S&P 500 struggles for direction as investor await inflation data

Introduction & Market Context

Qliro AB (STO:QLIRO) presented its Q2 2025 results on August 26, highlighting significant growth in payment volumes despite ongoing profitability challenges. The company's stock fell 7.59% to 20.70 SEK following the presentation, reflecting investor concerns about the widening operating loss despite strong volume growth.

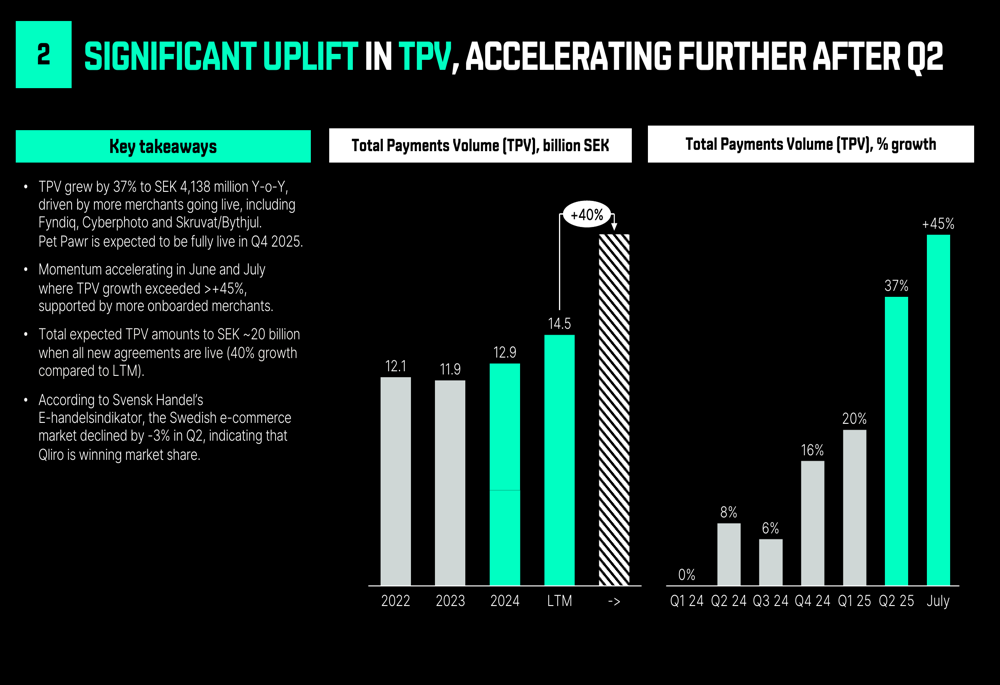

The Swedish fintech company is pursuing an ambitious strategy to become a leading composable payments provider in the Nordics and eventually across the EU. This comes against the backdrop of a challenging e-commerce environment in Sweden, where the market declined by 3% in Q2, making Qliro's volume growth even more notable as it indicates substantial market share gains.

