Asia FX moves little with focus on US-China trade, dollar steadies ahead of CPI

Plains All American Pipeline (NASDAQ:PAGP) reported solid second-quarter 2025 results with $672 million in adjusted EBITDA, according to the company’s earnings presentation released on August 8. The midstream energy operator maintained its full-year guidance while highlighting significant progress on its strategic initiatives, including a major NGL business divestiture and continued bolt-on acquisitions.

Quarterly Performance Highlights

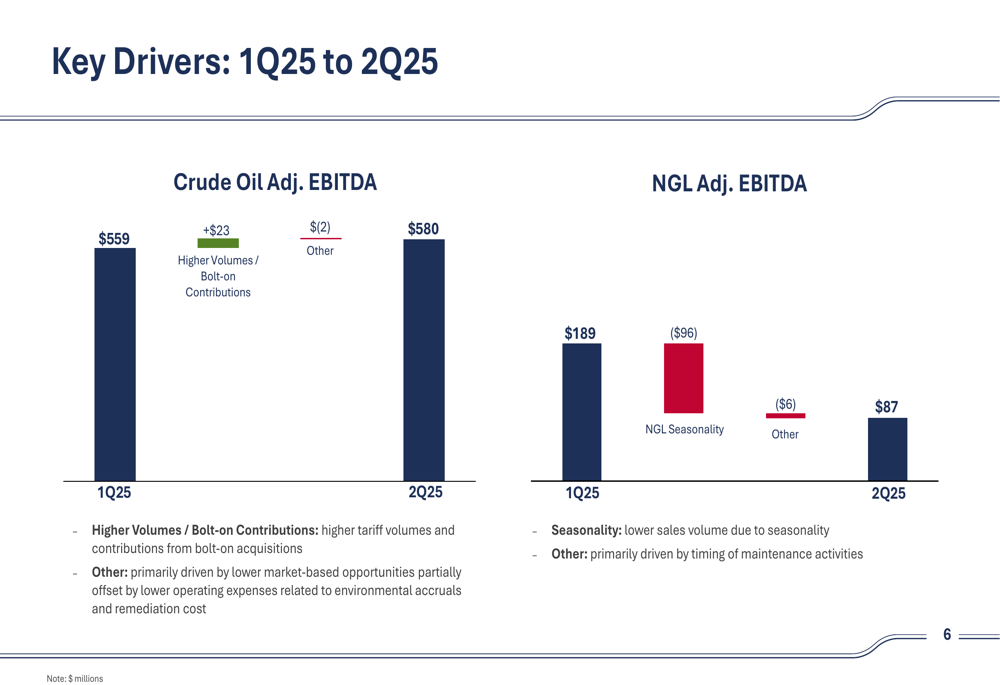

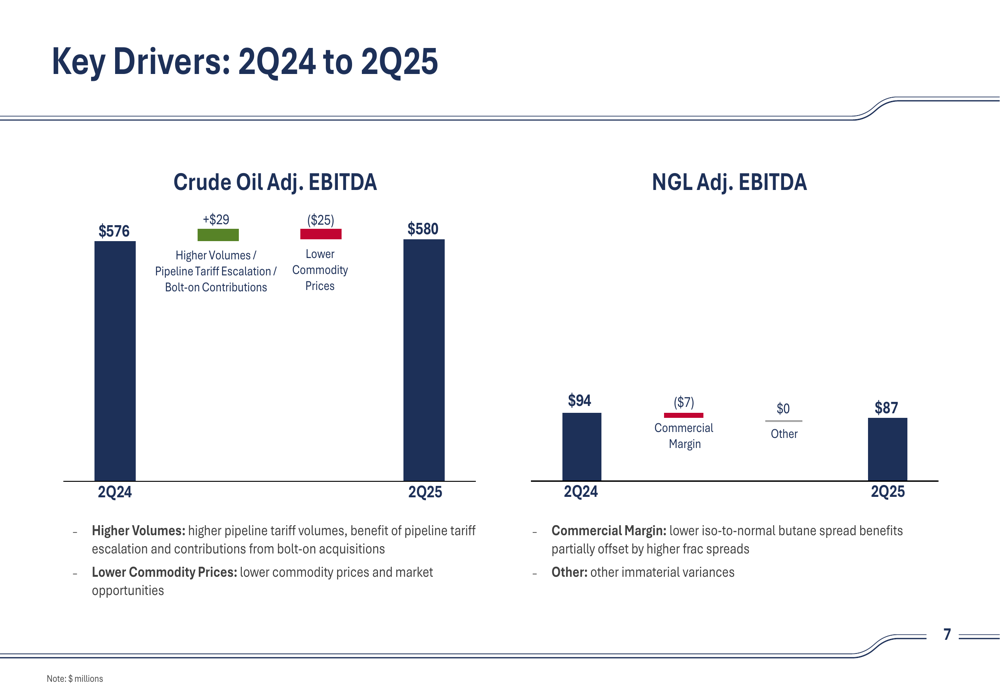

Plains delivered stable performance in Q2 2025, with adjusted EBITDA of $672 million attributable to PAA. The crude oil segment contributed $580 million, showing slight improvement from both the previous quarter ($559 million) and the same period last year ($576 million). Meanwhile, the NGL segment generated $87 million, reflecting typical seasonal weakness compared to Q1’s $189 million.

