US LNG exports surge but will buyers in China turn up?

Introduction & Market Context

Parker-Hannifin Corporation (NYSE:PH) reported its fourth quarter and full-year fiscal 2025 results on August 7, 2025, highlighting record margins and strong aerospace performance despite flat overall sales growth. The market responded positively to the results, with the stock trading up 3.28% to $720 in pre-market trading, according to available data.

The motion and control technologies company delivered impressive margin expansion across its segments, with aerospace systems emerging as the standout performer. This performance comes against a backdrop of mixed industrial market conditions, with the company’s strategic portfolio transformation toward longer-cycle businesses helping to offset shorter-cycle weakness.

Quarterly Performance Highlights

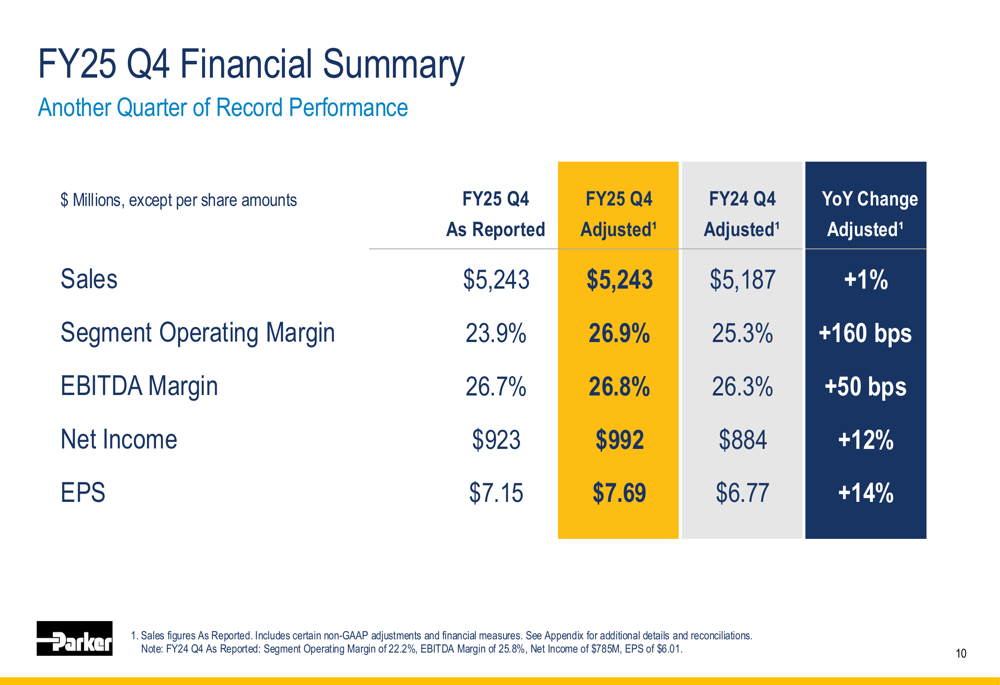

Parker-Hannifin reported fourth-quarter sales of $5.24 billion, representing a modest 1% increase compared to the same period last year. Despite the relatively flat sales growth, the company achieved significant margin improvement, with adjusted segment operating margin expanding 160 basis points to 26.9%.

As shown in the following financial summary, adjusted earnings per share grew 14% to $7.69, significantly outpacing sales growth and demonstrating the company’s operational efficiency:

The quarterly performance was driven by strong execution across segments, with particularly notable results in the aerospace business. Order rates showed encouraging trends, increasing 5% overall in the fourth quarter, suggesting potential growth momentum heading into fiscal 2026.

