BofA’s Hartnett says concentrated U.S. stock returns are likely to persist

Penske Automotive Group (NYSE:PAG) released its second quarter 2025 financial results presentation on July 30, showing improved profitability despite flat revenue, as the company continues to leverage its diversified business model and focus on operational efficiency.

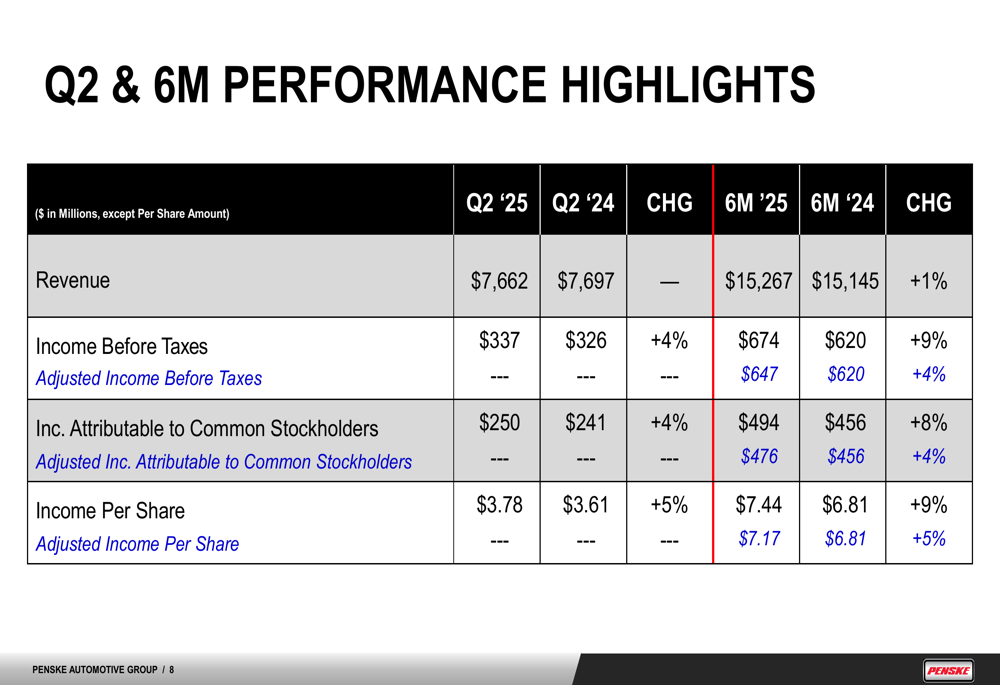

Quarterly Performance Highlights

Penske reported flat revenue at $7.7 billion for Q2 2025 compared to the same period last year, while six-month revenue increased slightly by 1% to $15.3 billion. Despite the revenue plateau, the company achieved notable growth in profitability metrics, with income before taxes rising 4% to $337 million in the quarter and 9% to $674 million for the six-month period.

Income per share showed stronger growth, increasing 5% to $3.78 in Q2 2025 and 9% to $7.44 for the first half of the year, reflecting the positive impact of the company’s ongoing share repurchase program.

As shown in the following performance summary table, Penske demonstrated consistent improvement across key financial metrics:

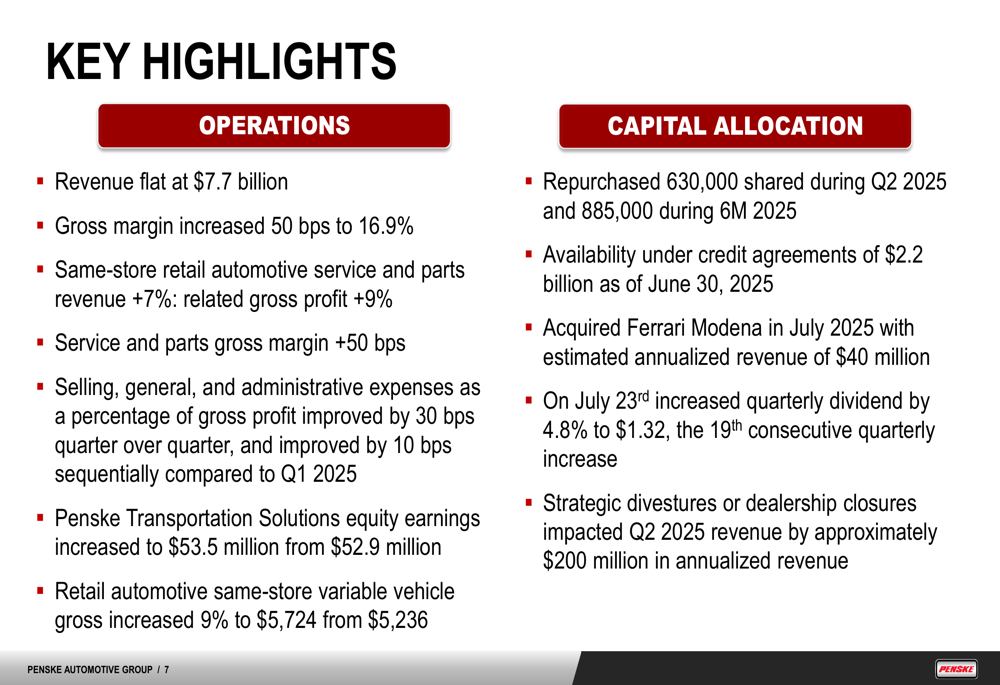

Gross margin expanded by 50 basis points to 16.9%, while selling, general, and administrative expenses as a percentage of gross profit improved by 30 basis points quarter-over-quarter. These efficiency gains highlight the company’s ability to enhance profitability even without significant revenue growth.

Operational Efficiency and Margin Expansion

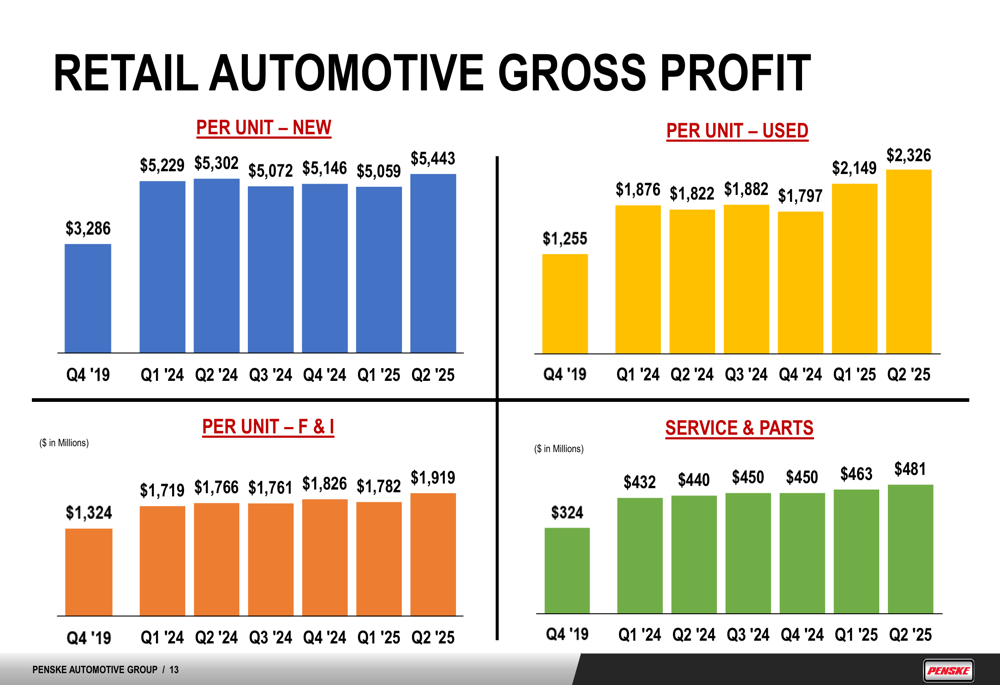

A key driver of Penske’s improved profitability has been the strong performance in its service and parts segment, with same-store retail automotive service and parts revenue increasing 7% and related gross profit rising 9%. The service and parts business typically generates higher margins than vehicle sales, making it a strategic focus for the company.

The following chart illustrates the consistent growth in gross profit per unit across various segments since Q4 2019:

Retail automotive same-store variable vehicle gross increased 9% to $5,724 from $5,236, further contributing to margin expansion. This improvement in per-unit profitability has helped offset the challenges in unit volume growth.

The company’s key operational highlights also include sequential improvement in SG&A expenses as a percentage of gross profit compared to Q1 2025:

Diversified Business Model

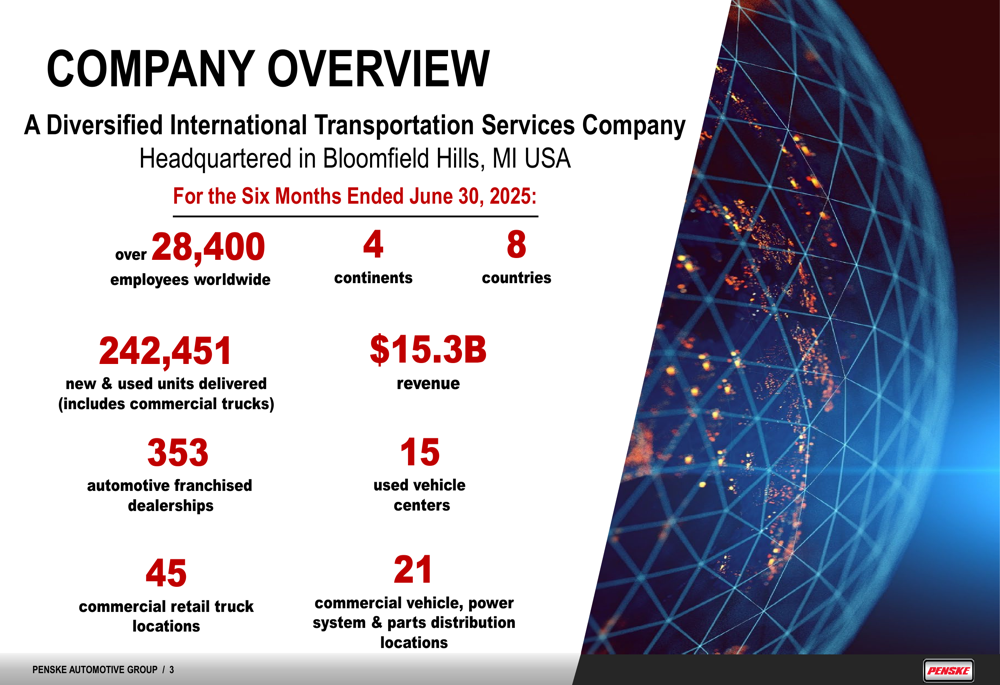

Penske’s diversified business model continues to be a source of resilience. The company operates across multiple segments including premium automotive retail, commercial trucks, and transportation solutions, with a global footprint spanning four continents and eight countries.

The following overview illustrates the scale and reach of Penske’s operations:

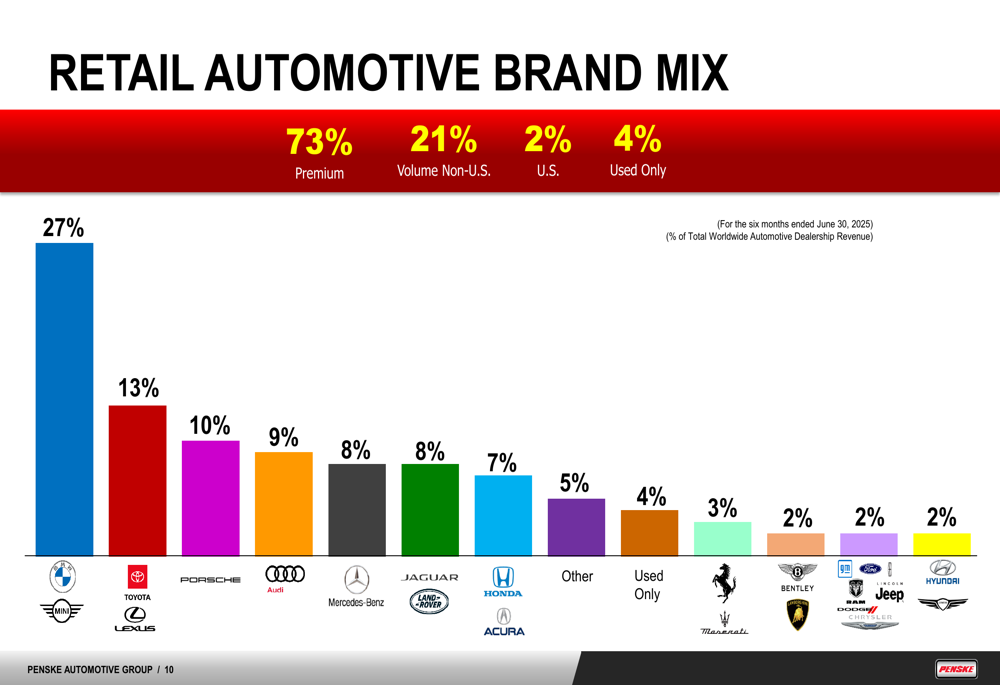

In the retail automotive segment, Penske maintains a strong focus on premium brands, which account for 73% of total worldwide automotive dealership revenue. BMW (ETR:BMWG) leads with 27% of the brand mix, followed by Toyota (NYSE:TM) at 13% and Porsche at 10%.

