US stock futures inch lower after Wall St marks fresh records on tech gains

Public Service Enterprise Group (NYSE:PEG) presented its second quarter 2025 financial results on August 5, showing significant year-over-year growth in both net income and operating earnings while reaffirming its full-year guidance. Despite the positive results, the stock was down 2.21% in trading following the presentation, with shares at $88.15 compared to the previous close of $90.14.

Quarterly Performance Highlights

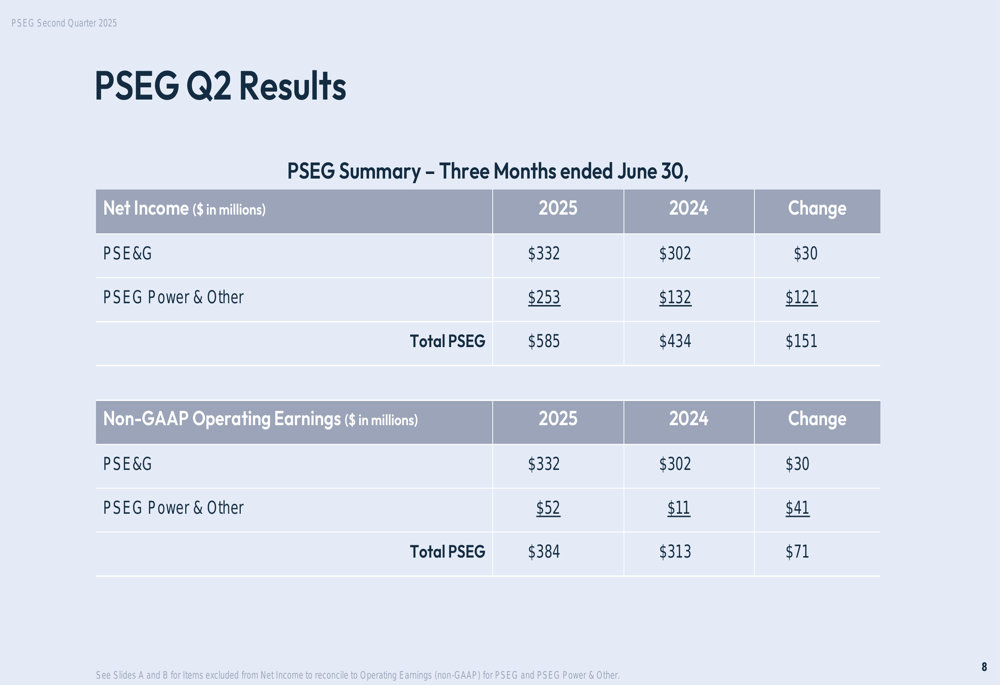

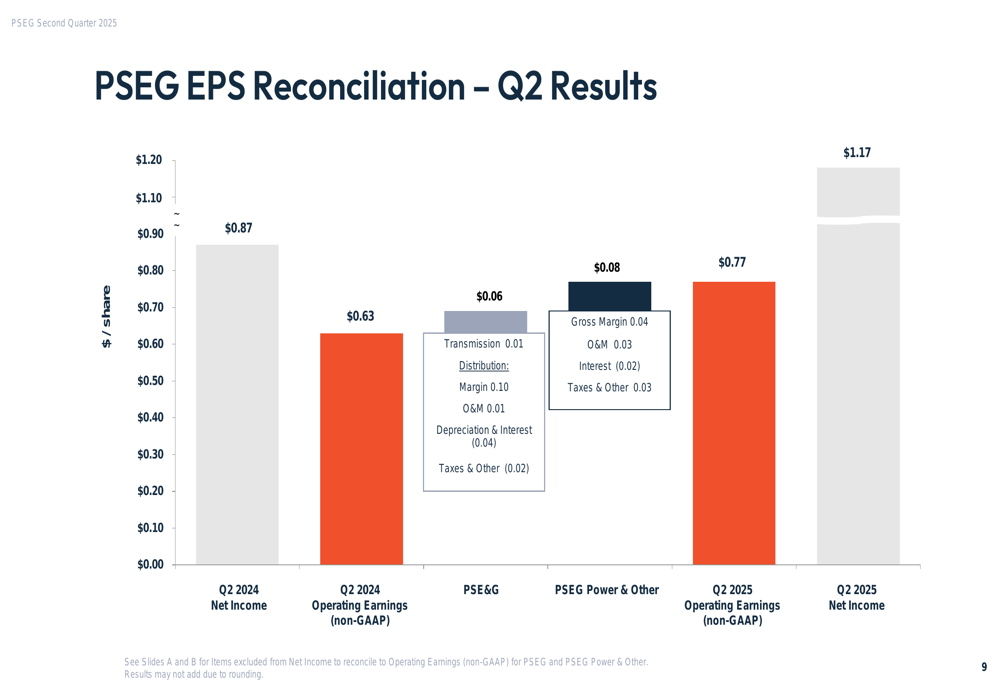

PSEG reported Q2 2025 net income of $1.17 per share, up from $0.87 in the same period last year, representing a 34.5% increase. Non-GAAP operating earnings came in at $0.77 per share compared to $0.63 in Q2 2024, a 22.2% improvement. The company’s total net income reached $585 million for the quarter, a $151 million increase from the $434 million reported in Q2 2024.

