Stock market today: S&P 500 climbs as health care, tech gain; Nvidia earnings loom

Introduction & Market Context

Pacific Premier Bancorp, Inc. (NASDAQ:PPBI) released its second quarter 2025 financial results on July 24, showing modest improvement in key metrics despite merger-related expenses. The presentation comes as Columbia Banking System (NASDAQ:COLB) plans to acquire Pacific Premier, a development that has influenced market perception of both companies.

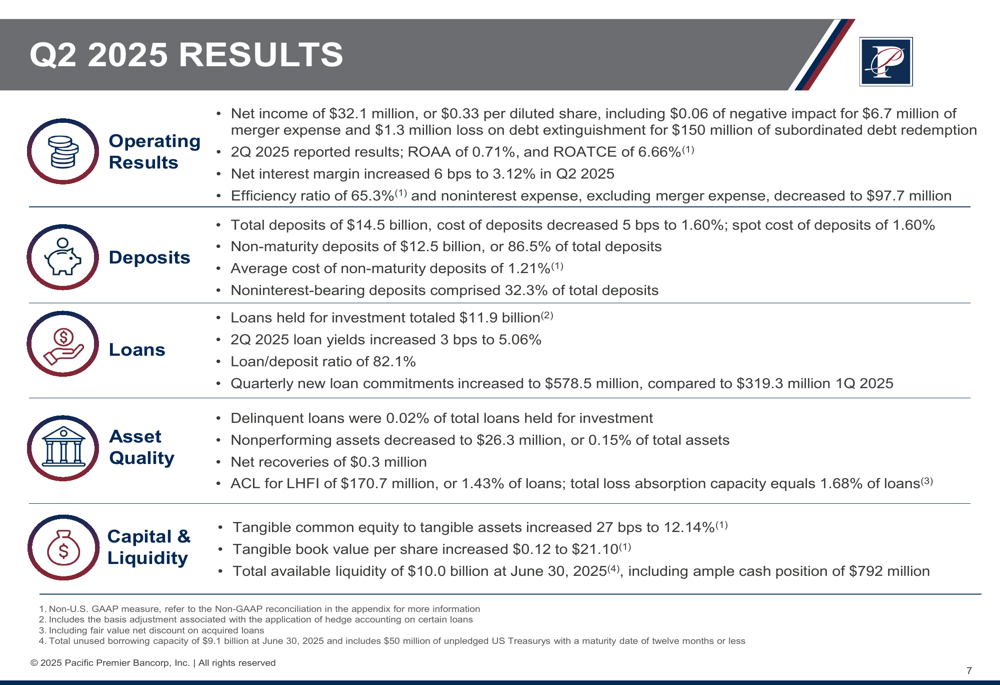

Pacific Premier reported net income of $32.1 million, or $0.33 per diluted share, which included a $0.06 negative impact from $6.7 million in merger expenses and a $1.3 million loss on debt extinguishment related to the redemption of $150 million in subordinated debt. The bank’s stock recently traded at $21.67, down 2.26% according to latest market data, though it had seen a 2.03% increase following Columbia Banking System’s strong Q1 2025 earnings announcement.