Segment Performance Analysis

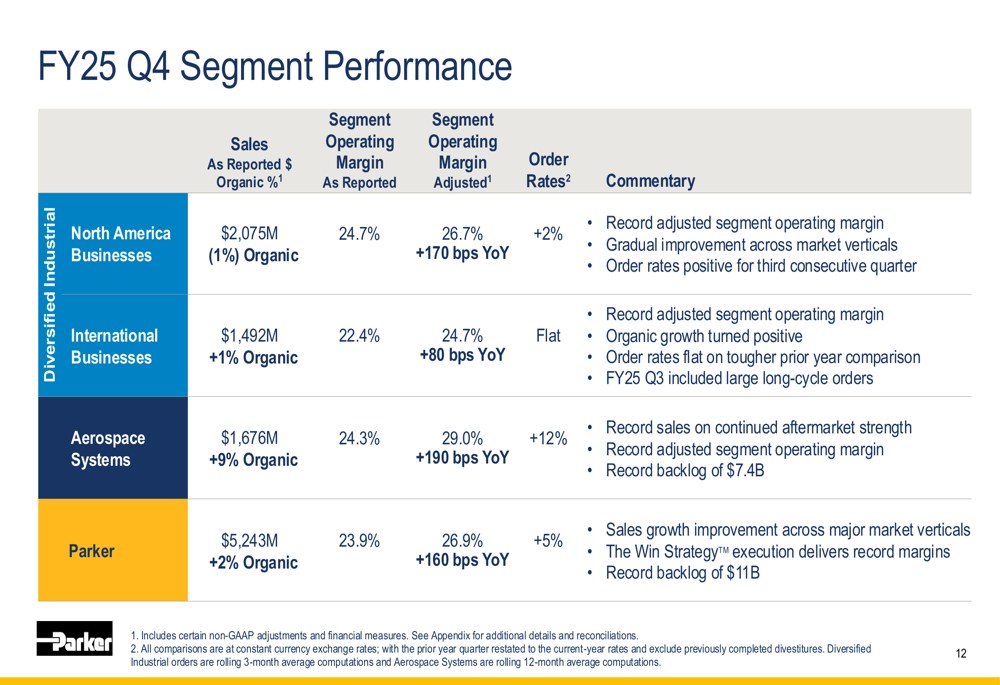

Parker-Hannifin’s segment performance revealed divergent trends between its aerospace and industrial businesses. The aerospace segment continued its exceptional performance with 9% organic growth, while the industrial segment showed mixed results with North America declining 1% organically.

The following segment breakdown illustrates these contrasting performances:

The aerospace systems segment was the clear standout, achieving an adjusted operating margin of 29.0%, an improvement of 190 basis points year-over-year. This exceptional margin performance, combined with 9% organic growth, underscores the strength of Parker’s aerospace portfolio.

Meanwhile, the industrial businesses demonstrated remarkable resilience in the face of challenging market conditions. Despite organic sales declines in North America, the segment achieved a 170 basis point margin improvement to 26.7%, highlighting the company’s ability to drive operational efficiencies regardless of top-line challenges.