As shown in the following chart detailing the quarter-to-quarter performance drivers:

The crude oil segment benefited from higher volumes and contributions from bolt-on acquisitions, which added $23 million compared to Q1. The NGL segment experienced its typical seasonal decline of $96 million, as expected given the stronger demand for propane and butane during winter months.

Year-over-year performance showed similar stability in the crude segment, with slight offsets between positive and negative factors:

The company’s leverage ratio stood at 3.3x as of Q2 2025, within its target range of 3.25x-3.75x, maintaining its investment-grade balance sheet ratings (BBB/BBB/Baa2).

Strategic Initiatives

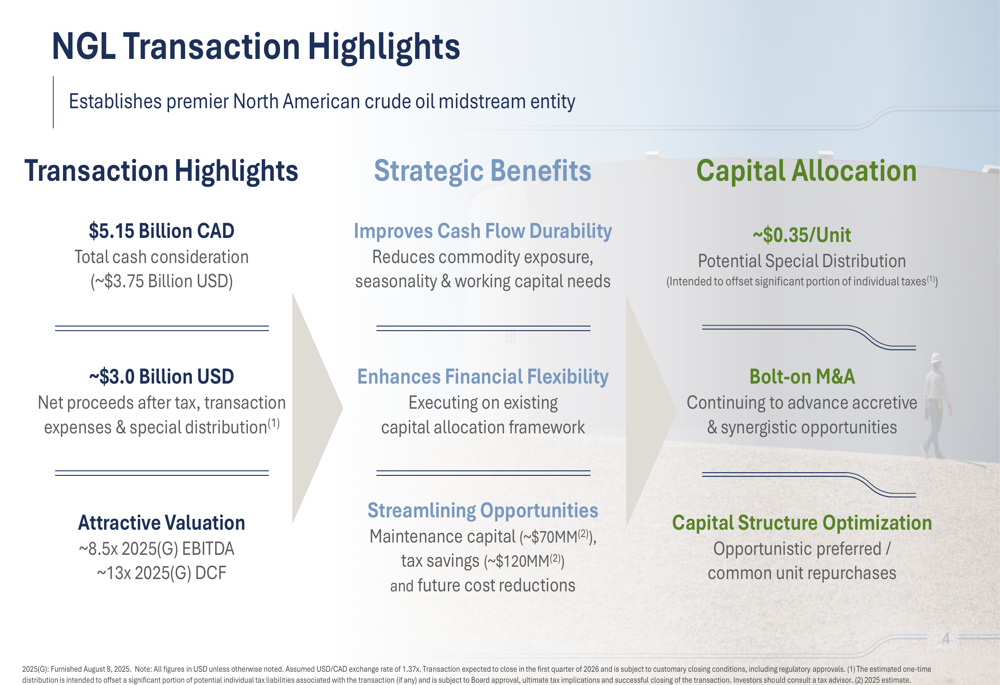

The most significant strategic development highlighted in the presentation was the divestiture of Plains’ NGL business for approximately $3.75 billion USD (CAD $5.15 billion), which is expected to generate net proceeds of approximately $3 billion after tax, transaction expenses, and a special distribution.