Quarterly Performance Highlights

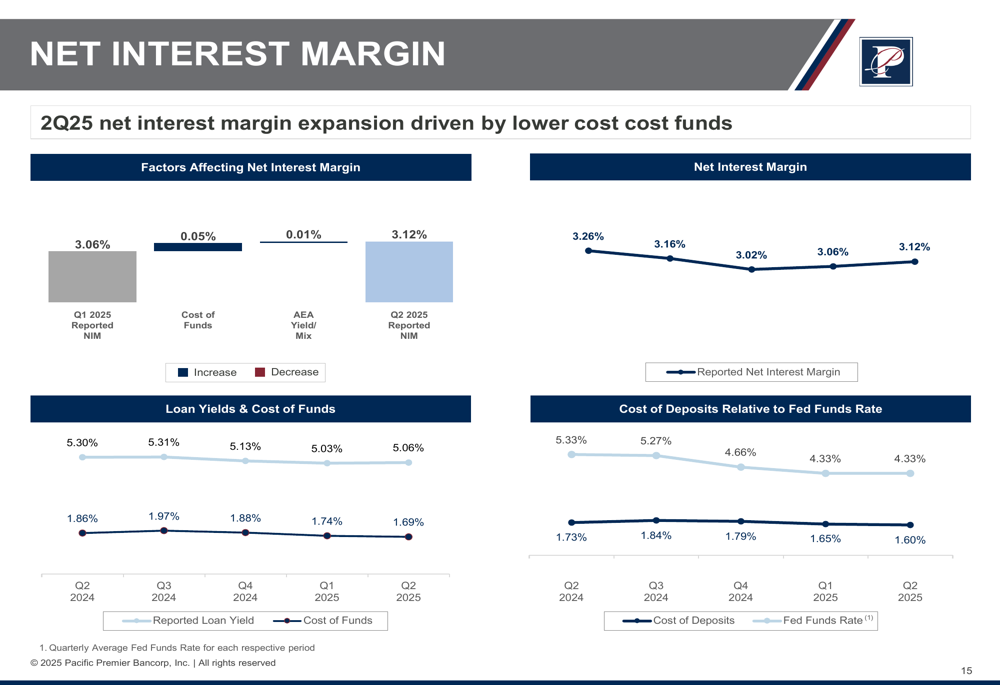

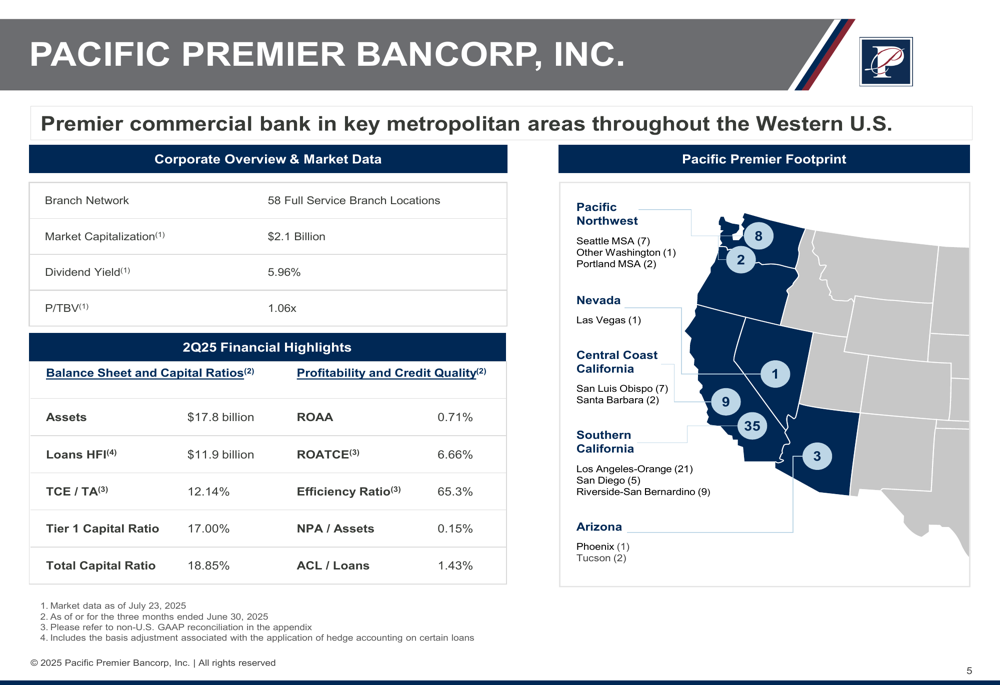

Pacific Premier demonstrated improved profitability metrics in Q2 2025, with return on average assets (ROAA) of 0.71% and return on average tangible common equity (ROATCE) of 6.66%. Notably, the bank’s net interest margin increased 6 basis points to 3.12%, reversing previous compression trends.

As shown in the following chart detailing net interest margin trends, the improvement was primarily driven by lower funding costs:

The bank’s efficiency ratio stood at 65.3% for the quarter, with noninterest expense (excluding merger expenses) decreasing to $97.7 million. Loan yields increased 3 basis points to 5.06%, while the cost of deposits decreased 5 basis points to 1.60%, contributing to margin expansion.

