Tesla could be a $10,000 stock in a decade, says longtime bull Ron Baron

Introduction & Market Context

Porch Group Inc. (NASDAQ:PRCH) presented its Q3 2025 earnings results on November 5, 2025, highlighting strong performance across its business segments despite ongoing housing market challenges. The company’s stock responded positively to the results, rising 9.31% in regular trading and an additional 3.35% in after-hours trading to reach $15.10.

The vertically integrated home services platform reported consolidated revenue of $118.1 million, exceeding analyst expectations of $111.13 million. However, the company posted an earnings per share (EPS) loss of $0.10, missing the forecasted loss of $0.03. Despite this miss, investors appeared to focus on the company’s robust gross profit growth and improved guidance.

Quarterly Performance Highlights

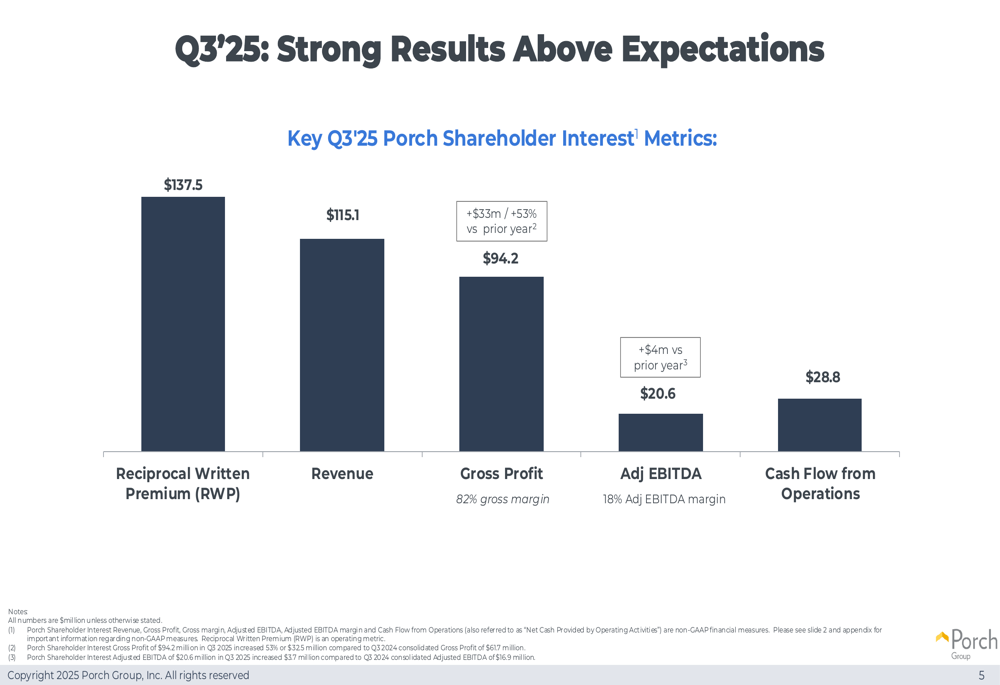

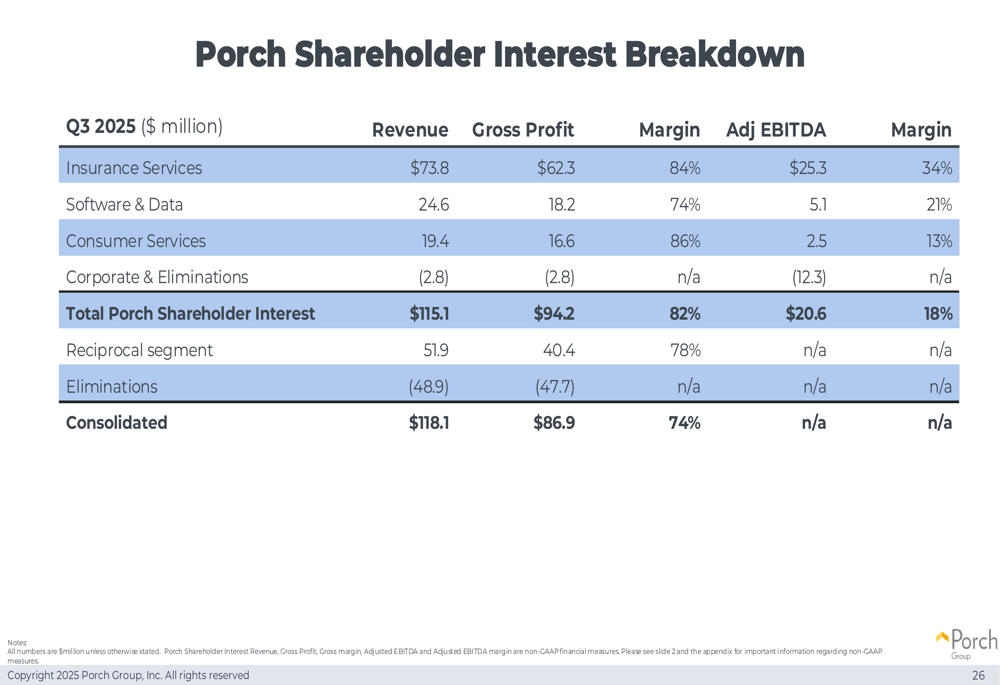

Porch Group’s Q3 2025 results demonstrated significant year-over-year improvements in key financial metrics. The company’s Porch Shareholder Interest revenue reached $115.1 million, with gross profit of $94.2 million representing an 82% margin. This gross profit figure marked a substantial increase of $33 million or 53% compared to the prior year.

As shown in the following chart of quarterly performance metrics:

Adjusted EBITDA for the quarter came in at $20.6 million, an 18% margin and $4 million higher than the previous year. The company also generated strong cash flow from operations of $28.8 million during the quarter.

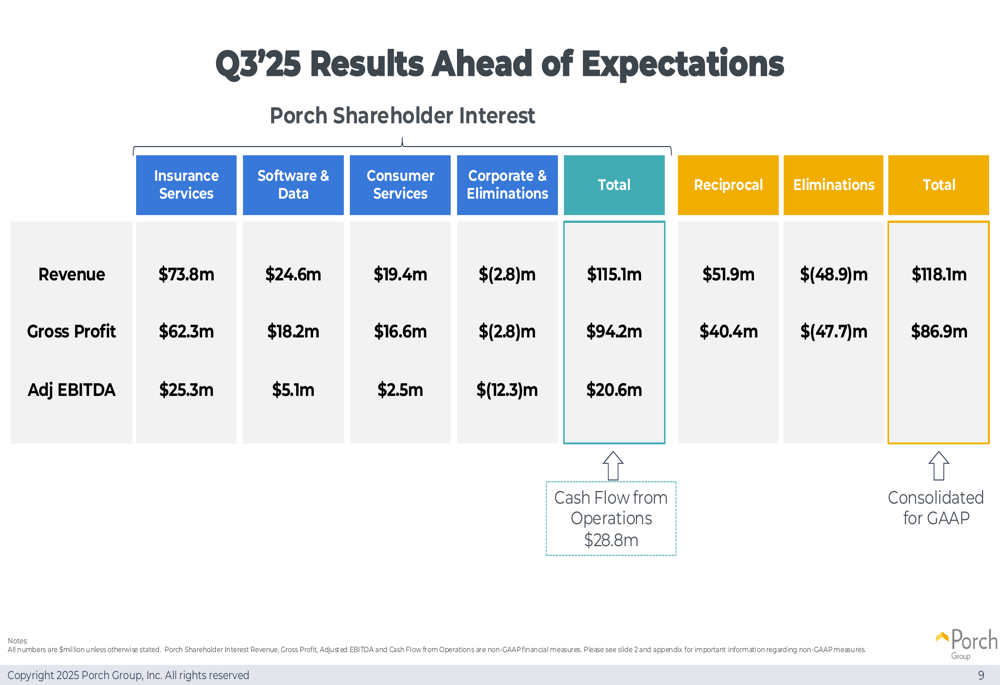

The detailed breakdown of Q3 results by segment shows the Insurance Services division leading performance:

Strategic Focus on Insurance Services

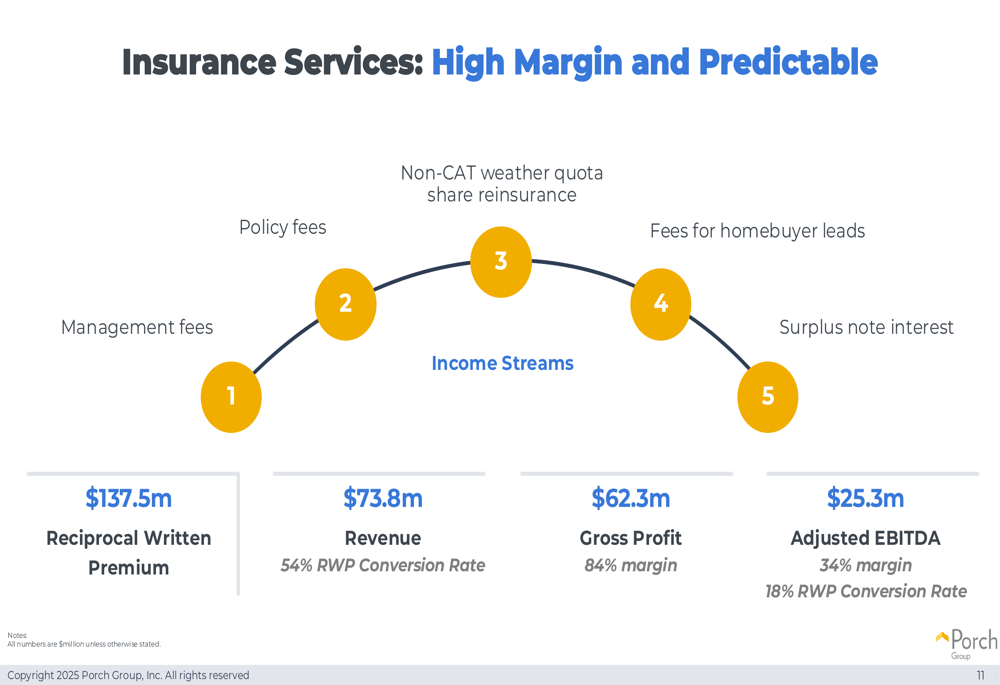

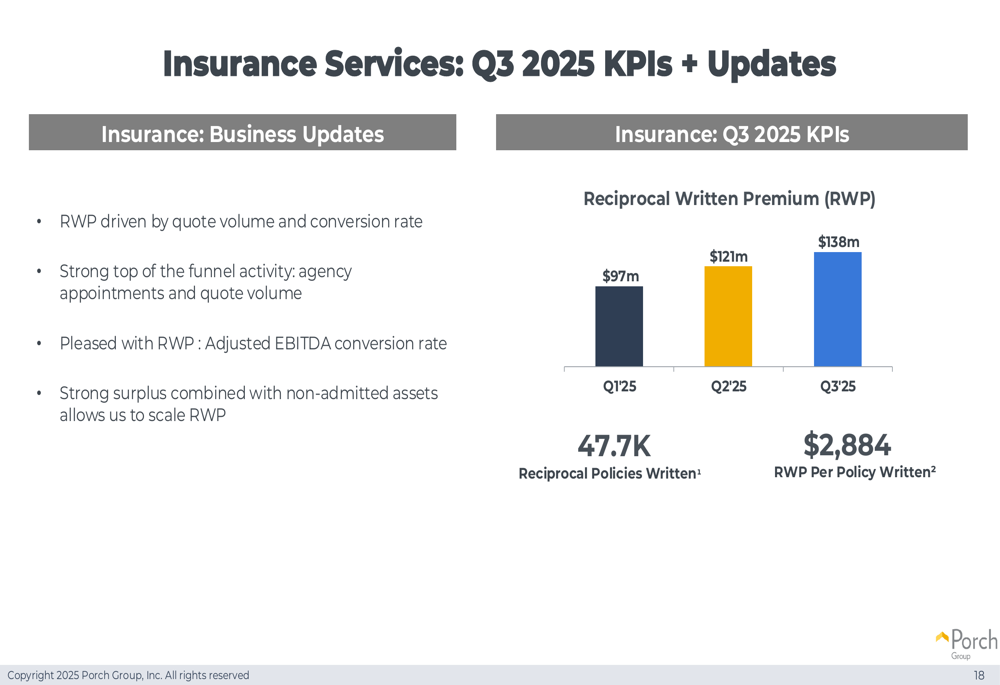

The Insurance Services segment continues to be Porch Group’s primary growth driver, generating $73.8 million in revenue with an impressive gross profit margin of 84% ($62.3 million) and adjusted EBITDA of $25.3 million (34% margin). The segment’s Reciprocal Written Premium (RWP) reached $137.5 million, with a conversion rate of 18% from RWP to Insurance Services Adjusted EBITDA.

The following image illustrates the high-margin, predictable nature of the Insurance Services business:

The company reported strong top-of-funnel activity with increasing agency appointments and quote volumes. During the quarter, Porch wrote 47,700 reciprocal policies with an average RWP per policy of $2,884.

Reciprocal Surplus Expansion

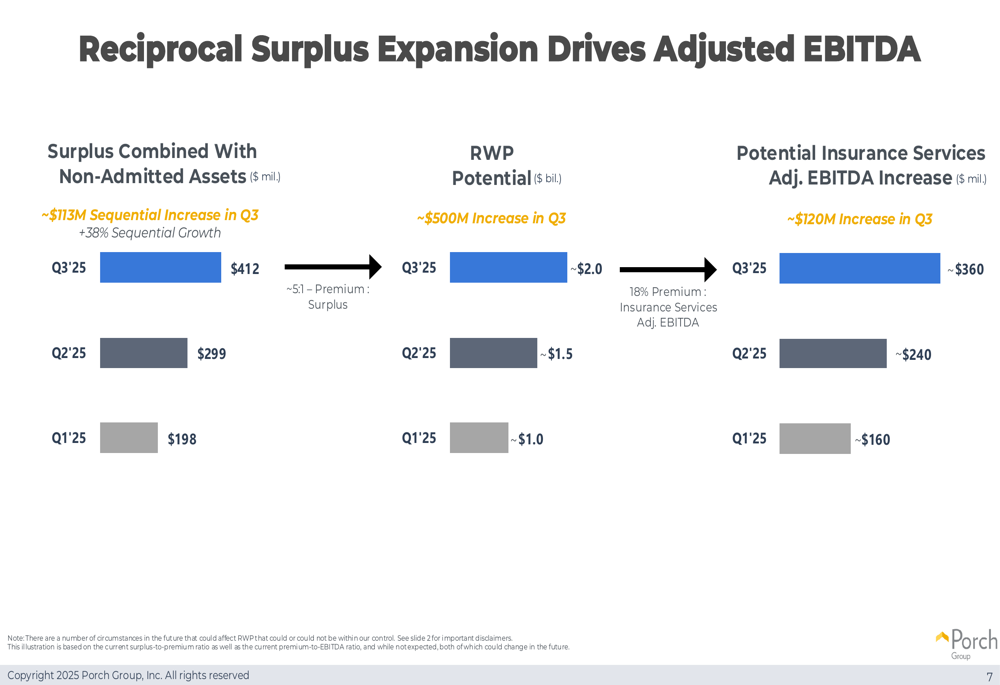

A key strategic focus for Porch Group is the expansion of its reciprocal surplus, which enables future premium growth. The company’s surplus combined with non-admitted assets grew to $412 million in Q3’25, a sequential increase of approximately $113 million from Q2’25.

This expansion of surplus is illustrated in the following chart, showing how it drives potential RWP and adjusted EBITDA growth:

With a premium-to-surplus ratio of approximately 5:1, the current surplus level could potentially support up to $2 billion in RWP, which at an 18% conversion rate could generate around $360 million in insurance services adjusted EBITDA.

Segment Performance

Beyond Insurance Services, Porch Group’s Software & Data segment delivered revenue of $24.6 million (up 7% year-over-year) with gross profit of $18.2 million (74% margin) and adjusted EBITDA of $5.1 million (21% margin). The segment serves 23,800 companies with an annualized average revenue per company of $4,140.

