US LNG exports surge but will buyers in China turn up?

Introduction & Market Context

Pet Valu Holdings Ltd. (TSX:PET) presented its Q1 2025 financial results on May 6, showing continued revenue growth amid challenging retail conditions. The Canadian pet specialty retailer reported a 7% year-over-year revenue increase while navigating margin pressures and a slight decline in store traffic. The company’s stock closed at $28.40 on May 5, up 0.85% for the day, and has traded in a 52-week range of $22.53 to $32.01.

As Canada’s leading specialty pet retailer, Pet Valu continues its expansion strategy with new store openings and renovations while investing in supply chain transformation and digital capabilities to maintain its competitive position in the growing pet care market.

Quarterly Performance Highlights

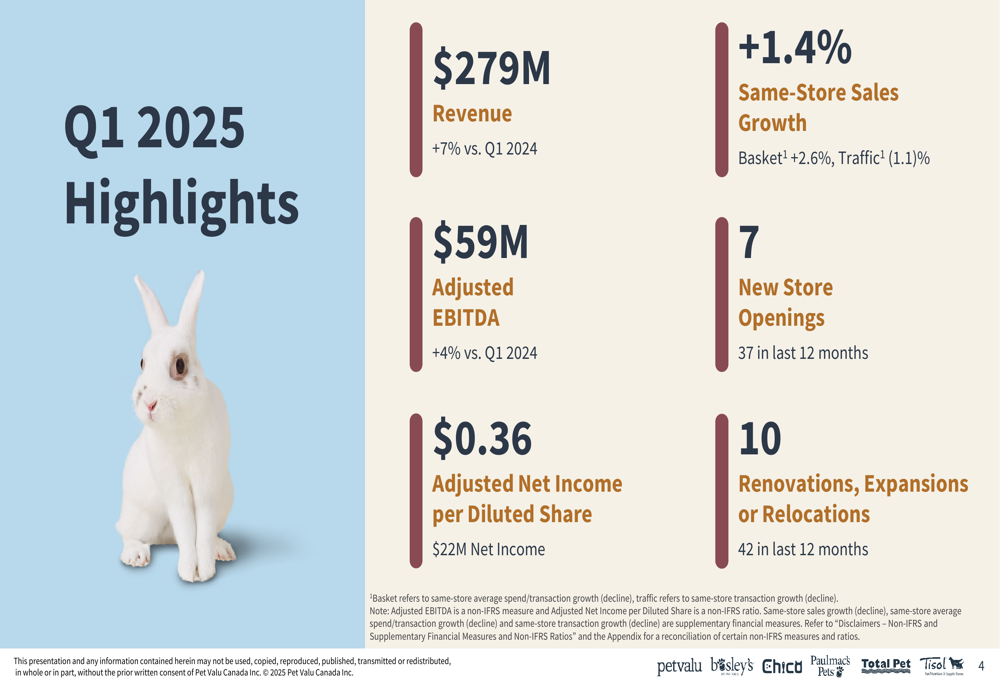

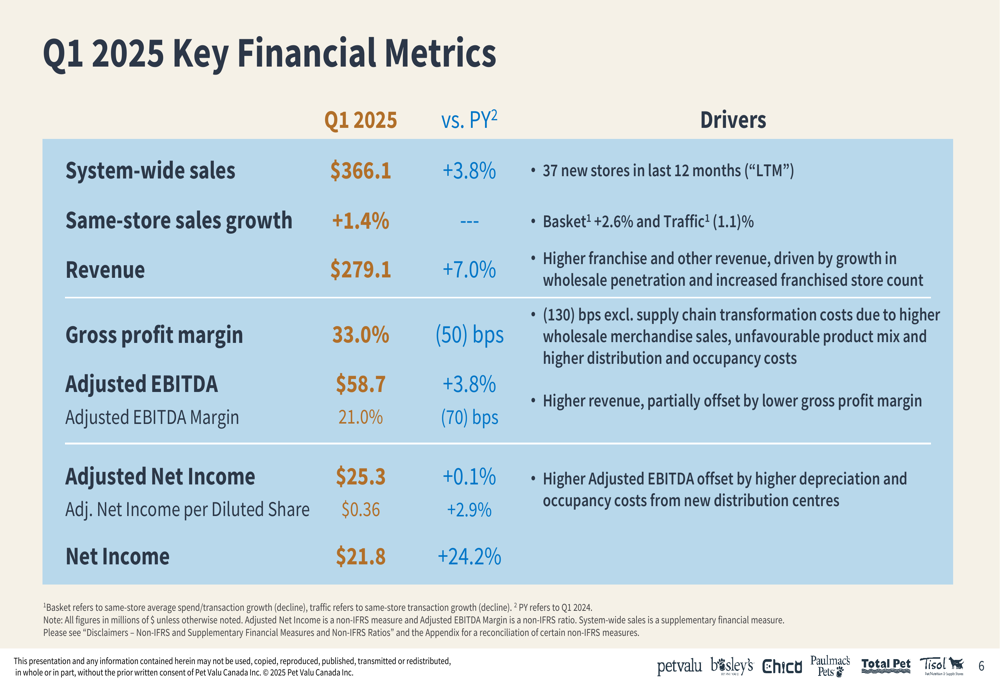

Pet Valu delivered solid top-line growth in Q1 2025, with revenue reaching $279.1 million, a 7% increase compared to the same period last year. System-wide sales, which include franchise-operated locations, grew 3.8% to $366.1 million. Same-store sales increased by 1.4%, driven by a 2.6% growth in average basket size that offset a 1.1% decline in customer traffic.

As shown in the following key performance indicators:

The company opened 7 new stores during the quarter, bringing the total to 37 new locations over the past 12 months. Additionally, Pet Valu completed 10 renovations, expansions, or relocations in Q1, with 42 such projects completed over the trailing twelve months, demonstrating its commitment to maintaining a modern store network.

CEO Richard Maltsbarger, along with President & COO Greg Ramier and CFO Linda Drysdale, presented the results:

Detailed Financial Analysis

While revenue growth remained strong, Pet Valu faced some margin pressure during the quarter. Gross profit margin declined by 50 basis points to 33.0%, while Adjusted EBITDA margin contracted by 70 basis points to 21.0%. Despite these challenges, Adjusted EBITDA increased by 3.8% to $58.7 million.

The company’s detailed financial metrics reveal the underlying performance drivers:

Net income showed impressive growth of 24.2% to $21.8 million, while Adjusted Net Income remained essentially flat at $25.3 million (+0.1%). Adjusted Net Income per Diluted Share increased by 2.9% to $0.36, benefiting from the company’s share repurchase program.

