Gold prices tick higher on fresh U.S. tariff threats, Fed rate cut hopes

Introduction & Market Context

Portillo’s Inc (NASDAQ:PTLO) shares plummeted 16.81% on Tuesday following the release of its second quarter 2025 earnings presentation, despite reporting modest revenue growth. The stock traded at $7.90 in pre-market, approaching its 52-week low of $7.85, as investors reacted negatively to signs of slowing same-restaurant sales growth and continued margin pressure.

The Chicago-based fast-casual restaurant chain, known for its hot dogs, Italian beef sandwiches, and chocolate cake, maintained its expansion plans while navigating a challenging economic environment characterized by persistent inflation and cautious consumer spending.

Quarterly Performance Highlights

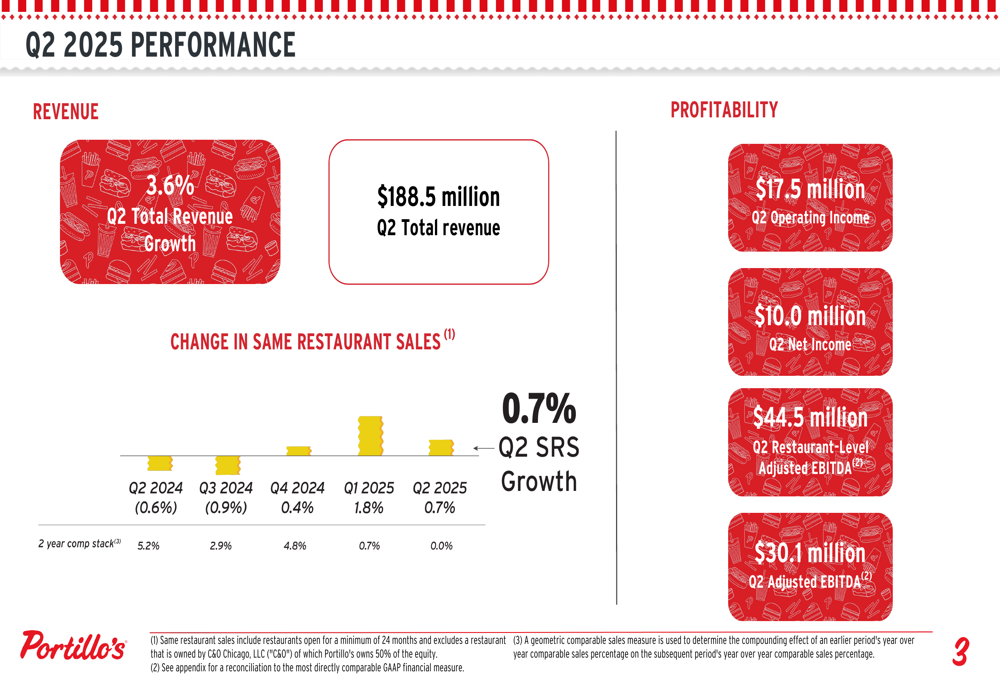

Portillo’s reported total revenue of $188.5 million for Q2 2025, representing a 3.6% increase compared to the same period last year. The company posted operating income of $17.5 million and net income of $10.0 million for the quarter.

Same-restaurant sales growth slowed significantly to 0.7% in Q2 2025, down from 1.8% in Q1 2025, indicating potential challenges in driving traffic at established locations. The two-year comparable sales stack showed 0.0% growth, suggesting stagnation in longer-term performance trends.

