5 big analyst AI moves: Apple lifted to Buy, AI chip bets reassessed

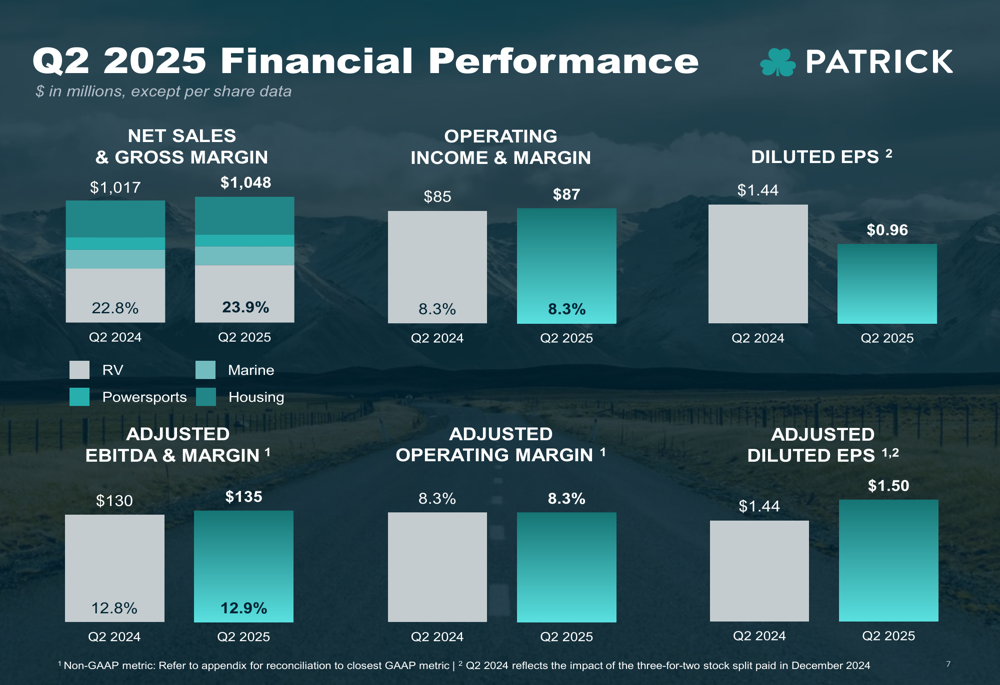

Patrick Industries, Inc. (NASDAQ:PATK) reported a 3% year-over-year increase in revenue to $1.05 billion for the second quarter of 2025, according to the company’s earnings presentation released on July 31. The outdoor recreation and housing products manufacturer demonstrated resilience amid challenging market conditions, though profitability metrics showed mixed results with adjusted earnings per share rising 4% while net income declined significantly.

Quarterly Performance Highlights

Patrick’s revenue growth was driven by a combination of organic growth (3%) and acquisitions (4%), which offset industry headwinds (-4%). The company reported adjusted EBITDA of $135 million with a margin of 12.9%, slightly up from 12.8% in the same period last year. Gross margin improved to 23.9% from 22.8% in Q2 2024, while operating margin remained stable at 8.3%.

However, diluted earnings per share fell to $0.96 from $1.44 in the prior-year period, representing a 33% decrease. On an adjusted basis, diluted EPS increased to $1.50 from $1.44, up 4% year-over-year.

As shown in the following financial performance comparison:

The company’s stock rose 2.36% during the regular trading session following the earnings release but declined 1.51% in aftermarket trading, reflecting mixed investor sentiment about the results.