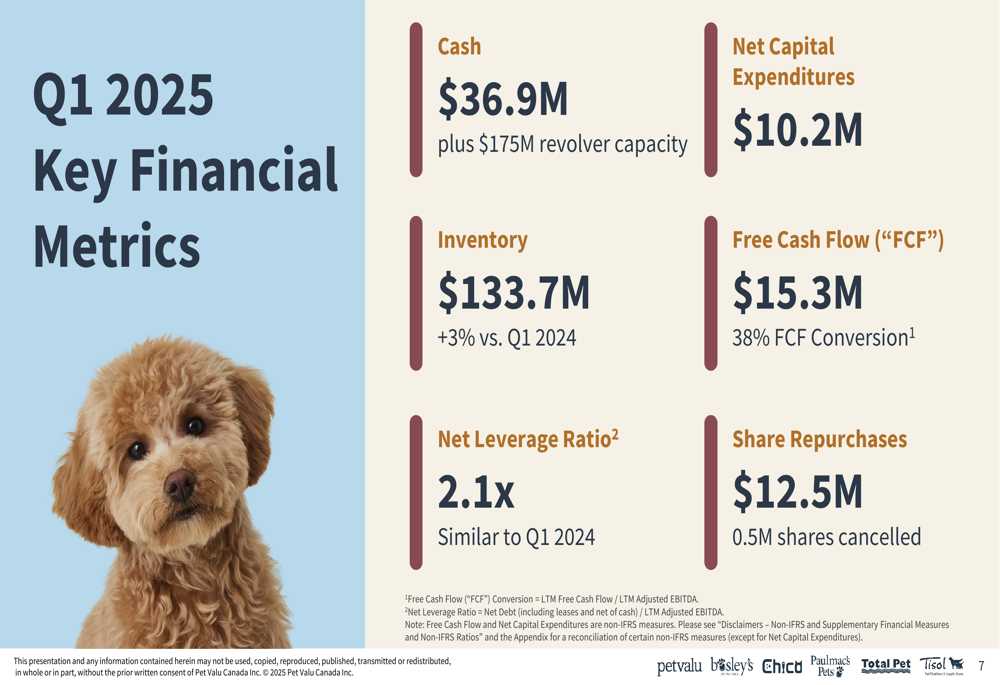

Pet Valu maintained a strong balance sheet with $36.9 million in cash plus $175 million in available revolver capacity. The company’s inventory position of $133.7 million represented a 3% increase compared to Q1 2024, while the net leverage ratio remained stable at 2.1x.

Additional financial metrics highlight the company’s capital allocation strategy:

Free Cash Flow for the quarter was $15.3 million, representing a 38% FCF conversion rate. The company continued its share repurchase program, buying back $12.5 million worth of shares and cancelling 0.5 million shares during the period.

Strategic Initiatives

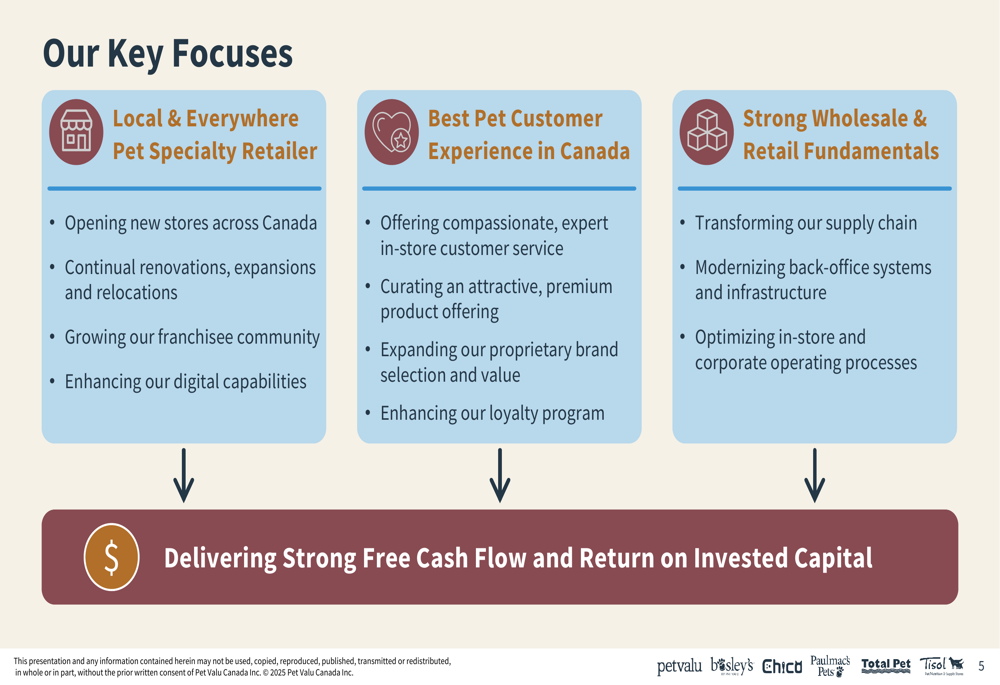

Pet Valu outlined three key strategic focuses that drive its business operations and long-term growth strategy. The company aims to strengthen its position as a "Local & Everywhere Pet Specialty Retailer" by expanding its store network, supporting its franchisee community, and enhancing digital capabilities.

