Wall St futures flat amid US-China trade jitters; bank earnings in focus

Ranger Energy Services Inc (NYSE:RNGR) released its second-quarter 2025 earnings presentation on July 29, showcasing a significant financial recovery from the previous quarter’s disappointing results. The company reported substantial improvements in net income, adjusted EBITDA, and free cash flow while continuing its commitment to shareholder returns through dividends and share repurchases.

Quarterly Performance Highlights

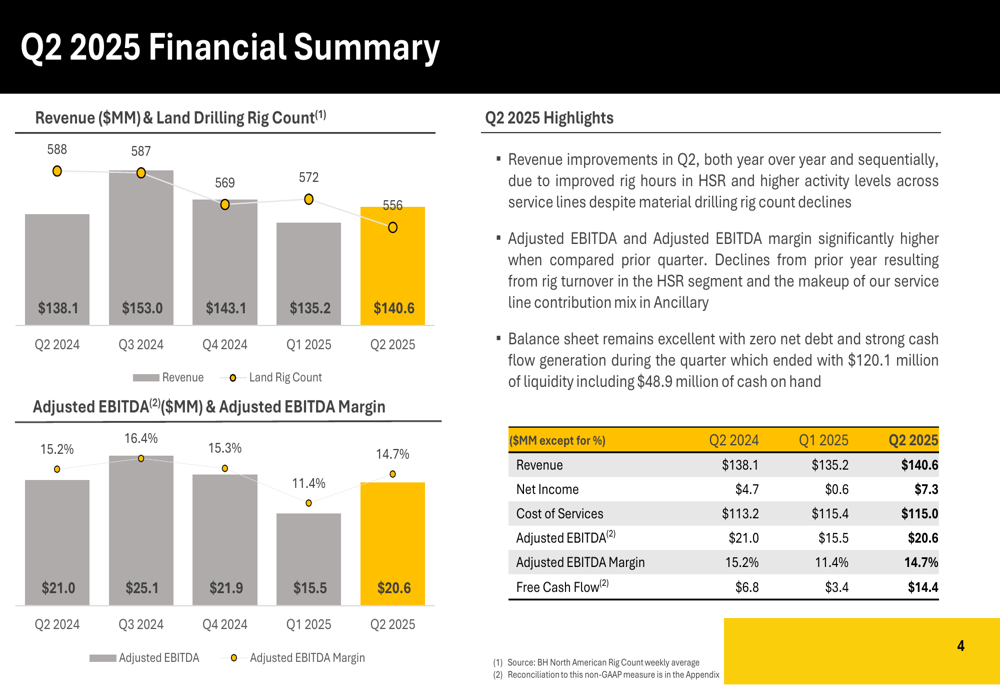

Ranger Energy delivered a strong financial performance in Q2 2025, with revenue reaching $140.6 million, up from $135.2 million in Q1 2025 and $138.1 million in Q2 2024. The company’s net income surged to $7.3 million, representing a dramatic improvement from the $0.6 million reported in Q1 2025 and a 55% increase from $4.7 million in the same quarter last year.

Free cash flow generation was particularly impressive, more than quadrupling from Q1 2025 to reach $14.4 million in Q2 2025, compared to just $3.4 million in the previous quarter and $6.8 million in Q2 2024.

As shown in the following financial summary chart, adjusted EBITDA recovered to $20.6 million in Q2 2025, up from $15.5 million in Q1 2025, though slightly below the $21.0 million reported in Q2 2024:

The adjusted EBITDA margin also rebounded to 14.7% in Q2 2025, a significant improvement from 11.4% in Q1 2025, though still slightly below the 15.2% achieved in the same quarter last year. This recovery is particularly notable following the company’s Q1 earnings miss, which had caused the stock to drop 13.11% after the announcement.

