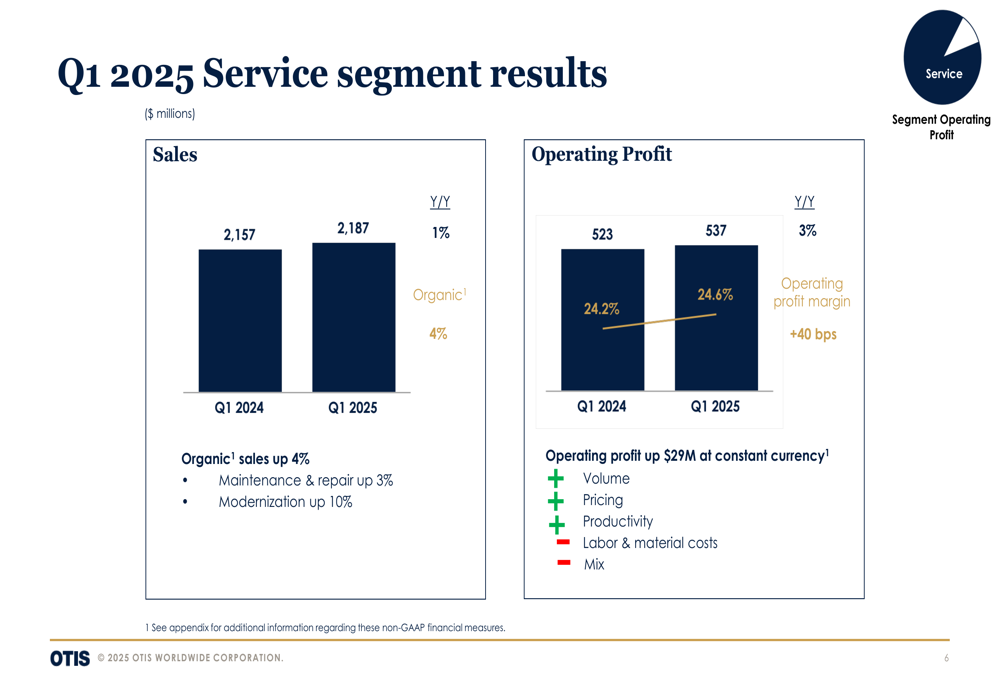

Otis delivered solid results in its service segment, which continues to be the primary growth driver for the company. Service organic sales increased 4% year-over-year, while modernization sales grew an impressive 10%. The company’s maintenance portfolio expanded by 4%, reinforcing its position as the industry leader.

As shown in the following summary of Q1 highlights, Otis achieved margin expansion in both segments, with service margins improving by 40 basis points and new equipment margins by 20 basis points:

The company generated $186 million in adjusted free cash flow, representing a 20% increase compared to the same period last year. This strong cash generation supported approximately $250 million in share repurchases during the quarter. Additionally, Otis increased its quarterly dividend by 8% in April, marking a 110% increase since the company’s spin-off.

Detailed Financial Analysis

Otis’s Q1 2025 results reveal divergent performance between its two main business segments. The service segment, which includes maintenance, repair, and modernization, posted sales of $2.19 billion, up 1% year-over-year with organic growth of 4%. Operating profit for this segment increased 3% to $537 million, with margins expanding to 24.6%.

