Crispr Therapeutics shares tumble after significant earnings miss

Introduction & Market Context

Perseus Mining Ltd (ASX:PRU) reported strong financial results for the June 2025 quarter, capitalizing on surging gold prices despite a slight dip in production and rising costs. The company’s presentation, delivered on July 28, 2025, highlighted how favorable gold market conditions helped boost cash margins and accelerate capital returns to shareholders while advancing key growth projects.

The gold miner’s stock closed at $3.56 on July 25, 2025, down 2.47% in the session but maintaining a position well above its 52-week low of $2.31, reflecting overall positive market sentiment toward the company’s performance and growth strategy.

Quarterly Performance Highlights

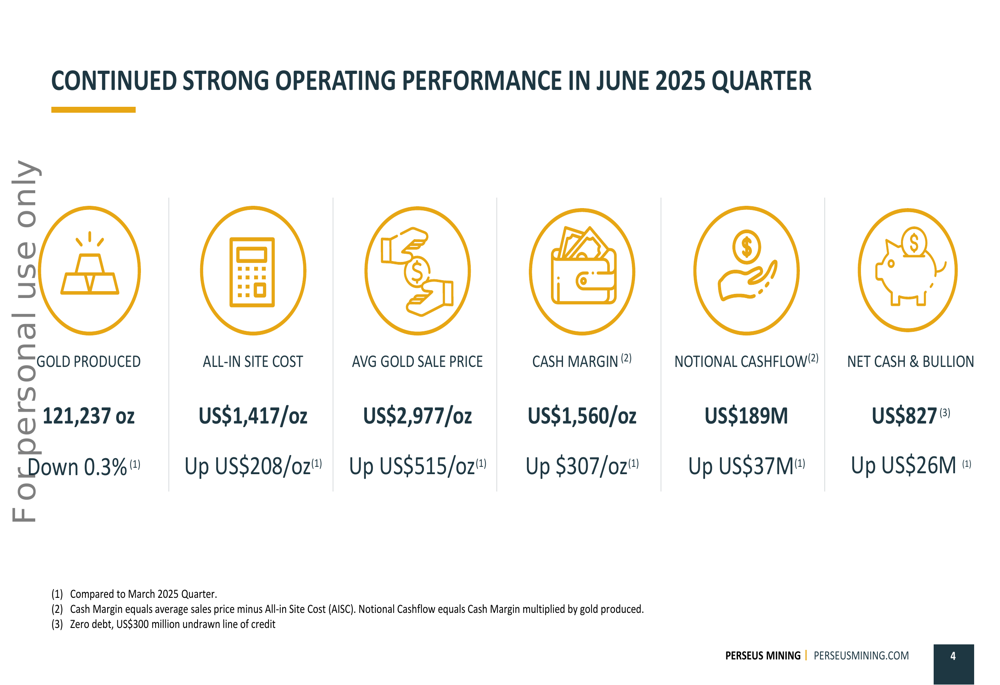

Perseus produced 121,237 ounces of gold in the June 2025 quarter, representing a marginal decrease of 0.3% compared to the March 2025 quarter. While all-in site costs rose to US$1,417 per ounce (up US$208/oz quarter-on-quarter), the company benefited significantly from higher gold prices, with the average realized price reaching US$2,977 per ounce, up US$515/oz from the previous quarter.

As shown in the following quarterly performance summary:

The combination of higher gold prices and controlled cost increases resulted in a cash margin of US$1,560 per ounce, representing a US$307 per ounce improvement over the March quarter. This translated to notional cashflow of US$189 million for the quarter, up US$37 million from the previous period, demonstrating the company’s ability to leverage the favorable gold price environment.