Segment Analysis

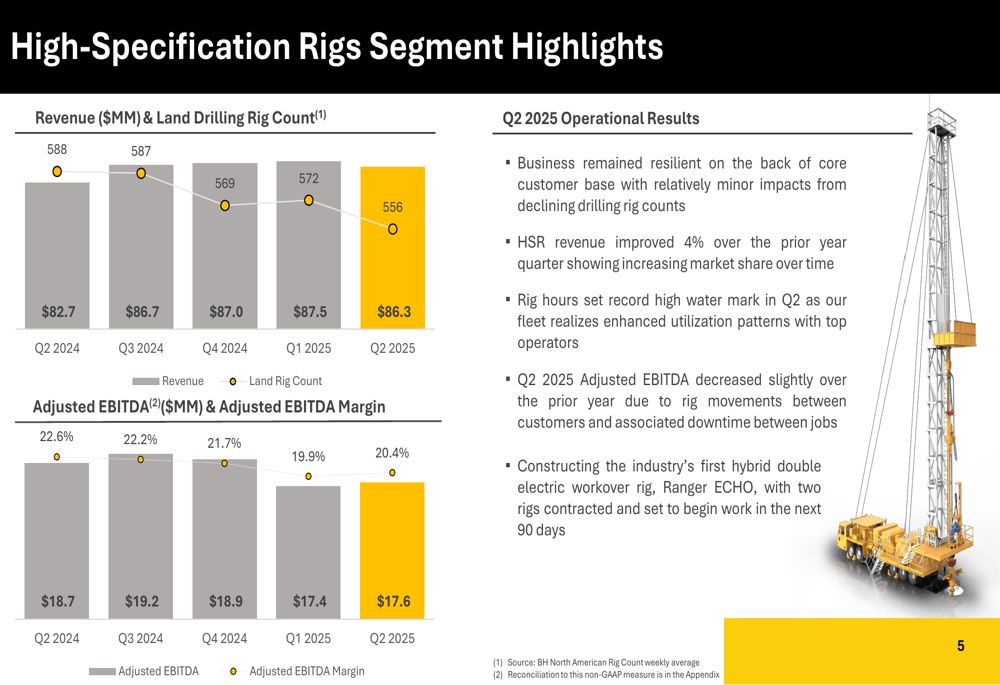

Ranger’s High-Specification Rigs segment remained the largest revenue contributor, generating $86.3 million in Q2 2025, up from $82.7 million in Q2 2024. The segment’s adjusted EBITDA was $17.6 million with a 20.4% margin, showing resilience despite a slight decrease from the 22.6% margin in Q2 2024. The company highlighted that rig hours reached a record high during the quarter.

The following chart illustrates the High-Specification Rigs segment’s performance over the past five quarters:

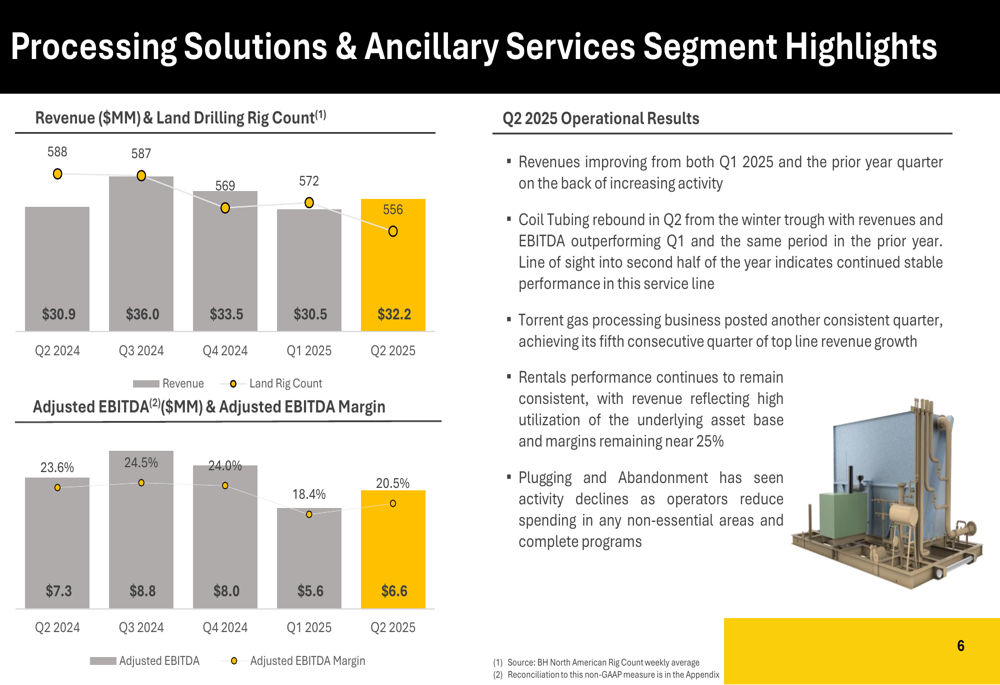

The Processing Solutions & Ancillary Services segment reported revenue of $32.2 million in Q2 2025, up from $30.9 million in Q2 2024. Adjusted EBITDA for this segment was $6.6 million with a 20.5% margin, down slightly from $7.3 million and 23.6% margin in Q2 2024. Management noted that the Coil Tubing business experienced a rebound, while the Torrent gas processing business continued to grow.