Quarterly Performance Highlights

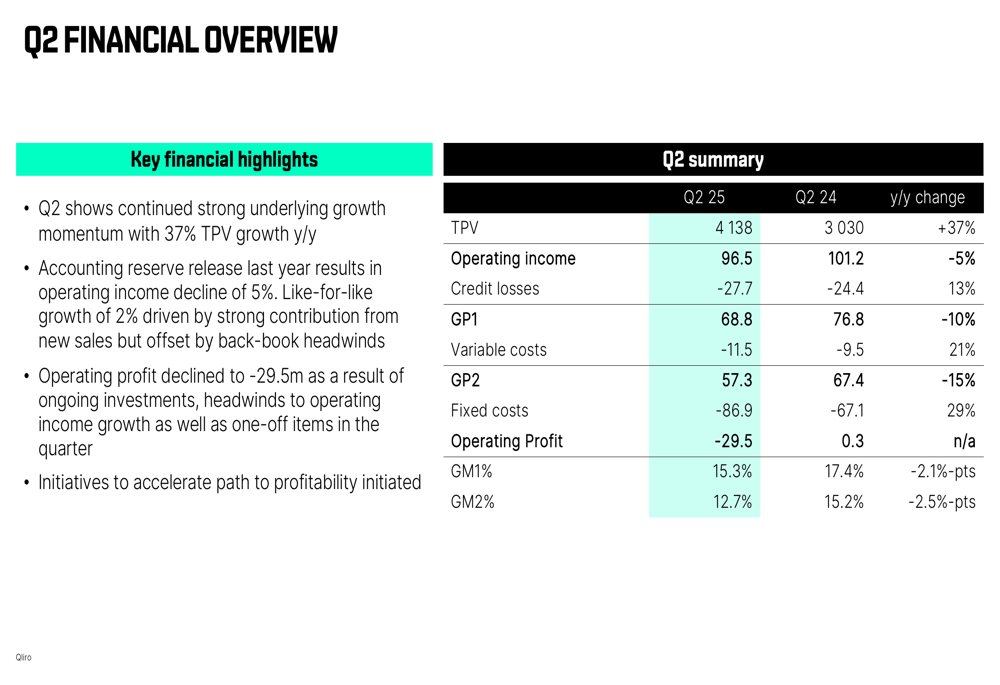

Qliro reported a 37% year-over-year increase in Total Payment Volume (TPV) to SEK 4,138 million for Q2 2025, with momentum accelerating to over 45% growth in July. This strong volume growth, however, did not translate to improved financial performance, as operating income decreased by 5% to SEK 96.5 million compared to Q2 2024.

As shown in the following comprehensive financial overview from the presentation:

The company's gross profit declined by 10% to SEK 68.8 million, while operating profit fell to negative SEK 29.5 million from a positive SEK 0.3 million in the same period last year. Credit losses increased by 13% to SEK 27.7 million, and both fixed and variable costs rose significantly, with fixed costs up 29% year-over-year.

The divergence between volume growth and financial performance is illustrated in this TPV growth chart:

Strategic Initiatives

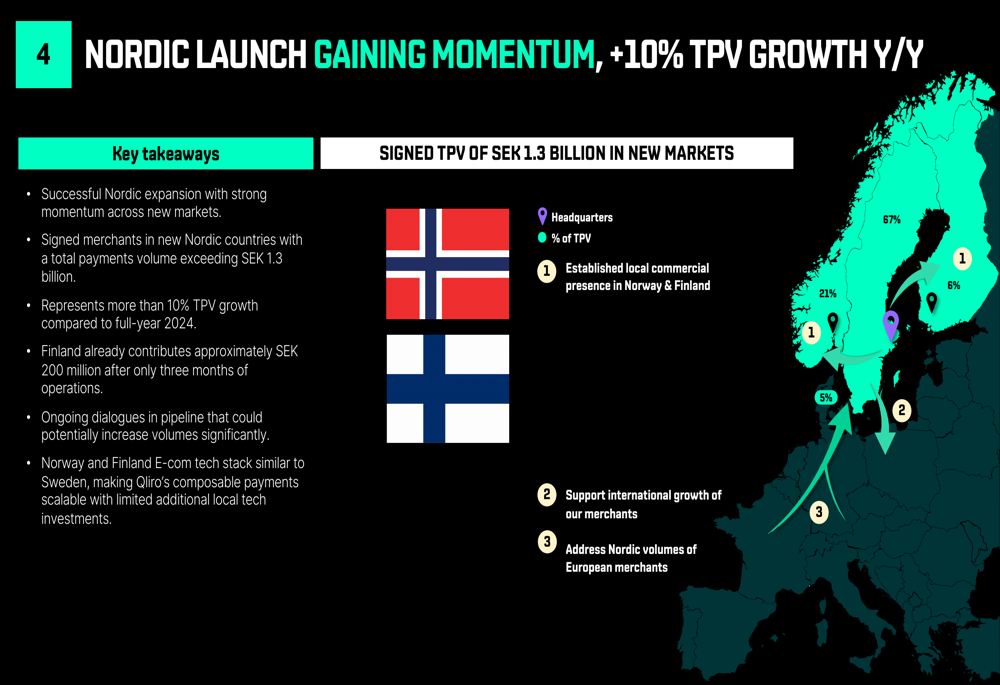

Qliro's strategic focus centers on Nordic expansion, growing its SME merchant base, and optimizing its Buy Now, Pay Later (BNPL) offering. The company has made significant progress in its Nordic expansion, signing merchants in Norway and Finland with a total payments volume exceeding SEK 1.3 billion.

