Oil prices hold sharp losses with focus on secondary India tariffs

Introduction & Market Context

Pacira BioSciences (NASDAQ:PCRX) recently presented its Q1 2025 earnings results, highlighting progress on its strategic initiatives despite mixed financial performance. The company’s stock has shown resilience with a 44% gain over the past six months, though it experienced a 4.76% decline following the earnings announcement due to revenue falling short of analyst expectations.

The presentation emphasized Pacira’s 5x30 growth strategy and significant patent litigation settlement for EXPAREL, which establishes exclusivity through 2039. This comes as the company positions itself as a leader in non-opioid pain management solutions in a market where nearly one in four Americans suffers from chronic pain.

Quarterly Performance Highlights

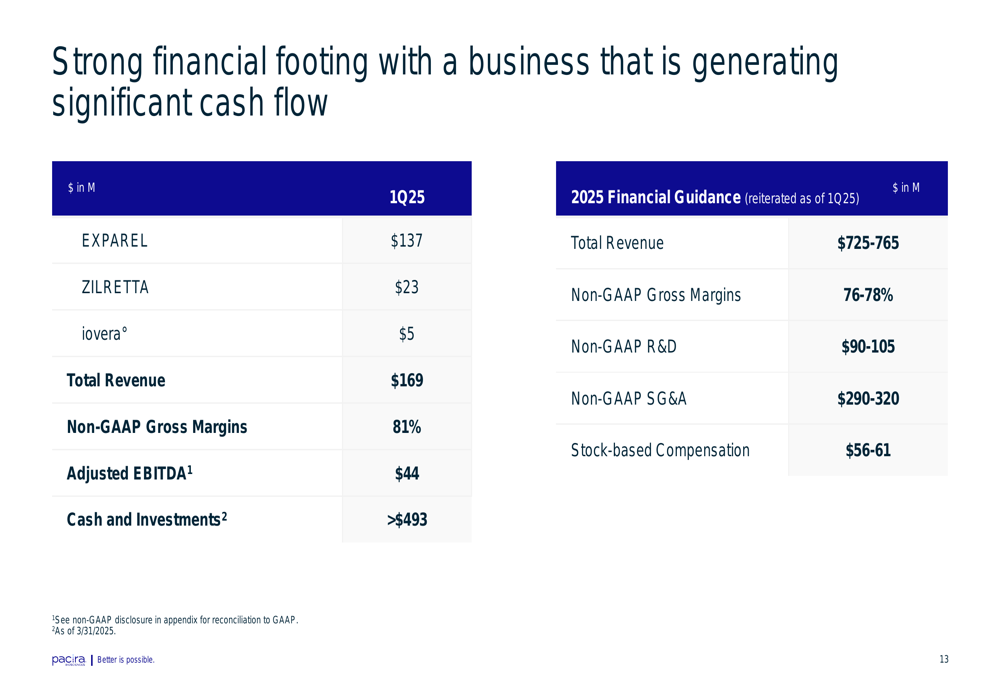

Pacira reported total revenue of $169 million for Q1 2025, though the earnings release showed actual revenue of $164.9 million, missing analyst expectations of $175.6 million. This discrepancy appears to be due to rounding or adjustments in the presentation figures.

The company highlighted strong performance in several key metrics:

As shown in the following financial performance summary:

EXPAREL, Pacira’s flagship product, generated $137 million in revenue (reported as $136.5 million in earnings release), with average daily sales up approximately 7% year-over-year. ZILRETTA contributed $23 million, while iovera added $5 million to the total.

Particularly noteworthy was the non-GAAP gross margin of 81%, representing a significant improvement from 72% in the same period last year. This margin enhancement was partly attributed to a favorable court ruling that eliminated the RDF royalty obligation, providing a low-single-digit percentage benefit to EXPAREL gross margins.