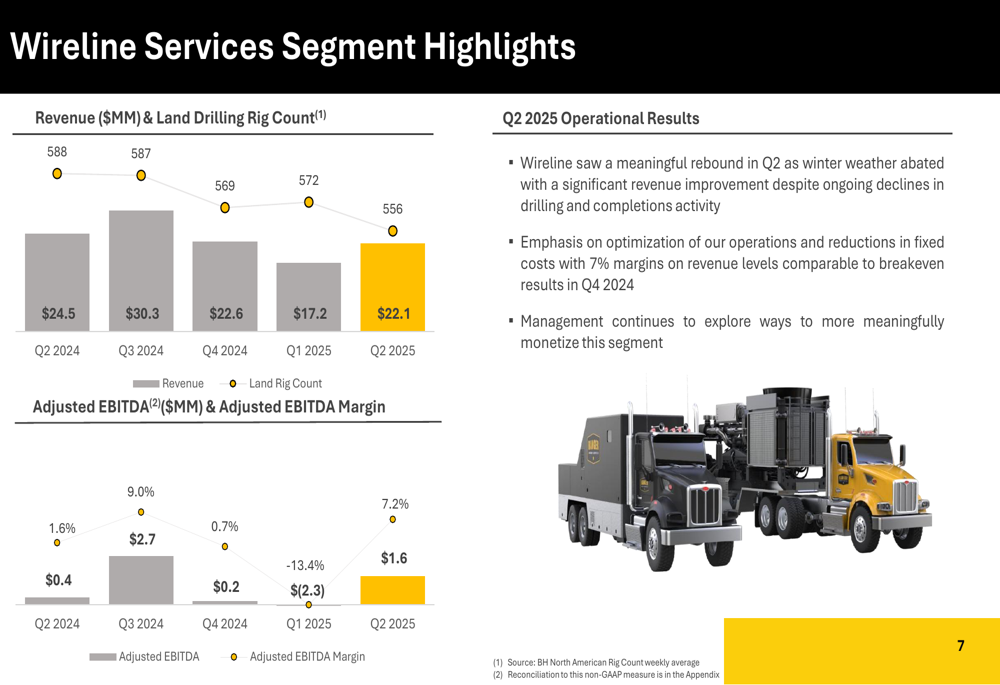

The most dramatic improvement came from the Wireline Services segment, which showed a meaningful rebound from Q1 2025. While revenue decreased slightly year-over-year to $22.1 million from $24.5 million in Q2 2024, adjusted EBITDA increased to $1.6 million with a 7.2% margin, compared to $0.4 million and 1.6% margin in Q2 2024. This represents a significant recovery from the negative 13.4% margin reported in Q1 2025.

Capital Allocation & Shareholder Returns

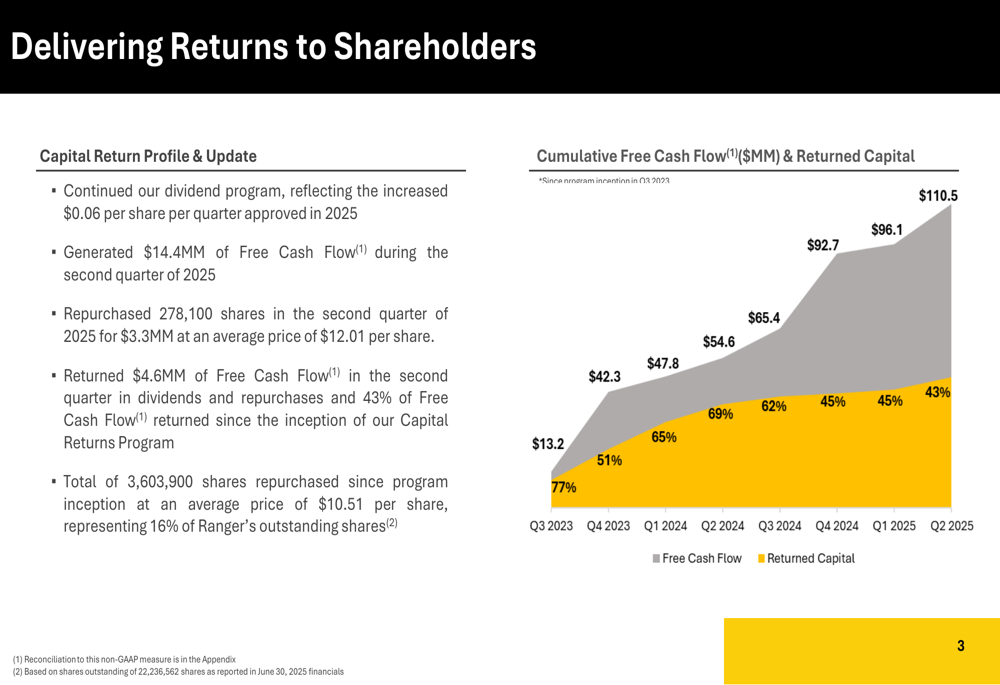

Ranger Energy continued its commitment to returning capital to shareholders in Q2 2025. The company maintained its dividend program at $0.06 per share per quarter and repurchased 278,100 shares for $3.3 million at an average price of $12.01 per share. In total, Ranger returned $4.6 million to shareholders during the quarter.