As shown in the following brand mix breakdown, this premium-weighted portfolio helps support higher margins:

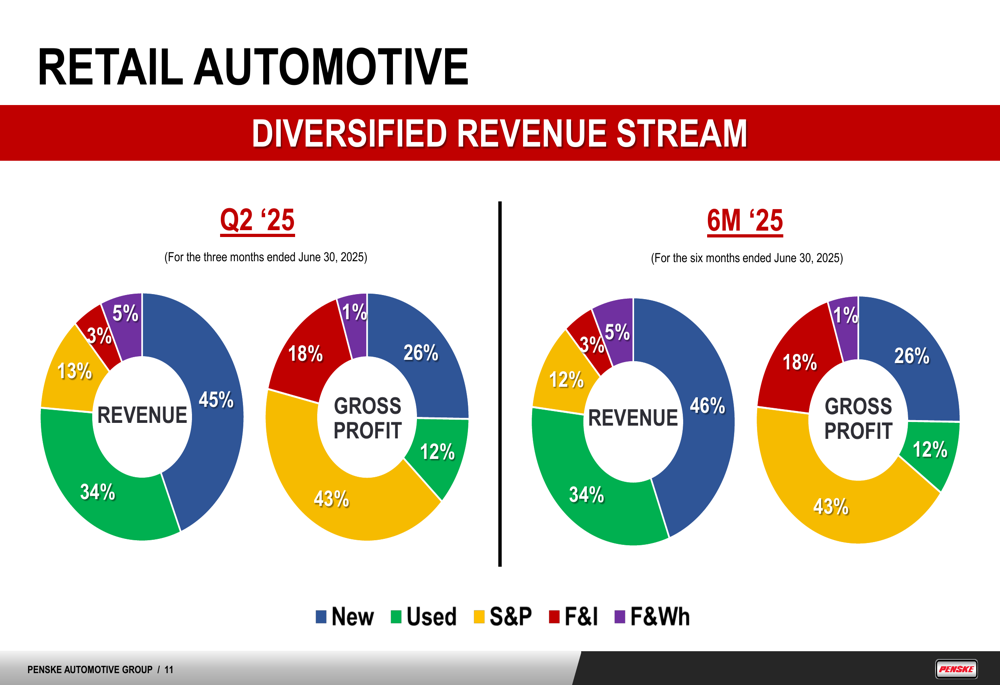

The company’s revenue streams are well-diversified across new vehicles, used vehicles, service and parts, finance and insurance, and fleet and wholesale operations:

Penske’s commercial truck segment, operated through Premier Truck Group, reported Q2 2025 revenue of $944 million, up from $892 million in Q2 2024. Earnings before taxes for this segment reached $54 million, representing a slight increase from $52 million in the prior year.

The company’s operations in Australia and New Zealand showed particularly strong growth, with six-month revenue reaching $541 million, a 42% increase compared to $381 million in the same period of 2024.

Additionally, Penske’s 28.9% ownership stake in Penske Transportation Solutions (PTS) continues to provide a steady stream of equity income, which increased to $53.5 million in Q2 2025 from $52.9 million in Q2 2024.

