Gold prices dip as December rate cut bets wane; Fed, econ. data in focus

Introduction & Market Context

Pet Center Comercio e Partcipacoes (BOVESPA:PETZ3), commonly known as Grupo Petz, presented its third quarter 2025 results on November 6, showcasing revenue growth across all channels and significant margin improvements. The company’s stock closed at 3.78 BRL following the announcement, representing a 4.23% increase, as investors responded positively to the company’s performance despite an EPS miss.

The Brazilian pet retail market remains highly fragmented, with Petz continuing to expand its footprint through its omnichannel strategy. The company now operates 264 stores across 24 states, with a total sales area of 221.1k square meters. Notably, 42% of these stores are less than four years old and have not yet reached maturity in terms of operational efficiency.

Quarterly Performance Highlights

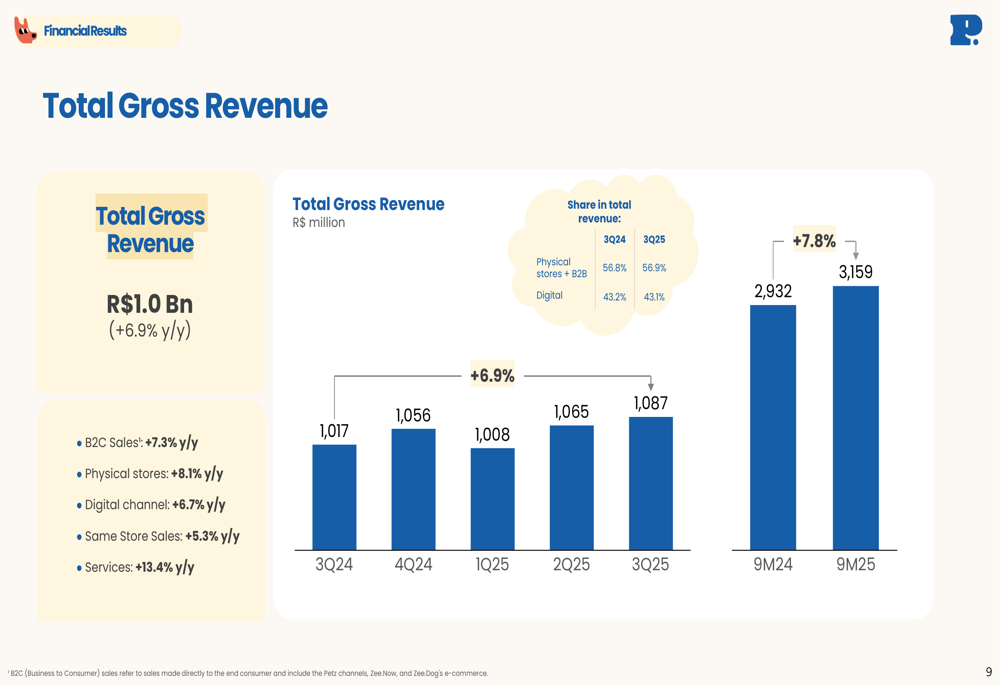

Petz reported total gross revenue of R$1.0 billion for Q3 2025, representing a 6.9% year-over-year increase. This growth was driven by positive performance across all sales channels, with physical store sales increasing by 8.1%, digital channel sales growing by 6.7%, and service revenue rising by 13.4%. Same-store sales growth remained solid at 5.3% year-over-year.

As shown in the following chart of quarterly revenue growth:

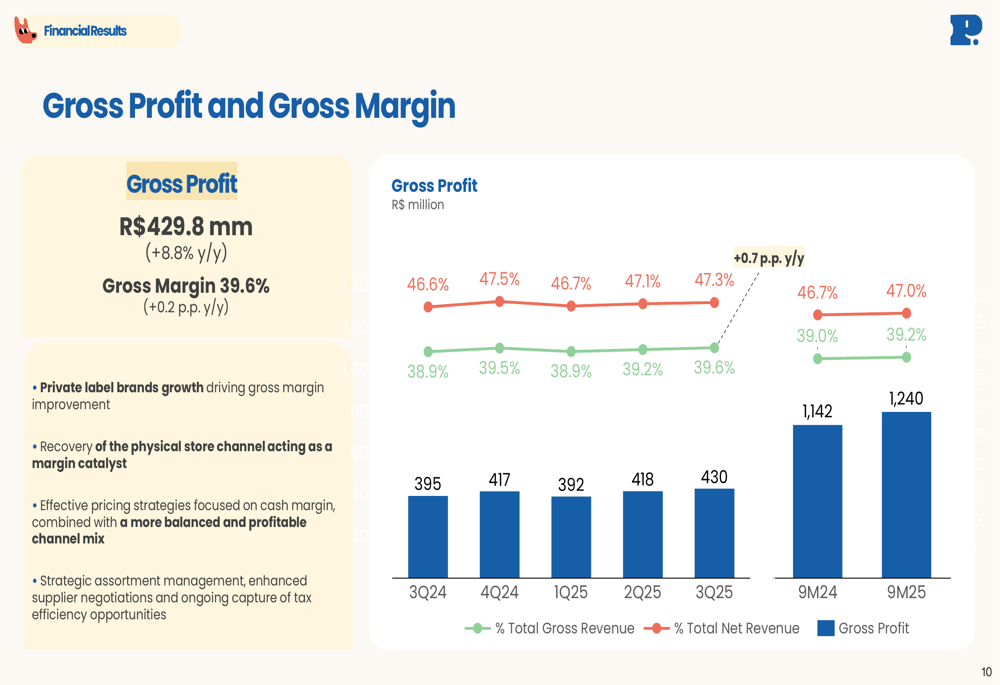

The company’s gross profit reached R$429.8 million, an 8.8% increase compared to the same period last year. Gross margin expanded to 39.6%, a 0.2 percentage point improvement year-over-year. This margin expansion was primarily attributed to the growth of private label products, recovery of physical store channel performance, and effective pricing strategies.

The following chart illustrates the gross profit and margin trends:

Adjusted EBITDA grew by 12.6% year-over-year to R$83.9 million, with the adjusted EBITDA margin improving by 0.4 percentage points to 7.7%. This performance reflects the company’s focus on operational efficiency and profitable growth.

Net income showed significant improvement, with accounting net income reaching R$33.7 million, a 124.1% increase year-over-year. Adjusted net income grew by 40.3% to R$31.3 million, resulting in an adjusted net margin of 2.9%, up 0.7 percentage points from the previous year.

Private Label and Services Growth

A standout performer in Petz’s portfolio has been its private label business, which grew by 36% year-over-year in Q3 2025. Private label products now account for 12.8% of total revenue, an increase of 2.7 percentage points compared to the same period last year. This growth has been a key contributor to the company’s gross margin expansion.

The company highlighted its focus on high-quality private label products with distinctive design and competitive pricing. Recent launches include the "Fuzz" brand and a collaboration between Zee.Dog and Farm.

As illustrated in the private label performance metrics:

Services continue to be a growth driver for Petz, with a 13.4% year-over-year increase in revenue. The company’s benefits club, Clubz, has seen strong momentum, doubling its subscriber base compared to the second quarter of 2025. Management noted an increase in purchase recurrence and share of wallet among Clubz members, contributing to the overall growth in services revenue.

Financial Position and Cash Generation

Petz demonstrated strong cash generation in the third quarter, with operating cash flow of R$176.1 million, representing a 66.4% increase year-over-year. This improvement was attributed to greater operational efficiency, strong cash profit results, and positive working capital variation, primarily due to extended supplier payment terms.

The company’s financial position strengthened significantly, moving from a net debt position of R$45.5 million in Q2 2025 to a net cash position of R$81.0 million by the end of Q3 2025, representing -0.3x adjusted EBITDA for the last twelve months.

The following chart illustrates the company’s cash flow, investments, and leverage position:

Total investments decreased by 10.8% year-over-year in Q3 2025 and by 19.1% for the first nine months of 2025. The company increased spending on renovations and maintenance by 75.1% year-over-year, focusing on HVAC upgrades, energy efficiency improvements, and addressing structural damage at one location.

Merger Update and Outlook

Petz provided an update on its pending merger with Cobasi, which is currently under review by Brazil’s antitrust authority (CADE). The company expects a final decision by mid-December, well ahead of the maximum deadline of January 2, 2026. Management expressed confidence in a favorable outcome, noting that over 90% of suppliers have confirmed they do not oppose the transaction.

The following slide outlines key points regarding the merger status:

The combined entity is expected to hold approximately 11% market share in what Petz describes as a "highly fragmented and competitive market." This merger represents a significant strategic move that could strengthen Petz’s competitive position in the Brazilian pet retail sector.

Looking ahead, the company plans to continue focusing on cash generation, expanding its private label offerings, and growing its omnichannel presence. The Clubz benefits program remains a strategic priority, with management highlighting its potential to drive customer loyalty and increase share of wallet.

Despite missing EPS expectations for the quarter, Petz’s strong revenue growth, margin expansion, and improved cash position suggest the company is executing effectively on its strategic initiatives while preparing for potential integration with Cobasi, pending regulatory approval.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.