Full-Year Fiscal 2025 Results

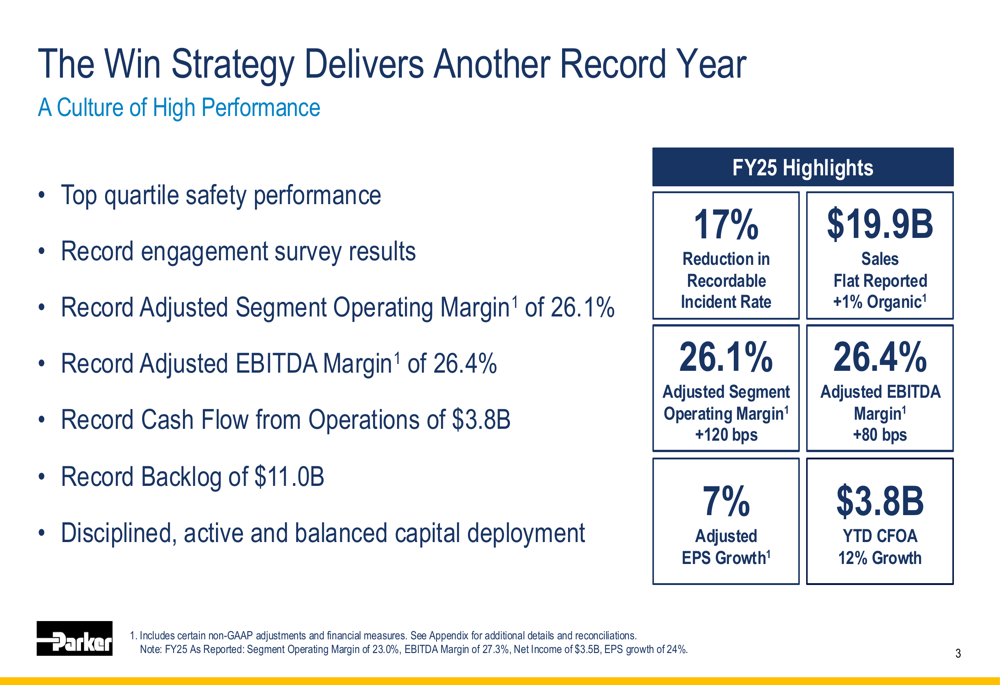

For the full fiscal year 2025, Parker-Hannifin delivered record results across multiple metrics despite relatively flat sales growth. The company reported sales of $19.9 billion, representing flat reported growth but a 1% increase on an organic basis.

As illustrated in the following slide, the company’s "Win Strategy" delivered record margins and cash flow performance:

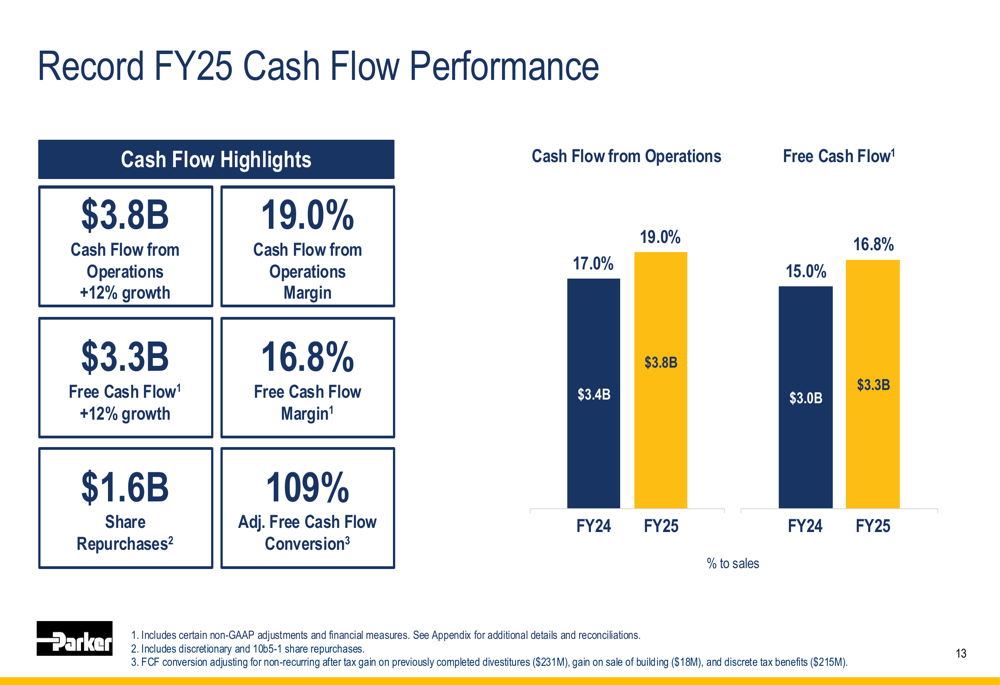

Particularly impressive was the company’s cash flow generation, with cash flow from operations reaching a record $3.8 billion, representing 19% of sales and a 12% increase compared to the previous year:

This strong cash flow performance enabled the company to return significant value to shareholders through $1.6 billion in share repurchases while maintaining financial flexibility for strategic investments.

