C3is Inc. closes $2 million registered direct offering

Introduction & Market Context

Raute Oyj (HEL:RAUTE), a global supplier of technology and services to the wood products industry, reported record-high quarterly EBITDA for Q1 2025 despite facing significant market challenges. The company presented its business review on May 7, 2025, highlighting strong operational execution that drove profitability improvements across its segments, even as order intake declined substantially.

The market responded cautiously to the mixed results, with Raute’s stock falling 7.06% to €15.8 following the announcement, reflecting investor concerns about the significant drop in order intake despite the impressive profitability metrics. The stock remains below its 52-week high of €17.4 but well above its 52-week low of €10.7.

Quarterly Performance Highlights

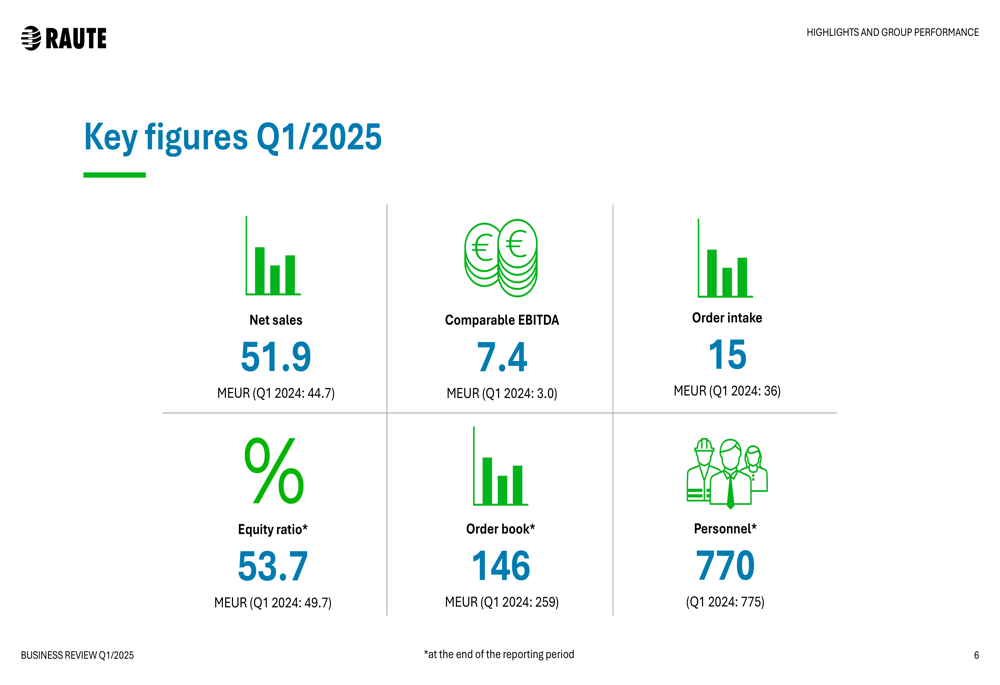

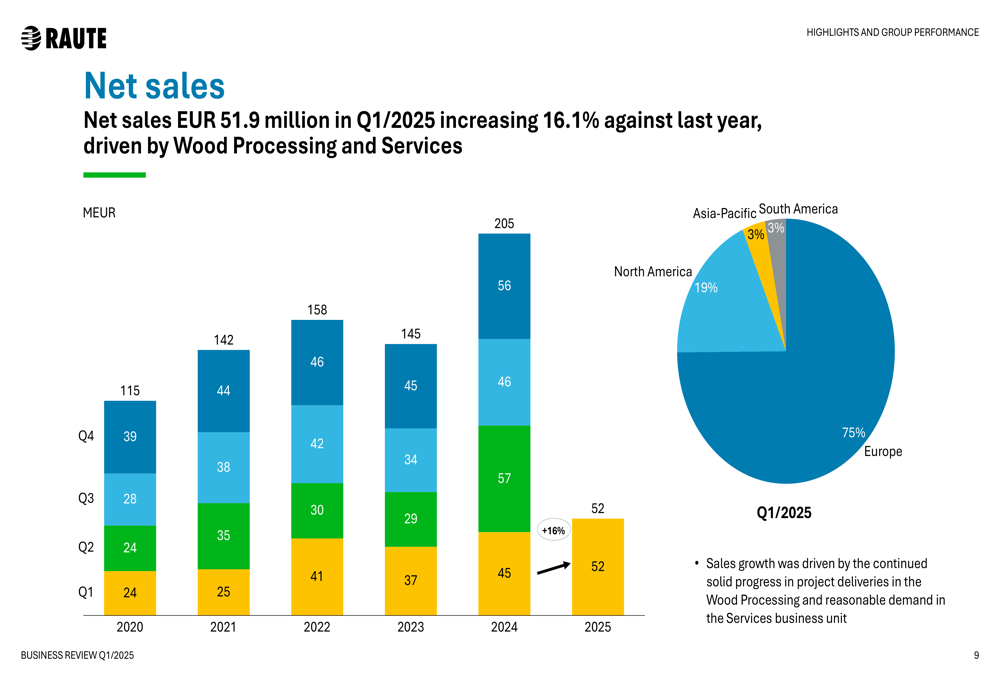

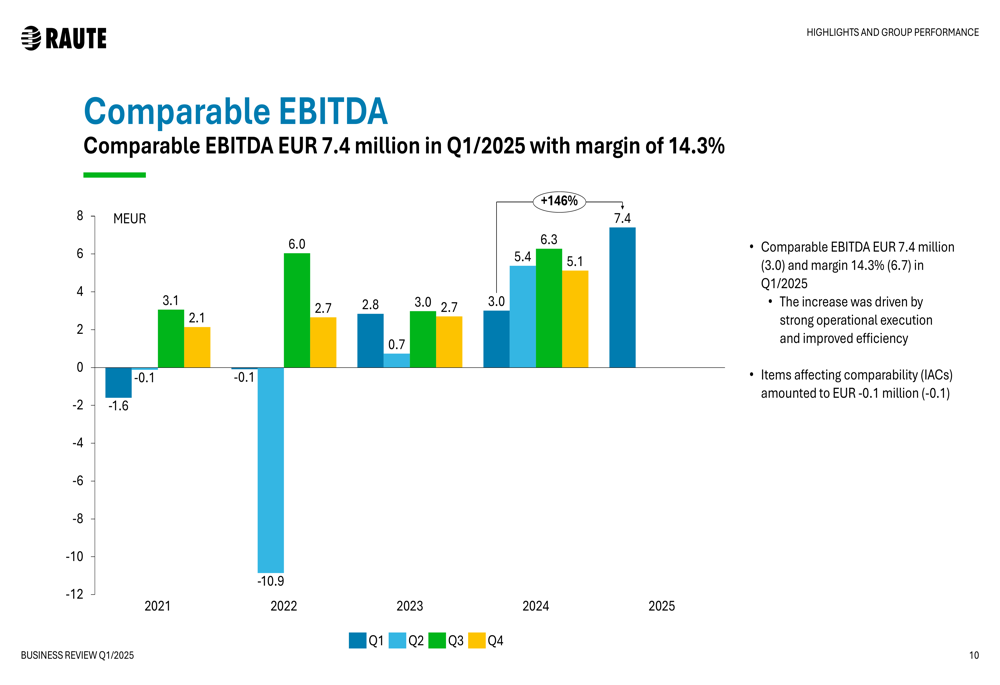

Raute achieved a comparable EBITDA of €7.4 million in Q1 2025, a significant increase from €3.0 million in Q1 2024, resulting in a margin improvement to 14.3% from 6.7%. Net sales grew to €51.9 million, up from €44.7 million in the same period last year.

As shown in the following chart of key Q1 2025 figures:

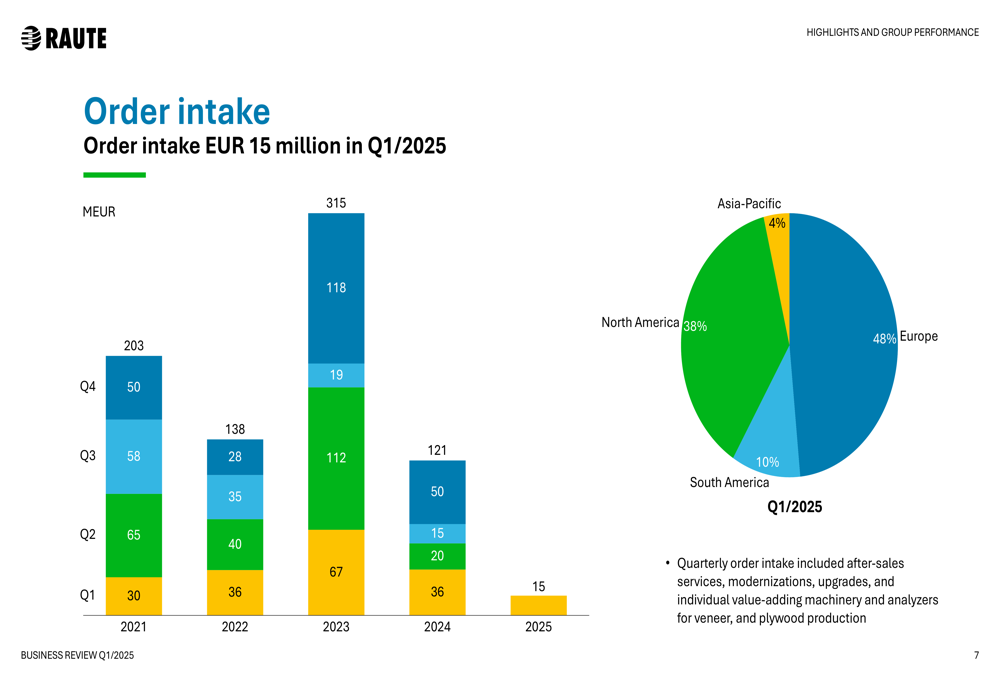

However, the company faced headwinds in new business generation, with order intake falling sharply to €15 million, compared to €36 million in Q1 2024. The order book stood at €146 million at the end of the quarter, significantly lower than the €259 million reported a year earlier.

The quarterly order intake trend reveals the challenging market environment Raute is navigating:

Despite the declining order intake, Raute delivered strong sales growth, with regional distribution heavily weighted toward Europe:

The company’s EBITDA performance has shown consistent improvement over recent quarters, reaching its highest level in Q1 2025:

Segment Performance Analysis

Raute’s operations are divided into three segments: Wood Processing, Services, and Analyzers, all of which showed revenue growth in Q1 2025.

