US stock futures inch lower after Wall St marks fresh records on tech gains

Palo Alto Networks Inc (NASDAQ:PANW) released its third-quarter fiscal year 2025 results on May 20, showing robust performance across key metrics despite a negative aftermarket stock reaction. The cybersecurity leader reported 15% year-over-year revenue growth and a significant milestone in its Next-Generation Security (NGS) business.

Quarterly Performance Highlights

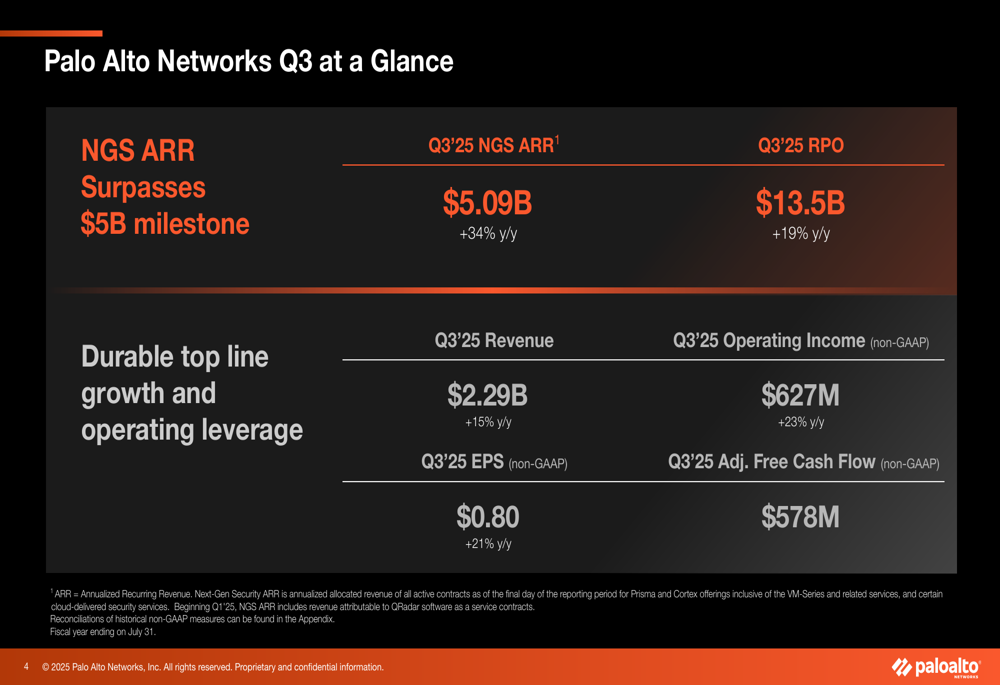

Palo Alto Networks delivered strong financial results for Q3 FY2025, meeting or exceeding guidance across all metrics. Revenue reached $2.29 billion, representing 15% year-over-year growth and hitting the high end of the company’s guidance range. Non-GAAP earnings per share came in at $0.80, a 21% increase year-over-year and above the guided range of $0.76-$0.77.

As shown in the following comprehensive overview of Q3 results:

A significant milestone was achieved as NGS Annual Recurring Revenue (ARR) surpassed $5 billion, reaching $5.09 billion with 34% year-over-year growth. Remaining Performance Obligation (RPO) grew to $13.5 billion, up 19% year-over-year, while non-GAAP operating income increased 23% to $627 million. The company also generated $578 million in adjusted free cash flow.

The detailed financial performance over the past five quarters shows consistent growth trends:

Despite these strong results, Palo Alto Networks’ stock fell approximately 4.27% in aftermarket trading to $186.17, suggesting investors may have had even higher expectations or concerns about specific aspects of the company’s outlook.