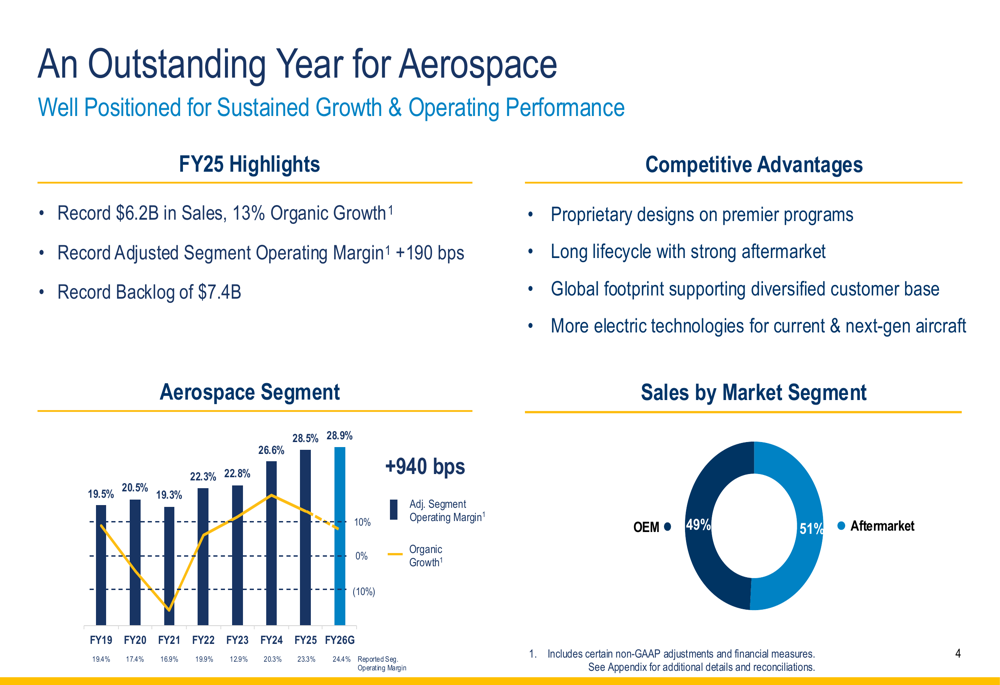

Aerospace Segment Success

The aerospace segment emerged as Parker-Hannifin’s crown jewel in fiscal 2025, delivering exceptional results across all key metrics. The segment achieved record sales of $6.2 billion, representing 13% organic growth, along with record operating margins and backlog.

The following chart illustrates the segment’s impressive margin trajectory, which has expanded from 16.9% in fiscal 2019 to 28.5% in fiscal 2025:

The aerospace segment benefits from several competitive advantages, including proprietary designs, long product lifecycles, and increasing content in more electric technologies. The balanced revenue mix between OEM (49%) and aftermarket (51%) provides both growth opportunities and stability.

This exceptional performance in aerospace helped offset challenges in the industrial segments and positions Parker-Hannifin well for continued growth in this high-margin business.

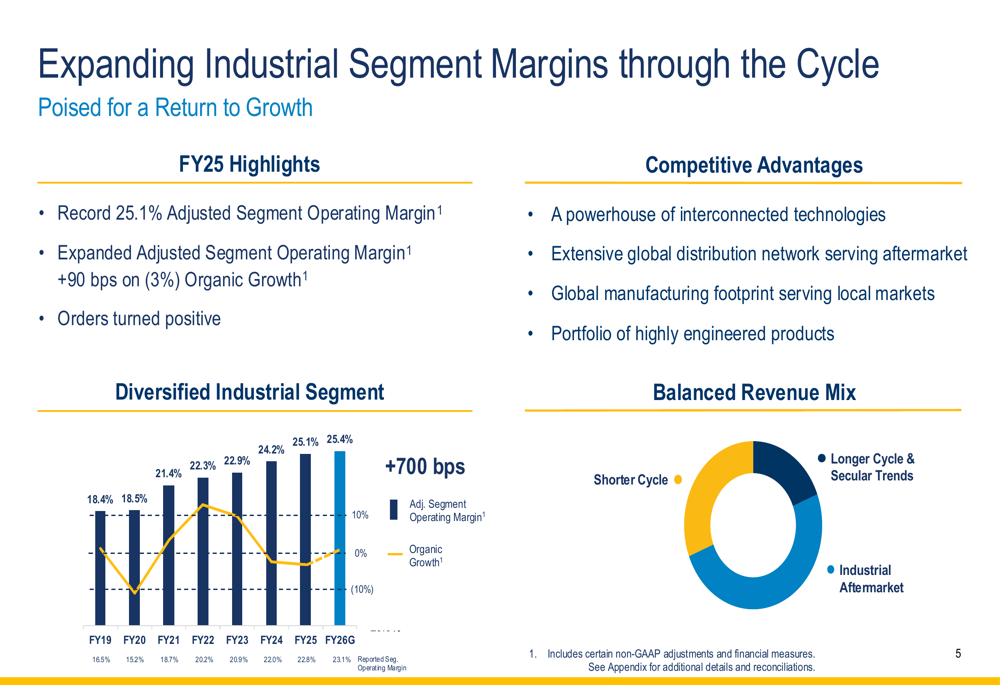

Industrial Segment Resilience

Despite facing headwinds with a 3% organic sales decline, Parker-Hannifin’s industrial segment demonstrated remarkable resilience by expanding adjusted operating margins by 90 basis points to a record 25.1%.