Segment Performance Analysis

Patrick’s revenue diversification strategy continued to provide resilience, with varying performance across its four main segments:

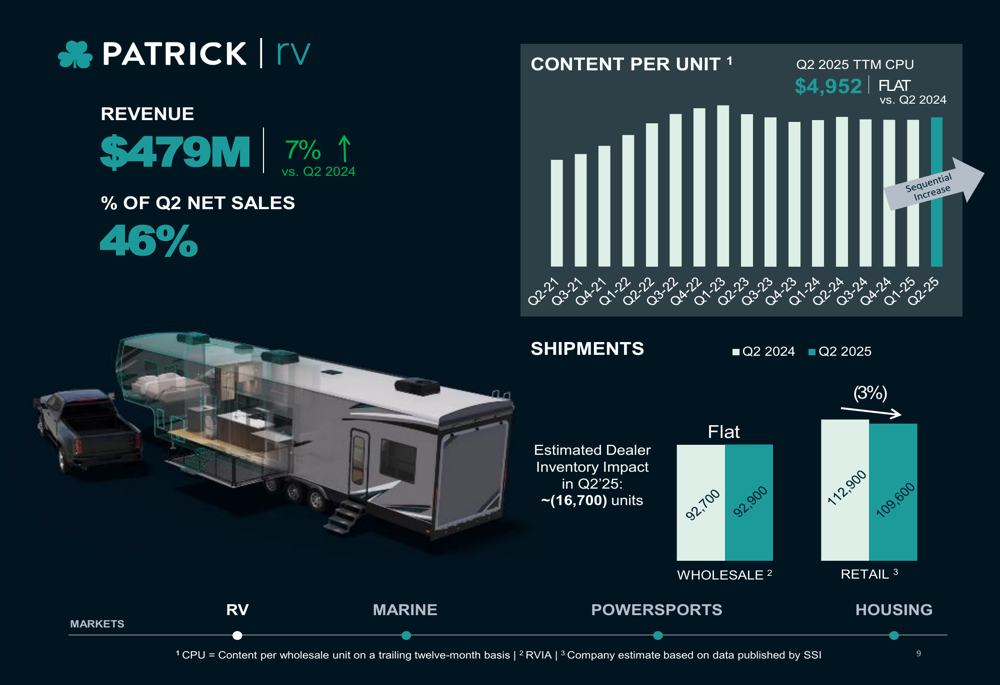

- RV: Revenue increased 7% year-over-year to $479 million, representing 46% of total sales. Wholesale shipments were flat at 92,900 units, while retail shipments declined 3% to 109,600 units.

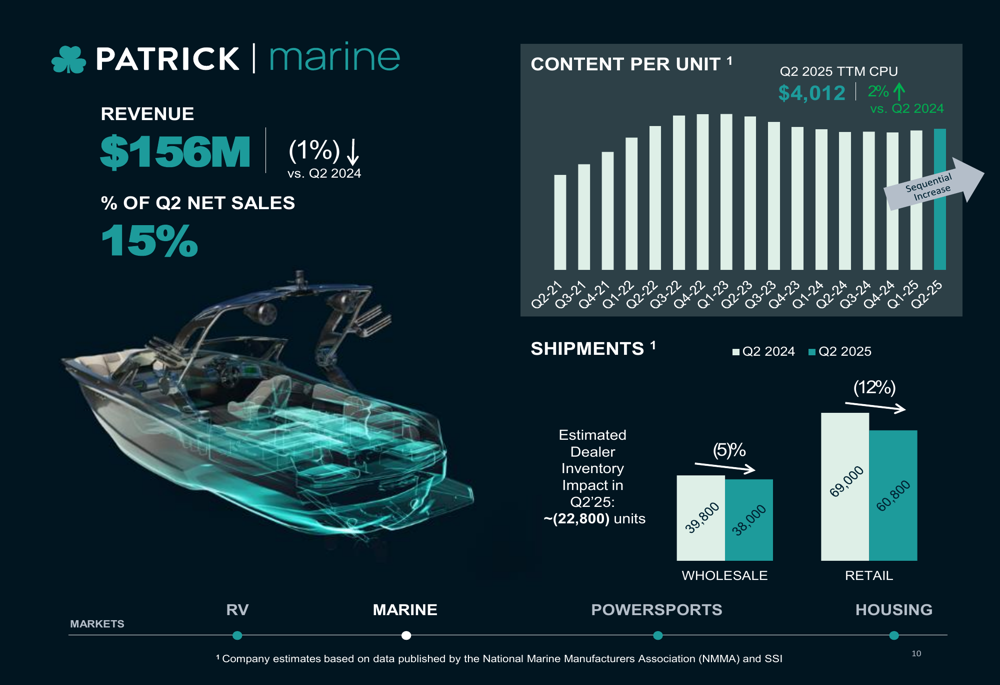

- Marine: Revenue decreased 1% to $156 million (15% of total sales), with wholesale shipments down 5% and retail shipments down 12%.