Full-Year FY25 Results

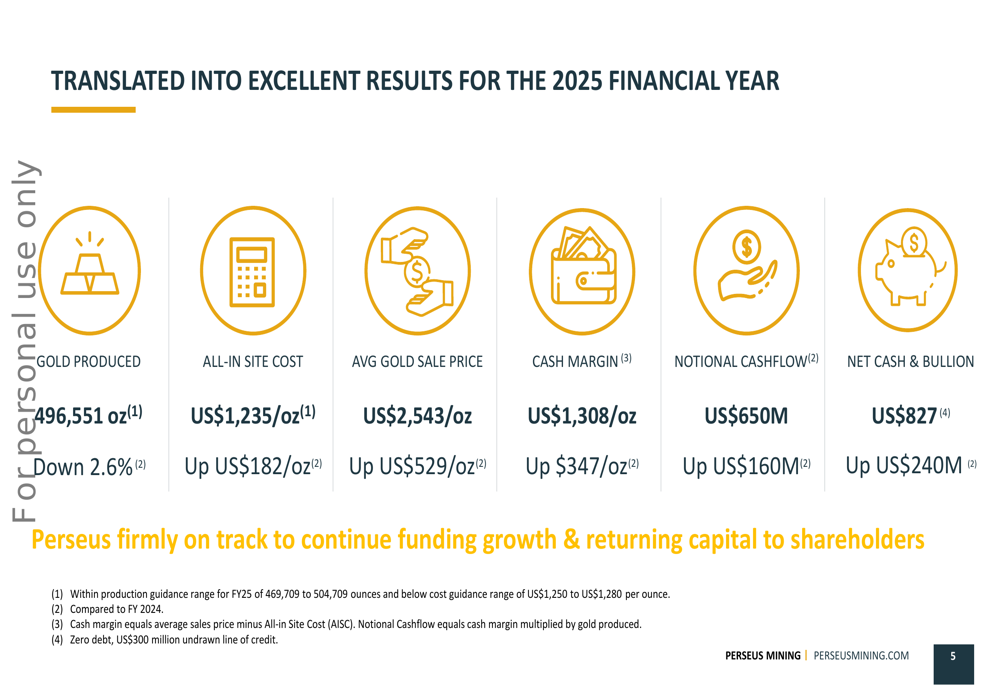

For the full 2025 financial year, Perseus achieved gold production of 496,551 ounces, which, while down 2.6% year-over-year, remained comfortably within the company’s guidance range of 469,709 to 504,709 ounces. The company’s all-in site cost for the year was US$1,235 per ounce, below the guided range of US$1,250 to US$1,280 per ounce despite increasing US$182 per ounce compared to FY24.

The full-year financial performance is summarized in the following slide:

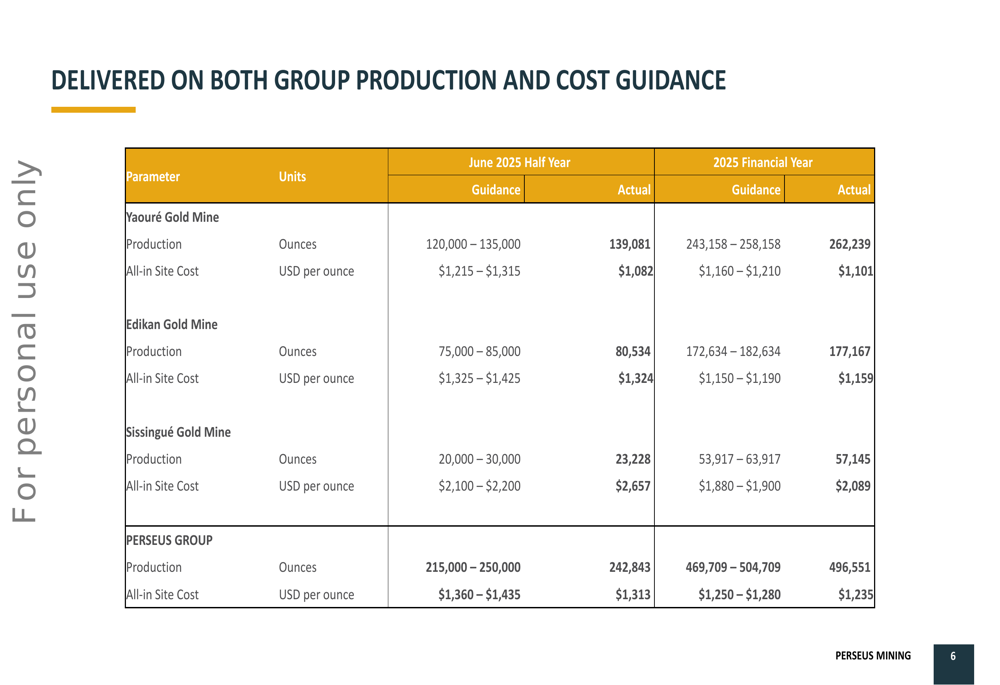

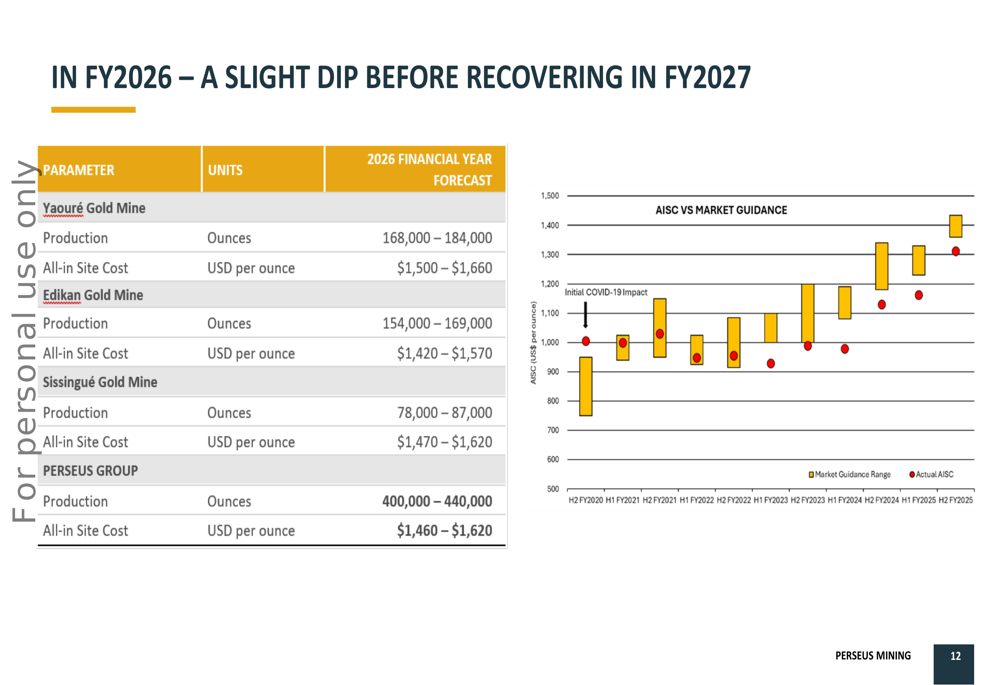

Perseus’s operations continued to outperform against guidance across its three mines, with Yaouré in Côte d’Ivoire being the standout performer, contributing 53% of the company’s total production. The detailed breakdown of guidance versus actual performance demonstrates the company’s operational discipline:

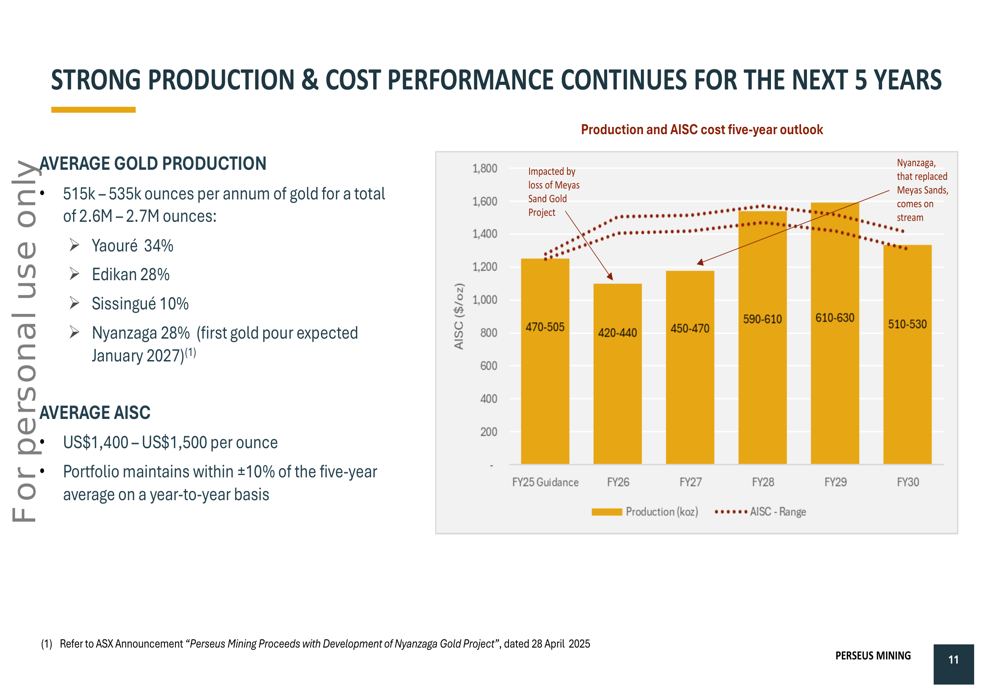

The company’s five-year production outlook remains robust, with average annual gold production expected to range between 515,000 and 535,000 ounces from FY25 to FY30, for a total of 2.6 to 2.7 million ounces over the period:

Growth Projects and Outlook

Perseus is advancing two significant growth projects that will shape its future production profile. The Nyanzaga Gold Project in Tanzania is progressing toward first gold production in Q1 2027, with construction scheduled to commence in July 2025. When operational, Nyanzaga is expected to contribute approximately 28% of Perseus’s production and is forecast to be the company’s lowest-cost asset.

The CMA Underground project at Yaouré received its final investment decision in January 2025, with underground mining activities scheduled to begin in Q1 FY26. This project will extend Yaouré’s operational life until at least 2035, securing the long-term future of Perseus’s flagship operation.

For FY26, Perseus has guided to lower production of 400,000-440,000 ounces at higher all-in site costs of US$1,460-US$1,620 per ounce, reflecting the transition period before Nyanzaga comes online:

Capital Management and Shareholder Returns

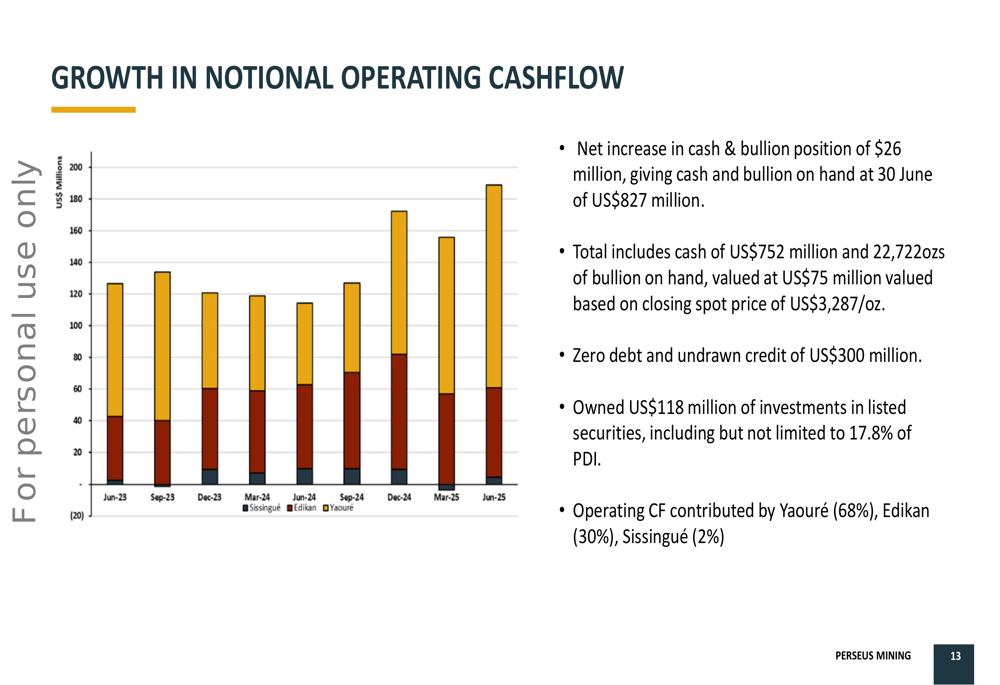

Perseus’s strong operational performance has translated into significant cash generation, with the company ending the June quarter with US$827 million in cash and bullion, up US$26 million from the March quarter and US$240 million year-over-year. The company maintains zero debt and has an undrawn credit facility of US$300 million.