Since the inception of its Capital Returns Program, the company has repurchased a total of 3,603,900 shares at an average price of $10.51 per share, representing approximately 16% of Ranger’s outstanding shares. The company has returned 43% of its free cash flow to shareholders since the program began.

The following chart illustrates Ranger’s cumulative free cash flow and capital return program:

Strategic Initiatives & Outlook

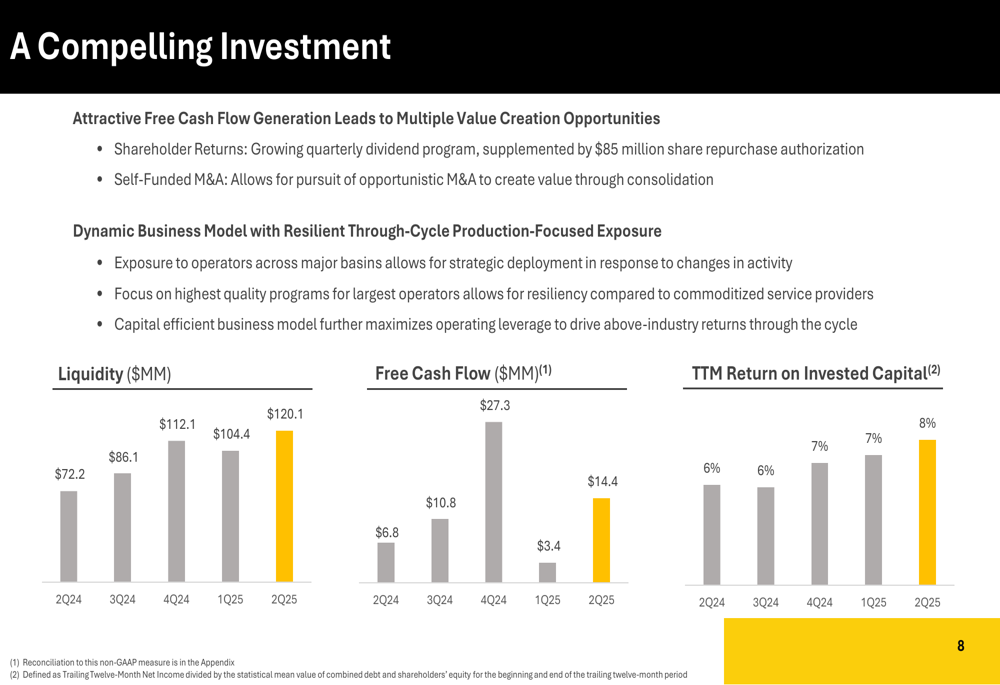

Ranger Energy emphasized its strong financial position, with zero net debt and $120.1 million of liquidity as of Q2 2025, a significant increase from $72.2 million in Q2 2024. This financial flexibility supports the company’s strategic priorities, which include maximizing free cash flow, prioritizing shareholder returns, and exploring merger and acquisition opportunities.

The company is also investing in innovation, announcing the construction of the industry’s first hybrid double electric workover rig, called Ranger ECHO. This initiative aligns with the company’s focus on modernizing its fleet and improving operational efficiency.

Ranger’s return on invested capital has improved from 6% in Q2 2024 to 8% in Q2 2025, reflecting the company’s emphasis on capital efficiency and quality programs. Management presented the following investment thesis highlighting the company’s attractive free cash flow generation and dynamic business model:

The Q2 2025 results represent a significant recovery from the challenging first quarter, where the company missed analyst expectations with an EPS of just $0.03 against a forecast of $0.25. The substantial improvement in net income, adjusted EBITDA, and free cash flow suggests that the operational challenges faced in Q1 2025, including extreme weather events and market uncertainty, have largely been addressed.

With its strong liquidity position, improving operational performance, and continued commitment to shareholder returns, Ranger Energy appears well-positioned to capitalize on opportunities in the energy services sector while maintaining its resilience through market cycles.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.