Strategic Initiatives

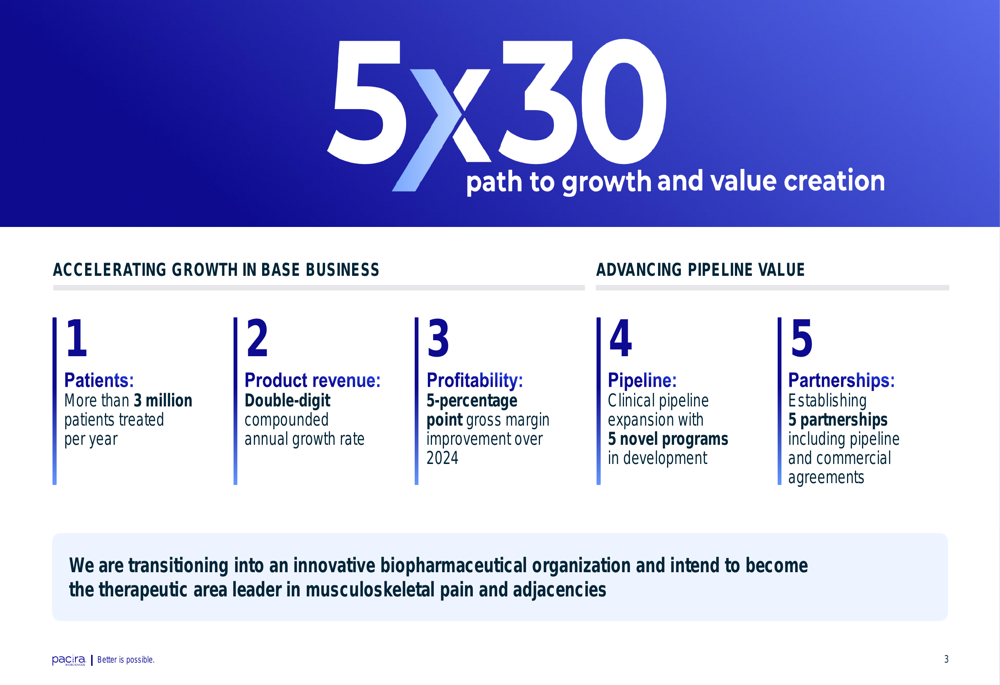

Central to Pacira’s presentation was its 5x30 growth strategy, which outlines five key areas of focus with quantitative targets:

As illustrated in the company’s strategic framework:

The strategy aims to treat more than 3 million patients annually, achieve double-digit compound annual growth in product revenue, improve gross margins by 5 percentage points over 2024 levels, expand the clinical pipeline with five novel programs, and establish five strategic partnerships.

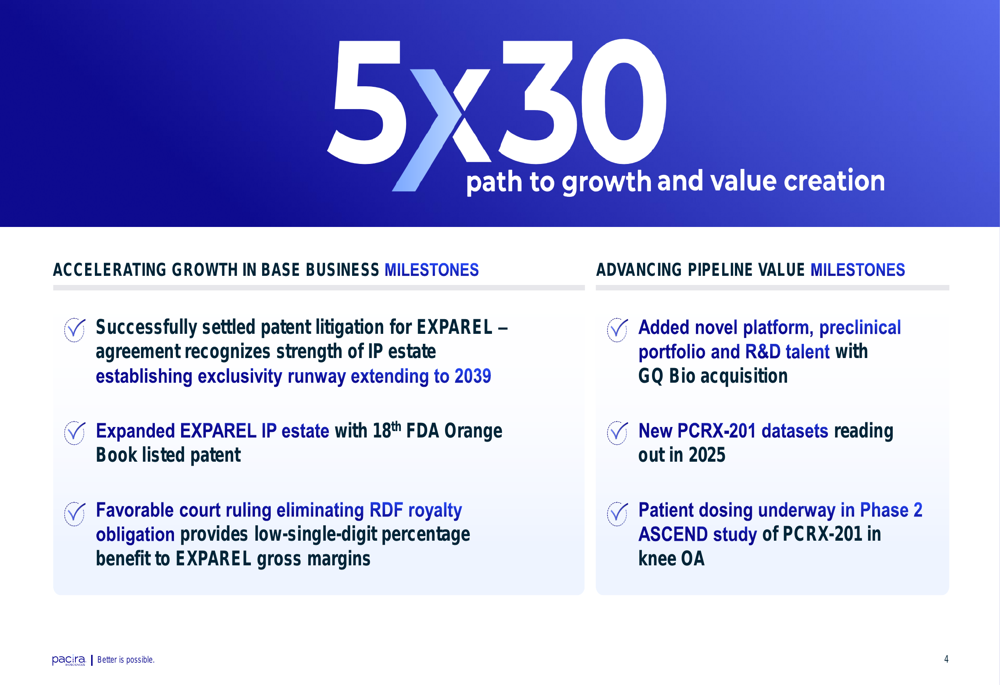

Pacira has already made significant progress on these initiatives, as shown in their milestone achievements:

A major win for the company was the successful settlement of patent litigation for EXPAREL, which establishes exclusivity extending to 2039. This settlement is volume-limited with no pricing restrictions, royalties, or technology transfer requirements, giving Pacira significant flexibility in its market approach.