As shown in the following slide, the industrial segment has consistently expanded margins through economic cycles:

The company’s diversified industrial portfolio, extensive global distribution network, and focus on highly engineered products have enabled it to weather market fluctuations while continuing to improve profitability. The positive order trends reported in the fourth quarter suggest potential stabilization in industrial markets.

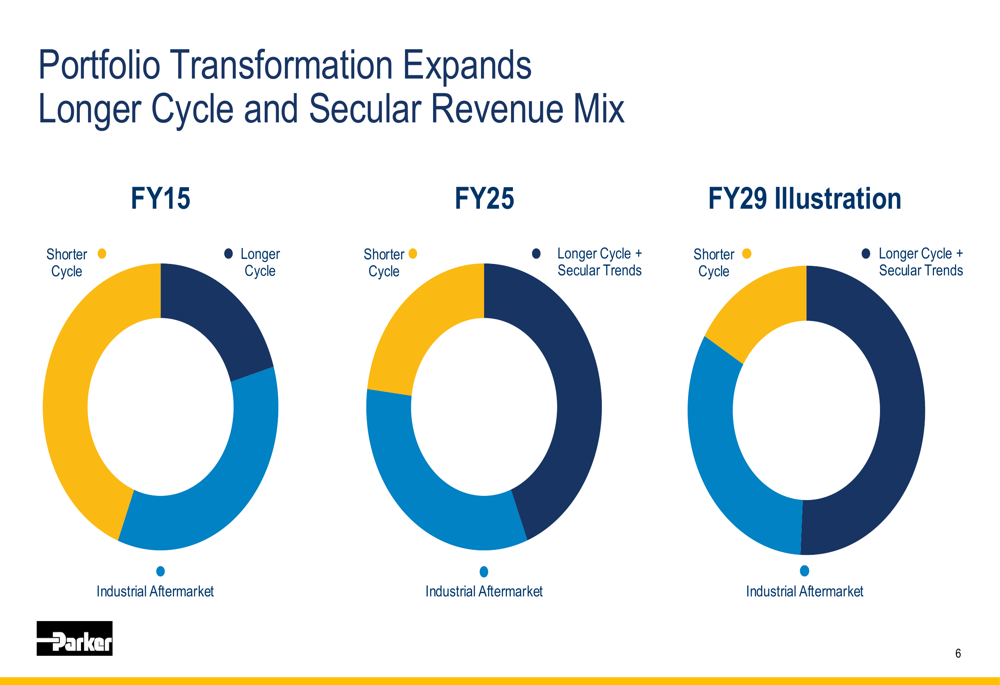

Strategic Initiatives

Parker-Hannifin continues to execute on its strategic portfolio transformation, shifting toward longer-cycle businesses and secular growth trends. This transformation is illustrated in the following chart, showing the evolution from fiscal 2015 to projected fiscal 2029:

A key element of this strategy is the recently announced acquisition of Curtis Instruments, which expands Parker’s electrification capabilities. Curtis is a leader in low voltage motor control solutions with applications across material handling, construction, and aerial work platforms:

This acquisition aligns with Parker’s long-term electrification strategy and adds complementary control solutions to its portfolio, positioning the company to capitalize on the growing electrification trend across multiple industries.

