Two National Guard members shot near White House

Introduction & Market Context

Proximar Seafood AS (OB:PROXI) presented its Q3 2025 results on November 14, showing significant revenue growth as the company continues to establish itself as a first-mover in Japan's land-based salmon farming industry. Following the announcement, Proximar's stock rose 8.36% to close at NOK 0.84, reflecting investor optimism despite ongoing financial challenges.

The Norwegian-based company, operating near Mount Fuji in Japan, has positioned itself strategically to serve the premium Japanese salmon market, with particular focus on the Tokyo metropolitan area of approximately 38 million people. This positioning continues to be central to Proximar's value proposition as it works to achieve profitability.

Quarterly Performance Highlights

Proximar reported Q3 2025 revenue of NOK 40.4 million, a dramatic increase from just NOK 145,000 in the same period last year. This growth was driven by NOK 24 million in sales and NOK 16.4 million in insurance payouts. The company harvested 356 tonnes in the quarter, with an impressive 99.2% superior grade achievement.

As shown in the following slide detailing Q3 highlights and pricing achievements:

The company achieved premium pricing of approximately NOK 97/kg for salmon over 3kg, significantly higher than the average Norwegian export price of NOK 69/kg. However, the actual realized average price was around NOK 67/kg, impacted by a harvest share below the 3kg threshold. This pricing dynamic underscores both the potential and challenges in Proximar's current production phase.

Operational Progress and Challenges

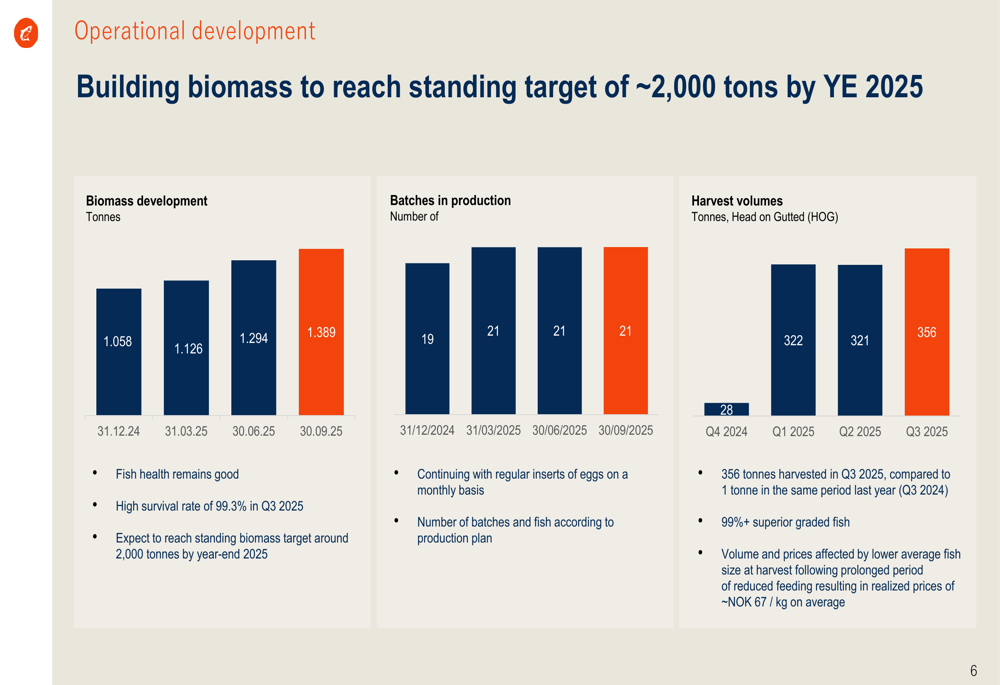

Proximar's biomass reached 1,389 tonnes by the end of Q3 2025, continuing its growth trajectory toward the year-end target of approximately 2,000 tonnes. The company maintained a strong survival rate of 99.3% in the grow-out phase, indicating good overall fish health despite some operational challenges.

