5 big analyst AI moves: Apple lifted to Buy, AI chip bets reassessed

Introduction & Market Context

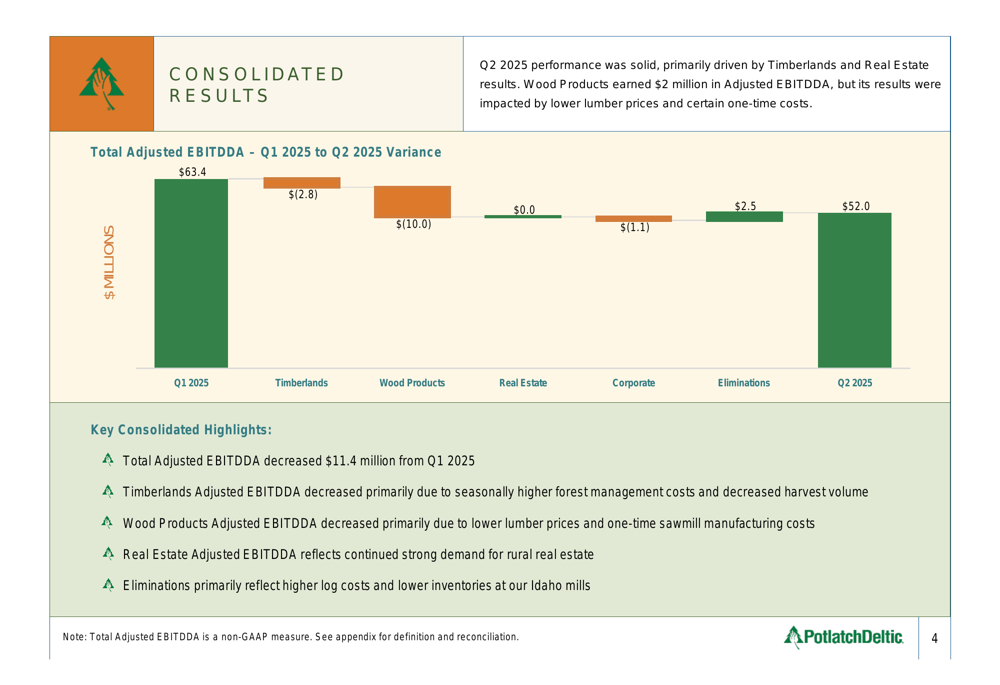

PotlatchDeltic Corporation (NASDAQ:PCH) reported its second quarter 2025 results on July 29, showing a decline in adjusted EBITDA despite achieving record lumber shipments. The timber and wood products company posted total adjusted EBITDA of $52.0 million, down from $63.4 million in the first quarter, primarily due to challenges in its Wood Products segment.

Despite the quarterly decline, investors responded positively to management’s optimistic outlook for the third quarter, sending shares up 4.83% in aftermarket trading to $43.65. The company’s strategic focus on returning capital to shareholders through dividends and share repurchases continues to be a priority, with a current dividend yield of 4.7%.

