ION expands ETF trading capabilities with Tradeweb integration

Introduction & Market Context

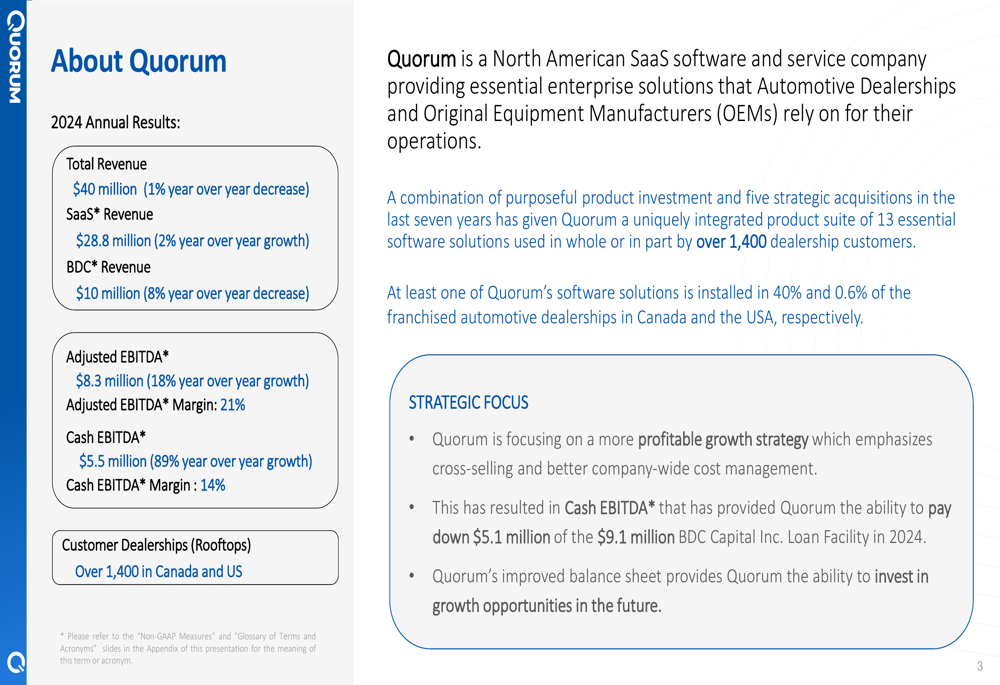

Quorum Information Technologies Inc . (TSXV:QIS), a North American SaaS software and service provider for automotive dealerships, presented its Q4 and full-year 2024 results on April 16, 2025, highlighting a strategic pivot toward profitability that has yielded significant improvements in key financial metrics despite relatively flat revenue growth.

The company, which serves over 1,400 dealership customers with 13 essential software solutions, has established a strong presence in the Canadian market, where it’s installed in 40% of franchised automotive dealerships, while maintaining a smaller 0.6% foothold in the much larger U.S. market.

Executive Summary

Quorum’s 2024 results reflect a successful shift toward prioritizing profitability over top-line growth. While total revenue remained relatively flat at $40 million (a 1% year-over-year decrease), the company achieved substantial improvements in profitability metrics, with Cash EBITDA surging 89% to $5.5 million and Adjusted EBITDA growing 18% to $8.3 million.

As shown in the following overview of Quorum’s business and 2024 results:

This enhanced profitability enabled Quorum to accelerate debt repayment, reducing its BDC Capital Inc. Loan Facility by $5.1 million during 2024. The company’s strategic focus now centers on cross-selling its expanded solution portfolio to existing customers, with management estimating a $54 million revenue opportunity within its current customer base.