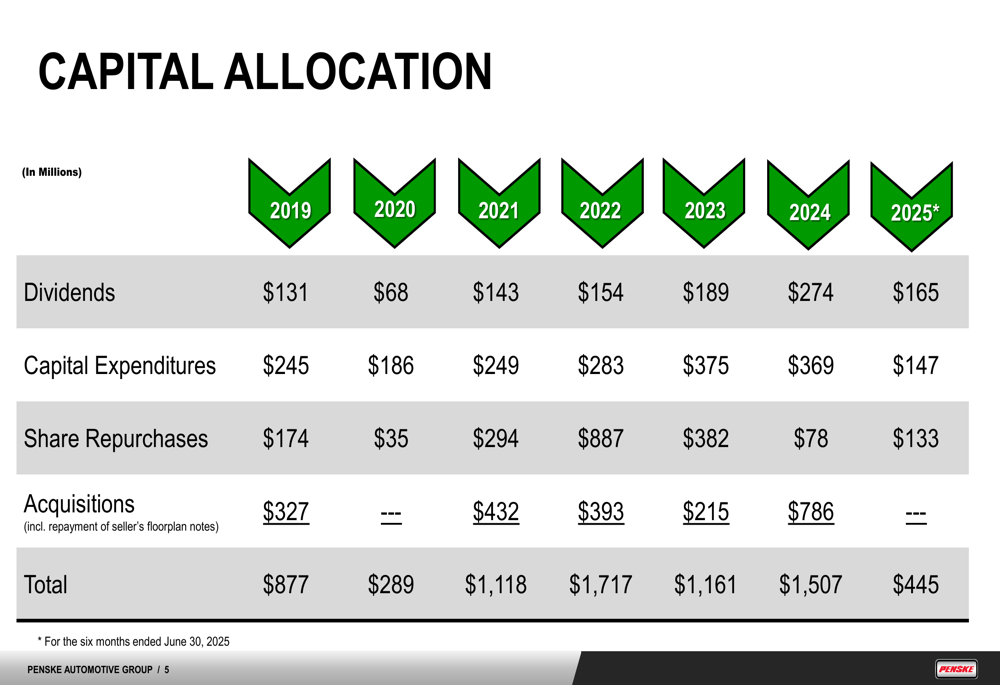

Capital Allocation and Financial Position

Penske has maintained a balanced approach to capital allocation, focusing on shareholder returns, strategic acquisitions, and maintaining a strong balance sheet. During Q2 2025, the company repurchased 630,000 shares, bringing the total for the first half of the year to 885,000 shares.

On July 23, 2025, Penske increased its quarterly dividend by 4.8% to $1.32 per share, marking the 19th consecutive quarterly increase. This continued dividend growth underscores the company’s commitment to returning capital to shareholders.

The following chart illustrates Penske’s capital allocation strategy over recent years:

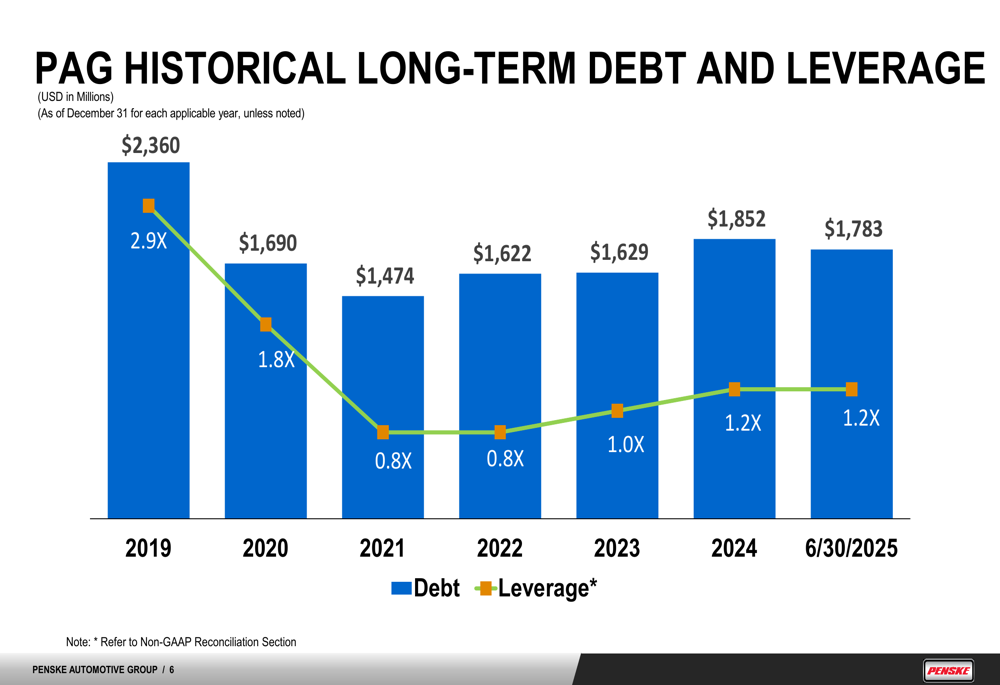

The company has also maintained a disciplined approach to debt management, with long-term debt of $1.78 billion as of June 30, 2025, and a leverage ratio of 1.2x:

In terms of strategic portfolio management, Penske acquired Ferrari (BIT:RACE) Modena in July 2025, with an estimated annualized revenue of $40 million. The company also completed strategic divestures or dealership closures that impacted Q2 2025 revenue by approximately $200 million on an annualized basis.

Forward-Looking Statements

While Penske’s Q2 2025 presentation focuses primarily on historical performance, the company’s Q1 2025 earnings call had highlighted potential challenges including tariff impacts and fluid market conditions expected in the latter half of 2025.

The stock closed at $168.01 on July 29, 2025, representing a decline of 1.32% or $2.24, suggesting ongoing investor concerns despite the improved profitability metrics. The stock has traded between $134.05 and $186.33 over the past 52 weeks.

Penske’s continued focus on operational efficiency, margin expansion, and its diversified business model positions the company to navigate potential market challenges. The strong performance in high-margin segments such as service and parts, along with strategic portfolio management through acquisitions and divestures, demonstrates management’s commitment to enhancing shareholder value even in a challenging revenue environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.