Product Portfolio and Growth Drivers

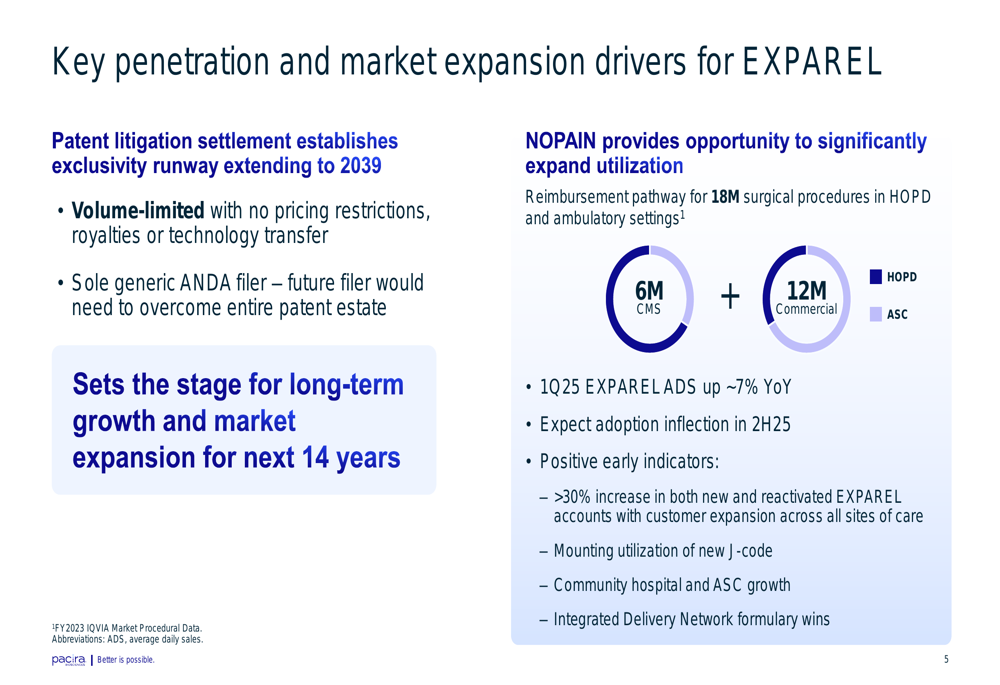

Pacira’s presentation highlighted several growth drivers for its key products. For EXPAREL, the NOPAIN Act represents a significant opportunity, providing a reimbursement pathway for approximately 18 million surgical procedures.

The company detailed its market expansion strategy as follows:

Early indicators of adoption include an increase in EXPAREL accounts, mounting utilization of a new J-code, community hospital and ASC growth, and integrated delivery network formulary wins. Management expects an adoption inflection in the second half of 2025.