The following comprehensive overview illustrates Pacific Premier’s Q2 2025 performance across key metrics:

Balance Sheet Strength

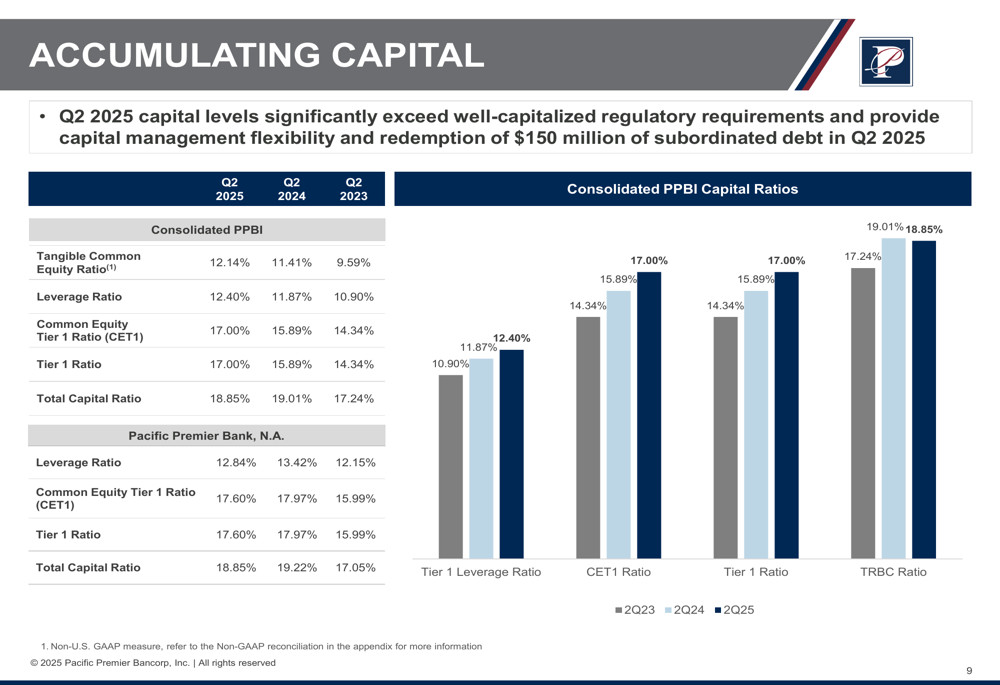

Pacific Premier maintained a strong capital position, with tangible common equity to tangible assets increasing 27 basis points to 12.14% and tangible book value per share rising $0.12 to $21.10. The bank’s capital ratios significantly exceed regulatory requirements, providing flexibility for the pending Columbia acquisition.

The following chart shows the bank’s improving capital position over time:

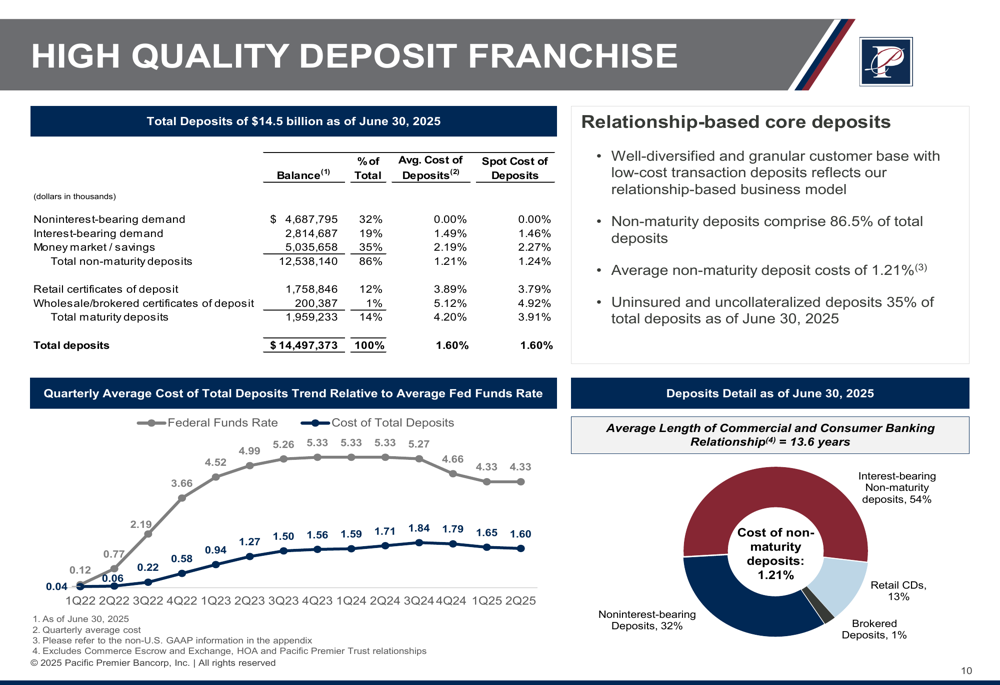

Total (EPA:TTEF) deposits stood at $14.5 billion as of June 30, 2025, with non-maturity deposits comprising 86.5% of the total. Noninterest-bearing deposits represented 32.3% of total deposits, contributing to the bank’s relatively low overall funding costs.

The deposit franchise details are illustrated in this breakdown:

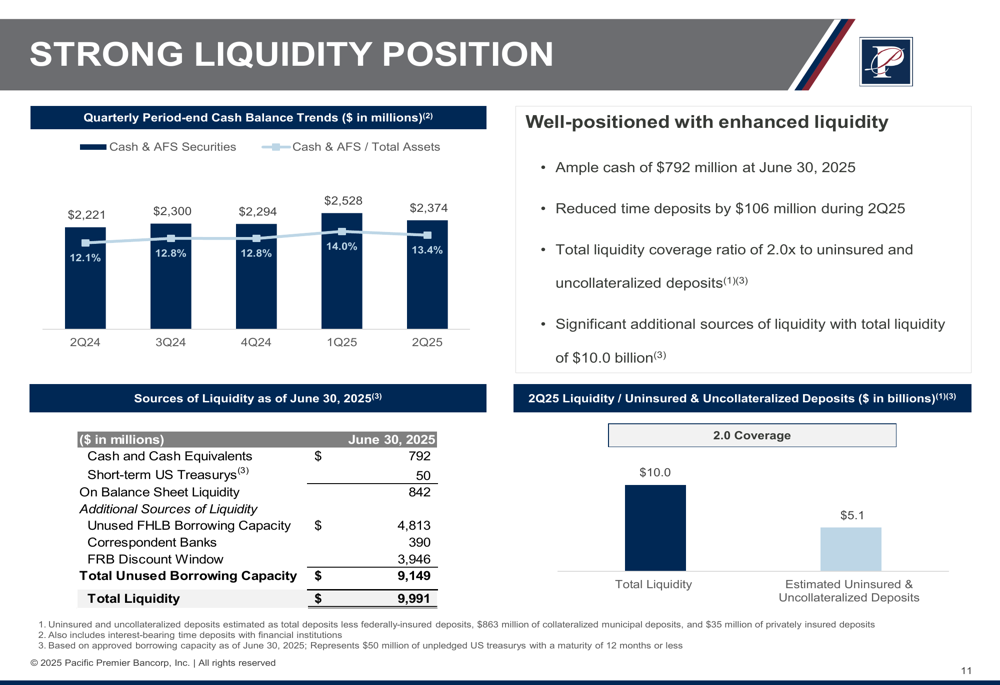

Pacific Premier maintained a strong liquidity position with total available liquidity of $10.0 billion at quarter-end, including $792 million in cash. The bank’s liquidity coverage ratio was 2.0x uninsured and uncollateralized deposits, providing substantial buffer against potential funding pressures.