The following chart illustrates the growth in notional operating cashflow by mine:

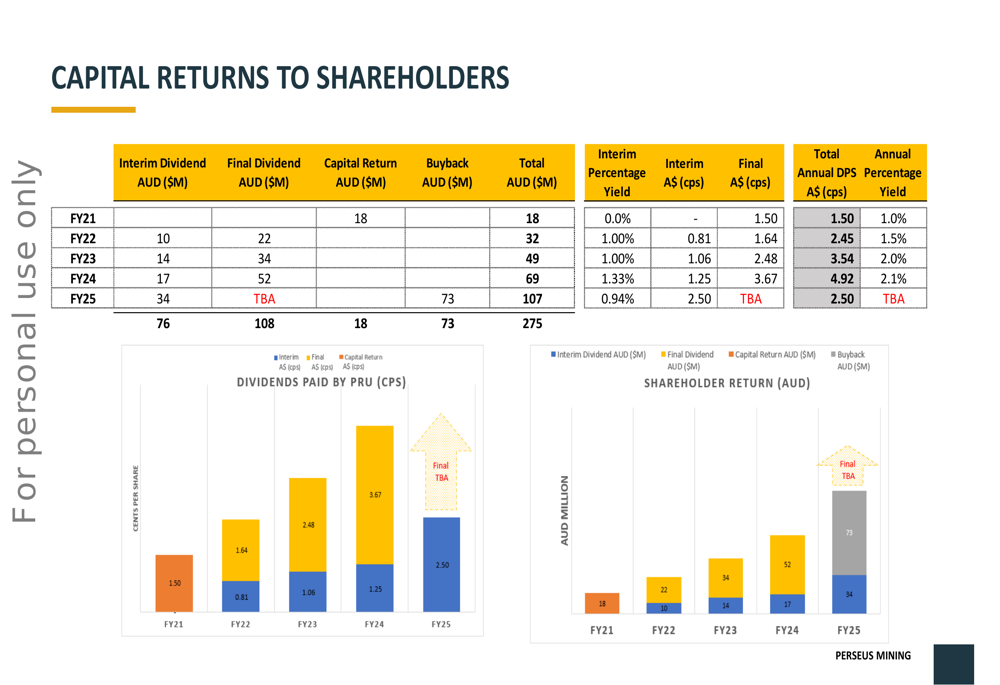

Perseus has significantly increased capital returns to shareholders, with total returns in FY25 reaching A$107 million, up from A$69 million in FY24. This includes an interim dividend of A$34 million and share buybacks totaling A$73 million:

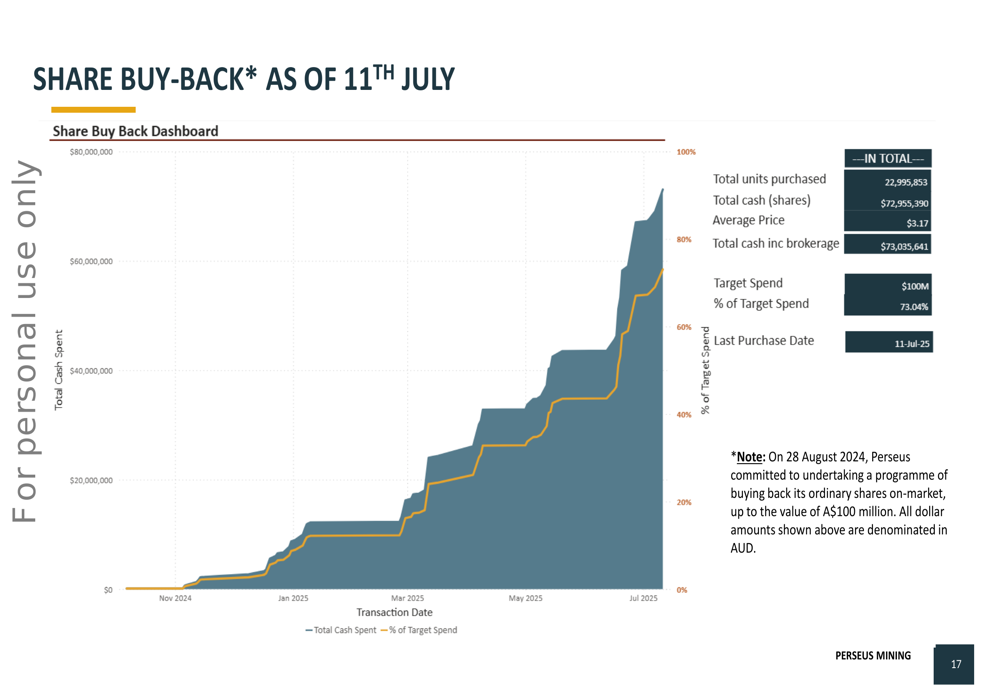

The company’s share buyback program, announced in August 2024, has made substantial progress, with 23 million shares repurchased at an average price of A$3.17, representing 73% of the A$100 million target:

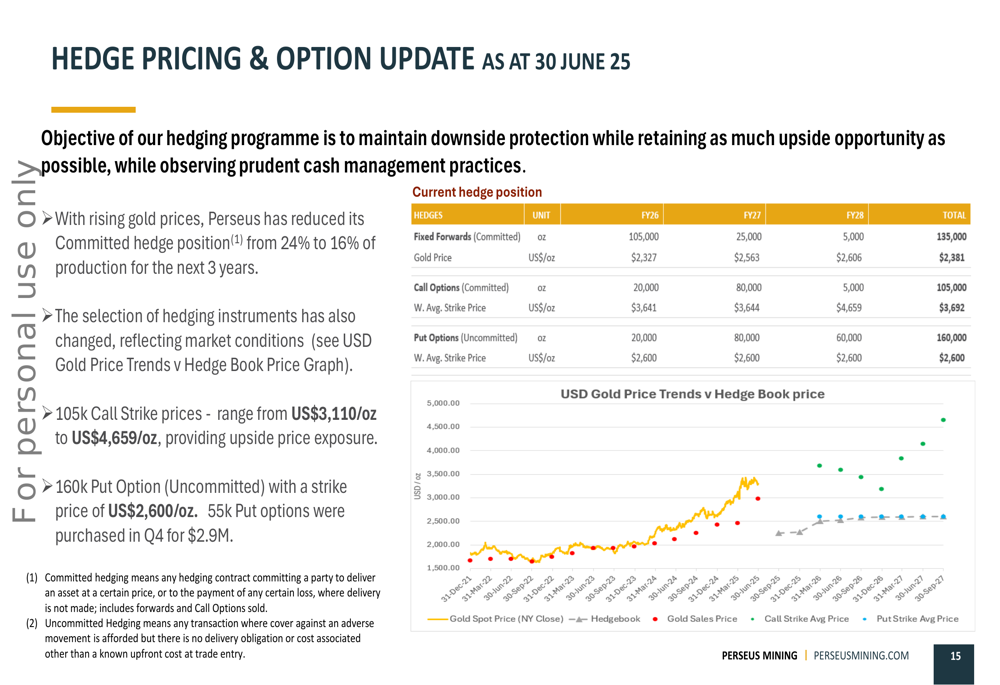

Perseus has also adjusted its hedging strategy in response to rising gold prices, reducing its committed hedge position from 24% to 16% of production for the next three years to retain greater upside potential:

Forward-Looking Statements

Looking ahead, Perseus is positioning itself for sustainable long-term growth while maintaining its focus on shareholder returns. The company’s five-year outlook indicates a temporary dip in production for FY26 before ramping up significantly in FY28-29 as Nyanzaga reaches full production.

Management emphasized that the company is "firmly on track to continue funding growth & returning capital to shareholders," leveraging its strong balance sheet and operational cash flow. With two major growth projects advancing and a disciplined approach to capital allocation, Perseus appears well-positioned to capitalize on the current favorable gold price environment while building for the future.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.