Quarterly Performance Highlights

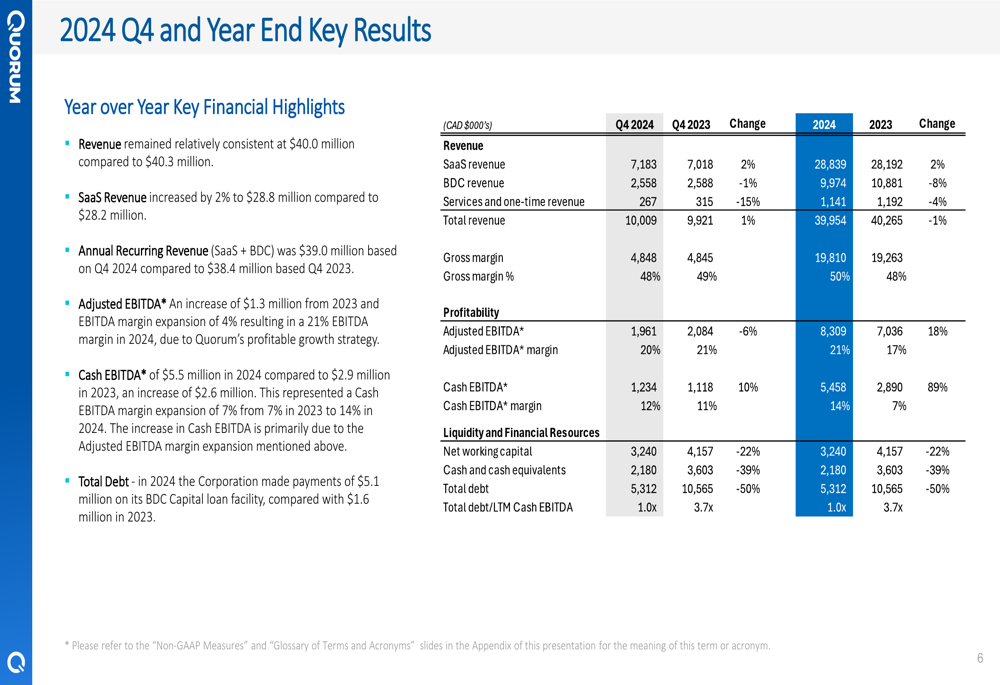

For Q4 2024, Quorum maintained its trajectory of improving profitability metrics while managing modest top-line growth. The detailed financial results table below shows the company’s performance for both the quarter and full year:

SaaS revenue, which represents the company’s core recurring revenue stream, grew 2% year-over-year to $28.8 million for the full year 2024. However, this growth was offset by an 8% decline in BDC (Business Development Center) revenue to $10 million, resulting in the slight overall revenue decrease.

The most notable improvements came in profitability metrics, with Q4 Adjusted EBITDA increasing 19% year-over-year to $2.1 million and Cash EBITDA growing 80% to $1.4 million. These gains reflect Quorum’s enhanced operational efficiency and strategic focus on higher-margin business activities.

Strategic Initiatives

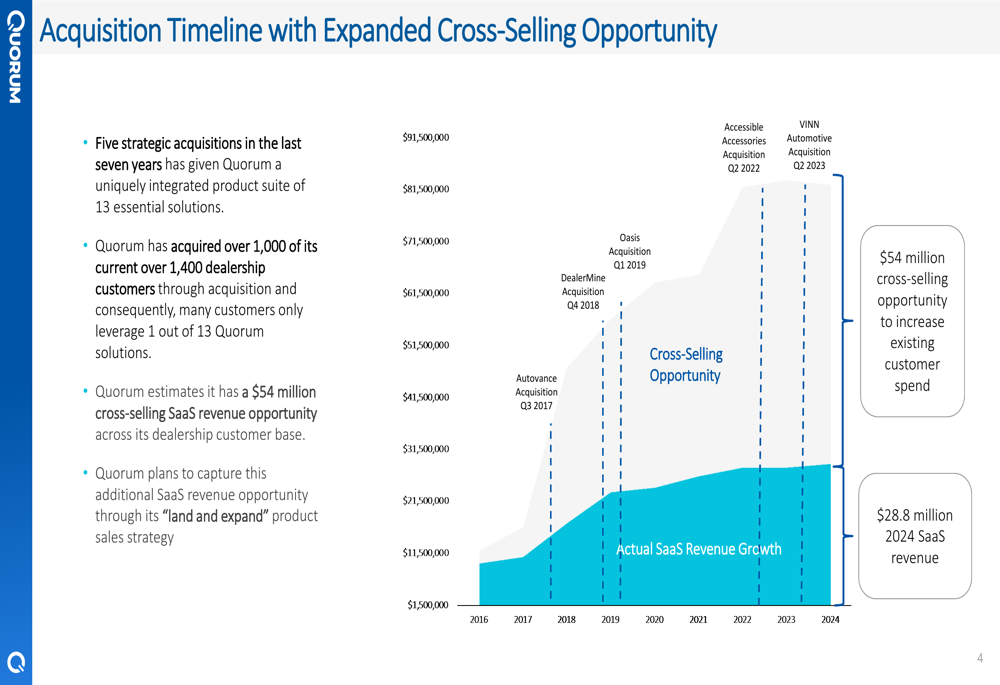

Quorum’s strategic pivot toward profitable growth has been built on leveraging its acquisition history to create cross-selling opportunities. The company has completed five strategic acquisitions that have expanded both its customer base and solution portfolio.