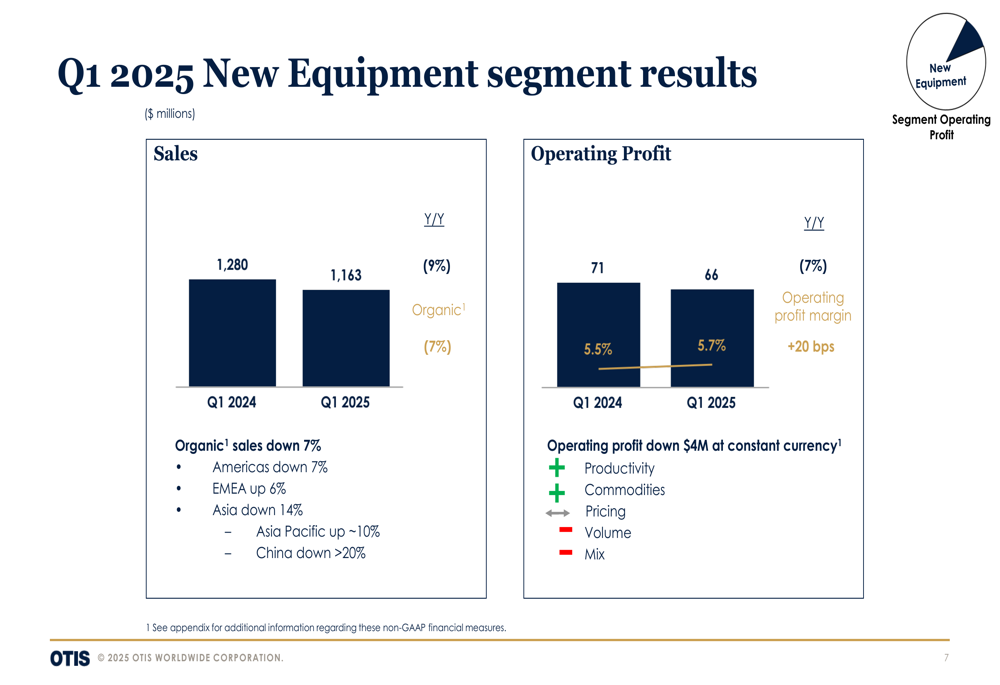

In contrast, the new equipment segment faced significant headwinds, with sales declining 9% to $1.16 billion and organic sales down 7%. Operating profit decreased 7% to $66 million, though margins improved slightly to 5.7% due to productivity improvements and commodity tailwinds.

The following chart illustrates the company’s overall financial performance for Q1 2025:

Regional performance varied significantly within the new equipment segment. While the Americas experienced a 7% decline in organic sales and EMEA (Europe, Middle East, and Africa) grew by 6%, Asia saw a substantial 14% drop, primarily driven by China, where sales fell more than 20%. In contrast, Asia Pacific (excluding China) delivered approximately 10% growth.

The orders and backlog data provide further insight into these regional disparities:

Strategic Initiatives

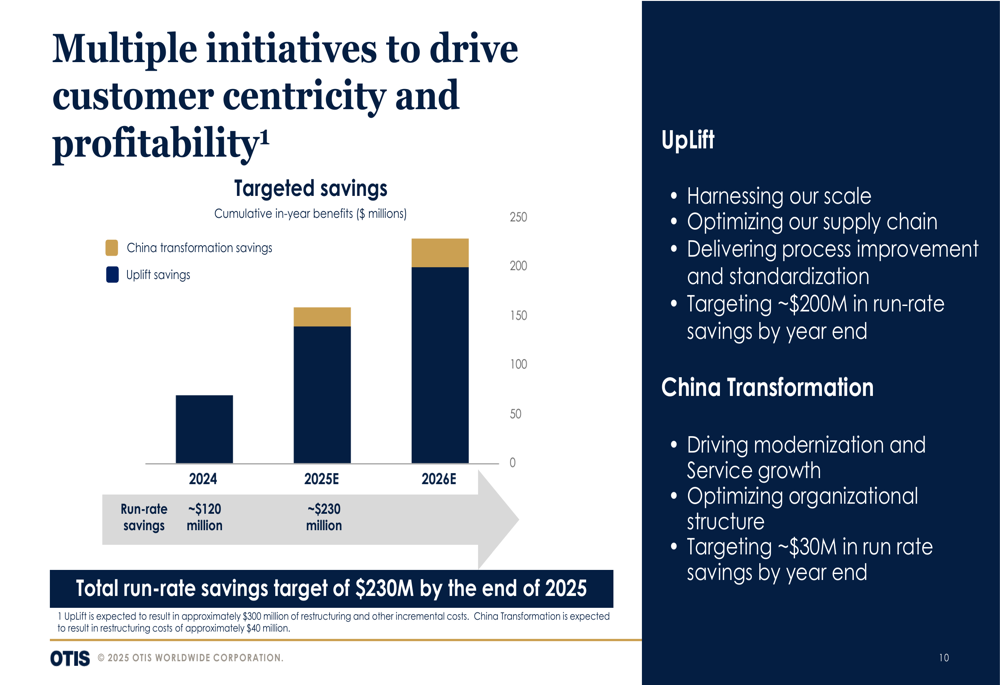

Otis is implementing two major transformation initiatives to drive customer centricity and profitability: the Uplift program and the China Transformation. These initiatives are expected to deliver significant cost savings over the coming years.

The following chart illustrates the projected cumulative benefits from these programs:

The Uplift program focuses on harnessing scale, optimizing supply chain, and delivering process improvements and standardization. It targets approximately $200 million in run-rate savings by year-end 2025. Meanwhile, the China Transformation aims to drive modernization and service growth while optimizing organizational structure, with targeted run-rate savings of approximately $30 million by year-end.

