BitMine stock falls after CEO change and board appointments

Introduction & Market Context

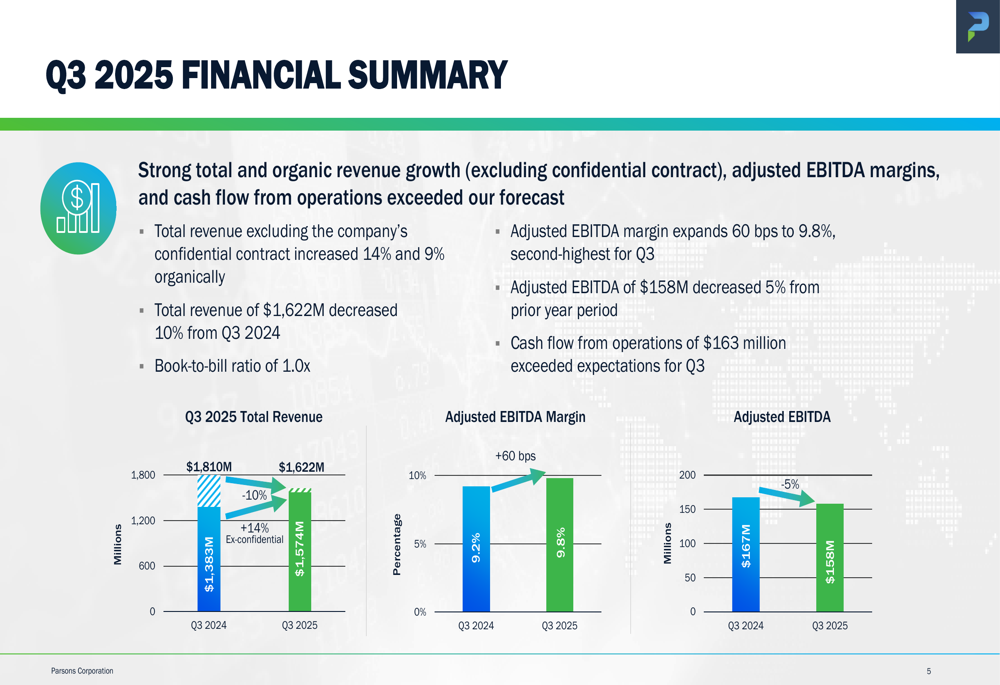

Parsons Corporation (NYSE:PSN) released its third-quarter 2025 earnings presentation on November 5, revealing a mixed performance that included an earnings beat but revenue shortfall. The engineering and defense contractor’s stock fell 5.22% in pre-market trading to $75.41 following the announcement, despite reporting earnings per share of $0.86 that exceeded analyst expectations of $0.75.

The company reported total revenue of $1.62 billion, representing a 10% year-over-year decrease, falling short of the forecasted $1.67 billion. However, Parsons emphasized that excluding a confidential contract, revenue actually increased 14% overall and 9% organically.

Quarterly Performance Highlights

Parsons highlighted several key achievements in its third-quarter presentation, including significant adjusted EBITDA margin expansion and strong free cash flow generation. The company’s adjusted EBITDA margin expanded 60 basis points to 9.8%, while cash flow from operations reached $163 million with free cash flow conversion of 135%.

The company maintained its book-to-bill ratio at 1.0x, continuing its streak of trailing twelve-month book-to-bill ratios of 1.0x or greater in every quarter since its IPO. Notably, the Critical Infrastructure segment has maintained a book-to-bill ratio above 1.0x for 20 consecutive quarters.

The financial summary reveals that while total revenue decreased compared to Q3 2024, Parsons achieved net income of $64 million. The company’s backlog increased by $48 million to $8.8 billion, with 72% of that amount funded – the highest level since the company’s IPO. Additionally, Parsons reported approximately $11 billion worth of contract wins not yet booked into backlog and a robust pipeline of $58 billion that includes more than 115 opportunities worth $100 million or more.

