Street Calls of the Week

Introduction & Market Context

Protector Forsikring ASA (OB:PROT) presented its Q3 2025 interim results on October 23, 2025, highlighting strong profitability metrics despite modest premium growth. The Norwegian insurer’s stock fell 7.68% following the announcement, closing at 462.5, as investors appeared concerned about the company’s growth trajectory despite solid financial performance.

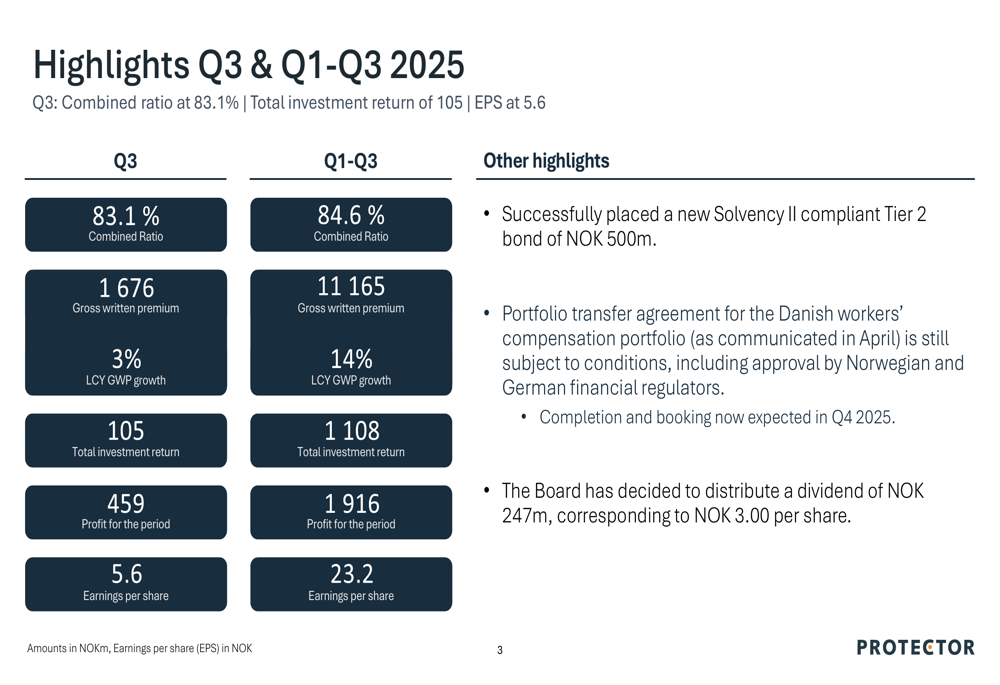

The company, which positions itself as "The Challenger" in the insurance market, delivered a combined ratio of 83.1% in Q3 2025, significantly outperforming its target of maintaining this key profitability metric below 91% in commercial sectors. However, premium growth was limited to just 3% in local currency terms during what the company described as "a small volume quarter."