The company outlined several strategic benefits from this transaction:

According to the presentation, this divestiture will improve cash flow durability by reducing commodity exposure, seasonality, and working capital needs. It also enhances financial flexibility while creating streamlining opportunities that could reduce maintenance capital by approximately $70 million and generate tax savings of approximately $120 million.

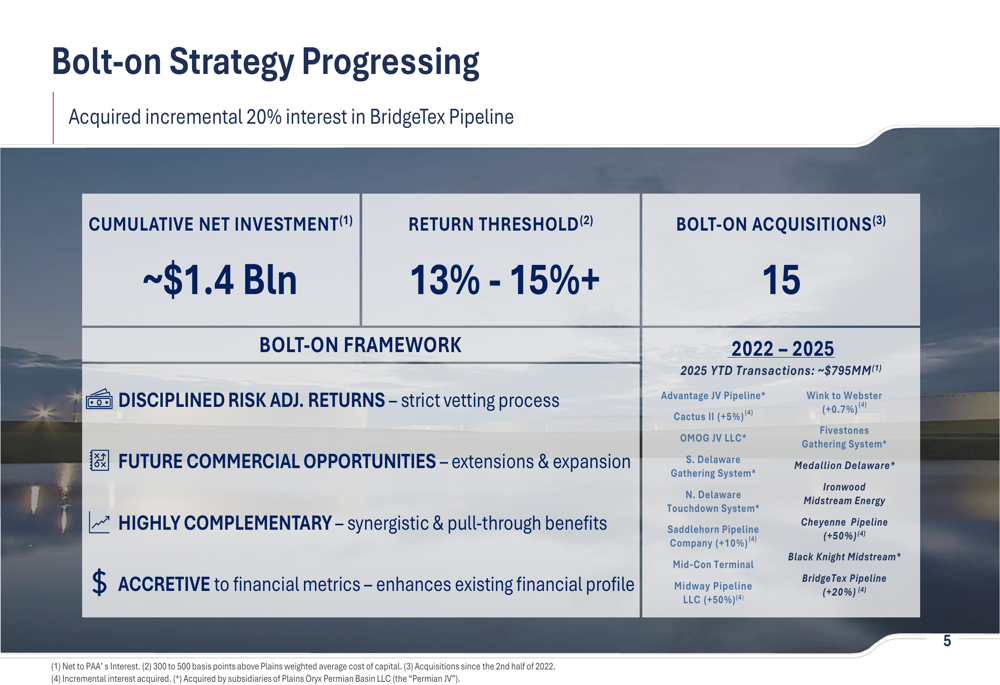

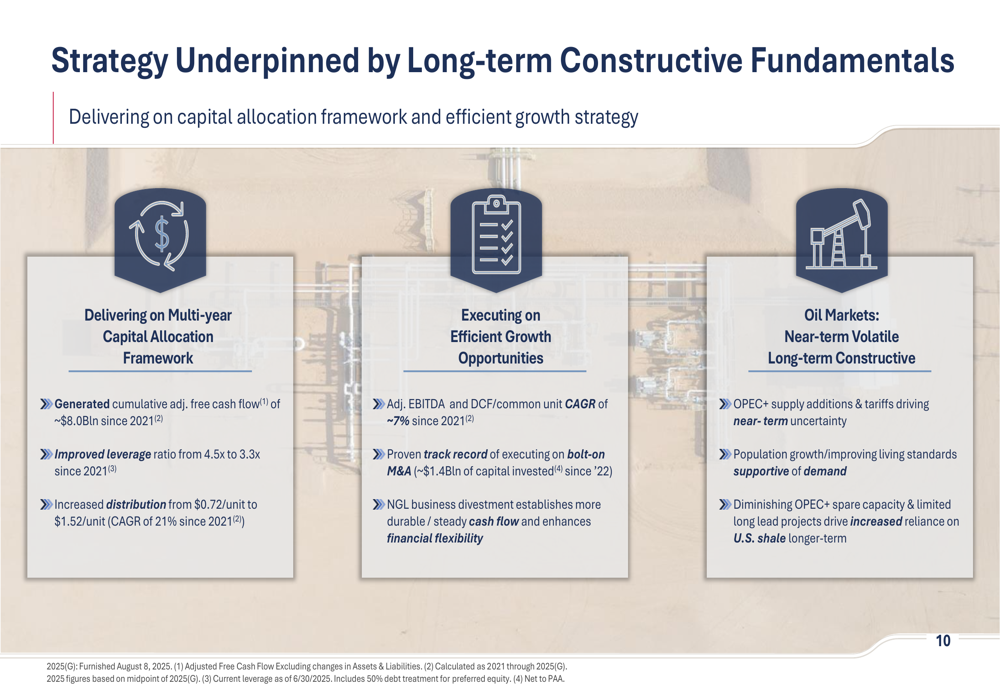

Simultaneously, Plains continues to execute its bolt-on acquisition strategy, with cumulative net