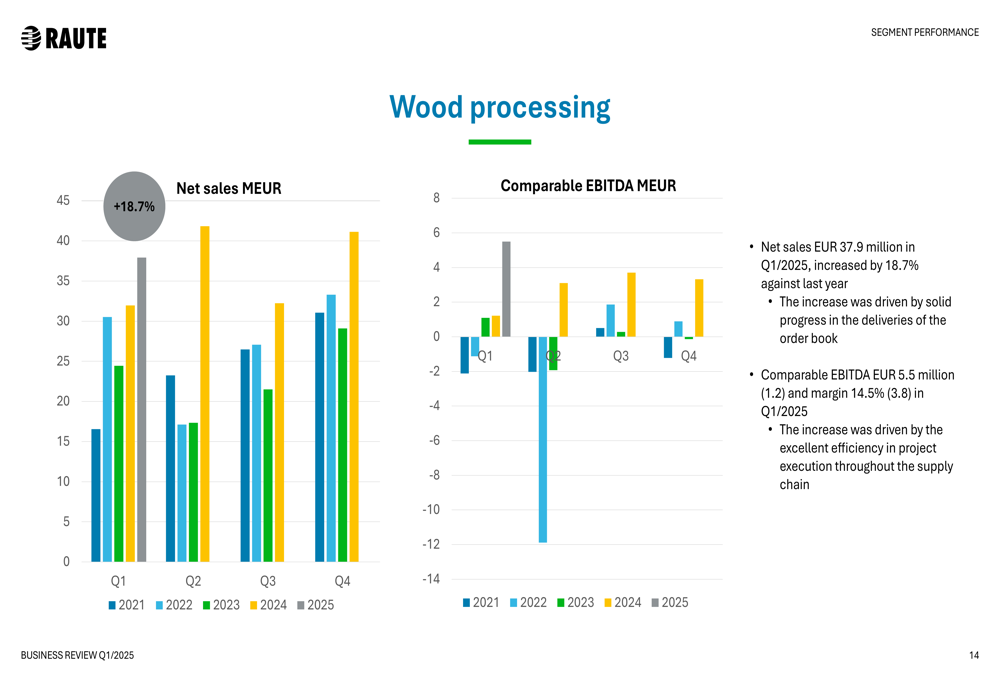

The Wood Processing segment, Raute’s largest business unit, delivered particularly strong results with net sales of €37.9 million, an 18.7% increase year-over-year. The segment’s comparable EBITDA surged to €5.5 million from €1.2 million in Q1 2024, with margin expanding to 14.5% from 3.8%. This improvement was attributed to excellent efficiency in project execution throughout the supply chain.

The segment’s performance is illustrated in the following chart:

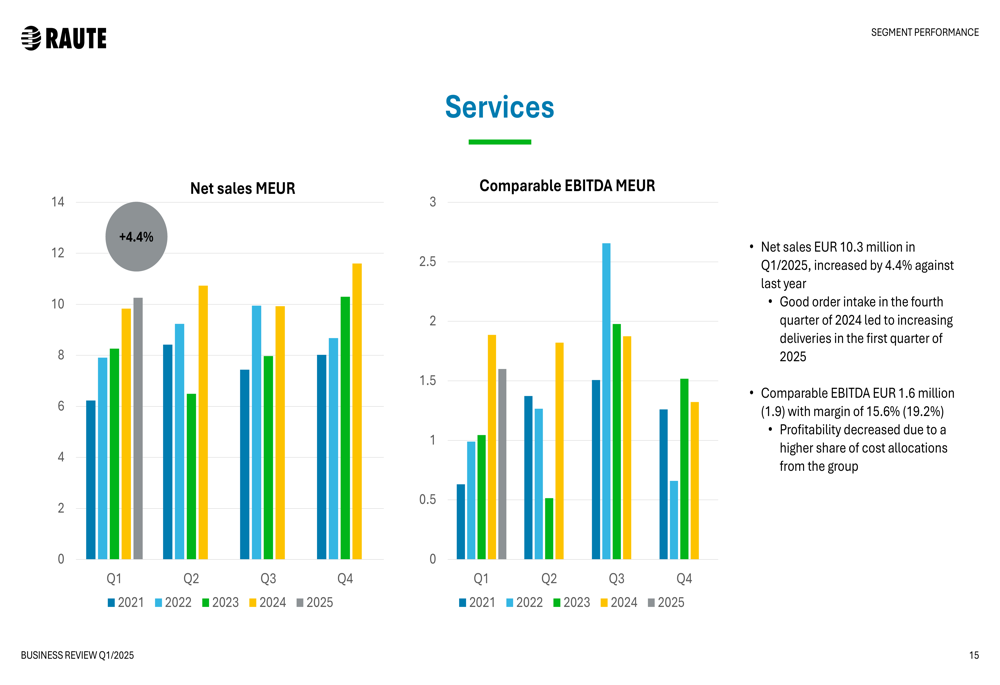

The Services segment reported modest growth with net sales of €10.3 million, up 4.4% from Q1 2024. However, its comparable EBITDA decreased to €1.6 million from €1.9 million, with margin contracting to 15.6% from 19.2%. The company explained that the profitability decrease was due to a higher share of cost allocations from the group.