Quarterly Performance Highlights

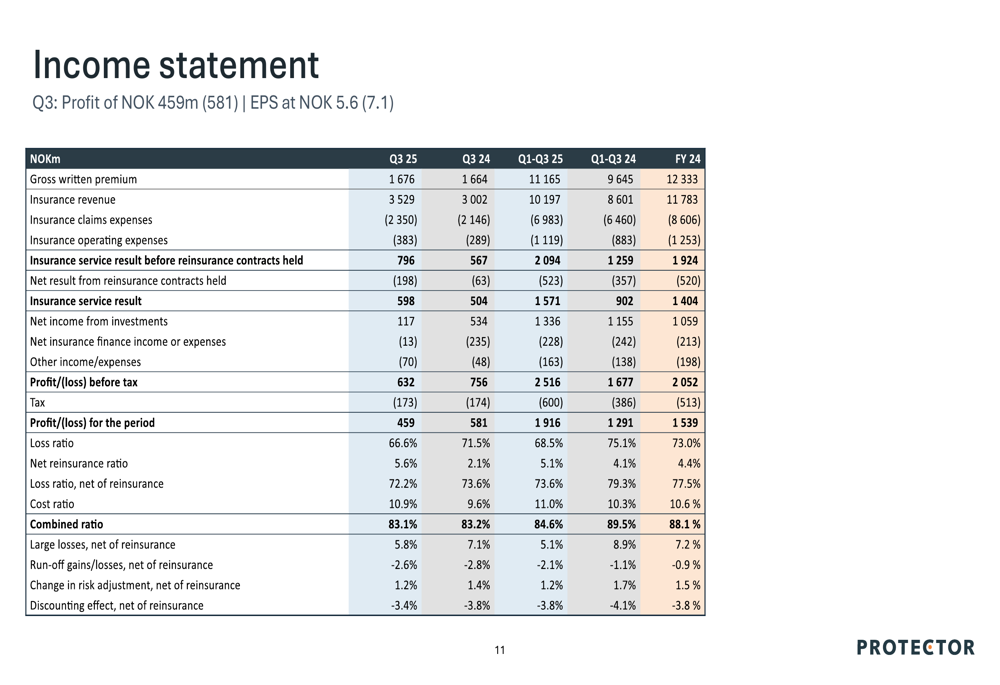

Protector reported a profit of 459 million Norwegian kroner (NOK) for Q3 2025, translating to earnings per share of 5.6 NOK. For the first nine months of 2025, profit reached 1,916 million NOK with earnings per share of 23.2 NOK.

The company’s Q3 gross written premium (GWP) amounted to 1,676 million NOK, representing modest growth of 3% in local currency terms. Year-to-date GWP reached 11,165 million NOK, reflecting stronger growth of 14% compared to the same period last year.

As shown in the following financial highlights table:

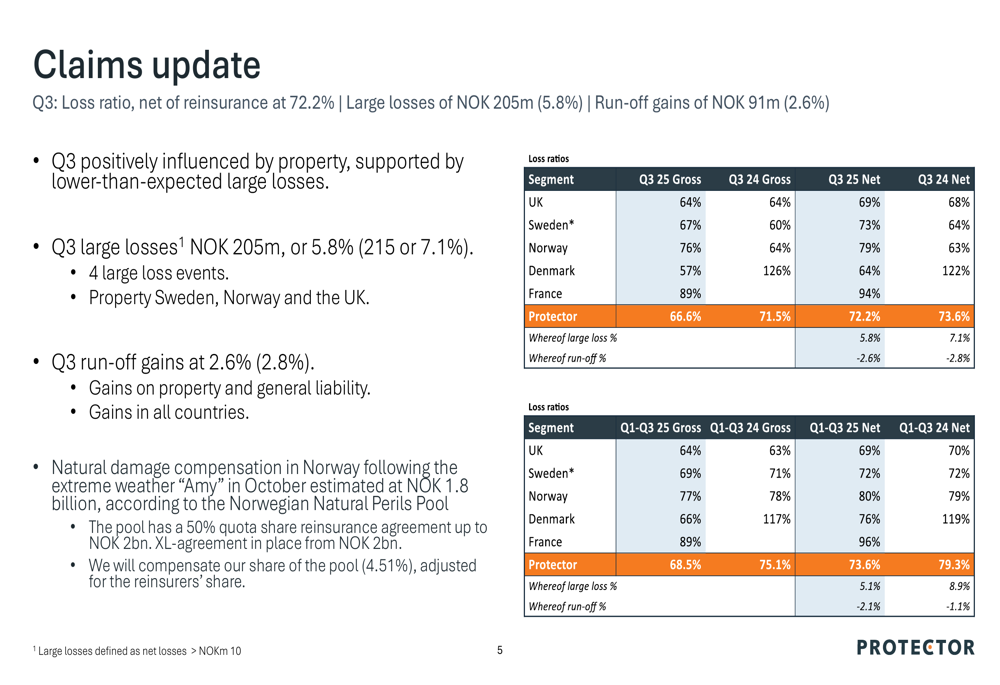

The Q3 loss ratio, net of reinsurance, was 72.2%, with large losses amounting to 205 million NOK (5.8%) and run-off gains of 91 million NOK (2.6%). The quarter was positively influenced by property performance.