- Powersports: Revenue fell 7% to $96 million (9% of total sales).

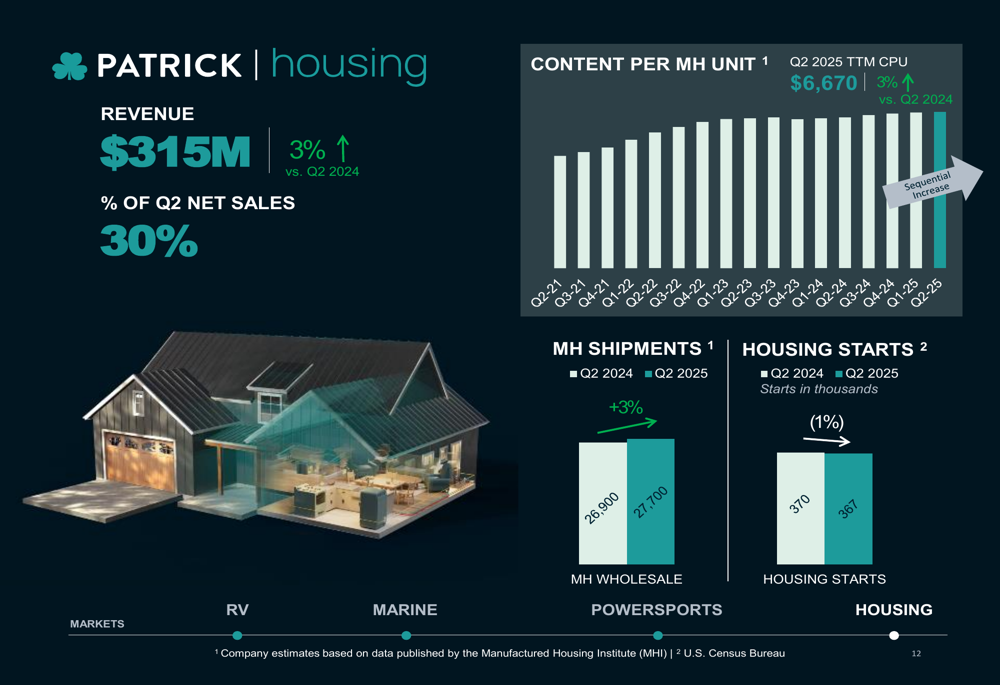

- Housing: Revenue grew 3% to $315 million (30% of total sales), with manufactured housing shipments up 3% to 27,700 units.

The RV segment performance details are illustrated here:

Similarly, the marine segment faced challenges with declining shipments:

The housing segment provided a bright spot with growth in both revenue and shipments:

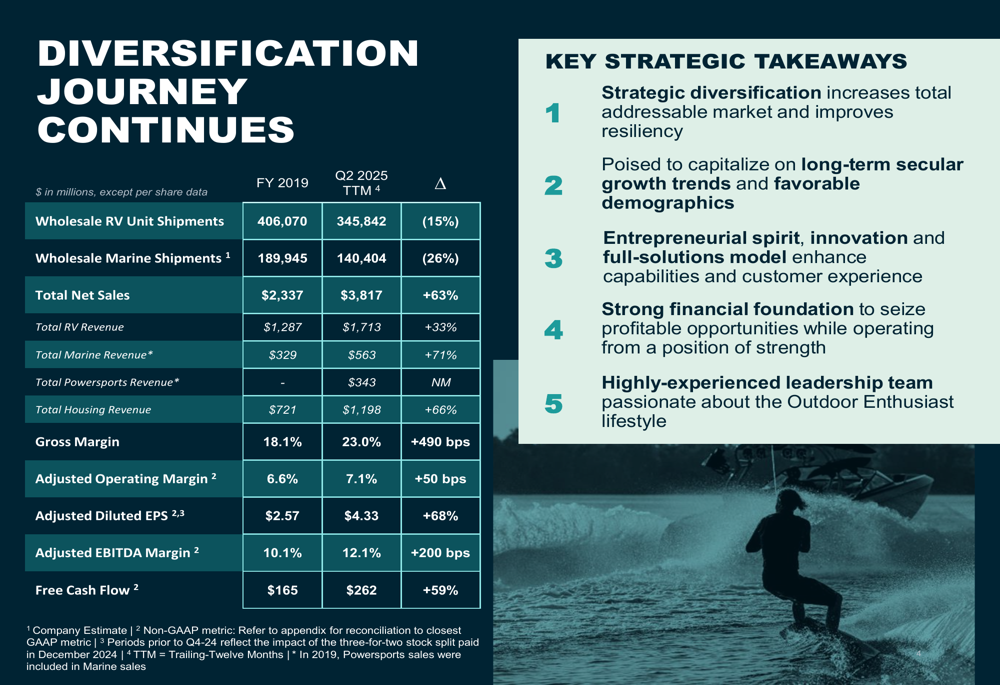

Strategic Positioning and Diversification

Patrick’s diversification strategy has significantly transformed the company since 2019, with total net sales growing 63% to $3.82 billion on a trailing twelve-month basis, despite declines in wholesale RV and marine shipments. This growth has been accompanied by margin improvements, with gross margin expanding 490 basis points to 23.0% and adjusted EBITDA margin increasing 200 basis points to 12.1%.

The following chart illustrates the company’s diversification journey and financial improvements:

CEO Andy Nemeth expressed optimism during the earnings call, stating, "We remain energized about the opportunities that are in front of us." The company highlighted that its strategic diversification has increased its total addressable market and improved business resilience.

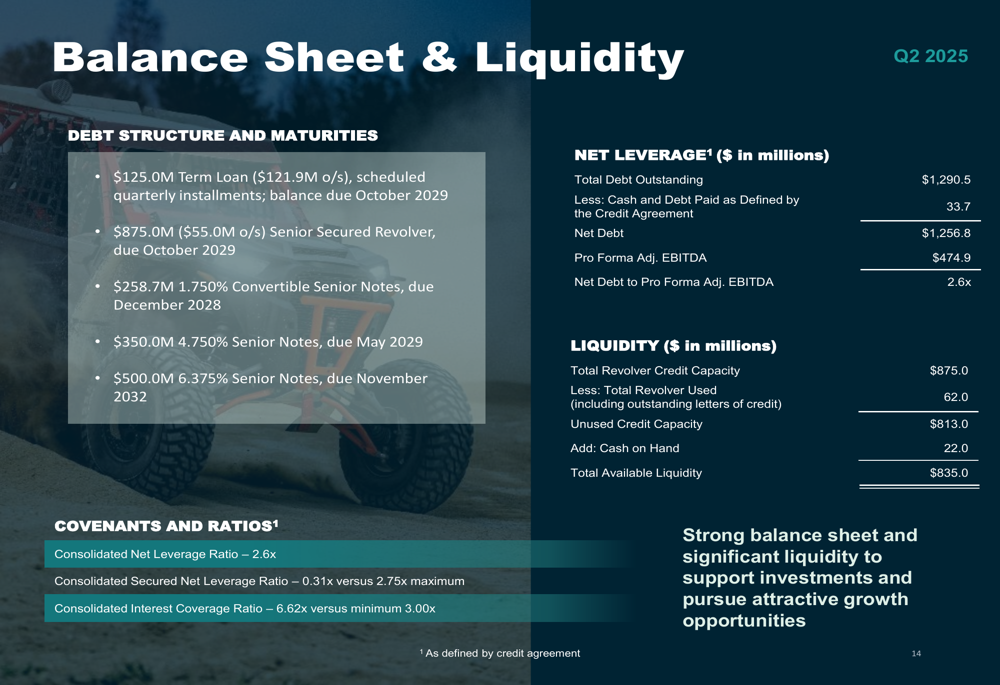

Financial Position and Capital Allocation

Patrick maintained a strong balance sheet with total available liquidity of $835 million at the end of Q2. The company’s net leverage ratio improved to 2.6x from 2.7x at the end of the first quarter. During the quarter, Patrick opportunistically repurchased approximately 277,800 shares at an average price of $84.43, totaling more than $23 million.