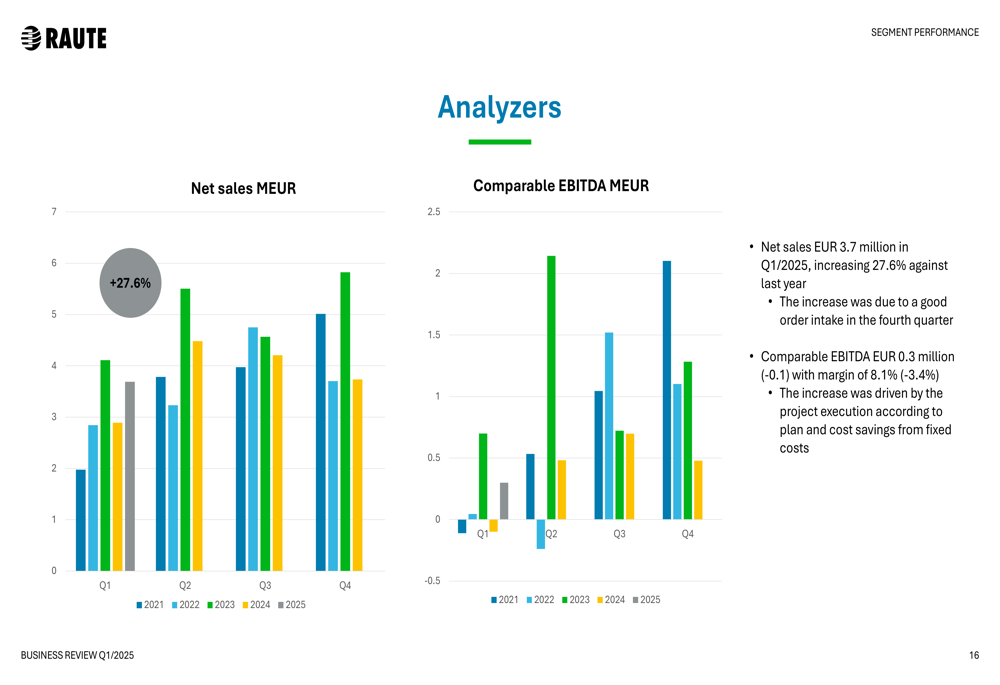

The Analyzers segment showed the strongest relative growth, with net sales increasing 27.6% to €3.7 million. The segment turned profitable with a comparable EBITDA of €0.3 million, compared to a loss of €0.1 million in Q1 2024, achieving a margin of 8.1%. This improvement was driven by better project execution and cost savings from fixed costs.

Financial Position and Cash Flow

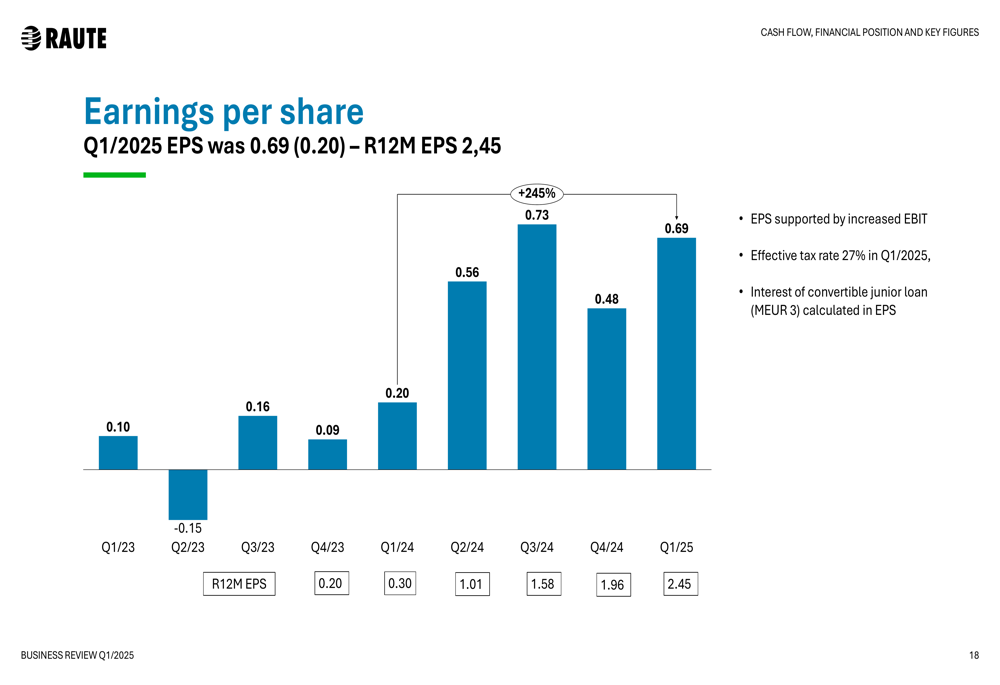

Raute’s earnings per share increased significantly to €0.69 in Q1 2025, supported by improved EBIT performance:

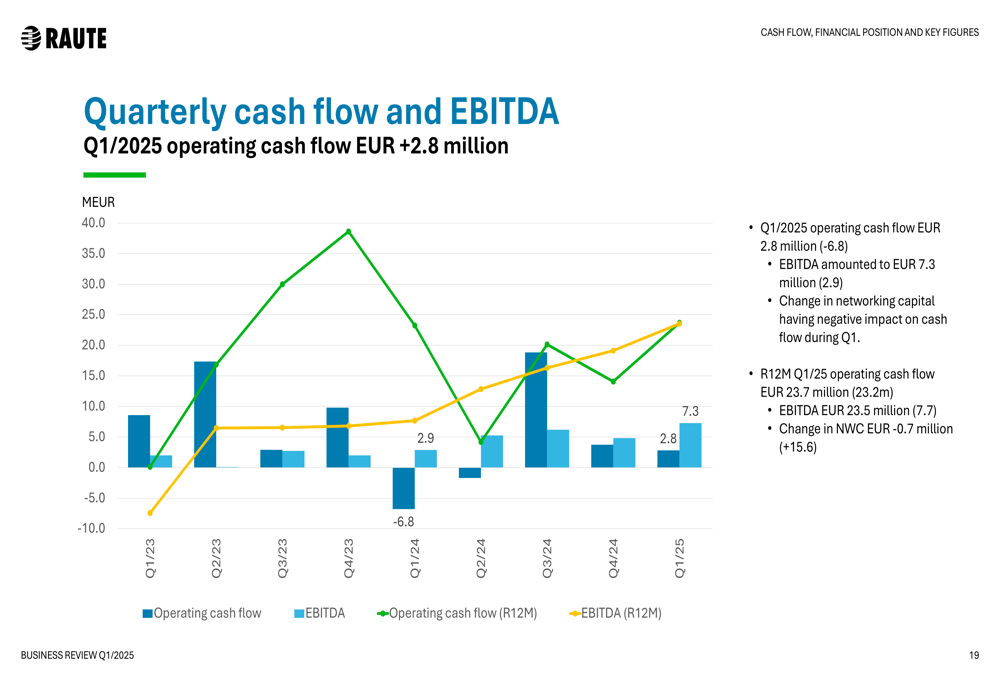

The company generated a positive operating cash flow of €2.8 million in Q1 2025, a substantial improvement from the negative €6.8 million in Q1 2024. This improvement came despite the strong EBITDA of €7.3 million being partially offset by negative changes in working capital.

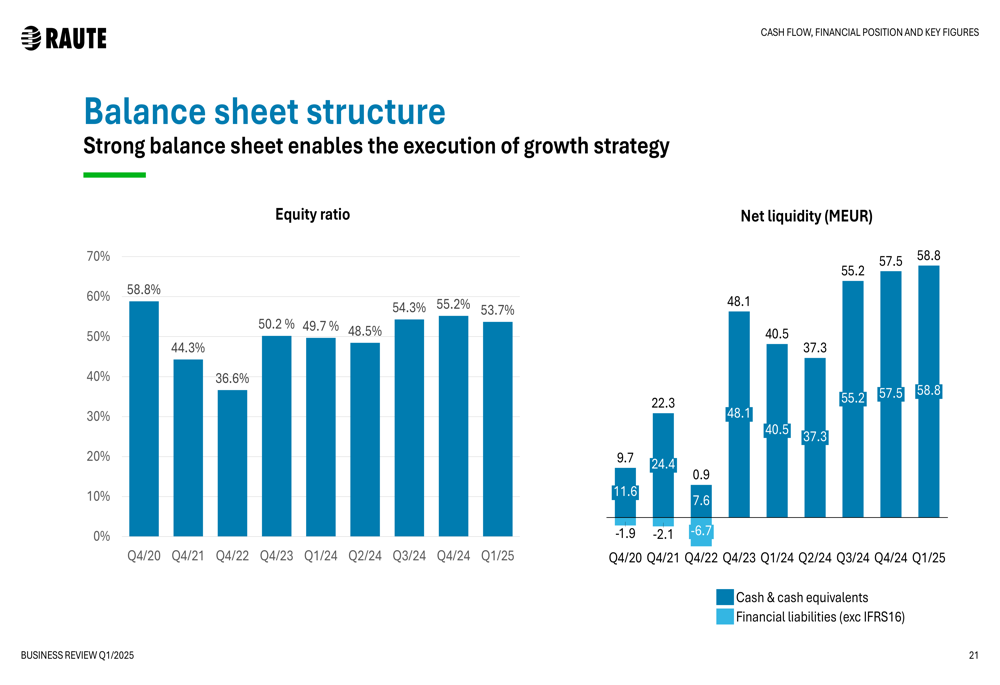

Raute maintained a strong balance sheet with an equity ratio of approximately 59% and net liquidity of €58.8 million at the end of Q1 2025. The company emphasized that this strong financial position enables the execution of its growth strategy, potentially including mergers and acquisitions.