The claims update provides a detailed breakdown by segment:

Protector maintained an 80% renewal rate during the quarter, with underlying GWP growth in local currencies reaching high single digits. The company achieved a milestone by winning its first client in the UK Real Estate market, while also pursuing significant opportunities in France, with tenders representing approximately €460 million for January 2026 inception.

Investment Portfolio Performance

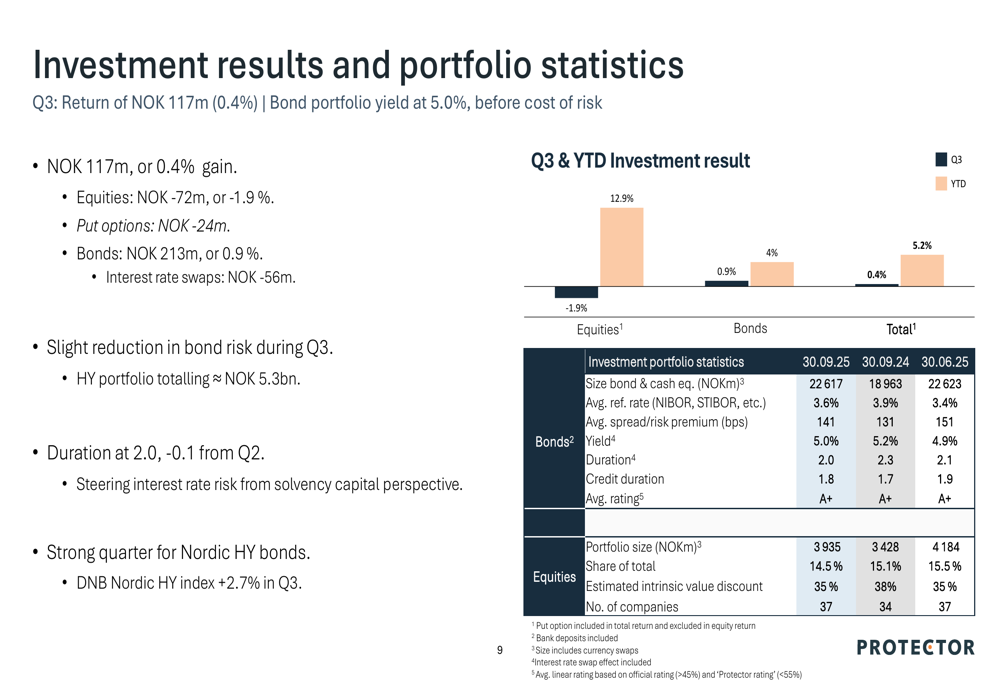

Protector’s investment portfolio delivered a return of 117 million NOK (0.4%) in Q3 2025, with the bond portfolio yield standing at 5.0%. The investment performance was primarily driven by strong bond returns of 213 million NOK, which offset losses in equities (-72 million NOK) and put options (-24 million NOK).

The company reported a slight reduction in bond risk, with its high-yield portfolio totaling approximately 5.3 billion NOK. The investment strategy continues to balance risk and return across asset classes.