As shown in the following financial summary table, both major business segments contributed to the growth:

The company’s PSE&G utility segment delivered $332 million in net income for Q2 2025, up $30 million from the prior year, while PSEG Power & Other saw a more dramatic improvement with net income of $253 million, up $121 million year-over-year.

The reconciliation between net income and operating earnings reveals the key drivers behind the quarterly performance:

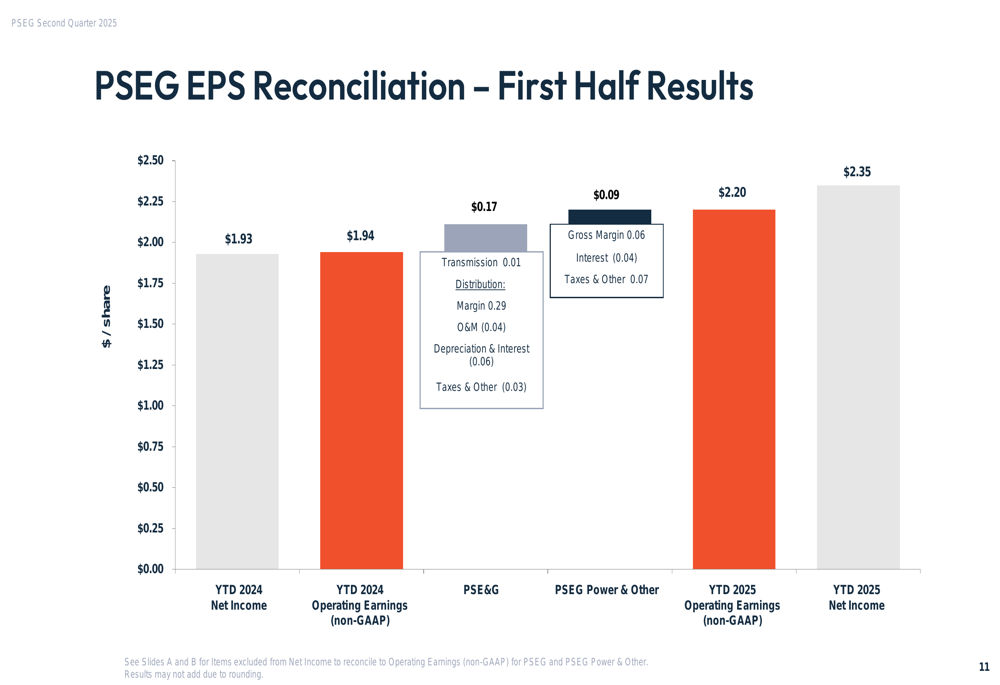

For the first half of 2025, PSEG’s results were equally impressive, with net income of $2.35 per share compared to $1.93 per share for the first half of 2024. Non-GAAP operating earnings for the six-month period reached $2.20 per share versus $1.94 in the prior year.