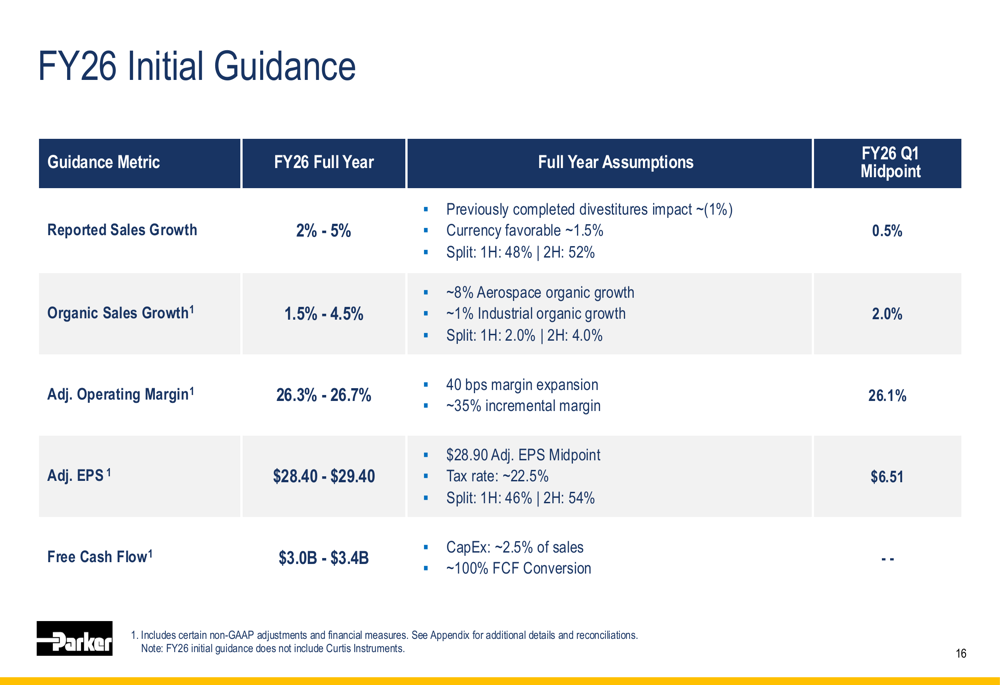

Fiscal 2026 Outlook

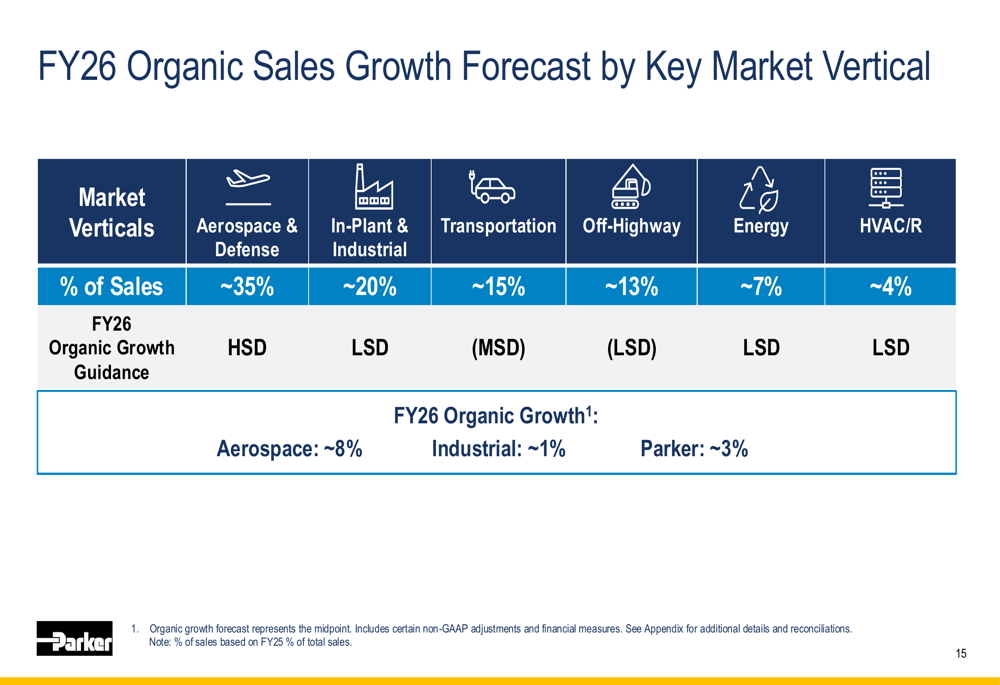

Looking ahead to fiscal 2026, Parker-Hannifin provided an optimistic outlook with continued margin expansion despite mixed organic growth expectations. The company projects reported sales growth of 2-5% and organic sales growth of 1.5-4.5%.