Cash flow from operations on a year-to-date basis grew 10% year-over-year to $189 million, while free cash flow on a trailing twelve-month basis was $262 million.

The company’s debt structure and liquidity position are detailed below:

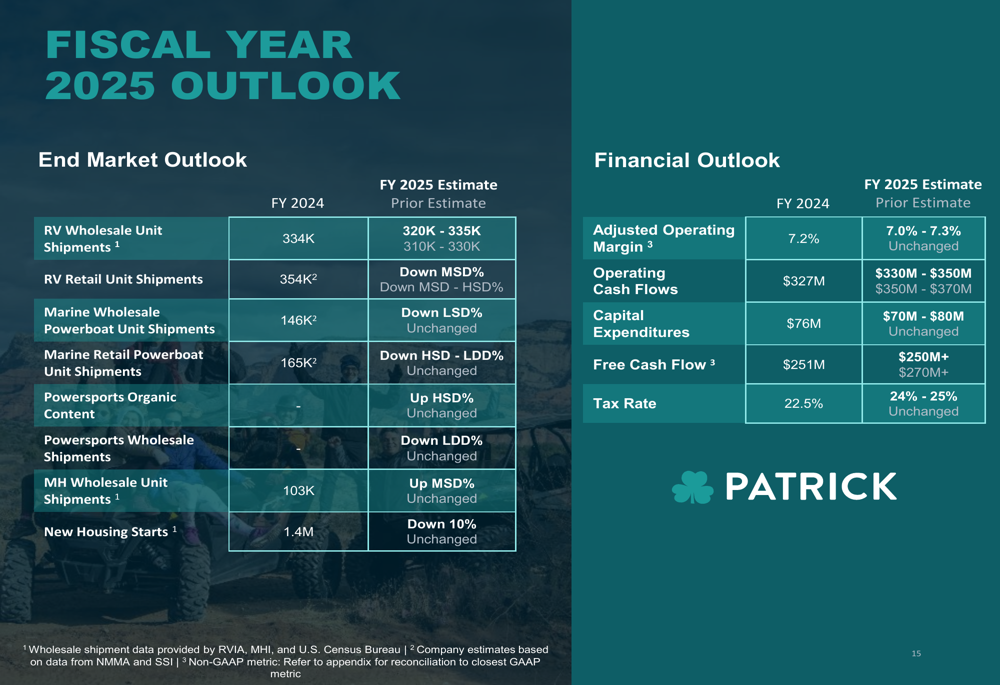

Market Trends and Outlook

Patrick identified several trends affecting its end markets, including lean dealer inventories in the RV segment, disciplined OEM production in powersports, and strong demand for affordable housing. The company noted that "as clarity improves surrounding the macroeconomic environment, we expect consumers and dealers to react more positively."

For fiscal year 2025, Patrick provided the following outlook:

The company expects RV wholesale unit shipments between 320,000 and 335,000 units, compared to 334,000 in fiscal 2024. Marine wholesale powerboat shipments are projected to decline by a low single-digit percentage. On the financial front, Patrick forecasts an adjusted operating margin between 7.0% and 7.3%, operating cash flows of $330-350 million, and free cash flow exceeding $250 million.

CFO Andy Rader expressed confidence in the company’s financial trajectory, stating, "We feel good about our ability to continue to leverage the business."

Despite the challenges in certain segments, Patrick’s diversified business model and strong financial foundation position the company to navigate current market conditions while pursuing growth opportunities across its various end markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.