The following chart illustrates the investment results and portfolio statistics:

Capital Position & Strategic Initiatives

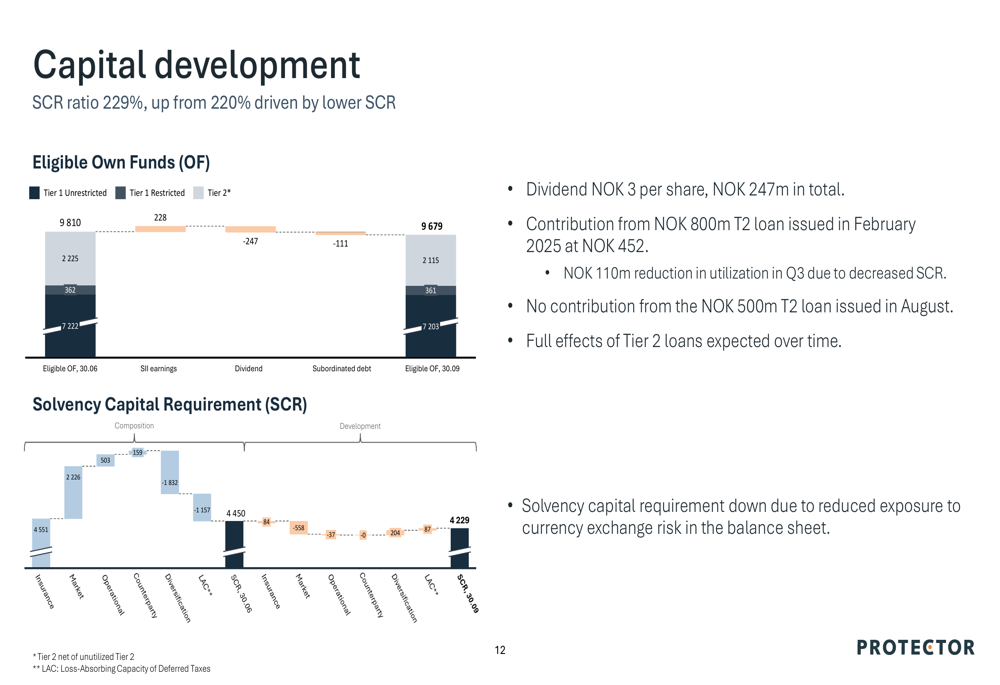

Protector’s capital position strengthened during the quarter, with the Solvency Capital Requirement (SCR) ratio improving to 229% from 220%, primarily driven by lower SCR due to reduced exposure to currency exchange risk in the balance sheet.

The company successfully placed a new Solvency II compliant Tier 2 bond of 500 million NOK during the quarter. The Board also approved a dividend distribution of 247 million NOK, corresponding to 3.00 NOK per share.

The following chart details the capital development:

Strategically, Protector continues to focus on its core values of being credible, innovative/open, bold, and committed, while pursuing its main targets of cost and quality leadership, profitable growth, and achieving top 3 positions in its markets.

Forward-Looking Statements

Looking ahead, Protector is positioning itself for growth in several markets. The company is targeting significant opportunities in the French market, with tenders representing approximately €460 million for January 2026 inception, and quotes submitted for 70-75% of this amount.

The company also announced a portfolio transfer agreement for its Danish workers’ compensation portfolio, indicating strategic portfolio management. According to the earnings call transcript, Protector is heavily investing in AI implementation across the organization to enhance efficiency, with executives emphasizing that "data is our currency."

The Norwegian Natural Perils Pool estimates that natural damage compensation following the extreme weather "Amy" in October will reach approximately 1.8 billion NOK, which may impact future quarters.

Despite the strong profitability metrics presented in the slides, investors appear concerned about growth prospects, particularly in the UK property market, which according to the earnings call, is experiencing a softening cycle. This market context helps explain the 7.68% stock price decline following the results announcement, despite the company’s solid financial performance.

The income statement provides a comprehensive view of the company’s financial performance:

Protector’s commitment to maintaining underwriting discipline over volume growth aligns with its strategic focus on profitability, as evidenced by its impressive combined ratio of 83.1% for Q3 2025. While this approach may limit short-term growth, it positions the company for sustainable long-term performance in a challenging insurance market environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.