The company’s Consumer Services segment generated $19.4 million in revenue (up 9% year-over-year) with gross profit of $16.6 million (86% margin) and adjusted EBITDA of $2.5 million (13% margin). This segment reported 93,900 monetized services with an average revenue per service of $206.

The comprehensive breakdown of Porch Shareholder Interest by segment is shown here:

Financial Position and Guidance

Porch Group ended the quarter with $132.1 million in cash and investments. The company continued its debt reduction strategy, repurchasing $12.8 million of 2026 notes during the quarter, leaving approximately $7.8 million in remaining principal balance. The board has authorized management to repurchase the remaining 2026 notes with cash from the balance sheet.

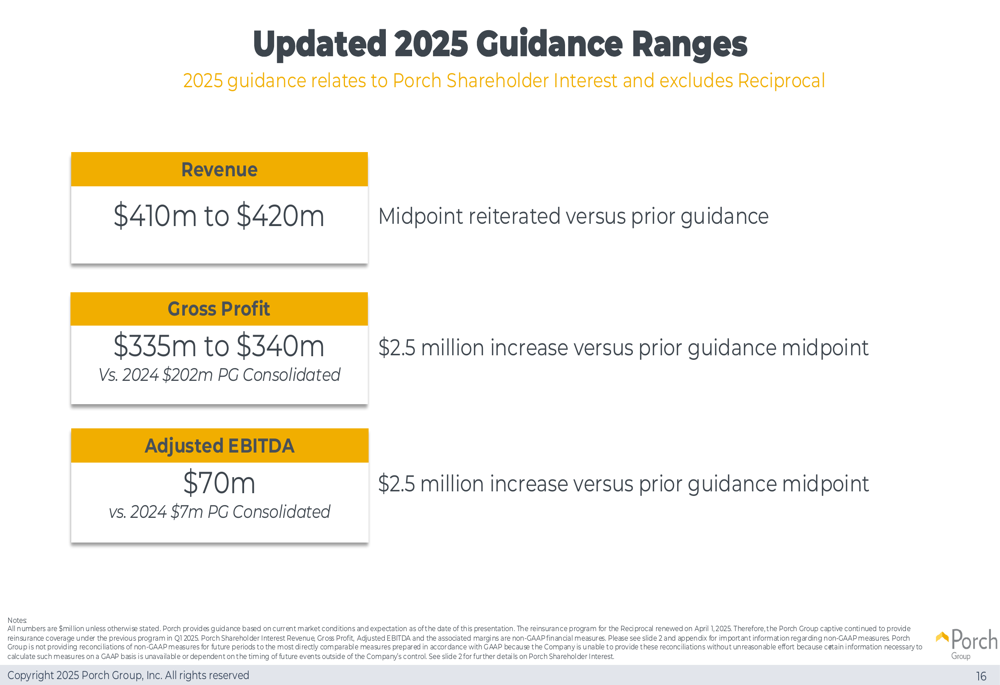

Based on strong Q3 performance, Porch Group updated its 2025 guidance:

The company maintained its revenue guidance of $410-420 million but increased its gross profit guidance to $335-340 million (up $2.5 million at the midpoint) and adjusted EBITDA guidance to $70 million (also up $2.5 million from prior guidance).

Forward-Looking Initiatives

Porch Group is making strategic investments to position itself for growth in 2026. In the Software & Data segment, the company continues to invest in product innovation, including AI capabilities, and is expanding its data business sales organization. The company now has 89 Home Factors in the market, which provide a system-wide margin advantage.

In Consumer Services, investments are focused on warranty claims management, which has seen frequency trending down more than 20% year-over-year, and expanding moving partnerships. These initiatives, combined with the potential housing market recovery, are expected to drive growth in 2026.

The Insurance Services segment’s key performance indicators show steady growth in written premiums:

CEO Matt Ehrlichman emphasized that the company has already surpassed its initial 2025 adjusted EBITDA guidance on a year-to-date basis and is well-positioned to scale RWP with robust top-of-funnel metrics. The management team expressed confidence that the seeds planted in 2025 will drive further growth in 2026, supported by the company’s advantaged underwriting capabilities and expanding Porch flywheel.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.