As shown in the following chart of quarterly performance metrics:

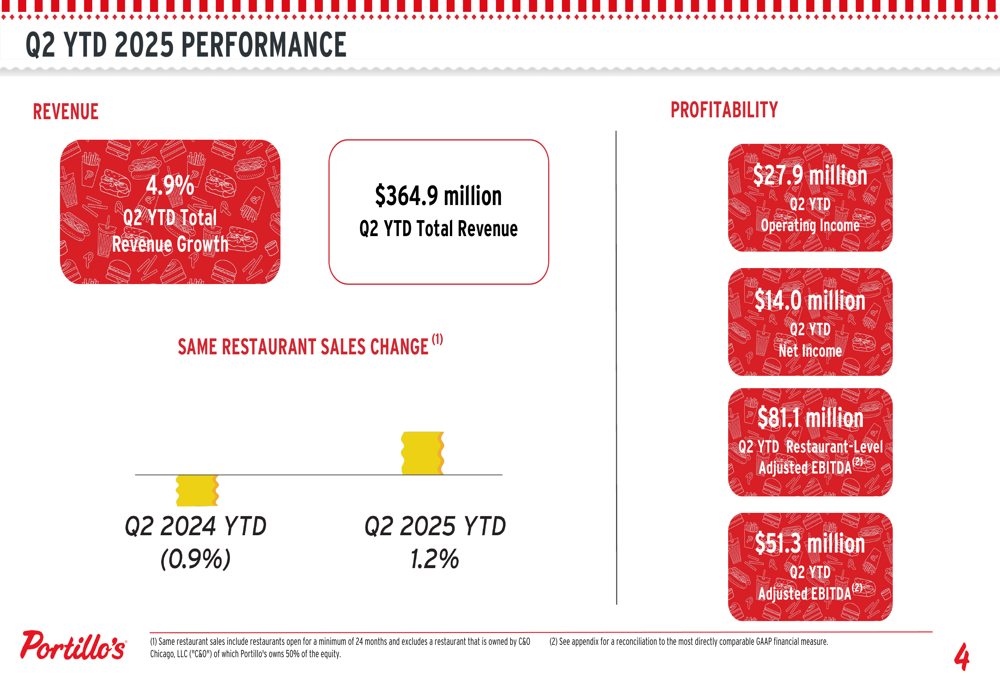

For the first half of 2025, Portillo’s reported year-to-date revenue of $364.9 million, a 4.9% increase over the prior year period. Operating income for the first six months reached $27.9 million, with net income of $14.0 million.

The year-to-date same-restaurant sales increase of 1.2% falls at the lower end of the company’s full-year guidance range of 1-3%, highlighting the deceleration in the second quarter:

Expansion Strategy

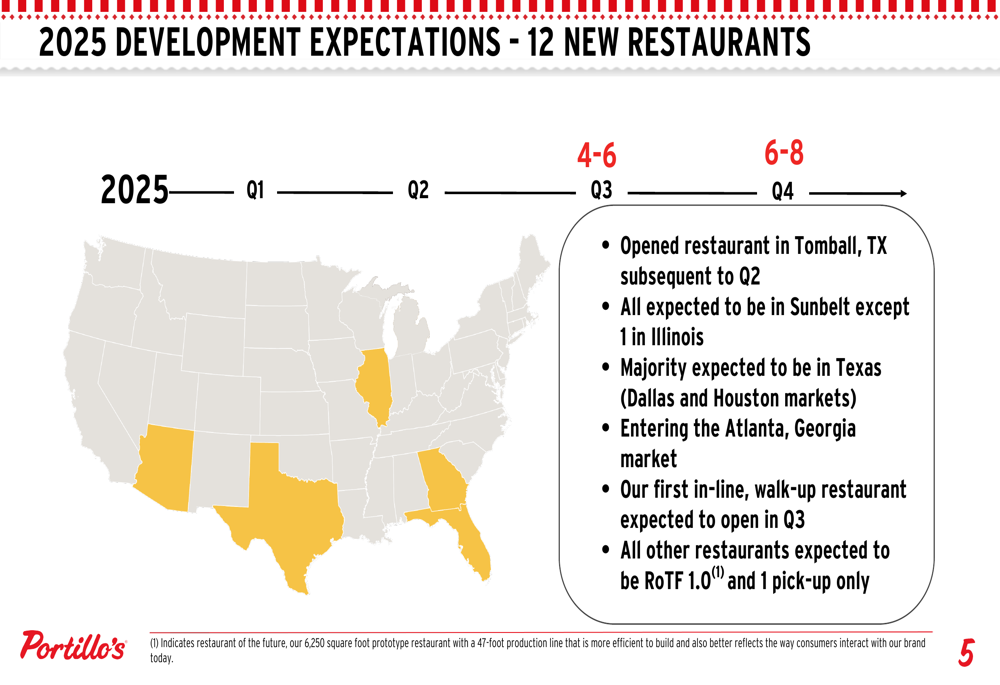

Despite the challenging operating environment, Portillo’s is maintaining its aggressive expansion strategy, with plans to open 12 new restaurants in 2025. The company expects 4-6 new locations to open in Q3, followed by 6-8 in Q4.

The expansion is heavily focused on the Sunbelt region, with the majority of new restaurants planned for Texas markets (Dallas and Houston). Portillo’s also announced its entry into the Atlanta, Georgia market and plans to open its first in-line, walk-up restaurant format in Q3, potentially testing a more cost-effective expansion model.

The company’s development strategy is illustrated in this geographic expansion map:

Financial Outlook

Portillo’s maintained its fiscal 2025 financial targets despite the slowing same-restaurant sales growth. The company continues to project 1-3% same-restaurant sales growth and 5-7% total revenue growth for the full year.

However, the presentation highlighted significant inflationary pressures, with commodity inflation expected at 3-5% and labor inflation at 3-4% for the year. These cost pressures are likely contributing to the projected compression in Restaurant-Level Adjusted EBITDA margin to 22.5-23%, down from 23.7% in fiscal 2024.

The company’s detailed financial targets for fiscal 2025 are outlined in this comprehensive guidance slide:

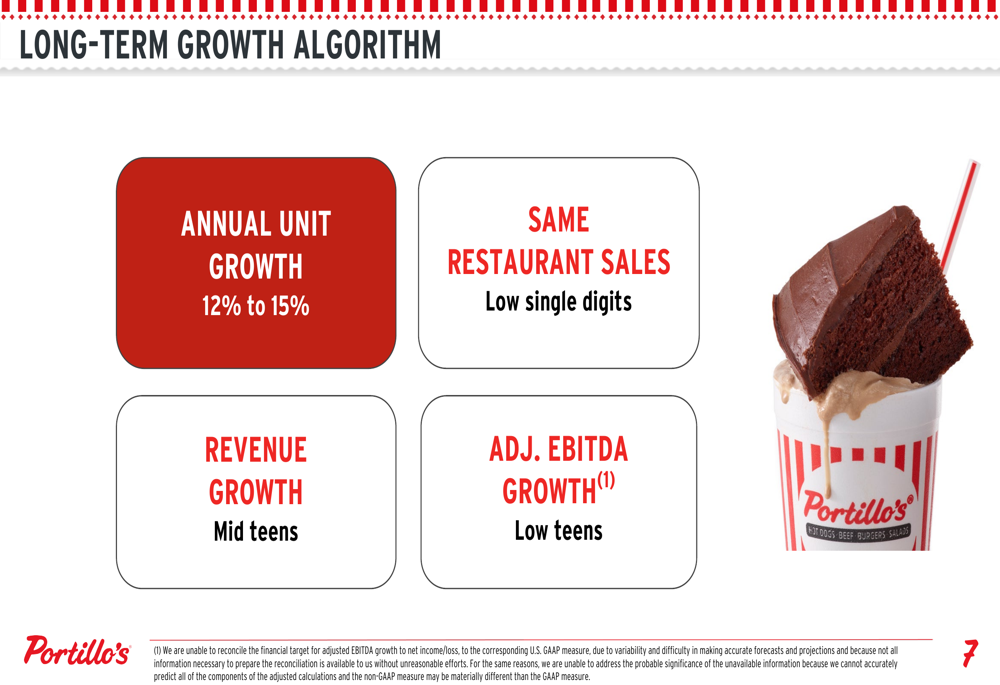

Looking beyond 2025, Portillo’s reiterated its long-term growth algorithm, targeting 12-15% annual unit growth and low single-digit same-restaurant sales increases. This strategy aims to deliver mid-teens revenue growth and low-teens Adjusted EBITDA growth over time:

Strategic Initiatives

The presentation emphasized four strategic pillars guiding Portillo’s business approach: running world-class operations, innovating the customer experience, developing restaurants with industry-leading returns, and taking care of team members.