Quarterly Performance Highlights

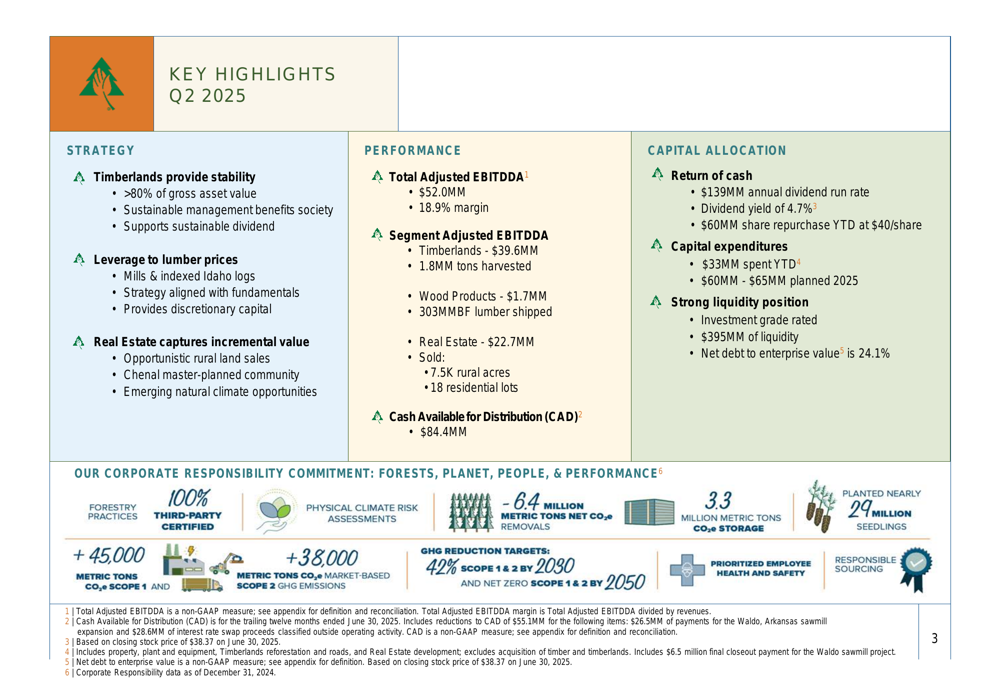

PotlatchDeltic’s Q2 2025 performance showed mixed results across its business segments. Total adjusted EBITDA reached $52.0 million with an 18.9% margin, as highlighted in the company’s presentation.

As shown in the following comprehensive overview of the quarter’s key metrics:

The company’s performance breakdown by segment reveals the challenges faced in the quarter:

- Timberlands: $39.6 million adjusted EBITDA (1.8 million tons harvested)

- Wood Products: $1.7 million adjusted EBITDA (303 MMBF lumber shipped)

- Real Estate: $22.7 million adjusted EBITDA (7,457 rural acres and 18 residential lots sold)

The following waterfall chart illustrates how each segment contributed to the $11.4 million decrease in total adjusted EBITDA from Q1 to Q2 2025:

Detailed Financial Analysis

The Wood Products segment experienced the most significant decline, with adjusted EBITDA falling from $11.7 million in Q1 to just $1.7 million in Q2, a $10.0 million decrease. This drop occurred despite lumber shipments reaching a quarterly record of 303 million board feet, up from 290 million in Q1.

The following chart breaks down the factors contributing to the Wood Products segment’s performance decline:

Average lumber prices decreased 1% to $450 per thousand board feet (MBF) in Q2, while the segment was also impacted by a $3.0 million lumber inventory charge and $2.8 million in one-time costs related to equipment upgrades at the St. Maries facility and a temporary power supply issue at the Waldo operation.

The lumber pricing and shipment trends can be seen in this chart:

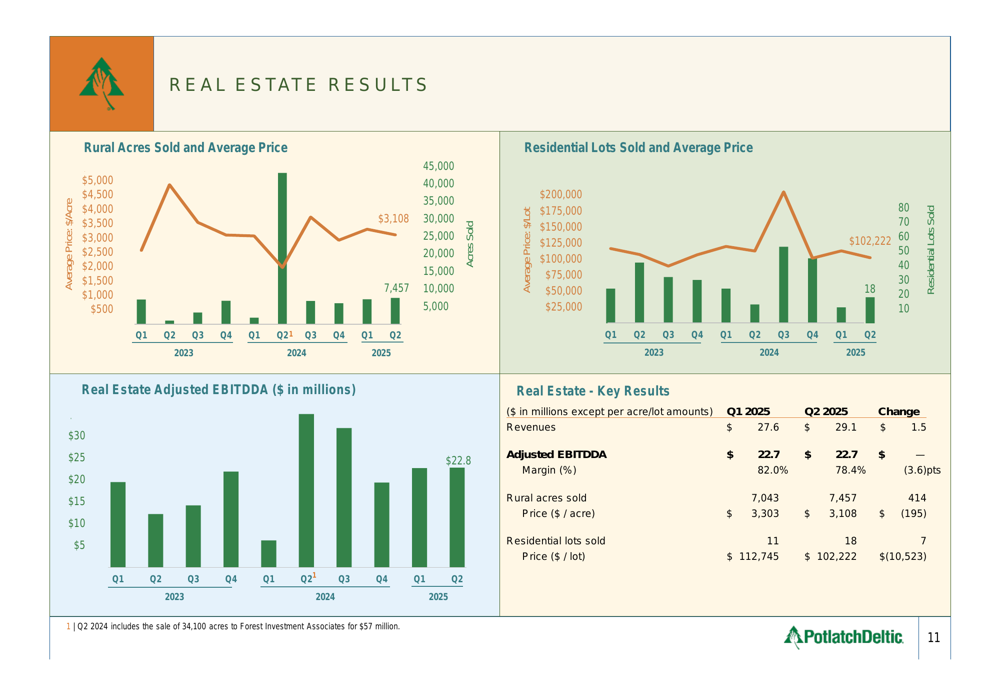

The Real Estate segment maintained stable performance with adjusted EBITDA unchanged at $22.7 million, despite slight variations in the mix of properties sold. Rural land sales remained strong with 7,457 acres sold at an average price of $3,108 per acre, while 18 residential lots were sold at an average price of $102,222 per lot.

The following chart shows the Real Estate segment’s performance metrics:

Strategic Initiatives & Capital Allocation

PotlatchDeltic continues to prioritize shareholder returns while maintaining a strong balance sheet. The company reported Cash Available for Distribution (CAD) of $84.4 million and has returned significant capital to shareholders through:

- $139 million annual dividend run rate (4.7% yield)

- $60 million in share repurchases year-to-date at an average price of $40 per share

Capital expenditures totaled $33 million year-to-date, with $60-65 million planned for the full year 2025.

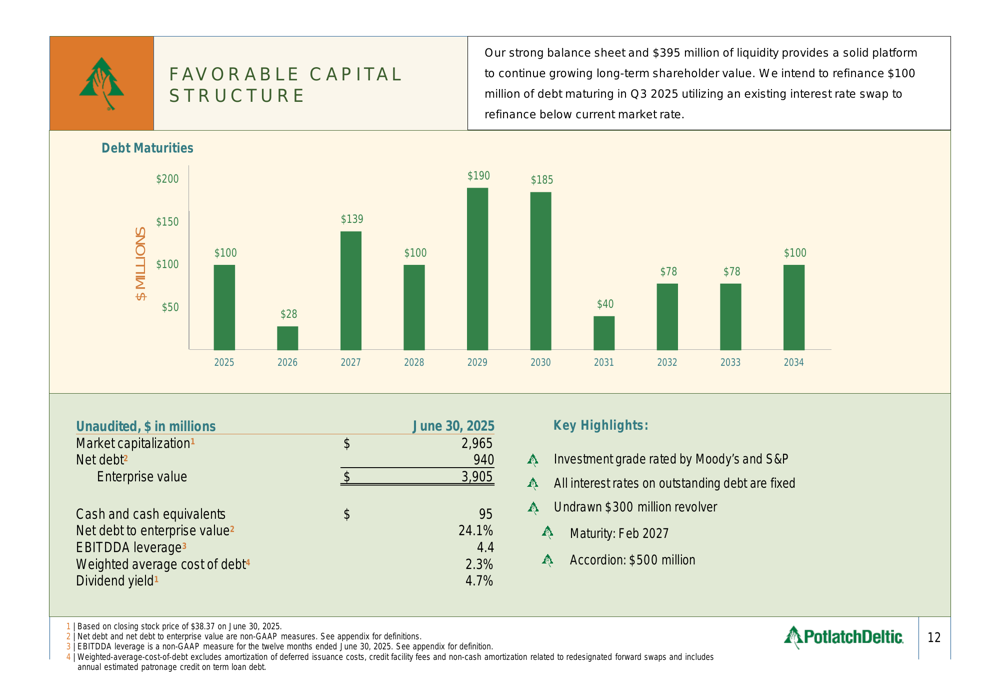

The company’s capital structure remains favorable with investment-grade ratings from Moody’s and S&P. All outstanding debt carries fixed interest rates, and the company maintains $395 million in liquidity, including an undrawn $300 million revolving credit facility.