Strategic Initiatives

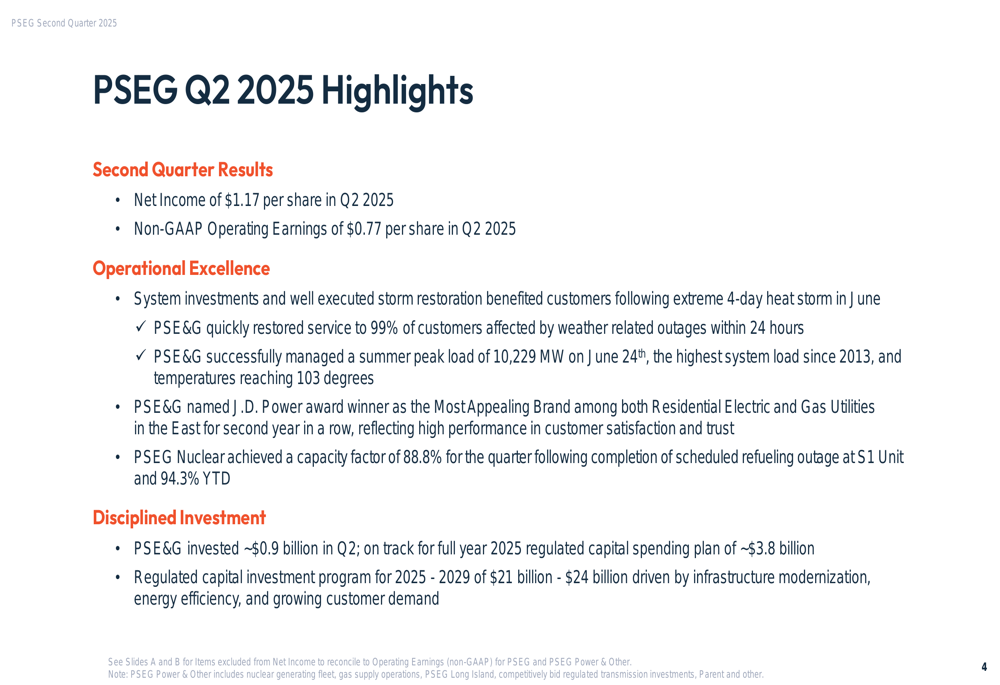

PSEG continues to execute on its strategic focus of growing its regulated utility business while maintaining operational excellence. The company invested approximately $0.9 billion in capital expenditures during Q2 2025 and approximately $1.7 billion year-to-date, keeping its regulated capital investment program on track.

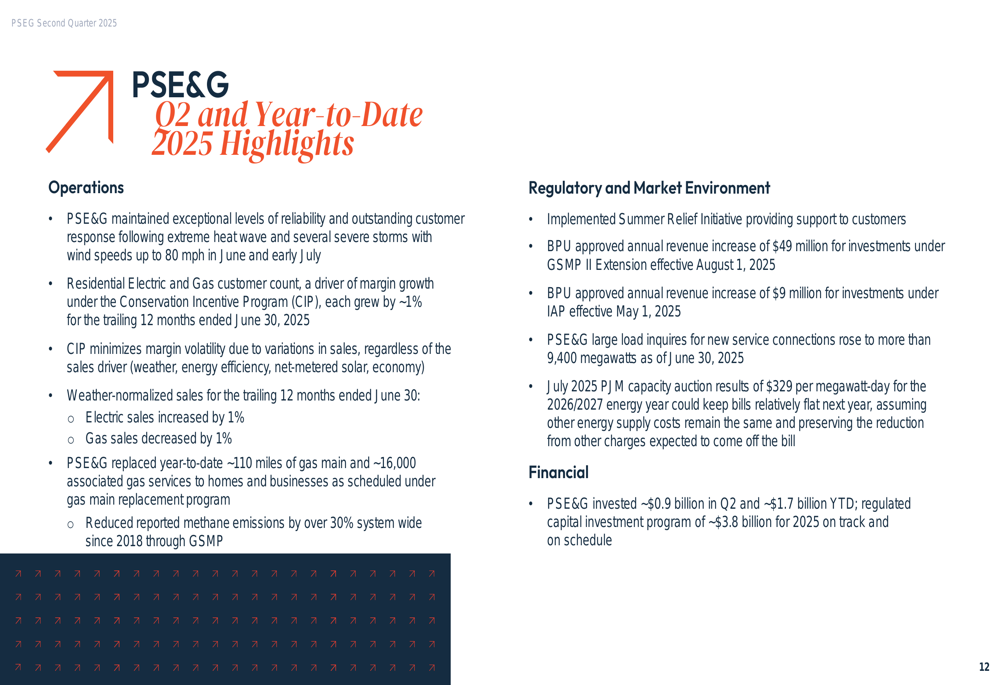

The presentation highlighted several operational achievements, including maintaining exceptional reliability during a heat storm, managing peak summer load of 10,229 MW, and achieving an 88.8% capacity factor at PSEG Nuclear. The company’s PSE&G utility segment also won a J.D. Power award, though specific details of the award were not provided.

As shown in the quarterly highlights slide, these operational successes underscore the company’s disciplined investment approach:

PSEG’s utility segment continues to show strong fundamentals, with both residential electric and gas customer counts growing by approximately 1%. The company also reported progress in its environmental initiatives, reducing reported methane emissions by over 30% system-wide since 2018.