Strategic Initiatives

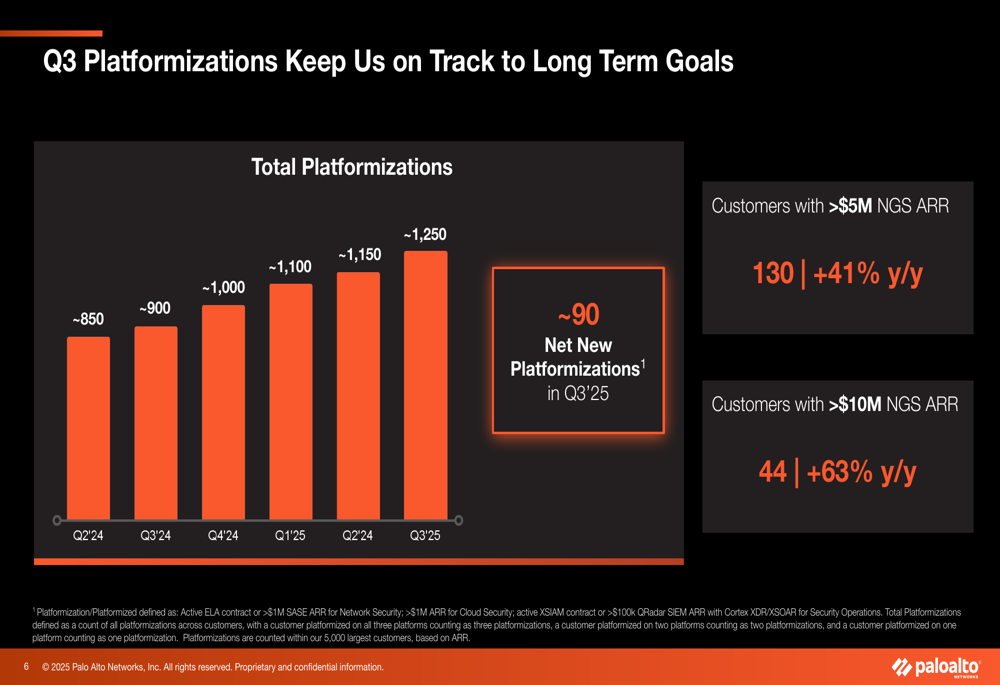

Palo Alto Networks continued to make progress on its platformization strategy, which aims to consolidate customers’ security spending across its three main platforms: Network Security, Cloud Security, and Security Operations. The company reported approximately 1,250 total platformizations in Q3, with around 90 net new additions.

The platformization strategy is showing particular strength at the high end of the market, with 130 customers generating over $5 million in NGS ARR (up 41% year-over-year) and 44 customers with over $10 million in NGS ARR (up 63% year-over-year).

As illustrated in the following chart showing the platformization progress:

CEO Nikesh Arora highlighted several large deals that demonstrate the success of this strategy, including a $90 million deal with a global consulting firm that platformized on XSIAM after already using Network Security solutions, and a $46 million deal with a US financial services firm that consolidated both Network Security and Cortex products.

AI-Driven Security Solutions

The company emphasized the growing importance of AI in cybersecurity, both as a driver of demand and as a technology embedded in its products. Palo Alto Networks reported approximately $400 million in AI-related ARR in Q3 FY2025.

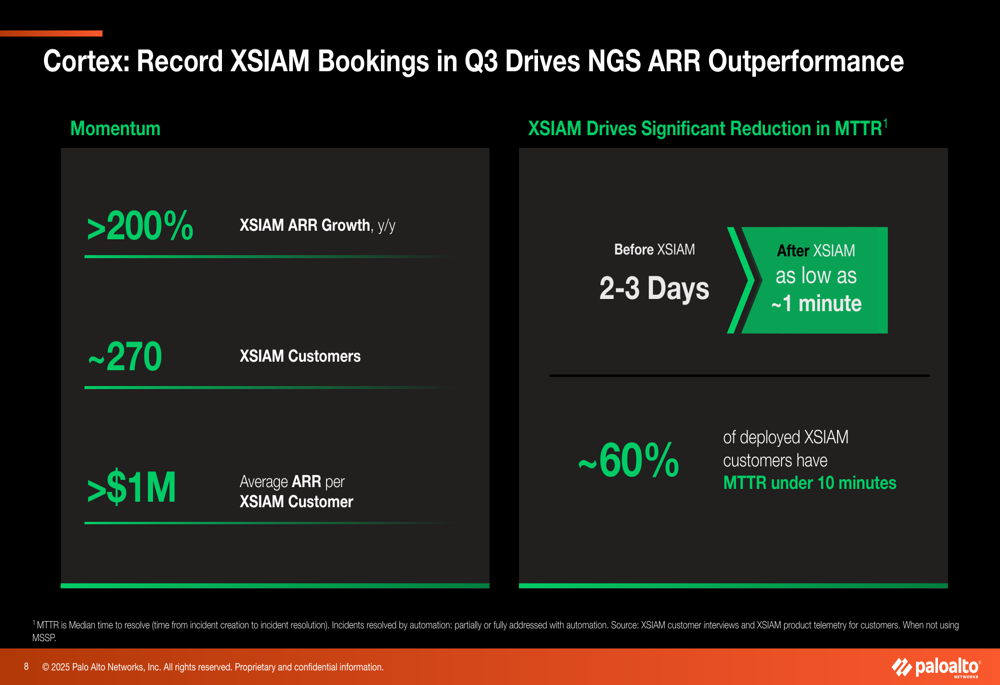

Cortex XSIAM, the company’s AI-powered security operations platform, showed particularly strong performance with over 200% ARR growth year-over-year and approximately 270 customers. The platform has demonstrated significant operational improvements for customers, reducing median time to resolve security incidents from 2-3 days to as low as one minute in some cases.