The following slide details the company’s initial guidance for fiscal 2026:

By market vertical, the company expects aerospace and defense to remain the strongest performer with high single-digit organic growth, while other segments show more modest growth or slight declines:

Notably, the company’s first-quarter fiscal 2026 results, which were released after this presentation, showed some variance from these projections. According to the earnings article, actual Q1 EPS came in at $6.94, exceeding the $6.51 midpoint guidance, while revenue slightly missed expectations at $4.96 billion with a 2% year-over-year decline versus the projected 0.5% growth.

The company also updated its aerospace growth forecast to 12% (higher than the original 8% projection) while lowering its industrial segment growth forecast to -3%, reflecting continued strength in aerospace and ongoing challenges in industrial markets.

Forward-Looking Statements

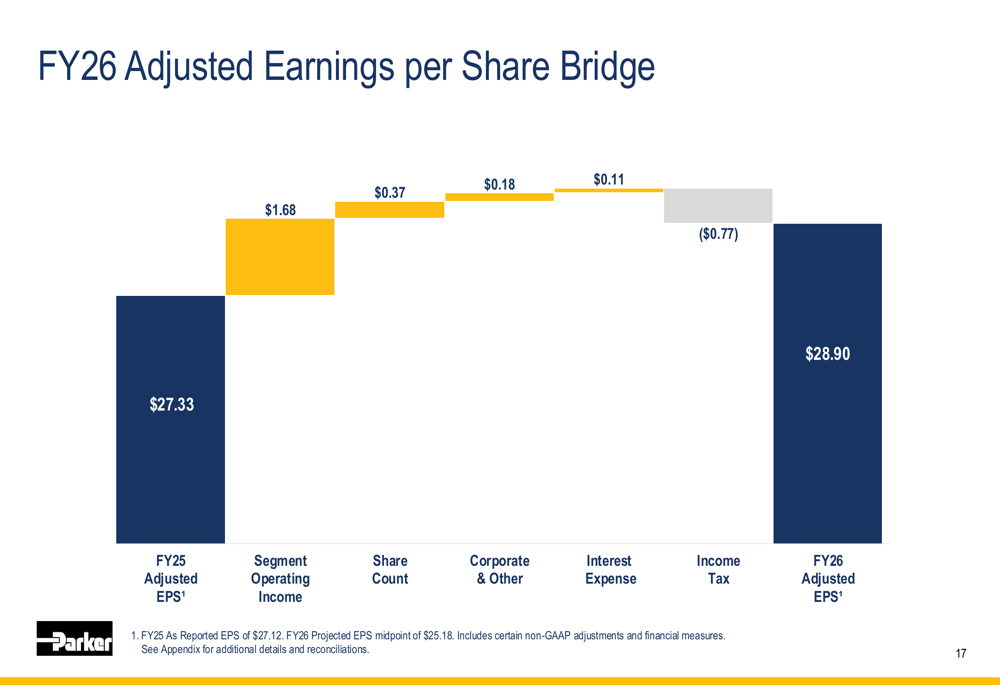

Parker-Hannifin expects continued margin expansion in fiscal 2026, with adjusted operating margin projected to reach 26.3-26.7%, representing approximately 40 basis points of improvement at the midpoint. Adjusted earnings per share is expected to grow to $28.40-$29.40.

The following earnings bridge illustrates the key drivers of projected EPS growth:

The company anticipates that segment operating income will be the primary driver of earnings growth, contributing $1.68 per share, with additional benefits from share count reduction and lower interest expense. These positive factors are partially offset by higher income taxes.

Free cash flow is projected to remain strong at $3.0-3.4 billion, with approximately 100% free cash flow conversion, providing continued flexibility for strategic investments and shareholder returns.

Conclusion

Parker-Hannifin’s fiscal 2025 results demonstrate the company’s ability to drive margin expansion and cash flow growth despite challenging market conditions in some segments. The exceptional performance of the aerospace business, combined with operational efficiency improvements across the portfolio, positions the company well for continued success in fiscal 2026.

The strategic portfolio transformation toward longer-cycle businesses and investments in electrification through acquisitions like Curtis Instruments align with key market trends and should support sustainable growth. While industrial markets remain challenging, the company’s demonstrated ability to expand margins regardless of top-line growth provides resilience.

With a record backlog of $11 billion and improving order rates, Parker-Hannifin appears well-positioned to deliver on its fiscal 2026 guidance, though investors should monitor the divergence between aerospace strength and industrial market conditions as the year progresses.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.