Together, these initiatives are expected to generate approximately $230 million in run-rate savings by the end of 2025, helping to offset challenges in the new equipment market, particularly in China.

Forward-Looking Statements

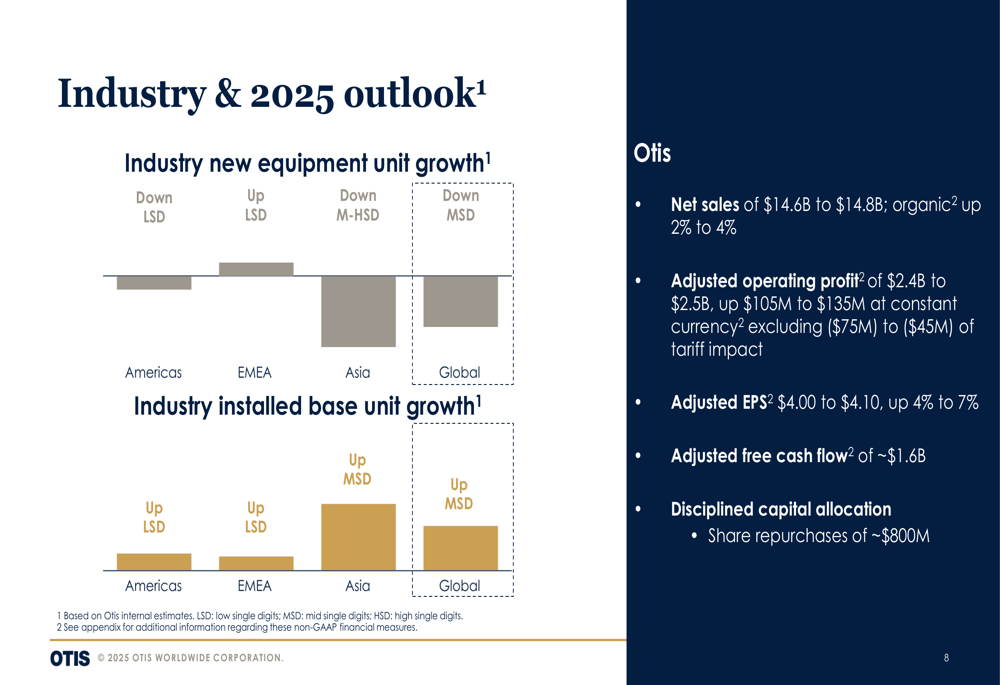

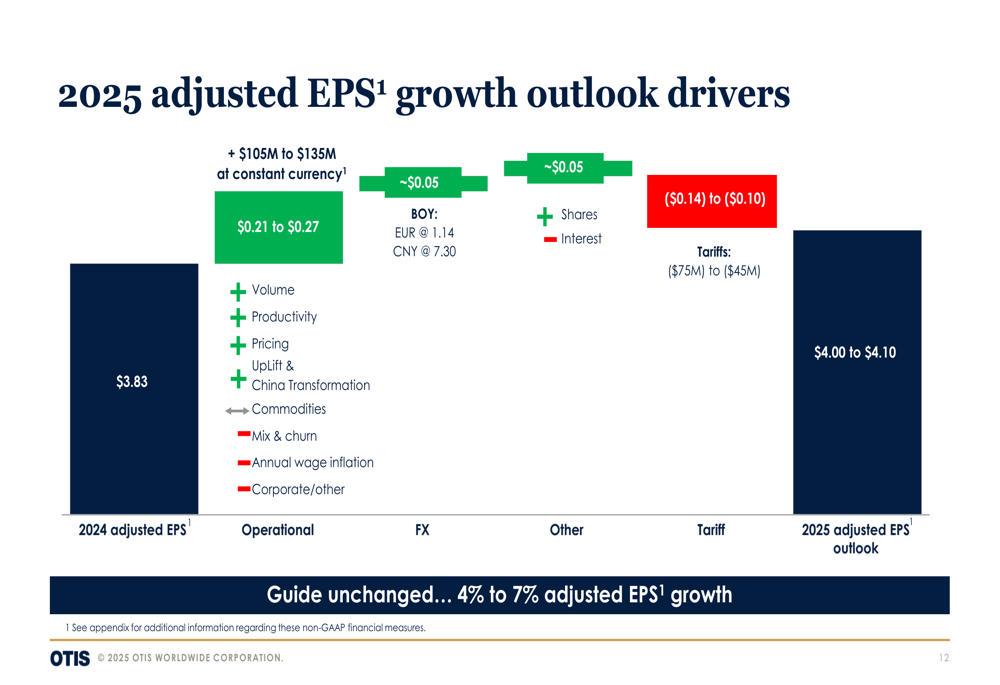

Otis provided its outlook for 2025, projecting net sales of $14.6 billion to $14.8 billion with organic growth of 2% to 4%. The company expects adjusted operating profit of $2.4 billion to $2.5 billion, up $105 million to $135 million at constant currency, excluding $75 million to $45 million of tariff impact.