Segment Performance Analysis

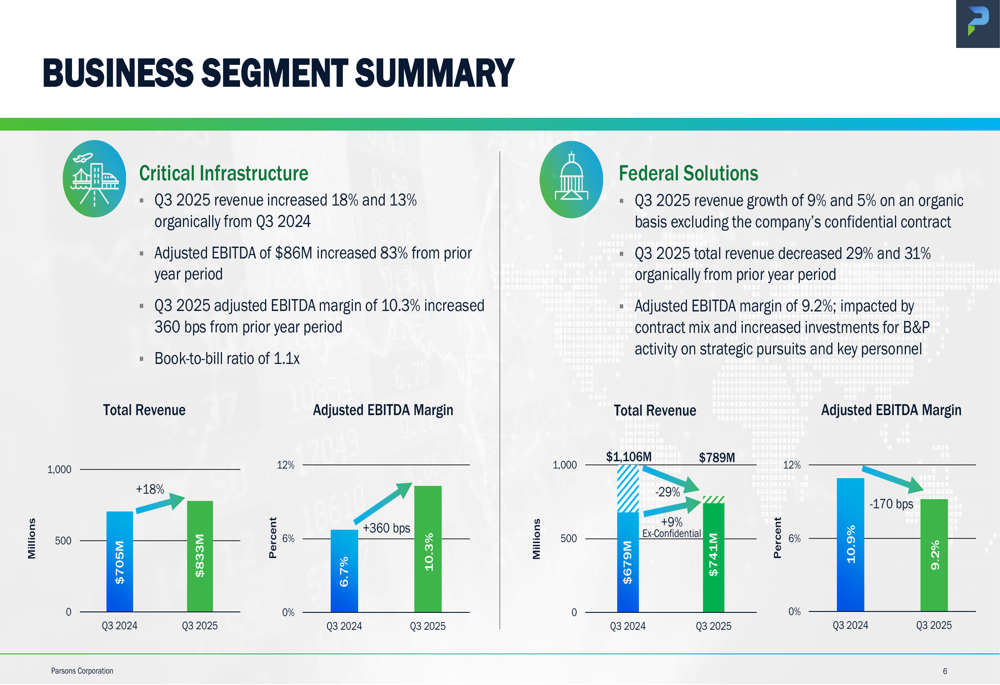

Parsons’ two business segments showed divergent performance in Q3 2025. The Critical Infrastructure segment demonstrated exceptional growth, with revenue increasing 18% (13% organically) to $833 million from $705 million in Q3 2024. More impressively, the segment’s adjusted EBITDA of $86 million represented an 83% increase from the prior year period, with margins expanding 360 basis points to 10.3%.

In contrast, the Federal Solutions segment faced challenges, with total revenue decreasing 29% to $789 million from $1,106 million in Q3 2024. However, excluding the company’s confidential contract, the segment would have shown 9% revenue growth and 5% organic growth. The segment’s adjusted EBITDA margin declined 170 basis points to 9.2%, which Parsons attributed to contract mix and increased investments in business development activities.

Contract Wins and Strategic Initiatives

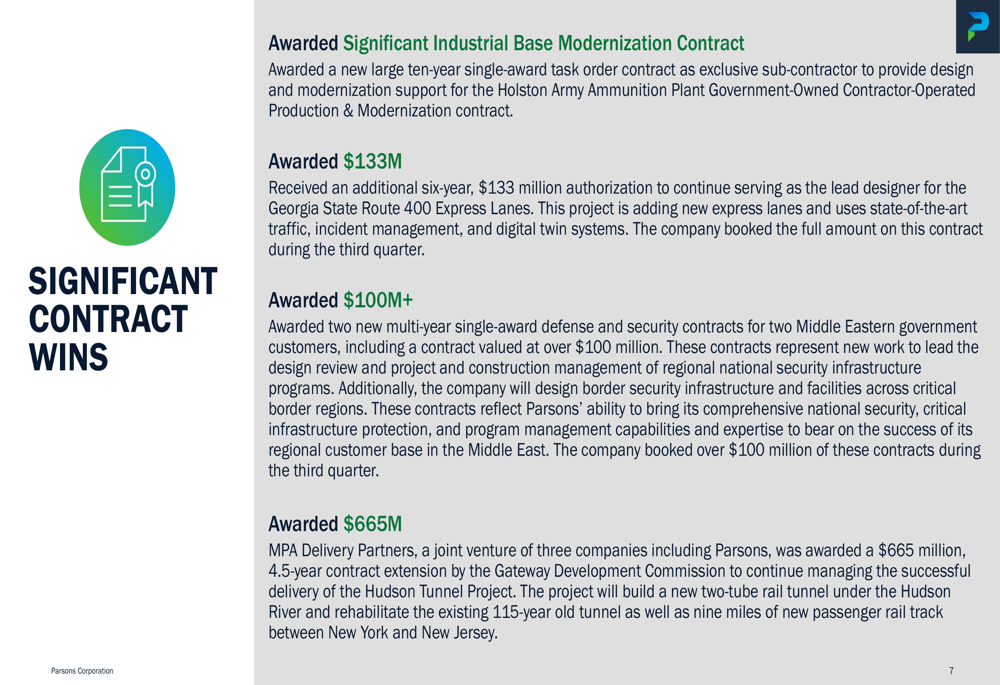

Parsons secured several significant contract wins during the quarter, bolstering its future revenue prospects. Notable awards included a ten-year single-award task order contract for the Holston Army Ammunition Plant, a $133 million six-year authorization for Georgia State Route 400 Express Lanes, and two defense and security contracts worth over $100 million for Middle Eastern government customers.

The company also highlighted a substantial $665 million, 4.5-year contract extension from the Gateway Development Commission for the Hudson Tunnel Project, which involves building a new two-tube rail tunnel under the Hudson River.

Additionally, Parsons was awarded $88 million in task orders under the Air Base Air Defense (ABAD) IDIQ contract vehicle, bringing year-to-date awards through this vehicle to over $190 million. The company also secured three contracts in the PFAS market totaling $23 million and won prime positions on four multiple-award IDIQ contracts with federal customers, with a combined ceiling value of $43.5 billion.

