Asia FX moves little with focus on US-China trade, dollar steadies ahead of CPI

Introduction & Market Context

Primerica, Inc. (NYSE:PRI) released its second quarter 2025 earnings presentation on August 7, revealing solid financial performance despite mixed operational results. The financial services company reported adjusted operating earnings per share of $5.46, exceeding analyst expectations of $5.20, yet saw its stock decline 4.38% to $255.46 following the announcement.

The company, which positions itself as a sales and distribution leader for financial products serving middle-income families, demonstrated strength in its Investment and Savings Products (ISP) segment while facing headwinds in its Term Life business. This performance occurred against a backdrop of economic uncertainty that CEO Glenn Williams acknowledged during the earnings call.

Quarterly Performance Highlights

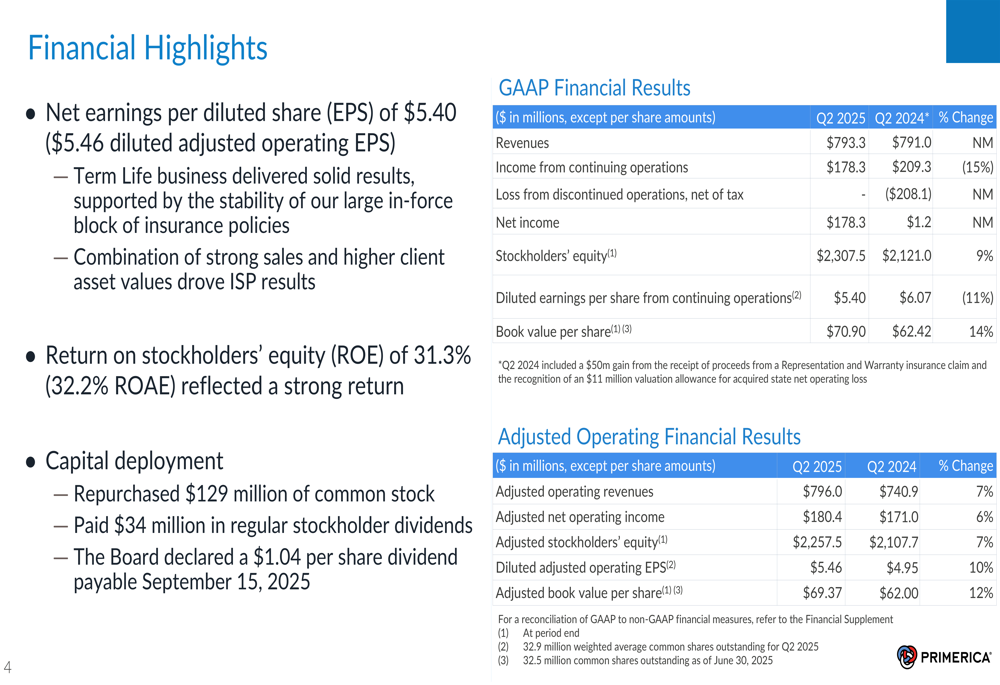

Primerica delivered adjusted operating revenues of $796.0 million in Q2 2025, a 7.4% increase from $740.9 million in the same period last year. Adjusted net operating income reached $180.4 million, up 5.5% from $171.0 million in Q2 2024.

The company reported GAAP diluted earnings per share of $5.40, compared to $6.07 in the prior-year period, while adjusted operating EPS rose 10.3% to $5.46 from $4.95. Return on stockholders’ equity remained robust at 31.3% (32.2% on an adjusted basis).

As shown in the following financial highlights table from the presentation:

Primerica maintained its commitment to shareholder returns, repurchasing $129 million of common stock and paying $34 million in stockholder dividends during the quarter. The company also declared a quarterly dividend of $1.04 per share.