The following chart illustrates the company's biomass development:

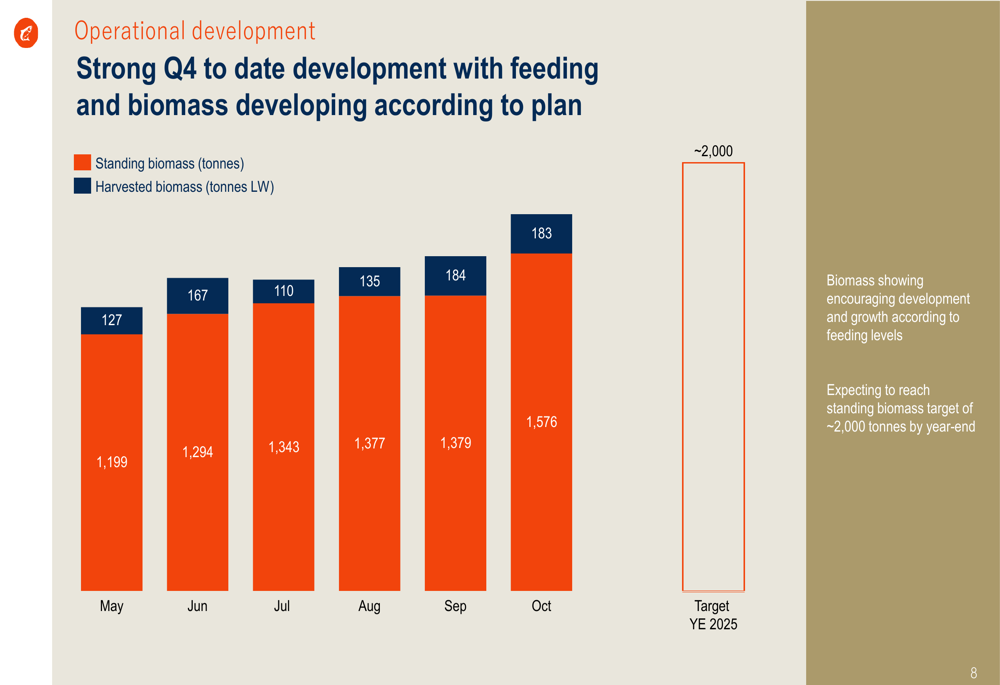

The presentation highlighted several operational challenges that affected growth during Q3, including issues with the feeding system, feed distribution problems, and elevated temperatures following a summer heatwave in Japan. In response, Proximar implemented comprehensive improvements including enhanced feeding systems, improved feed distribution, and additional cooling capacity.

These improvements appear to be yielding results, as shown in the strong October biomass growth:

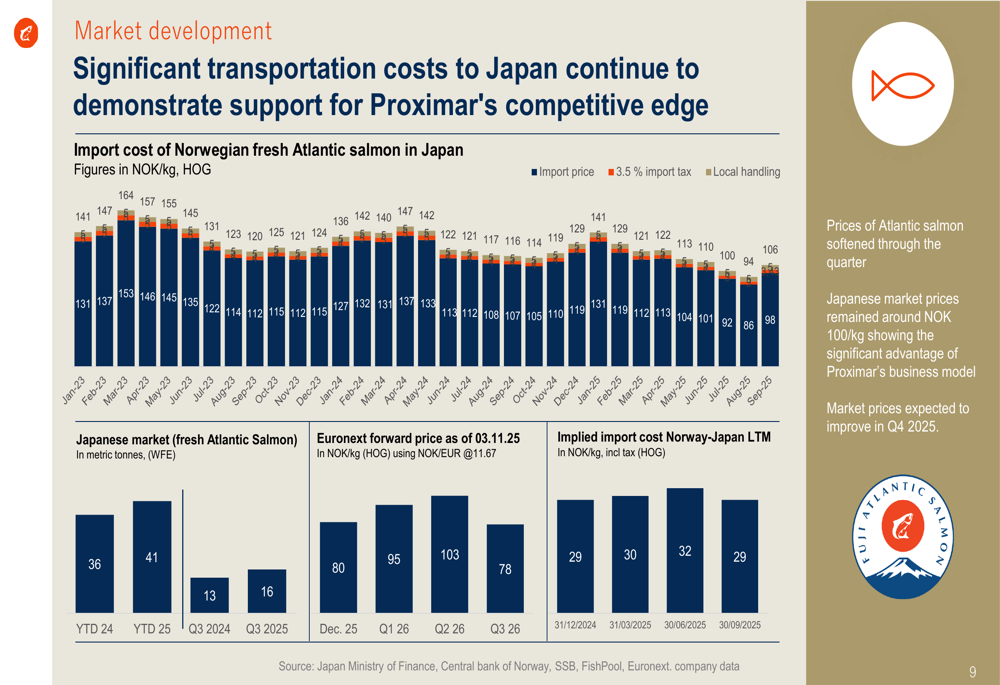

The company's competitive advantage in the Japanese market remains significant due to transportation costs for imported salmon, as illustrated in this market development slide:

Financial Results and Refinancing

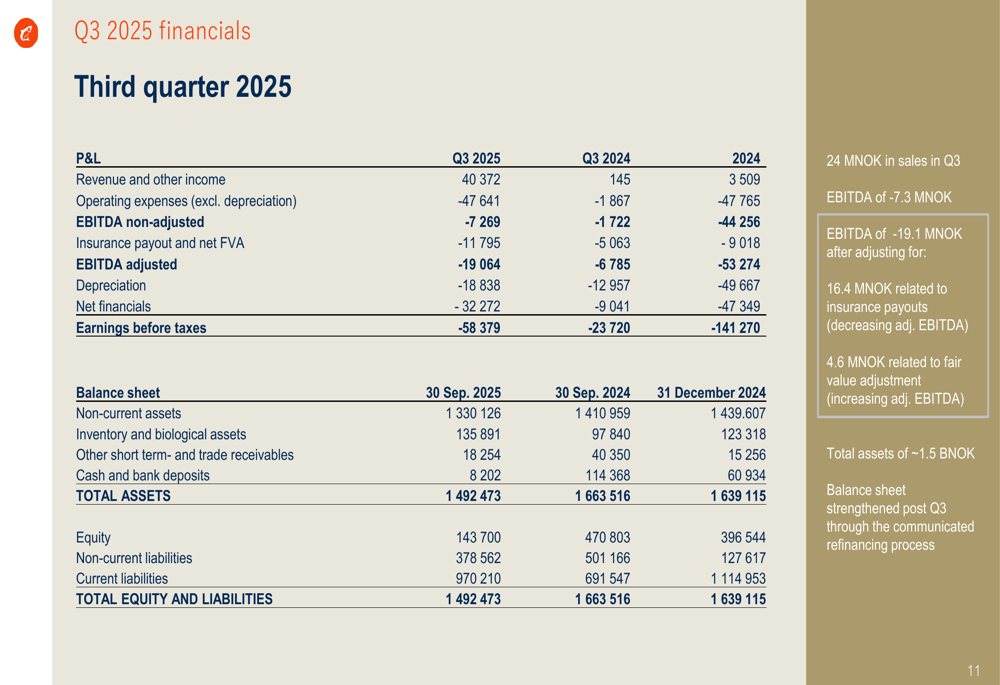

Despite revenue growth, Proximar continues to operate at a loss, reporting an EBITDA of negative NOK 7.3 million for Q3 2025. After adjustments, including insurance payouts and fair value adjustments, the adjusted EBITDA was negative NOK 19.1 million. The company posted a net loss of NOK 58.4 million for the quarter.

The financial position remains challenging with total assets of approximately NOK 1.5 billion against equity of just NOK 143.7 million as of September 30, 2025. The following slide provides a detailed overview of the company's financial results:

A critical development was the completion of a comprehensive refinancing plan in October, which included:

- A NOK 150 million rights issue

- Conversion of approximately NOK 200 million of convertible bonds to equity

- Extension of the syndicated loan until August 2026

- Extension of the shareholder loan until October 2027

According to the company, these measures will improve the equity-to-debt ratio by approximately NOK 550 million, which will be reflected in the Q4 accounts.

Strategic Outlook and Revised Guidance

Proximar has adjusted its harvest guidance, pushing some volumes from 2025 into 2026 to optimize production and improve price achievement. The company now expects to harvest approximately 550,000 fish in 2025 (down from the previous guidance of 900,000) and approximately 1,250,000 fish in 2026 (up from 1,000,000).

This strategic adjustment aims to increase average harvest weights to above 3.5kg (HOG) for 2026, as illustrated in the following guidance slide:

The company emphasized its unique position as a first-mover in Japan's land-based salmon farming industry, with its strategic location providing significant competitive advantages:

CEO Joachim Nielsen acknowledged the challenges of 2025, particularly the biofilter incidents, but expressed optimism about 2026, stating: "We are well positioned for 2026 as we now see good performance in the system and biology." He also highlighted that "The Japanese price levels, even during a depressed pricing environment, illustrate clearly the strong advantage of Proximar as a local producer in Japan."

While Proximar faces ongoing financial challenges, the company's strategic positioning, operational improvements, and completed refinancing provide a foundation for potential improvement in 2026, assuming it can successfully execute its revised harvest strategy and maintain its premium market position in Japan.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.