After the quarter ended, Parsons acquired Applied Sciences Consulting, a Florida-based engineering firm specializing in water and stormwater solutions, enhancing its water expertise and strengthening its presence in Florida. The company also received recognition as one of the World’s Best Companies in 2025 by TIME and Statista and was honored by Glassdoor as one of the Best-Led Companies in 2025.

Guidance and Outlook

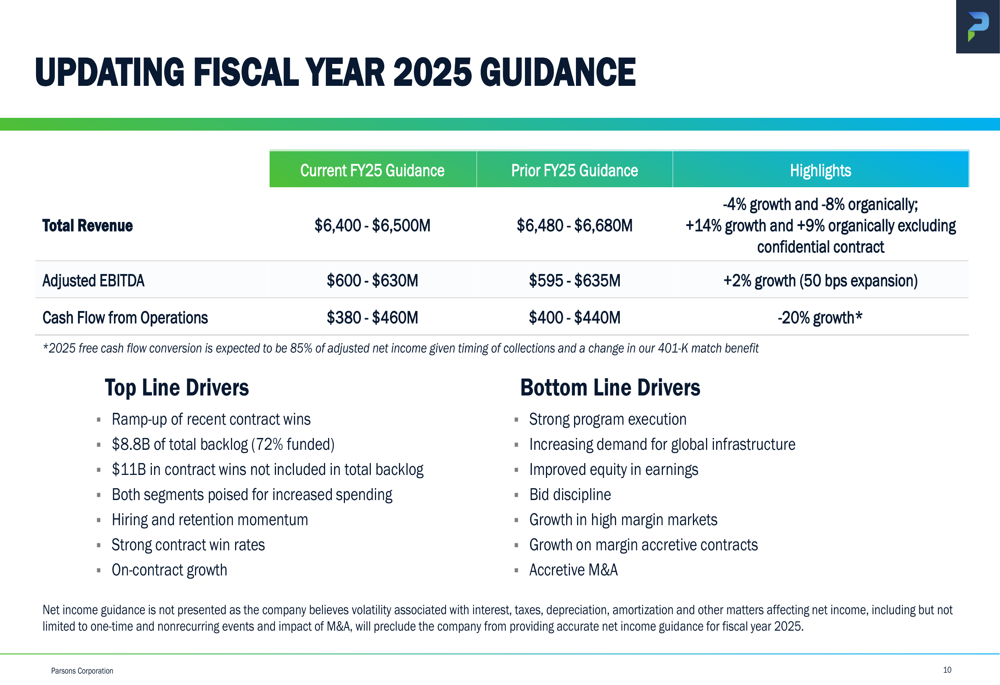

In response to the quarter’s performance, Parsons modified its fiscal year 2025 revenue guidance downward to $6.4-$6.5 billion from the previous range of $6.48-$6.68 billion. This adjustment represents a 4% year-over-year decline or 8% organically. However, excluding the confidential contract, the guidance would reflect 14% growth and 9% organic growth.

Despite the revenue guidance reduction, Parsons maintained its adjusted EBITDA guidance at $600-$630 million, slightly narrowing the range from the previous $595-$635 million. This represents approximately 2% growth and 50 basis points of margin expansion. The company also updated its cash flow from operations guidance to $380-$460 million, compared to the previous range of $400-$440 million.

The company’s guidance assumes that approximately 51% of total revenue will be generated from the Federal Solutions segment, with an overall adjusted EBITDA margin of approximately 9.5% at the midpoint of the revenue guidance – up 50 basis points from 2024. Parsons expects sequential revenue growth of approximately 4% from Q3 to Q4 2025 to achieve its full-year guidance.

Investor Reaction and Market Perspective

Despite the earnings per share beat, investors reacted negatively to Parsons’ revenue miss and guidance adjustment. The stock fell 5.22% in pre-market trading to $75.41, reflecting concerns about the company’s top-line performance. This reaction came despite Parsons’ strong cash flow generation and margin expansion during the quarter.

During the earnings call, analysts inquired about the impact of government shutdowns on Parsons’ operations. Management expressed confidence in Q4 performance despite these challenges, anticipating increased activity once the government reopens. The company also highlighted the low recompete rate for major contracts in 2026 as a positive factor for future stability.

Conclusion

Parsons’ third-quarter 2025 results present a mixed picture, with strong earnings performance and margin expansion contrasted against revenue challenges that prompted a guidance adjustment. The Critical Infrastructure segment continues to demonstrate robust growth and profitability improvement, while the Federal Solutions segment shows underlying strength when excluding the impact of a confidential contract.

With a solid backlog, significant contract wins, and strategic acquisitions, Parsons appears well-positioned for future growth despite near-term revenue headwinds. The company’s ability to maintain its adjusted EBITDA guidance while generating strong cash flow suggests effective cost management and operational efficiency, though investors remain cautious about top-line performance in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.