Forward-Looking Statements

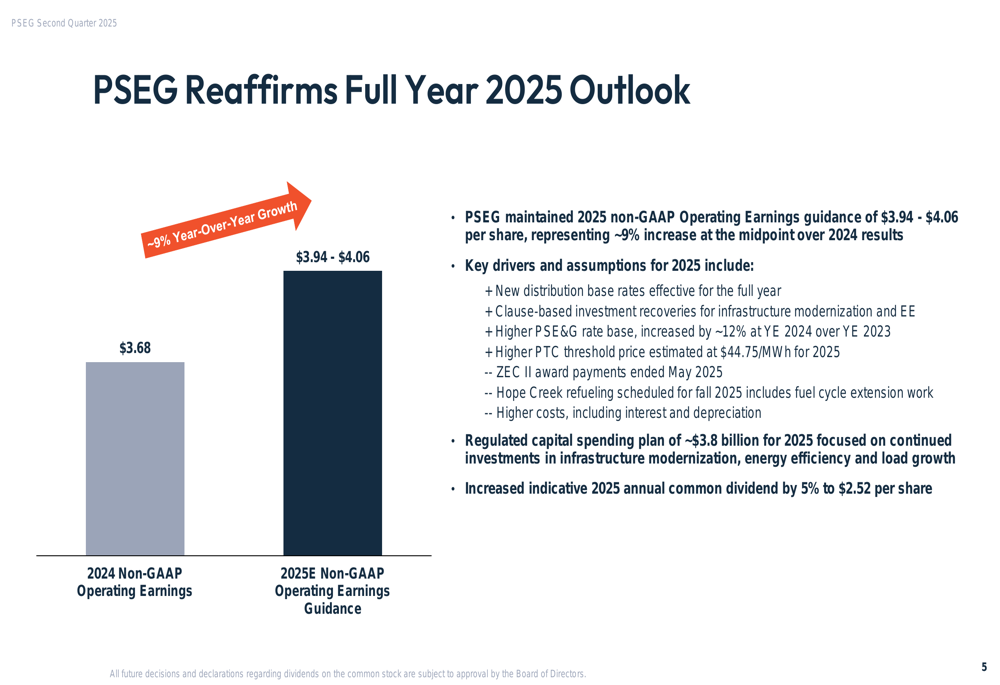

PSEG reaffirmed its full-year 2025 non-GAAP operating earnings guidance of $3.94 to $4.06 per share, representing approximately 9% growth at the midpoint compared to 2024 results of $3.68 per share. The company also maintained its long-term earnings growth outlook of 5%-7% based on the 2025 guidance midpoint.

The following slide illustrates the company’s 2025 outlook and key growth drivers:

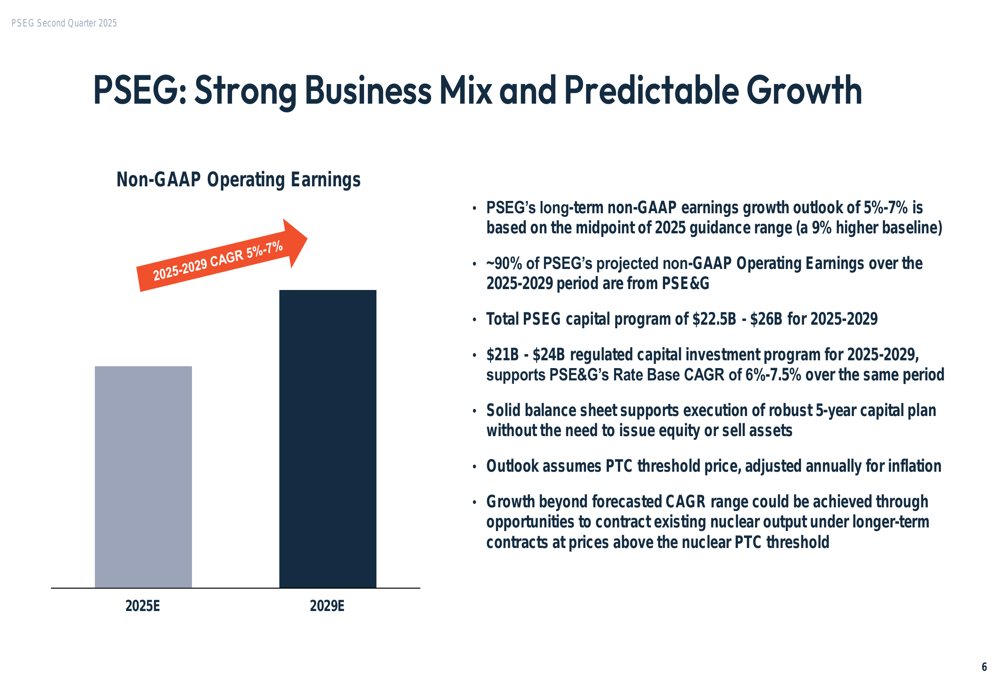

Looking further ahead, PSEG outlined its business mix and growth trajectory through 2029, noting that approximately 90% of projected earnings are expected to come from its regulated PSE&G utility operations. The company plans a total capital program of $22.5 billion to $26 billion for 2025-2029, with $21 billion to $24 billion allocated to regulated capital investments.

The company also announced an increase to its indicative 2025 annual common dividend by 5% to $2.52 per share, reflecting confidence in its financial outlook and commitment to shareholder returns.

Financial Position

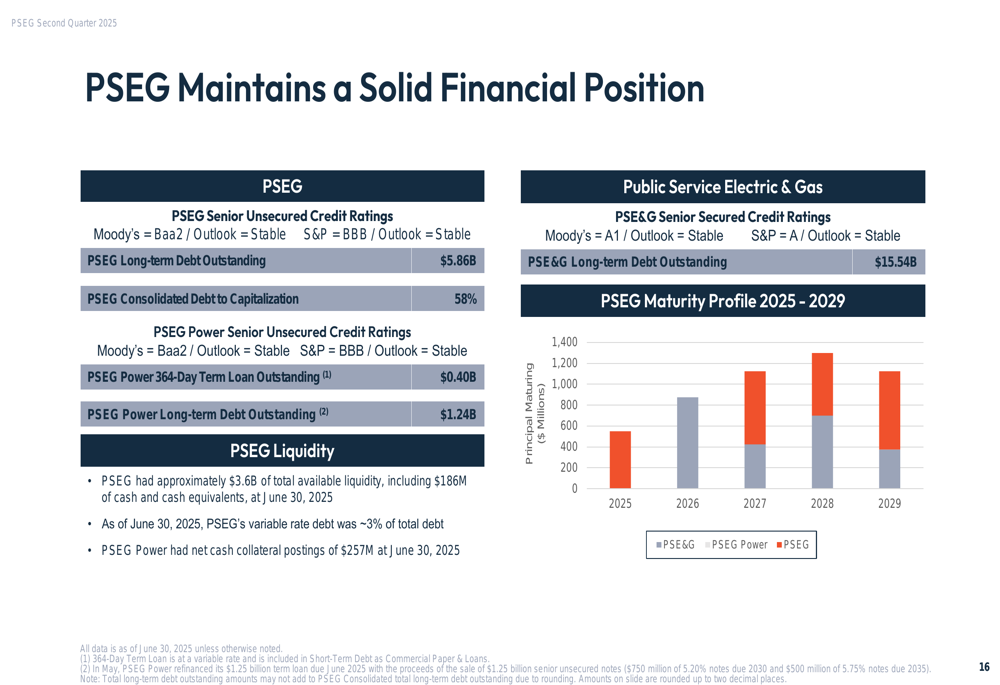

PSEG maintains a solid financial position with strong credit ratings and ample liquidity to support its growth initiatives. As of June 30, 2025, the company had approximately $3.6 billion of total available liquidity and a consolidated debt-to-capitalization ratio of 58%.

The following slide details the company’s credit ratings and debt profile:

Management emphasized that the company’s strong balance sheet will support its five-year capital plan without requiring equity issuance, an important consideration for investors concerned about potential dilution.

In the nuclear segment, PSEG noted that its Salem 1, Salem 2, and Hope Creek nuclear plants concluded their Zero Emission Credit (ZEC) sales in May, and that Hope Creek will transition from 18-month to 24-month fuel cycles, which should improve operational efficiency.

PSEG is also implementing customer relief measures to address higher pass-through energy supply costs, including a summer moratorium on service disconnections, deferral of electric supply increases, and expanded customer assistance programs. These initiatives reflect the company’s recognition of affordability challenges while maintaining its financial trajectory.

This balanced approach to growth, operational excellence, and customer needs appears to be supporting PSEG’s consistent financial performance, even as the stock faced downward pressure on the day of the presentation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.