As shown in the following metrics highlighting XSIAM’s performance:

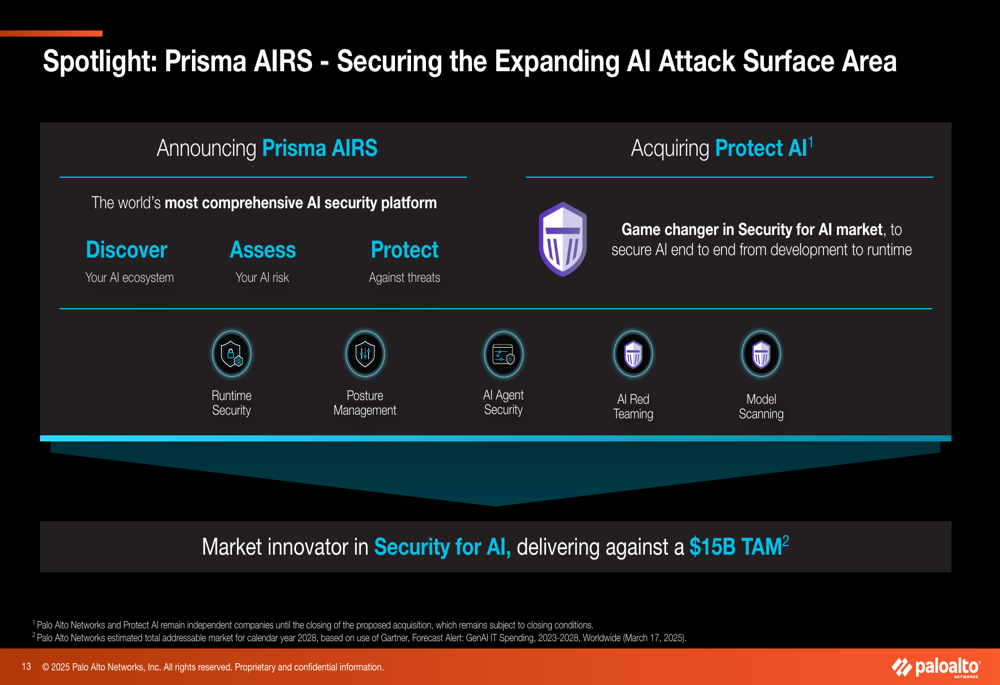

The company also announced a new AI security initiative with the introduction of Prisma AIRS (AI Risk Security), described as "the world’s most comprehensive AI security platform." Additionally, Palo Alto Networks announced the acquisition of Protect AI, which it characterized as a "game changer in Security for AI market."

The following slide illustrates the company’s strategy for securing AI systems:

Network Security Performance

Palo Alto Networks’ traditional network security business continued to evolve toward software-based solutions. Software (ETR:SOWGn) firewalls showed approximately 20% ARR growth year-over-year, with about 70% of software firewall ARR deployed in public cloud environments.