These strategic priorities reflect the company’s focus on balancing growth with operational excellence in an increasingly competitive restaurant landscape:

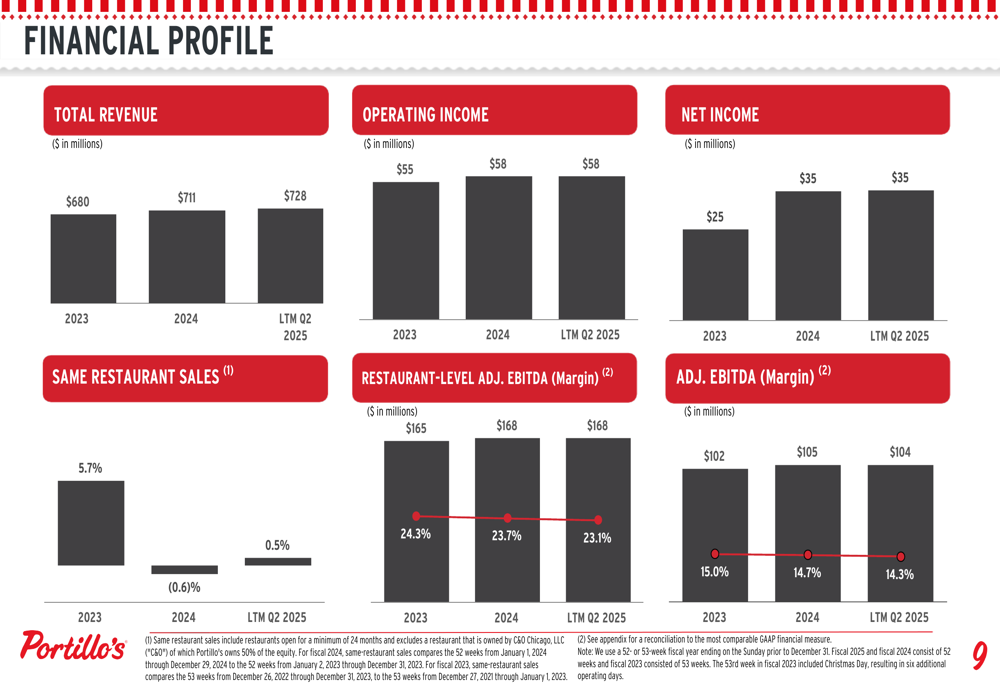

Margin Pressure and Financial Trends

A concerning trend evident in the presentation is the gradual erosion of profit margins over time. The company’s financial profile shows Restaurant-Level Adjusted EBITDA margin declining from 24.3% in 2023 to 23.7% in 2024 and further to 23.1% for the last twelve months ended Q2 2025.

Similarly, Adjusted EBITDA margin has contracted from 15.0% in 2023 to 14.3% in the most recent period, suggesting ongoing challenges in maintaining profitability amid rising costs:

Market Reaction and Outlook

The steep 16.81% decline in Portillo’s stock price following the earnings presentation suggests investors are increasingly concerned about the company’s ability to maintain growth while preserving margins in the current economic environment.

The slowdown in same-restaurant sales growth from 1.8% in Q1 to 0.7% in Q2, combined with ongoing margin compression, appears to have overshadowed the company’s continued revenue growth and expansion plans.

Looking ahead, Portillo’s faces the dual challenge of accelerating same-restaurant sales while managing inflationary pressures to protect margins. The success of its expansion strategy, particularly in new markets like Atlanta and with new restaurant formats, will be critical in determining whether the company can deliver on its long-term growth algorithm.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.