The following chart illustrates the company’s acquisition timeline and the substantial cross-selling opportunity:

With an estimated $54 million in potential SaaS revenue from cross-selling to existing customers, Quorum’s "land and expand" strategy aims to deepen relationships with current dealerships rather than focusing primarily on new customer acquisition. This approach requires less capital investment while potentially yielding higher margins.

The company’s solution suite addresses key challenges in the automotive retail sector, including the need to transform vehicle product mix, create frictionless workflows, improve dealership profitability, and adapt to evolving consumer demand.

Detailed Financial Analysis

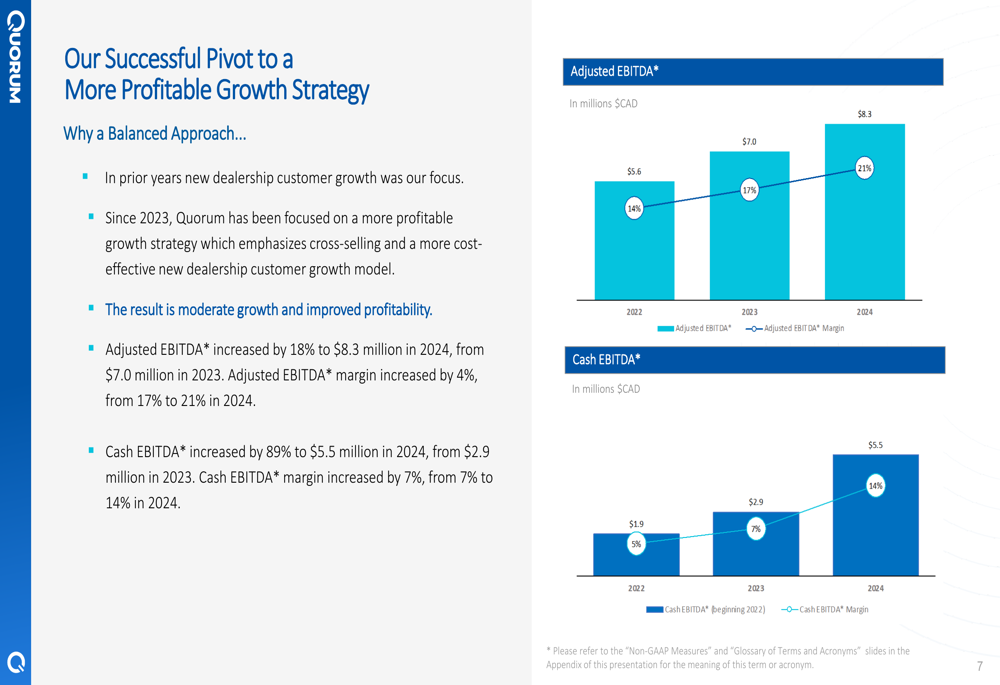

Quorum’s financial performance shows a clear trend toward improved profitability and cash generation. The following chart illustrates the company’s progress in growing both Adjusted EBITDA and Cash EBITDA:

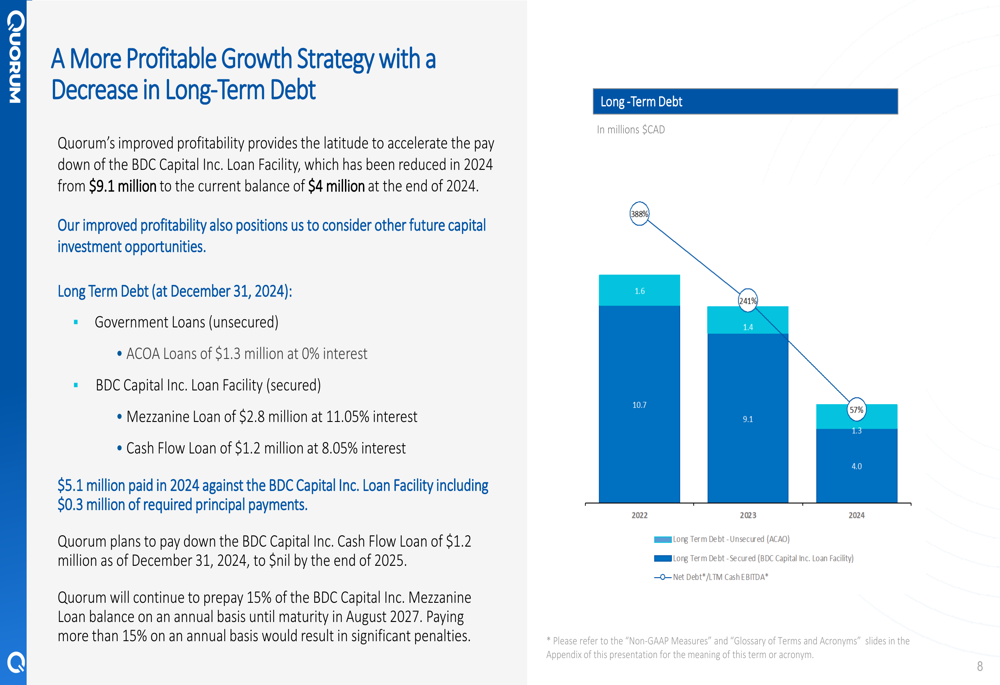

This enhanced profitability has directly translated into accelerated debt reduction. In 2024, Quorum reduced its BDC Capital Inc. Loan Facility from $9.1 million to $4 million, as shown in the following chart:

The company’s long-term debt at the end of 2024 consisted of ACOA Loans of $1.3 million at 0% interest, a Mezzanine Loan of $2.8 million at 11.05% interest, and a Cash Flow Loan of $1.2 million at 8.05% interest. Management plans to pay down the Cash Flow Loan entirely by the end of 2025 and prepay 15% of the Mezzanine Loan annually.

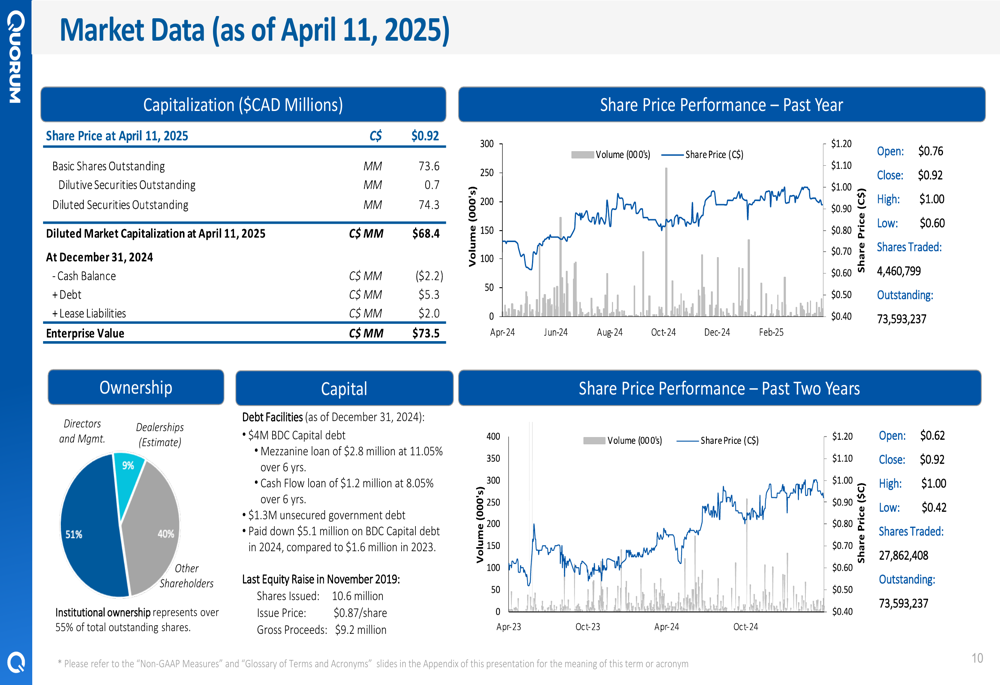

From a market perspective, Quorum’s shares were trading at $0.92 as of April 11, 2025, giving the company a diluted market capitalization of $68.4 million and an enterprise value of $73.5 million. The company has a strong insider ownership structure, with 51% of shares held by directors and management, and over 55% institutional ownership overall.

Forward-Looking Statements

Looking ahead, Quorum has outlined a clear strategy focused on capturing the estimated $54 million cross-selling opportunity within its existing customer base. The company plans to continue prioritizing profitable growth over pure revenue expansion, with an emphasis on margin improvement and debt reduction.

Management expects to completely eliminate the Cash Flow Loan by the end of 2025 while continuing to prepay 15% of the Mezzanine Loan annually, further strengthening the company’s balance sheet and financial flexibility.

While the presentation highlights significant opportunities in the U.S. market, where Quorum currently has only a 0.6% penetration compared to 40% in Canada, the company appears to be taking a measured approach to expansion, focusing first on maximizing value from existing relationships before aggressively pursuing new market share.

As Quorum continues its strategic pivot toward profitability, investors will likely be watching closely to see if the company can maintain its impressive margin expansion while eventually returning to more robust top-line growth through successful execution of its cross-selling initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.