The industry outlook varies by region, as shown in the following slide:

For 2025, Otis anticipates adjusted EPS of $4.00 to $4.10, representing growth of 4% to 7%. The company also projects adjusted free cash flow of approximately $1.6 billion and plans to repurchase around $800 million in shares.

The drivers of the 2025 adjusted EPS growth outlook are broken down as follows:

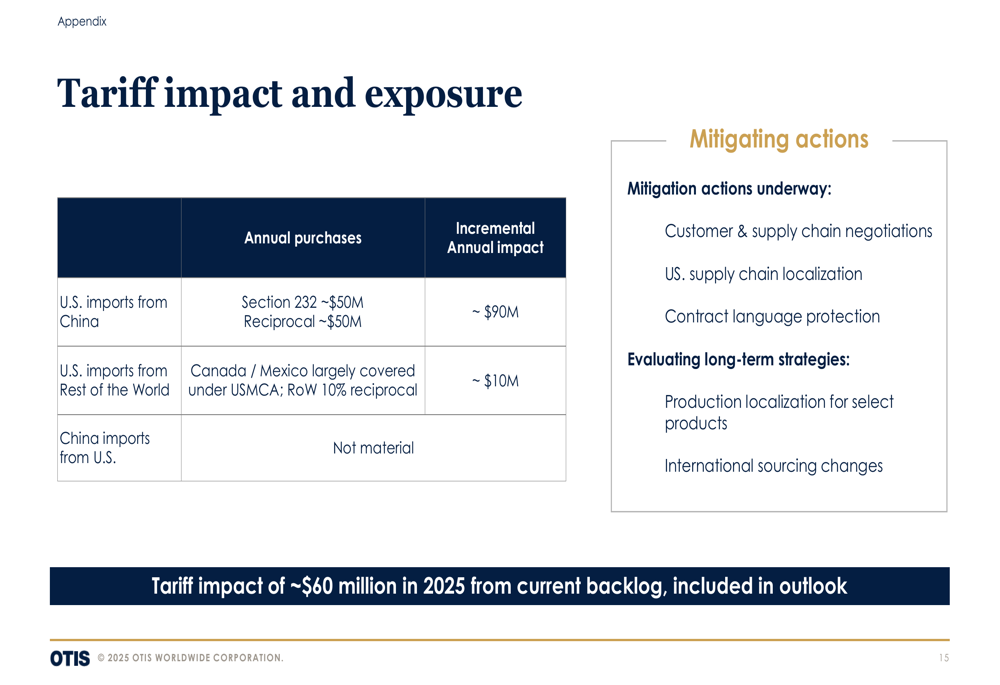

Tariff Impact and Mitigation Strategies

Otis is addressing the impact of tariffs, which are expected to affect the company’s 2025 results. The company has identified approximately $90 million in U.S. imports from China and $10 million from the rest of the world that are subject to tariffs.

To mitigate these impacts, Otis is implementing several strategies, including customer and supply chain negotiations, U.S. supply chain localization, and contract language protection. The company is also evaluating long-term strategies such as production localization for select products and international sourcing changes.

The following slide details the tariff impact and exposure:

Segment Performance Analysis

The service segment continues to be the cornerstone of Otis’s business model, generating consistent growth and profitability. In Q1 2025, this segment benefited from volume growth, pricing improvements, and productivity gains, partially offset by higher labor and material costs.

The detailed service segment results are illustrated below:

Meanwhile, the new equipment segment faced challenges, particularly in China. Despite these headwinds, the segment achieved margin expansion through productivity improvements and commodity tailwinds, which helped offset the negative impacts of lower volume and unfavorable mix.

The new equipment segment results are shown in the following slide:

As Otis navigates the evolving market landscape, the company’s focus on service growth, modernization opportunities, and cost optimization initiatives positions it to weather the current challenges in the new equipment market while driving long-term value creation for shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.