The following chart details the company’s debt maturity profile:

Forward-Looking Statements

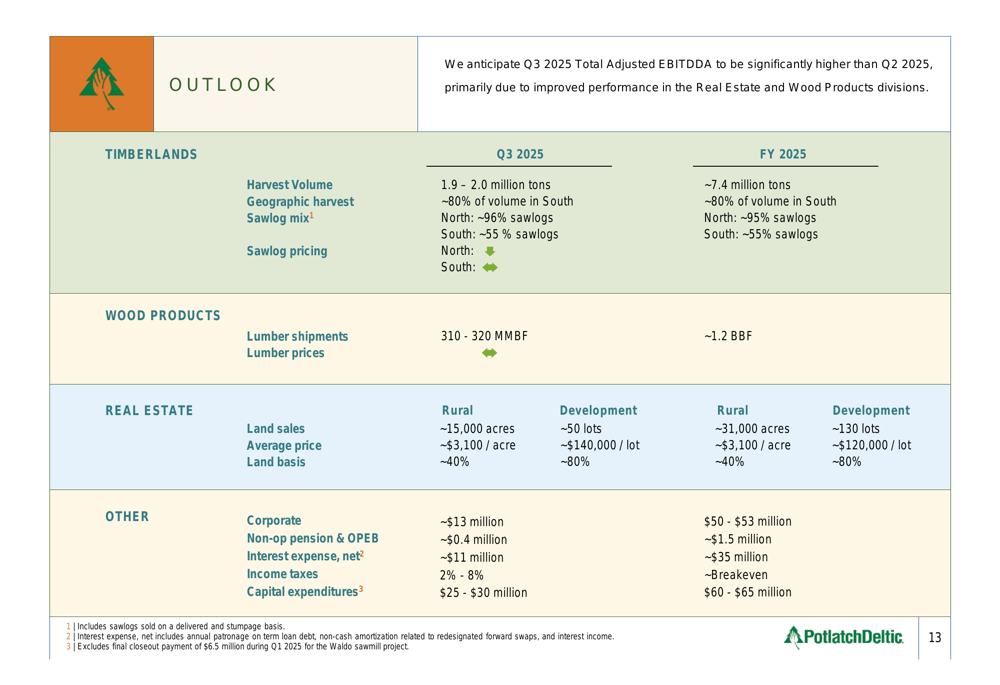

PotlatchDeltic provided an optimistic outlook for Q3 2025, projecting significantly higher adjusted EBITDA compared to Q2. This positive guidance was a key factor in the stock’s 4.83% rise in aftermarket trading following the earnings release.

Key elements of the Q3 outlook include:

- Timber harvest of 1.9-2.0 million tons (approximately 80% in the South)

- Lumber shipments of 310-320 million board feet

- Rural land sales of approximately 15,000 acres at around $3,100 per acre

- Development sales of approximately 50 lots at around $140,000 per lot

According to the earnings call transcript, CEO Eric Creamers expressed optimism about lumber prices, stating: "We think July is the low point for the year. We think we’ll be potentially $50 higher in September." He also noted that "demand for rural land has never been higher."

The detailed outlook for Q3 and full-year 2025 is presented in this comprehensive guidance table:

Analyst Perspectives

Market analysts have focused on PotlatchDeltic’s ability to navigate the challenging lumber market while leveraging its diversified business model. The company’s timberland assets (representing over 80% of gross asset value) continue to provide stability, while the real estate segment captures incremental value.

According to InvestingPro analysis, PotlatchDeltic maintains a FAIR financial health score of 2.39, with particularly strong cash flow metrics. The stock currently trades near its InvestingPro Fair Value, suggesting balanced market pricing despite recent volatility.

Analysts during the earnings call questioned management about the potential impact of lumber tariffs and market dynamics, as well as the company’s capital allocation strategy. Management’s focus on share repurchases to enhance shareholder value appears to have resonated positively with investors, as evidenced by the stock’s performance following the earnings release.

With lumber prices expected to recover in the coming months and continued strong demand for rural land, PotlatchDeltic appears positioned to deliver improved results in the second half of 2025, though economic uncertainty and housing market fluctuations remain potential headwinds.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.