The following chart details the bank’s liquidity sources and position:

Loan Portfolio Quality

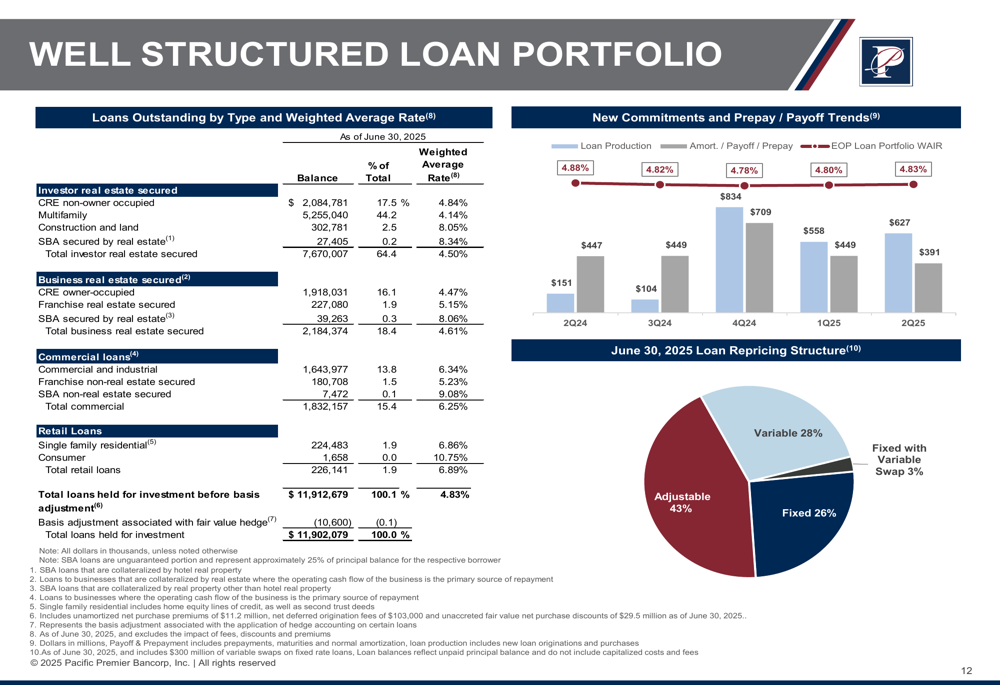

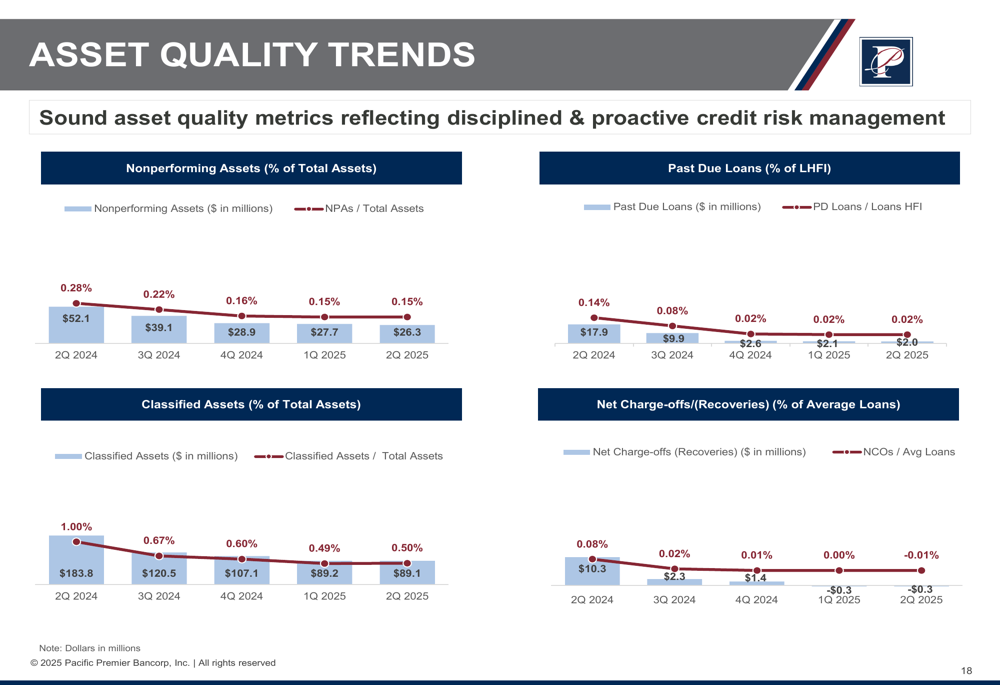

Total loans held for investment reached $11.9 billion, with multifamily loans representing 44.2% of the portfolio. The bank reported strong asset quality metrics, with nonperforming assets decreasing to $26.3 million, or just 0.15% of total assets. Delinquent loans remained minimal at 0.02% of total loans, and the bank recorded net recoveries of $0.3 million for the quarter.