Outlook and Guidance

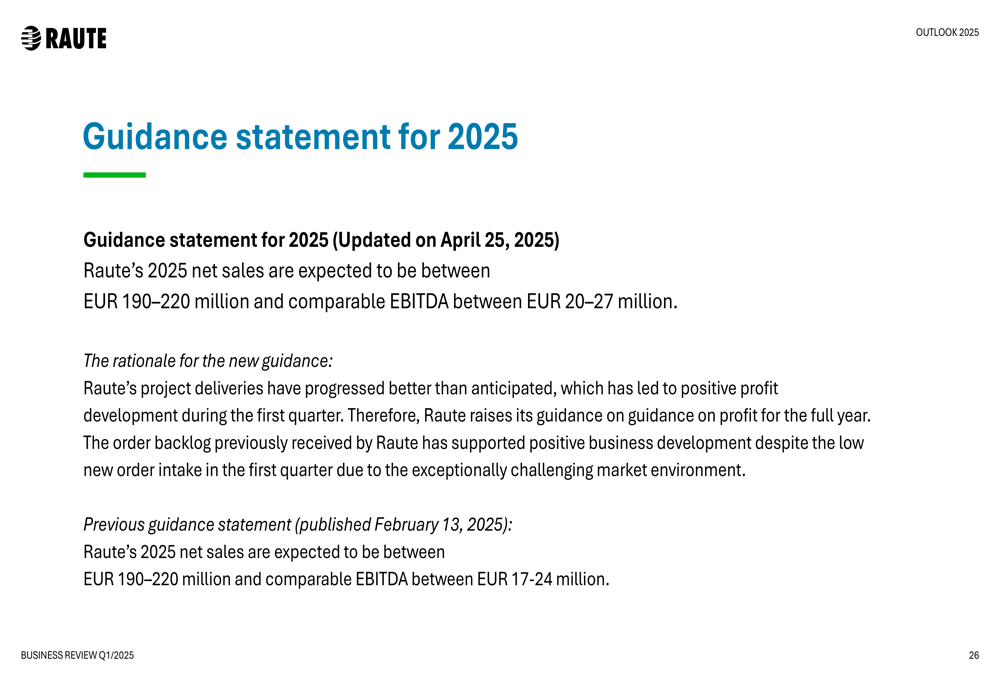

Raute’s management provided an updated outlook for 2025, noting that the global investment sentiment remains cautious, particularly in the wood products industry. The company indicated that a wider recovery in its markets appears to be postponed until the latter part of 2025.

Despite these challenges, Raute raised its guidance for 2025, now expecting comparable EBITDA between €20-27 million, up from the previous guidance of €17-24 million. Net sales expectations remained unchanged at €190-220 million.

CEO Mika Saariaho expressed confidence in the company’s ability to deliver strong results for the full year 2025, citing better-than-anticipated progress in project deliveries as the key driver behind the positive profit development in the first quarter.

Market Reaction

Despite the record EBITDA and raised guidance, Raute’s stock price fell 7.06% following the earnings announcement. This decline likely reflects investor concerns about the significant drop in order intake and the broader market uncertainties affecting the construction sector.

According to available market data, Raute maintains impressive gross profit margins of 49.84% and has demonstrated strong revenue growth of 40.69% over the last twelve months. The stock is trading at a P/E ratio of 7.93x, suggesting potential undervaluation despite the recent market challenges.

The contrast between Raute’s strong operational performance and the market’s cautious reaction highlights the tension between the company’s current profitability and concerns about future revenue streams given the declining order book. As Raute navigates these challenges, investors will be closely watching order intake trends in upcoming quarters for signs of market recovery.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.