The Nordic expansion strategy is visualized in this regional breakdown:

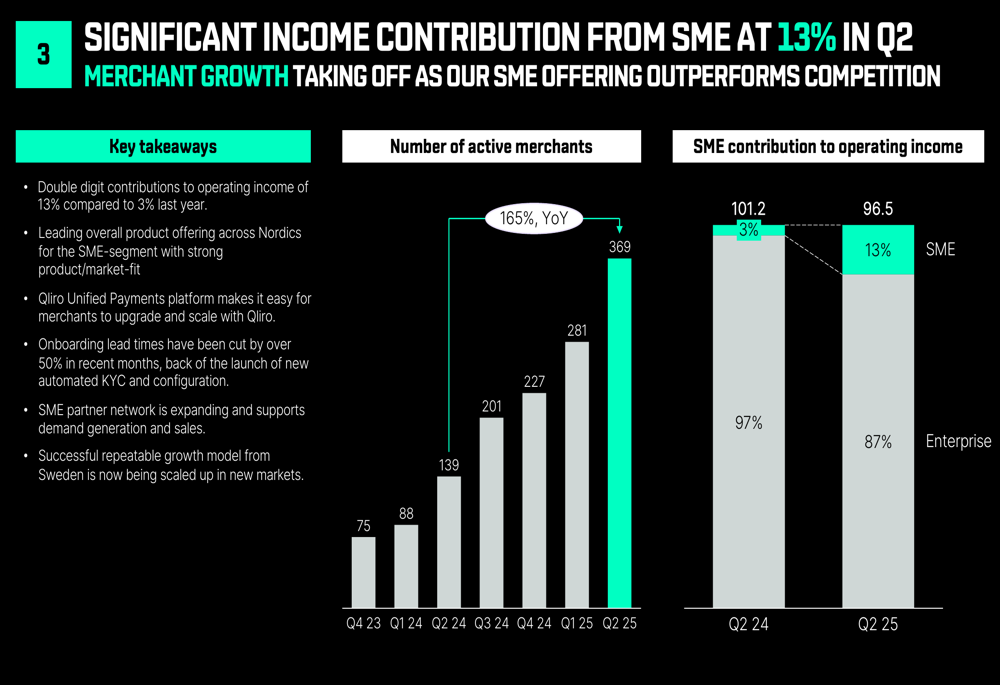

Small and medium-sized enterprises (SMEs) have become an increasingly important segment for Qliro, with their contribution to operating income growing from 3% in Q2 2024 to 13% in Q2 2025. The company has also improved its onboarding efficiency, cutting lead times by over 50% in recent months.

This chart illustrates the growing importance of the SME segment:

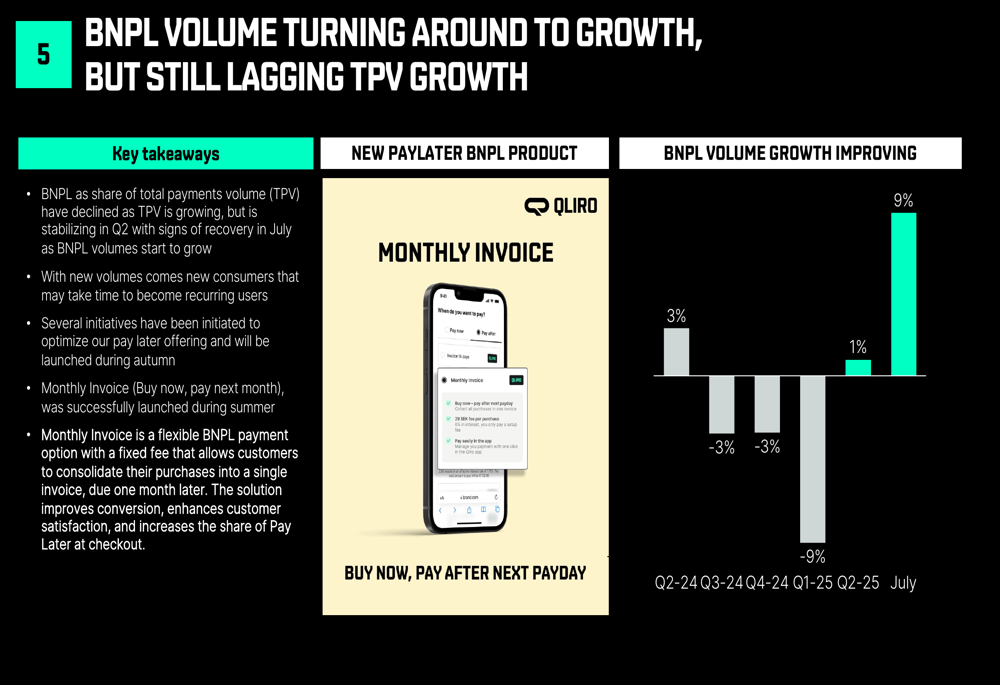

After experiencing declines in its BNPL business, Qliro is seeing early signs of recovery, with BNPL volumes returning to growth in Q2 2025 and accelerating to 9% year-over-year growth in July. The company plans to launch several initiatives to optimize its pay later offering during the autumn.