The loan portfolio composition is detailed in the following breakdown:

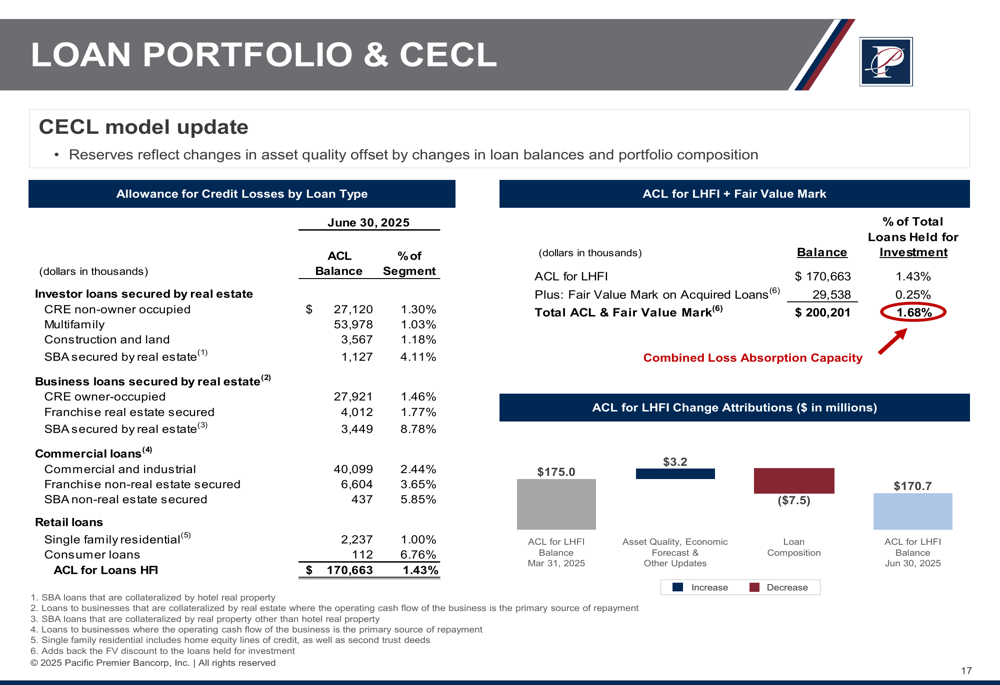

Pacific Premier maintained an allowance for credit losses of $170.7 million, representing 1.43% of loans held for investment. When including fair value marks on acquired loans, the total loss absorption capacity equaled 1.68% of loans.

The following chart provides details on the allowance for credit losses by loan segment:

Asset quality trends have shown consistent improvement over recent quarters, as illustrated in the following charts:

Strategic Positioning

While Pacific Premier’s presentation did not directly address the pending acquisition by Columbia Banking System, the bank’s strong financial position appears to support Columbia’s strategic rationale for the merger. According to Columbia’s Q1 2025 earnings report, the acquisition is expected to provide significant benefits, including $127 million in pretax cost savings and EPS accretion of 14% in 2026 and 15% in 2027.

Pacific Premier’s extensive branch network of 58 locations across the Western United States, particularly in Southern California, aligns with Columbia’s stated goal of expanding its physical footprint in these markets. As Columbia’s CEO Clint Stein noted, "This acquisition provides the physical footprint to support our Southern California banking teams."

The bank’s corporate overview highlights its geographic presence:

Pacific Premier’s quarterly loan commitment volume increased to $578.5 million in Q2 2025, compared to $319.3 million in the previous quarter, suggesting improved lending momentum heading into the merger. This growth, combined with the bank’s strong capital and liquidity positions, positions Pacific Premier as an attractive acquisition target despite the integration risks that typically accompany bank mergers.

According to the earnings article, analysts have recently revised their earnings estimates upward for Pacific Premier, with price targets ranging from $23 to $31, suggesting potential upside from current trading levels. The acquisition is expected to receive regulatory approval in the second half of 2025, subject to standard closing conditions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.