Distribution and Sales Force Analysis

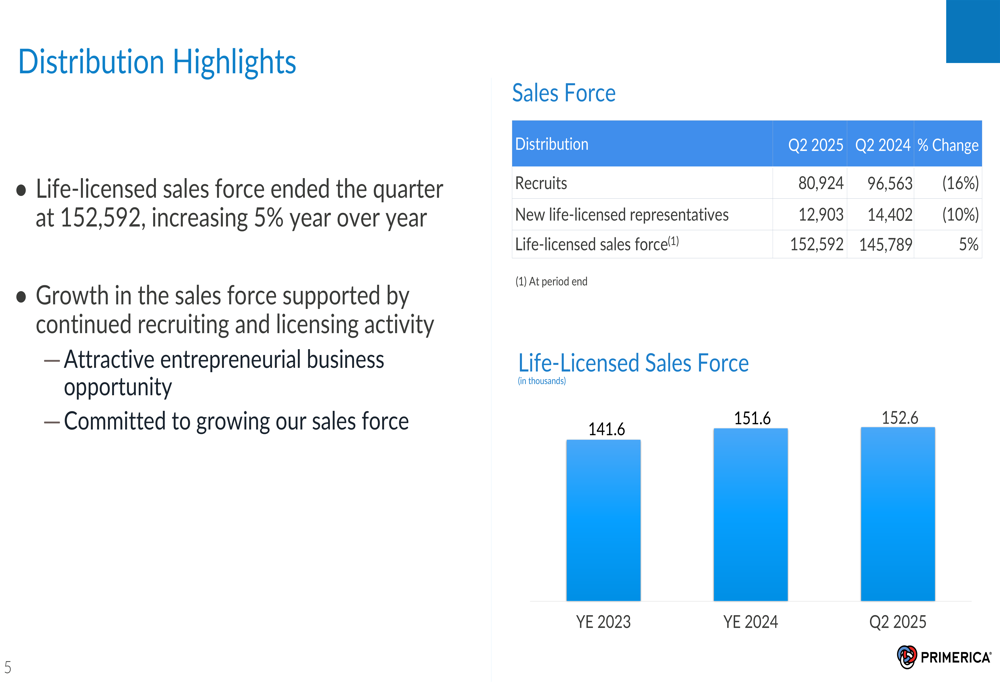

A key strength for Primerica continues to be its expanding sales force, which grew 5% year-over-year to 152,592 life-licensed representatives. However, recruiting and new licensing activities showed signs of pressure, with recruits declining 16% to 80,924 and new life-licensed representatives decreasing 10% to 12,903 compared to Q2 2024.

The following chart illustrates the consistent growth in Primerica’s life-licensed sales force:

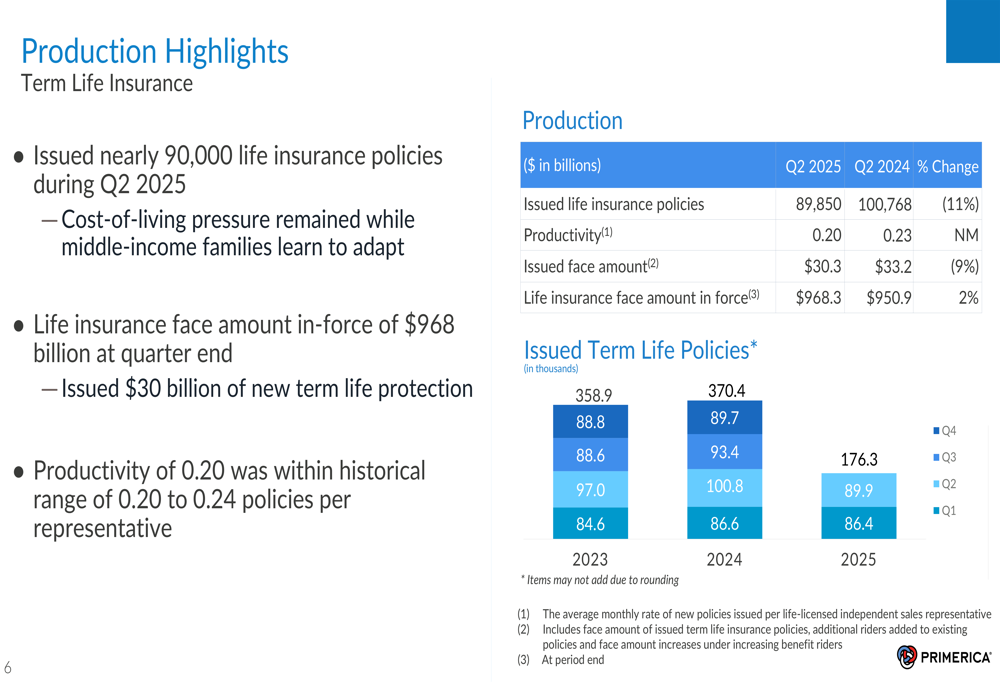

Despite the larger sales force, productivity metrics showed some weakness. Term life insurance productivity fell to 0.20 policies per representative from 0.23 in the prior-year period, contributing to an 11% decline in issued life insurance policies (89,850 versus 100,768 in Q2 2024).

Segment Performance

Term Life Insurance (NSE:LIFI)

Primerica’s Term Life segment showed modest growth, with operating revenues increasing 3% to $441.8 million and operating income before taxes rising 5% to $155.0 million. Adjusted direct premiums grew 5% year-over-year to $673.9 million, reflecting the ongoing value of the company’s in-force business.

The presentation highlighted that while lapse rates remained elevated compared to long-term expectations, mortality experience continued to be favorable. The benefits and claims ratio held steady at 57.5%, compared to 57.4% in Q2 2024.

The following chart shows the quarterly trend in issued term life policies:

Despite the quarterly decline in new policies, Primerica’s life insurance face amount in force grew 2% to $968.3 billion, underscoring the long-term stability of the company’s core business.

Investment and Savings Products

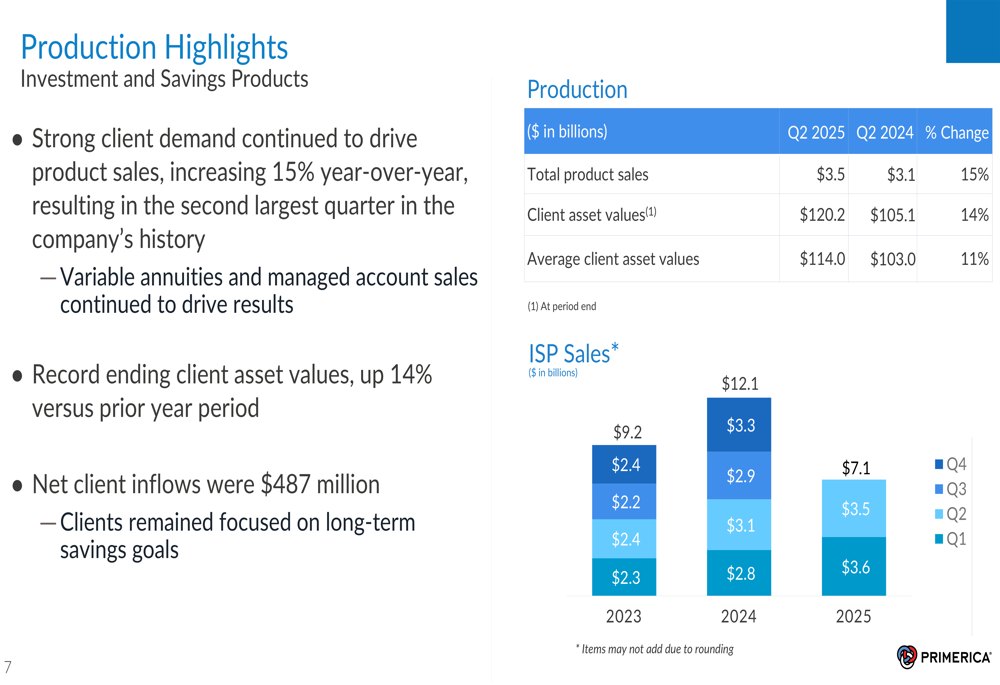

The ISP segment emerged as the growth driver for Primerica in Q2 2025, with total operating revenues increasing 14% to $298.3 million and operating income before taxes rising 6% to $79.4 million. Product sales grew 15% year-over-year to $3.5 billion, while client asset values reached a record $120.2 billion, up 14% from Q2 2024.