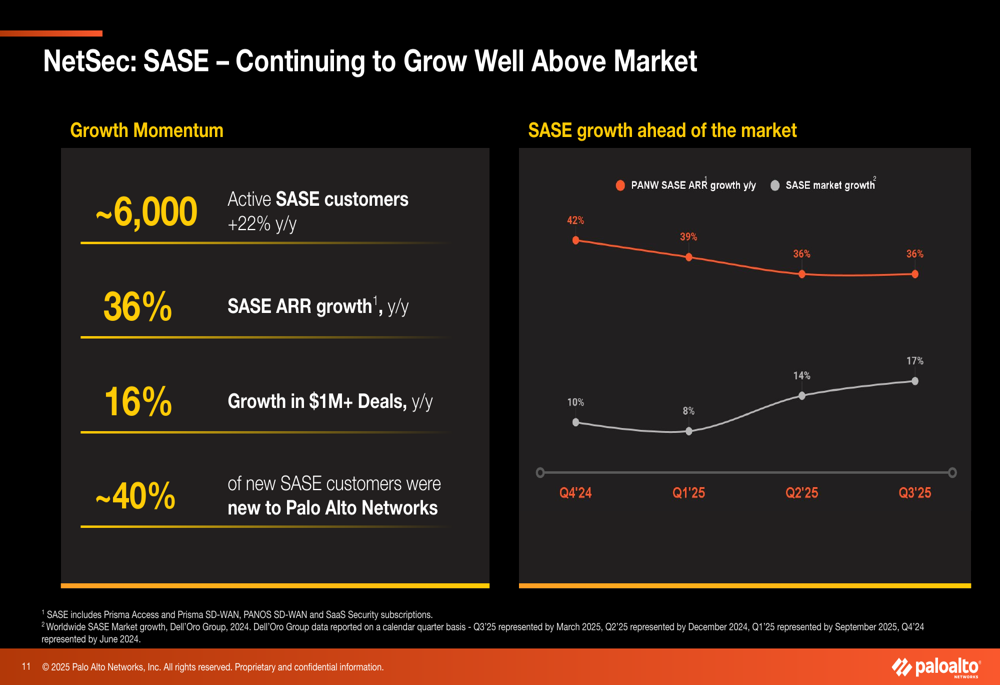

The company’s Secure Access Service Edge (SASE) offerings demonstrated strong momentum with 36% ARR growth year-over-year, significantly outpacing the overall market growth of 17%. Palo Alto Networks now has approximately 6,000 active SASE customers, a 22% increase year-over-year.

As illustrated in the following comparison of SASE growth versus the market:

The Prisma Access Browser, which the company positions as "the future OS of the AI-driven enterprise," has sold approximately 3 million licenses, representing 11x year-over-year growth.

Forward-Looking Statements

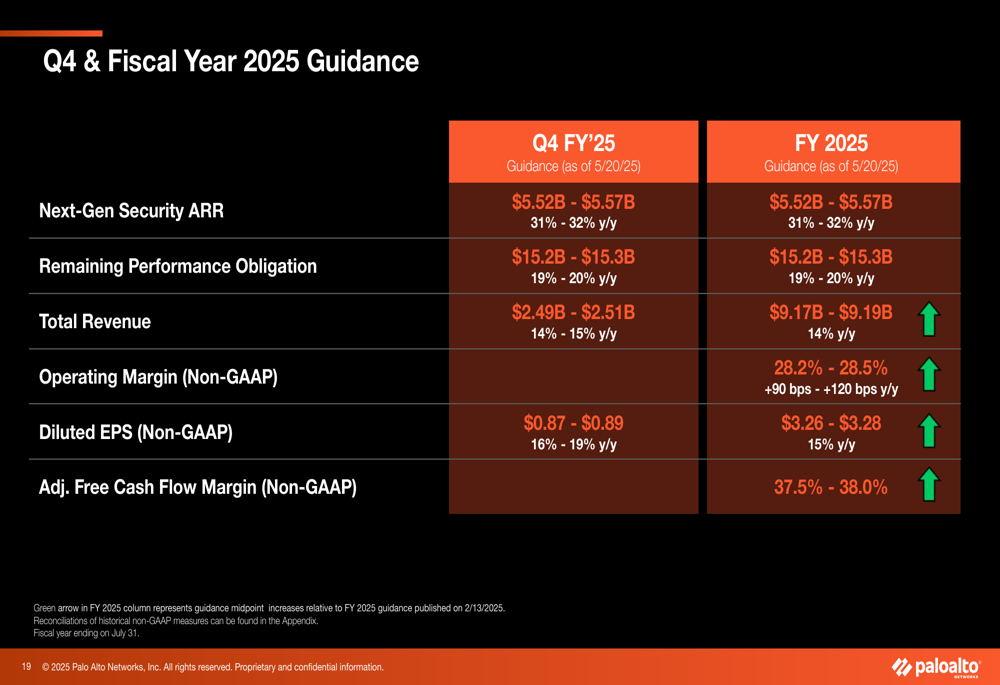

For the fourth quarter of fiscal year 2025, Palo Alto Networks expects revenue between $2.49 billion and $2.51 billion (14-15% year-over-year growth) and non-GAAP earnings per share between $0.87 and $0.89 (16-19% year-over-year growth).

For the full fiscal year 2025, the company guided for revenue of $9.17-$9.19 billion (14% year-over-year growth) and non-GAAP earnings per share of $3.26-$3.28 (15% year-over-year growth). The company also raised guidance for NGS ARR to $5.52-$5.57 billion (31-32% year-over-year growth).

The following slide details the company’s updated guidance:

CFO Dipak Golechha noted that the company is seeing a shift in its net new NGS ARR mix toward new market offerings rather than advanced subscription upgrades, indicating expansion into new growth areas.

Market Context

Palo Alto Networks attributed the robust demand for cybersecurity to several factors, including AI transformation driving enterprise data architecture changes, the critical need to secure AI systems, rising vendor consolidation, and a heightened threat environment. The company specifically highlighted the emergence of "100x faster AI-powered ransomware attacks" as a driver of demand.

The company’s results and guidance suggest continued strong execution in a competitive cybersecurity landscape, with particular emphasis on positioning for the AI-driven future of enterprise security. Despite the aftermarket stock decline, Palo Alto Networks demonstrated solid financial performance and strategic progress in its third quarter.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.