investment of approximately $1.4 billion since 2022. The company has completed 15 bolt-on acquisitions during this period, targeting 13-15%+ returns.

Notable recent transactions include acquiring an additional 20% interest in BridgeTex Pipeline, which adds to the company’s Permian Basin infrastructure portfolio.

Capital Allocation & Shareholder Returns

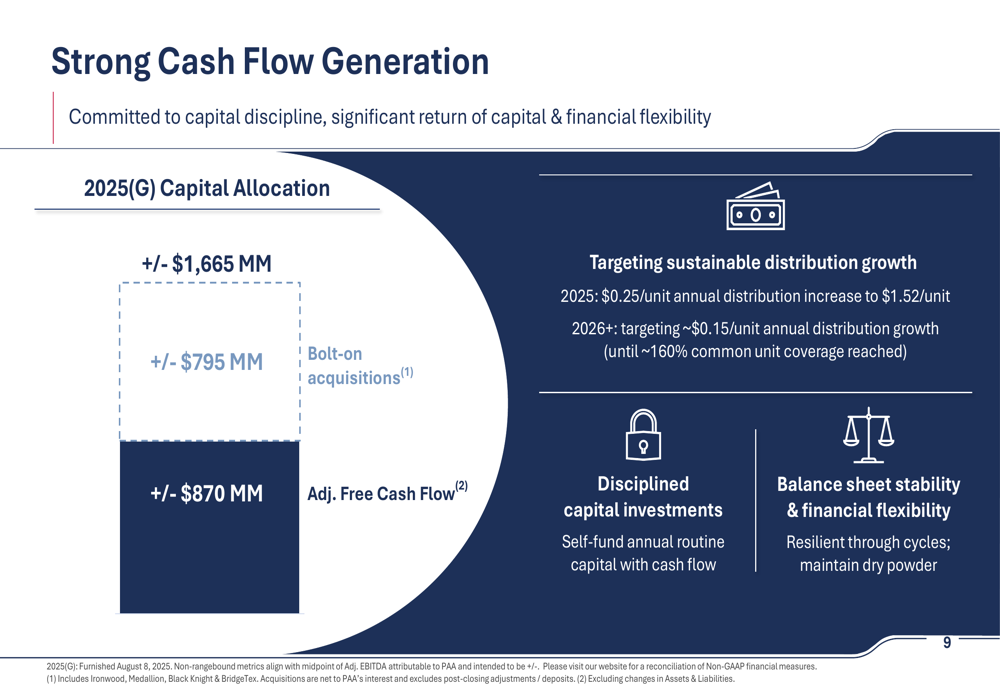

Plains outlined its capital allocation strategy for 2025, projecting approximately $1,665 million in available capital, split between bolt-on acquisitions ($795 million) and adjusted free cash flow ($870 million).