The BNPL recovery trend is shown in this chart:

Detailed Financial Analysis

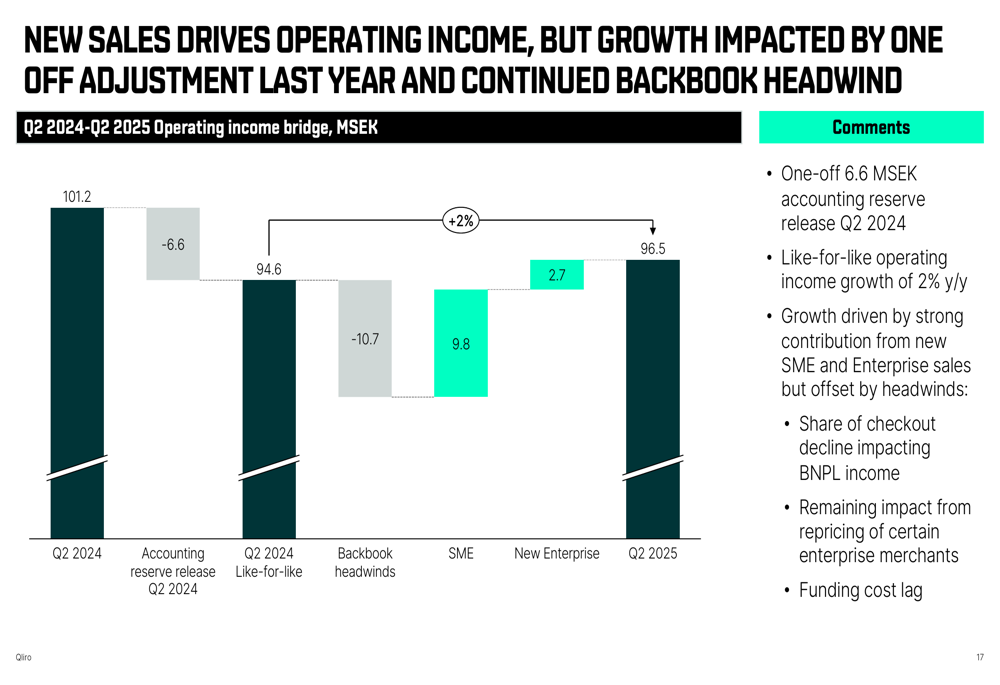

Despite strong volume growth, Qliro's operating income declined due to several factors. The company provided a detailed bridge analysis explaining the year-over-year change:

A one-off accounting reserve release of SEK 6.6 million in Q2 2024 created a challenging comparison base. Additionally, back book headwinds of SEK 10.7 million, including checkout decline, repricing of certain enterprise merchants, and funding cost lag, negatively impacted results. These headwinds were partially offset by SEK 9.8 million in SME contribution and SEK 2.7 million from new enterprise sales.

The company has also undertaken profitability initiatives, with SEK 2.2 million in costs taken during Q2 2025 expected to yield annual run-rate savings of SEK 4 million. These initiatives include bank and Swish cost reduction, card acquiring cost reduction, and vendor renegotiations.