The strong performance was driven by increased demand for variable annuities and managed accounts, as illustrated in the following chart showing consistent growth in ISP sales:

Sales-based revenues increased 15% to $115.9 million, while asset-based revenues grew 17% to $154.7 million, benefiting from the 11% increase in average client asset values. This performance aligns with CEO Williams’ comment that "despite continued economic and government policy uncertainty, our investment clients remain committed to their long-term savings goals."

Financial Position and Expense Management

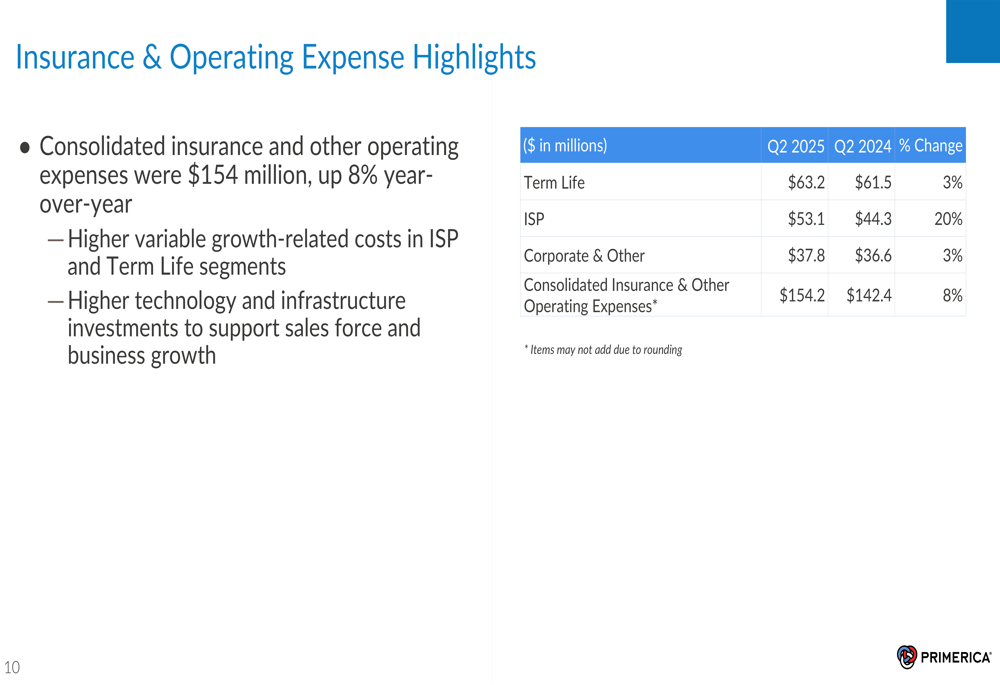

While Primerica demonstrated strong top-line growth, expenses increased at a faster rate in some areas. Consolidated insurance and other operating expenses rose 8% year-over-year to $154.2 million, with the ISP segment experiencing a 20% increase in expenses to $53.1 million.

The company attributed the higher expenses to variable growth-related costs in both the ISP and Term Life segments, as well as increased technology and infrastructure investments to support sales force and business growth.

Primerica maintained a strong financial position with adjusted stockholders’ equity of $2.26 billion, up from $2.11 billion in the prior-year period. Adjusted book value per share increased to $69.37 from $62.00 a year ago.

Forward-Looking Statements

According to the earnings call transcript, Primerica projects continued strength in its ISP segment, with sales expected to rise above 10% for the full year 2025. However, the company anticipates a 5% decline in total new life policies for the year, reflecting ongoing challenges in that segment.

Management also forecasted expense increases of approximately $40 million and expects the benefit and claims ratio to remain around 58%. These projections, combined with analysts’ downward revisions of future earnings expectations, may help explain the stock’s negative reaction despite the quarterly earnings beat.

The company’s presentation emphasized its positioning to continue creating stockholder value through its capital-light business model, complementary business segments, and focus on the underserved middle-income market. However, investors appear to be weighing these strengths against the challenges in new policy issuance and rising expenses.

As Primerica navigates economic uncertainty, its diversified business model—with strength in investment products offsetting challenges in insurance—demonstrates the resilience that has helped the company maintain dividend payments for 16 consecutive years.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.