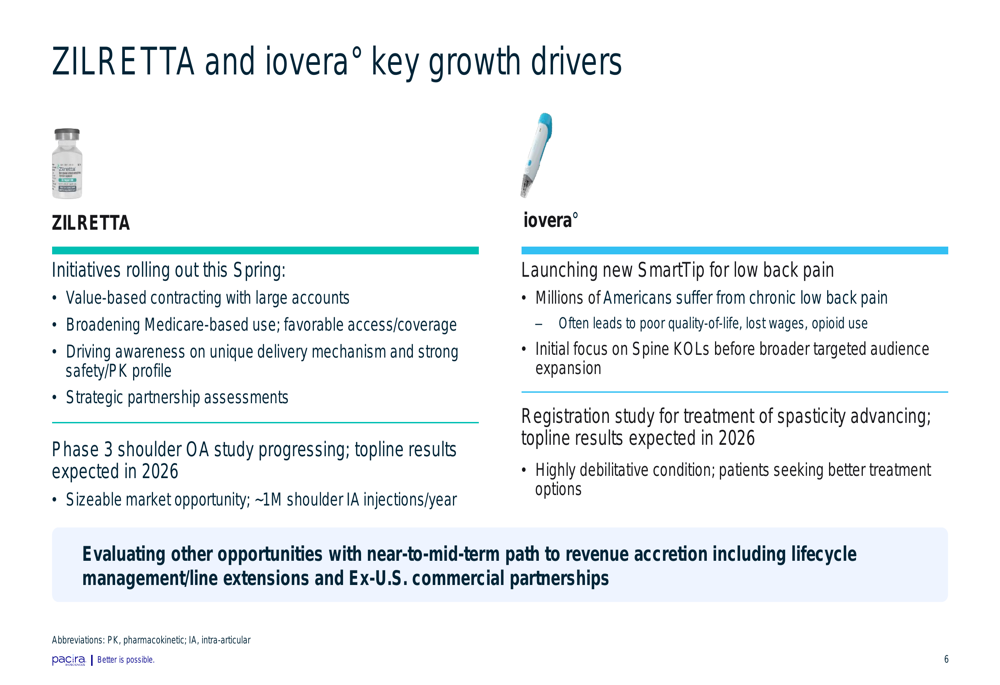

For ZILRETTA and iovera, Pacira outlined specific growth initiatives:

ZILRETTA initiatives include value-based contracting with large accounts, broadening Medicare-based use, and driving awareness of its unique delivery mechanism. A Phase 3 shoulder osteoarthritis study is progressing with topline results expected in 2026.

For iovera, the company is launching a new SmartTip for low back pain, initially focusing on spine key opinion leaders, and advancing a registration study for treatment of spasticity with results expected in 2026.

Pipeline Development

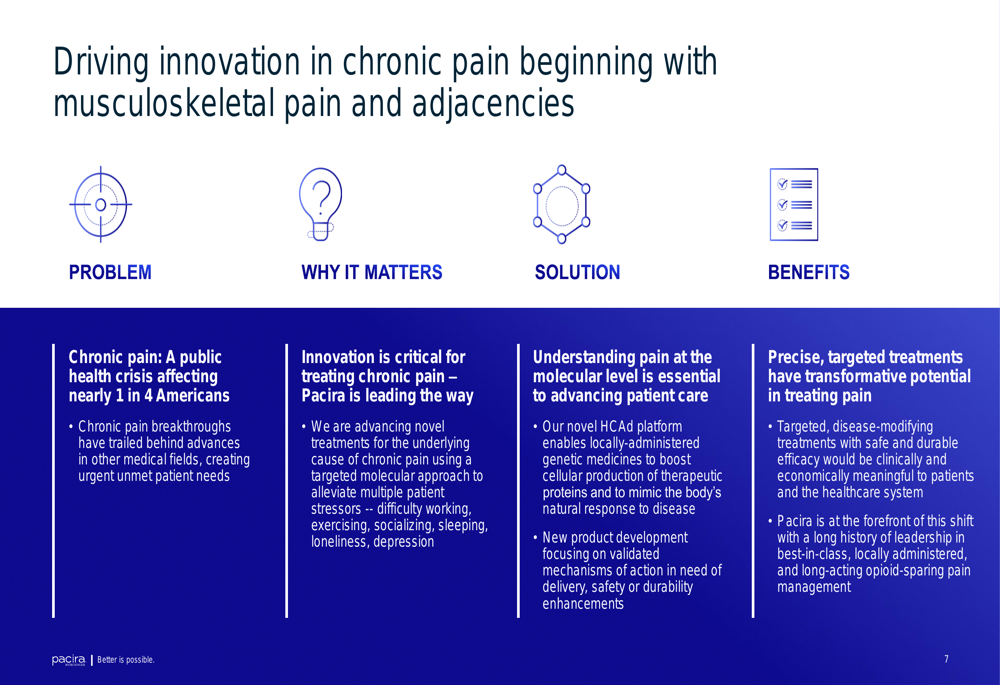

Pacira emphasized its commitment to innovation in chronic pain management, positioning itself at the forefront of treating this public health crisis:

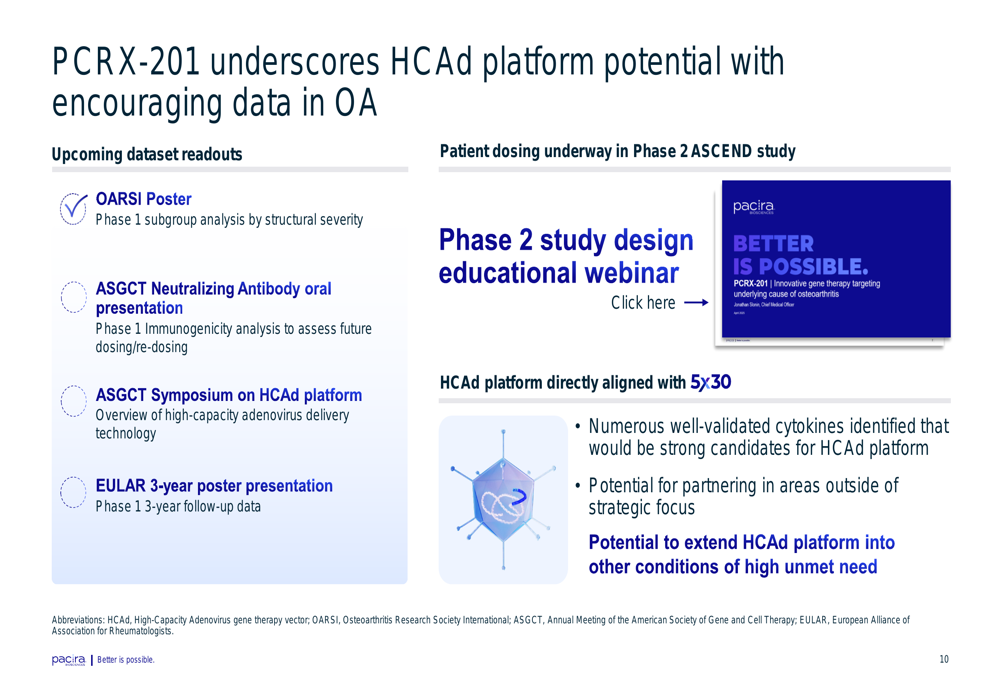

The company’s pipeline is anchored by PCRX-201, a gene therapy candidate for knee osteoarthritis that delivers IL-1Ra to block the IL-1 pathway, potentially slowing inflammation-associated joint degradation and reducing pain.

The presentation highlighted the potential of the HCAd platform:

Upcoming data readouts for PCRX-201 include presentations at major medical conferences. The HCAd platform offers several advantages, including smaller doses to achieve desired effects, locally sustained delivery with redosing potential, and a favorable cost of goods profile.

Financial Outlook and Guidance

For 2025, Pacira provided the following financial guidance:

- Total (EPA:TTEF) revenue: $725-765 million

- Non-GAAP gross margins: 76-78%

- Non-GAAP R&D: $90-105 million

- Non-GAAP SG&A: $290-320 million

- Stock-based compensation: $56-61 million

The company also outlined its capital allocation strategy, focused on three key areas:

Pacira emphasized its disciplined approach to capital allocation, aiming to drive shareholder value by accelerating growth in its base business, advancing its innovative pipeline, and opportunistically returning capital to shareholders through a recently authorized $300 million share repurchase program.

Conclusion

Pacira’s Q1 2025 presentation portrayed a company in transition, with strong strategic positioning despite mixed financial results. The EXPAREL patent settlement through 2039 provides a long runway for growth, while the 5x30 strategy offers a clear roadmap for expansion.

However, investors should note the discrepancy between the presentation’s revenue figures and the actual reported results, which fell short of analyst expectations. This gap, along with declining ZILRETTA sales, contributed to the negative market reaction following the earnings announcement.

Looking ahead, Pacira’s success will depend on effectively executing its strategic initiatives, particularly the market expansion for EXPAREL through the NOPAIN Act and advancing its pipeline candidates like PCRX-201. The company’s strong gross margins and disciplined capital allocation approach provide a solid foundation, but revenue growth will be critical to maintaining investor confidence.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.