The company’s approach to shareholder returns focuses on sustainable distribution growth:

For 2025, Plains is targeting a $0.25 per unit annual distribution increase to $1.52 per unit, followed by approximately $0.15 per unit annual growth from 2026 onward. This represents significant growth from the $0.72 per unit distribution level in 2021.

The company highlighted its track record of delivering on its multi-year capital allocation framework, having generated cumulative adjusted free cash flow of approximately $8.0 billion since 2021 while improving its leverage ratio from 4.5x to 3.3x during the same period.

Forward-Looking Statements

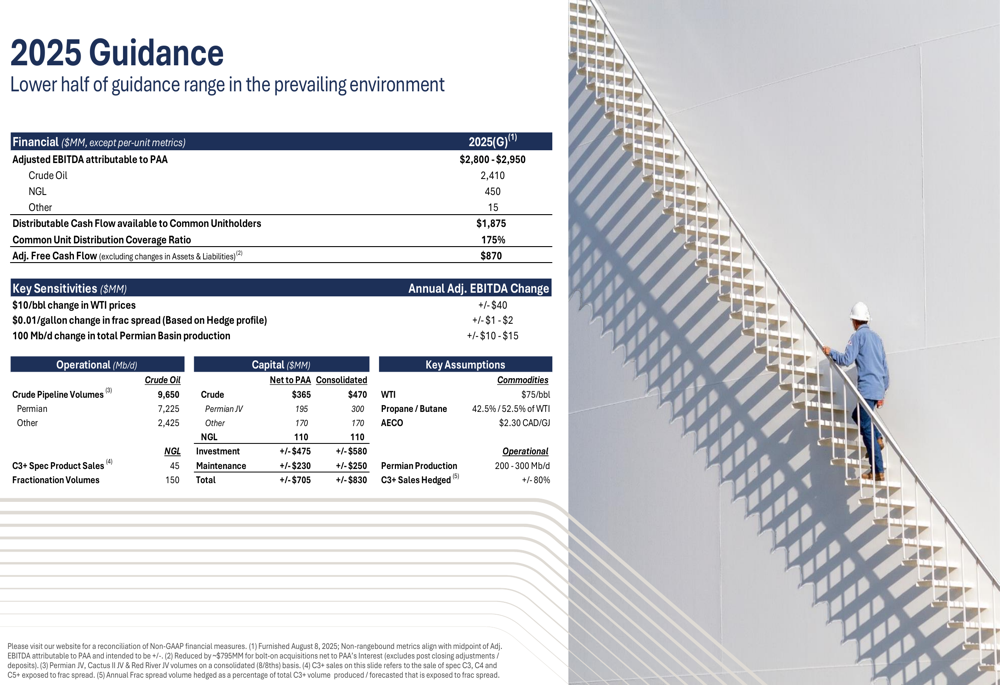

Plains maintained its full-year 2025 guidance with adjusted EBITDA attributable to PAA projected at $2.80-2.95 billion, including $2.41 billion from the crude oil segment and $450 million from the NGL segment.

The company’s detailed guidance includes key sensitivities:

Management characterized oil markets as "near-term volatile, long-term constructive," noting that OPEC+ supply additions and tariffs are driving near-term uncertainty. However, they remain optimistic about long-term fundamentals, citing population growth, improving living standards, diminishing OPEC+ spare capacity, and limited long-lead projects as factors that will drive increased reliance on U.S. shale production.

In pre-market trading following the presentation, Plains GP Holdings shares were down 0.73% to $19.15, according to market data. The stock has traded between $16.61 and $22.31 over the past 52 weeks.

With its strategic portfolio reshaping well underway and continued focus on bolt-on acquisitions, Plains appears positioned to maintain its steady performance while enhancing its financial flexibility and shareholder returns in the coming years.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.