The second strategic pillar focuses on delivering the "Best Pet Customer Experience in Canada" through compassionate service, attractive product offerings, proprietary brands, and loyalty program enhancements. Finally, Pet Valu is investing in "Strong Wholesale & Retail Fundamentals," including supply chain transformation, back-office modernization, and in-store optimization.

These strategic initiatives are designed to deliver strong free cash flow and return on invested capital:

The company’s mission statement reinforces its customer-centric approach: "To be Canada’s preferred pet retailer delivering the products, care, expertise, and memorable moments that devoted pet lovers want...locally in stores and everywhere online."

Forward-Looking Statements

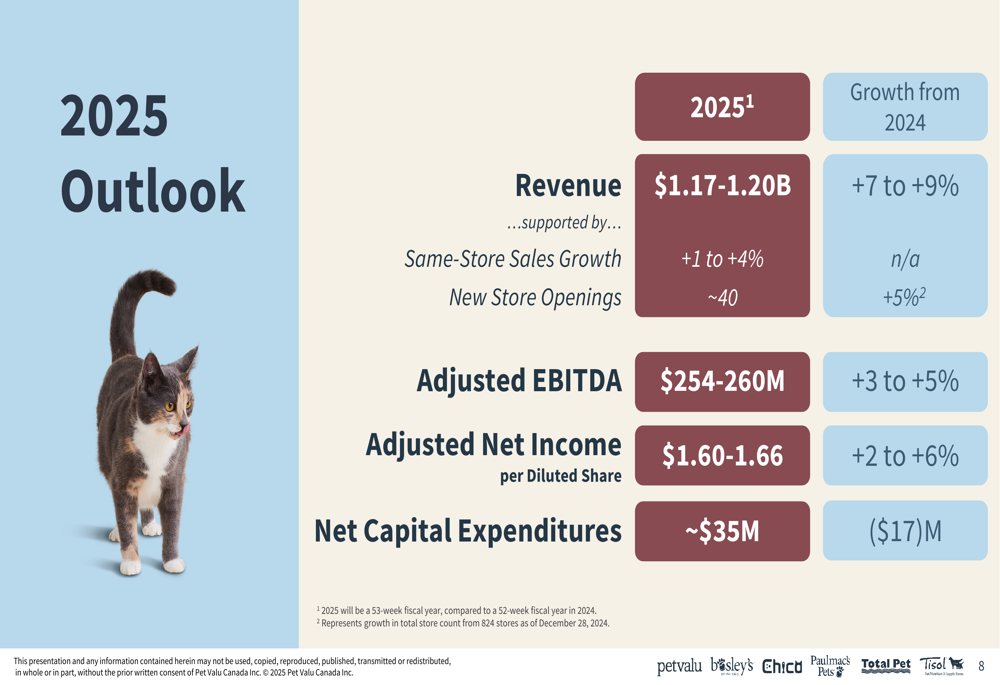

Despite the margin pressures in Q1, Pet Valu maintained an optimistic outlook for the full year 2025. The company projects revenue of $1.17-1.20 billion, representing growth of 7-9% from 2024. This growth is expected to be driven by same-store sales growth of 1-4% and approximately 40 new store openings, which would expand the store count by 5%.

The company’s detailed outlook for 2025 shows confidence in continued growth:

Adjusted EBITDA is forecast to reach $254-260 million, up 3-5% from 2024, while Adjusted Net Income per Diluted Share is expected to be $1.60-1.66, representing growth of 2-6%. Net Capital Expenditures are projected to be approximately $35 million, a decrease of $17 million from the previous year.

Management noted that fiscal 2025 will be a 53-week year, which will provide an additional week of sales compared to the standard 52-week fiscal 2024. This factor will contribute to the overall revenue growth for the year.

As Pet Valu continues to navigate a competitive retail environment, its focus on store expansion, enhanced customer experience, and operational efficiency positions the company to maintain its leadership in the Canadian pet specialty market while delivering value to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.