Capital Position and Funding

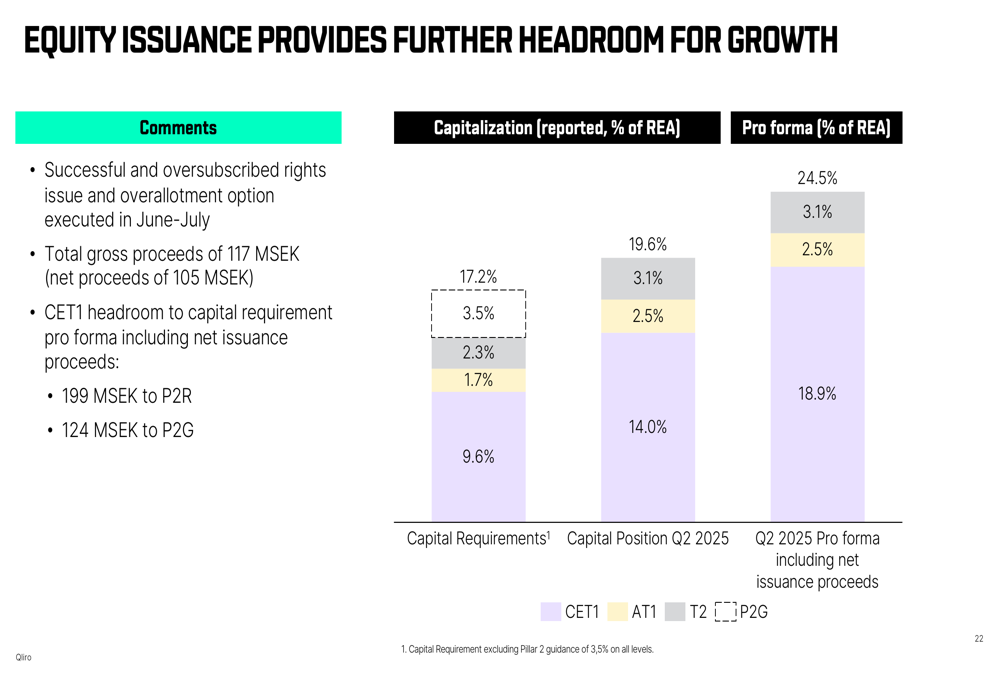

Qliro successfully raised SEK 117 million through an oversubscribed rights issue in Q2, with net proceeds of SEK 105 million. Combined with a SEK 70 million Tier 2 bond issued in the quarter, the company has significantly strengthened its capital position.

The improved capital position is illustrated in this chart:

The capital raise has increased Qliro's CET1 ratio from 19.6% to 24.5% on a pro forma basis, providing additional headroom for growth investments.

Forward-Looking Statements

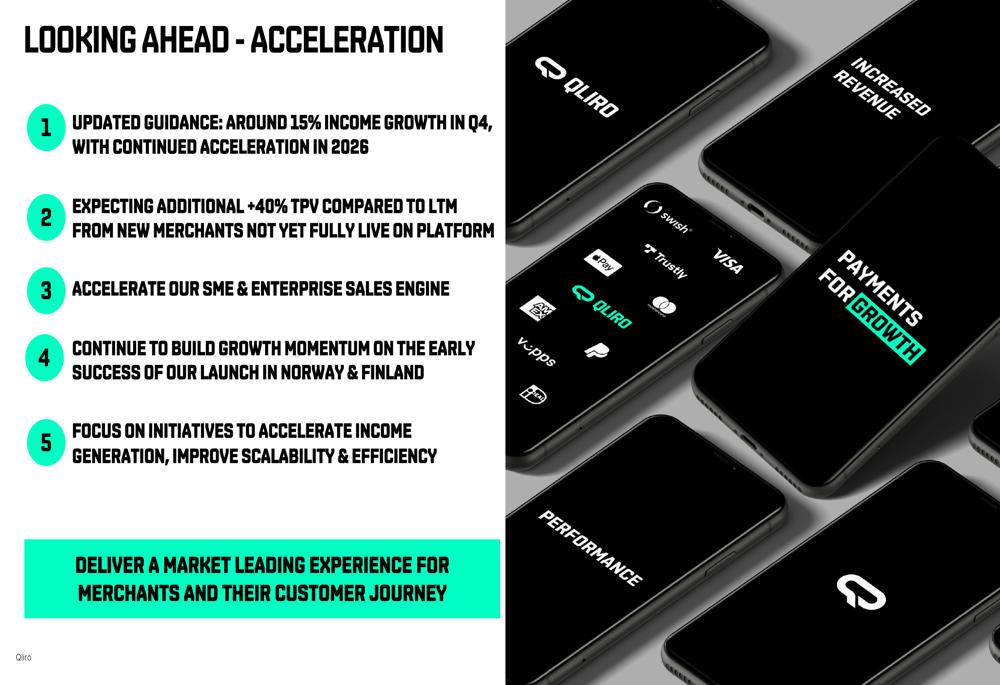

Looking ahead, Qliro has updated its guidance to around 15% income growth in Q4, a more modest outlook compared to its previous guidance of 15-30% income growth in the second half of 2024 mentioned in the Q1 earnings call.

The company expects to maintain its strong TPV growth momentum, projecting an additional 40% TPV compared to the last twelve months. Key focus areas include accelerating SME and enterprise sales, building on early success in Norway and Finland, and implementing initiatives to improve income generation, scalability, and efficiency.

Qliro's strategic roadmap is summarized in this forward-looking slide:

While Qliro continues to demonstrate impressive volume growth and market share gains, the company faces significant challenges in translating this growth into improved profitability. The widening operating loss and increased costs associated with Nordic expansion will likely remain key concerns for investors in the near term, even as the company builds a foundation for potential long-term success in the competitive Nordic payments market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.